Trump to impose 100% tariff on China starting November 1

Introduction & Market Context

Arthur J. Gallagher & Co . (NYSE:AJG) released its Q2 2025 CFO Commentary presentation on July 31, highlighting the company’s financial performance and strategic initiatives. The insurance broker continues to demonstrate resilience with strong adjusted margins despite facing some revenue headwinds. The presentation comes after the company reported its 20th consecutive quarter of double-digit growth in Q1 2025, setting expectations for continued momentum.

In aftermarket trading following the presentation, AJG shares fell 3.79% to $275.02, reflecting investor concerns despite the company’s generally positive outlook. This reaction appears more pronounced than the modest 0.34% decline seen after the Q1 earnings release.

Quarterly Performance Highlights

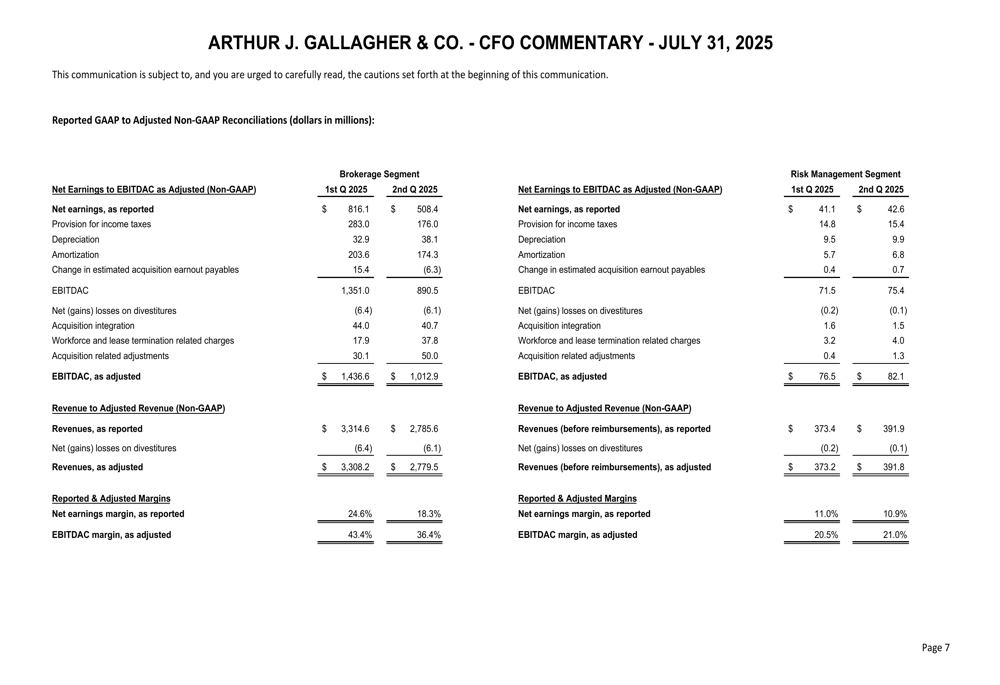

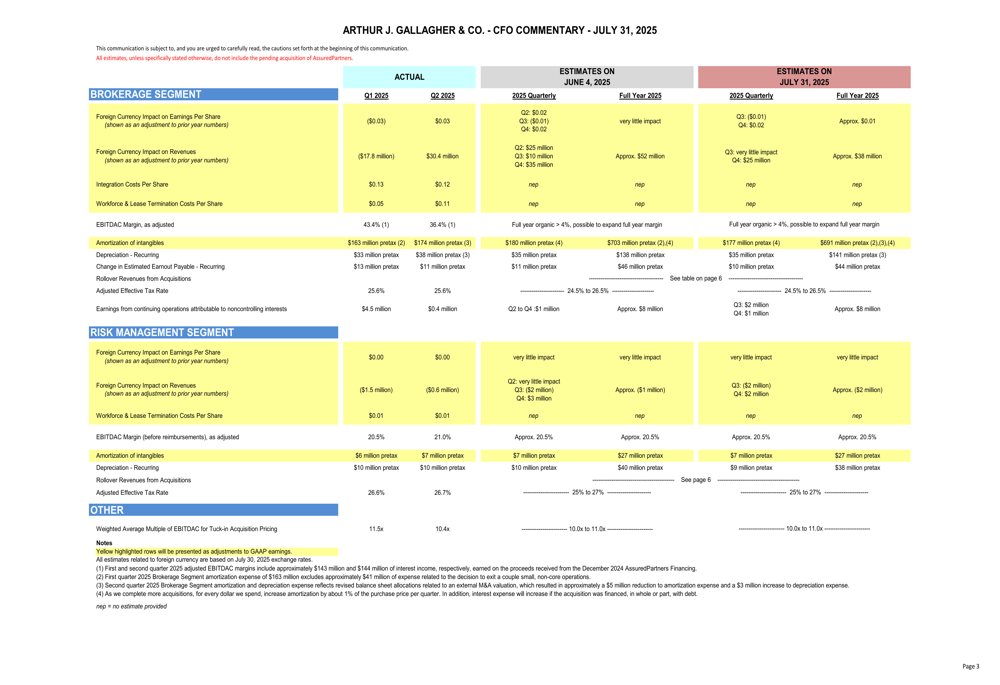

Gallagher’s Q2 2025 results show solid adjusted EBITDAC margins across its business segments, though with expected seasonal variations from Q1. The Brokerage segment posted a 36.4% adjusted EBITDAC margin in Q2, down from 43.4% in Q1, while the Risk Management segment improved to 21.0% in Q2 from 20.5% in Q1.

As shown in the following detailed reconciliation of GAAP to non-GAAP measures:

The company’s margin performance remains a bright spot, consistent with the Q1 earnings report that highlighted a 41.1% adjusted EBITDAC margin, up 338 basis points year-over-year. This trend of margin expansion appears to be continuing into Q2, though with expected seasonal fluctuations.

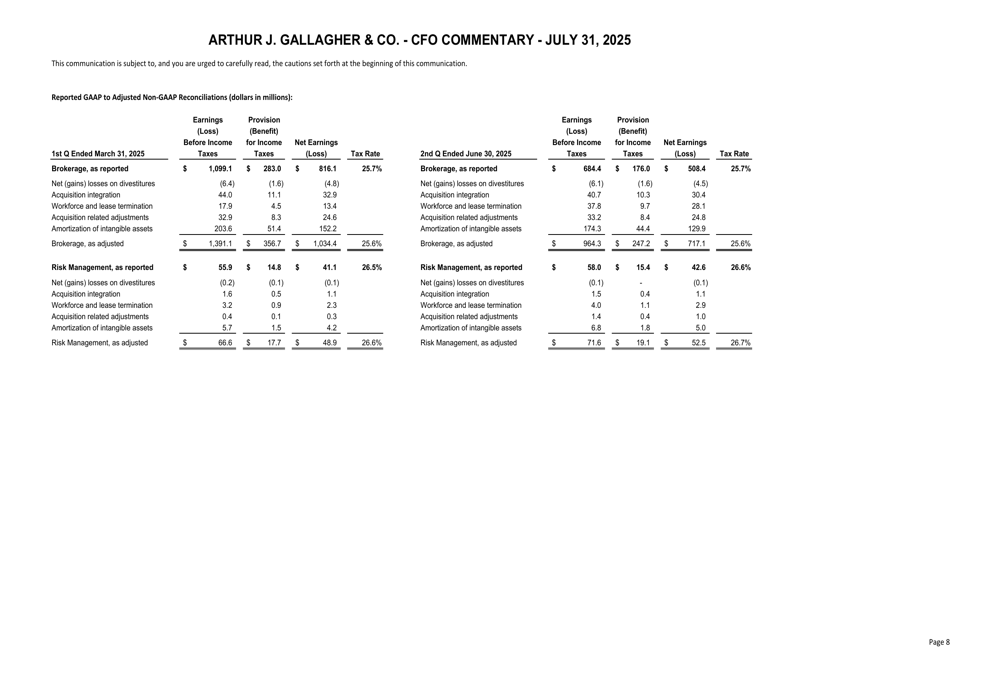

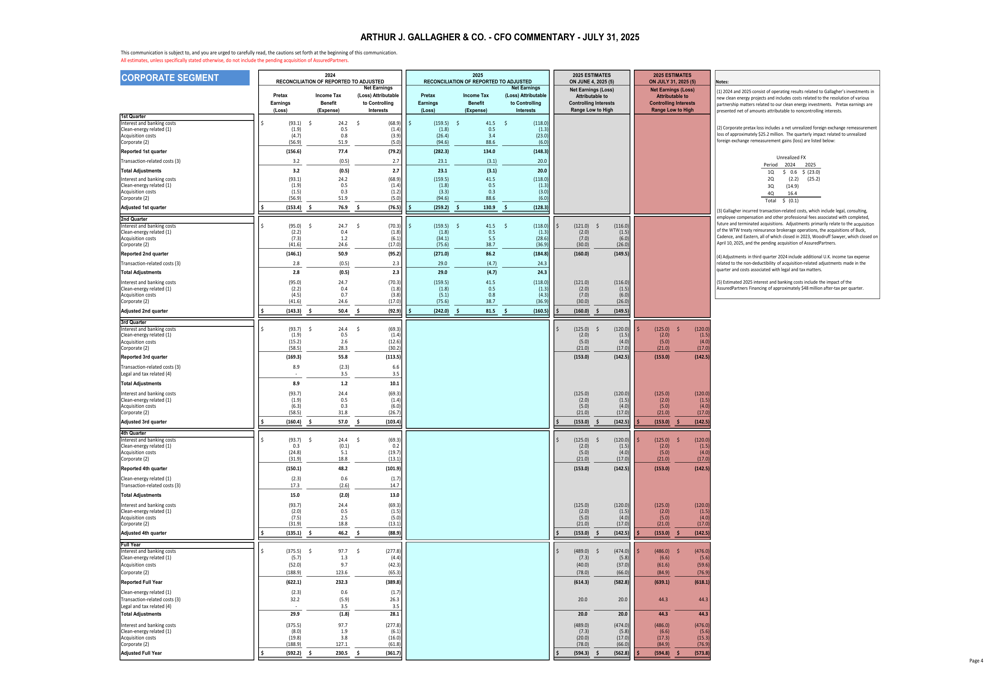

The presentation also provides a comprehensive breakdown of earnings before income taxes for both major segments:

Tax rates have remained stable across segments, with the Brokerage segment at 25.7% and the Risk Management segment at 26.6% in Q2 2025, providing consistency in after-tax earnings calculations.

Acquisition Strategy and Impact

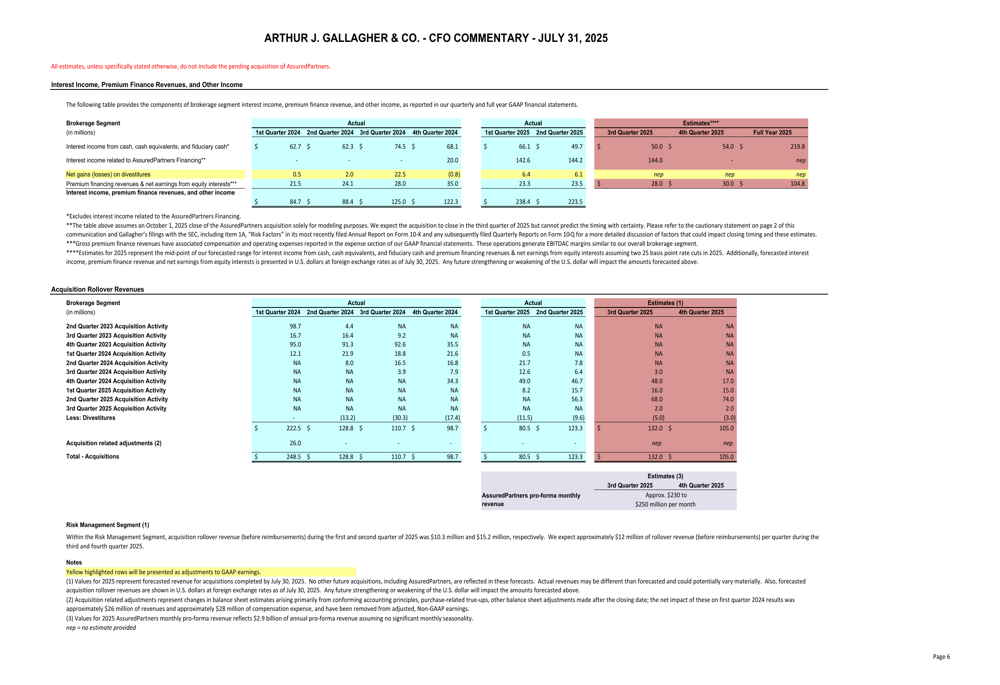

Gallagher’s acquisition strategy continues to be a major growth driver, with significant rollover revenues from recent acquisitions. The company reported acquisition rollover revenues of $80.5 million in Q1 2025 and $123.3 million in Q2 2025 for the Brokerage segment.

The presentation provides particular insight into the Assured Partners acquisition, estimating pro-forma monthly revenue between $230-250 million in the third and fourth quarters of 2025:

This acquisition activity aligns with CEO J. Patrick Gallagher Jr.’s comments from the Q1 earnings call that the company is transforming into one with "more large accounts, stronger platforms, better sales tools." The company completed 11 tuck-in mergers in Q1 alone, and the acquisition momentum appears to be continuing.

Clean Energy Investments

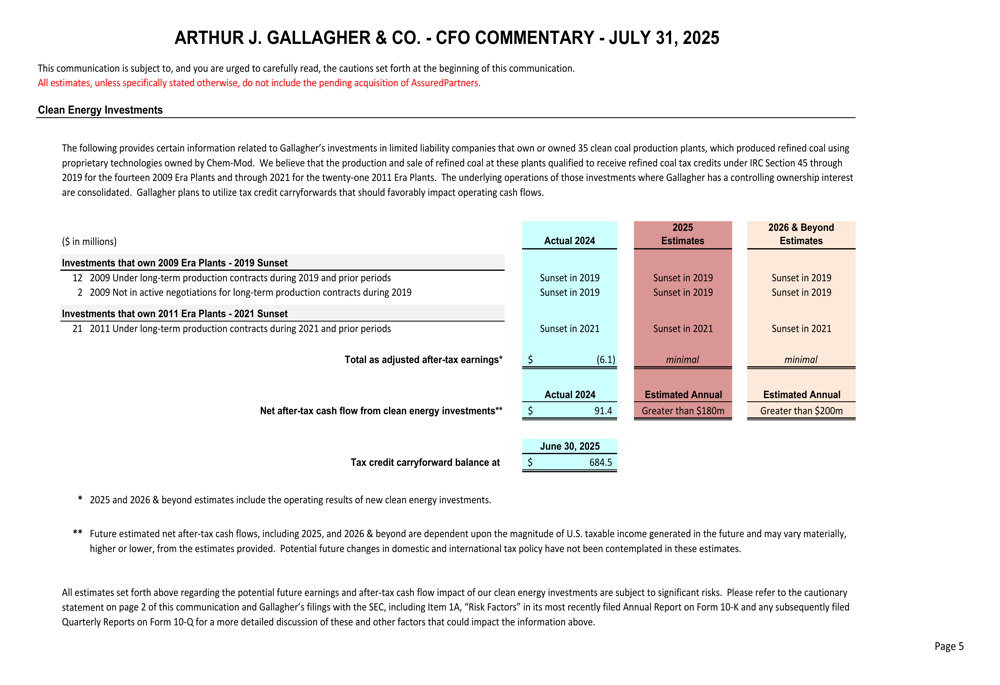

A notable strategic focus highlighted in the presentation is Gallagher’s clean energy investment portfolio. The company expects significant cash flow generation from these investments, with estimated annual net after-tax cash flow exceeding $180 million in 2025 and growing to over $200 million in 2026 and beyond.

The presentation details the current status of these investments:

With a tax credit carryforward balance of $684.5 million as of June 30, 2025, these investments represent a significant long-term value driver for Gallagher, though they remain dependent on future taxable income and potential changes in tax policy.

Forward Guidance

The CFO Commentary provides detailed estimates for the remainder of 2025, including segment-specific projections for Q3, Q4, and full-year results. The company expects continued strong performance in both its Brokerage and Risk Management segments.

The following table outlines these detailed projections:

Foreign currency impact is estimated at approximately $52 million for the full year, an important factor for a company with significant international operations. The presentation also includes detailed corporate segment reconciliations:

These forward-looking estimates align with the company’s previously stated goal of 6-8% organic growth in its brokerage segment for 2025, as mentioned in the Q1 earnings call.

Market Reaction

Despite the generally positive outlook presented in the CFO Commentary, Gallagher’s stock faced pressure in aftermarket trading, dropping 3.79% to $275.02. This places the stock near the lower end of its 52-week range of $274.25-$351.23, suggesting investor concerns about growth sustainability or integration challenges with recent acquisitions.

The market reaction appears more severe than after the Q1 earnings report, which saw only a modest 0.34% decline despite a slight revenue miss. This could indicate growing investor caution about Gallagher’s ability to maintain its growth trajectory while successfully integrating major acquisitions like Assured Partners.

The presentation’s detailed reconciliations of non-GAAP measures highlight the company’s focus on adjusted metrics, which have consistently shown strength even when GAAP results face challenges. This approach has been a hallmark of Gallagher’s financial reporting strategy.

As the company moves into the second half of 2025, investors will be watching closely to see if the projected margins and acquisition synergies materialize as expected, particularly given the significant investments in both acquisitions and clean energy initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.