5 big analyst AI moves: Nvidia, AMD upgraded; ASML seen on €1,000 path

Introduction & Market Context

Asahi Co., Ltd. (TSE:3333) presented its financial results for the fiscal year ended February 20, 2025, on April 4, 2025, highlighting record-breaking sales performance and significant growth in its e-commerce and electric bicycle segments. The bicycle retailer has achieved consecutive record highs in net sales since its listing in 2004, with its market share increasing from 24% to 25% during the fiscal year.

The company has successfully navigated market changes, including a lengthening replacement cycle for bicycles and growing demand for electric-assist models, by strengthening its omnichannel approach that merges online and offline operations (OMO) and enhancing customer relationship management (CRM).

Financial Performance Highlights

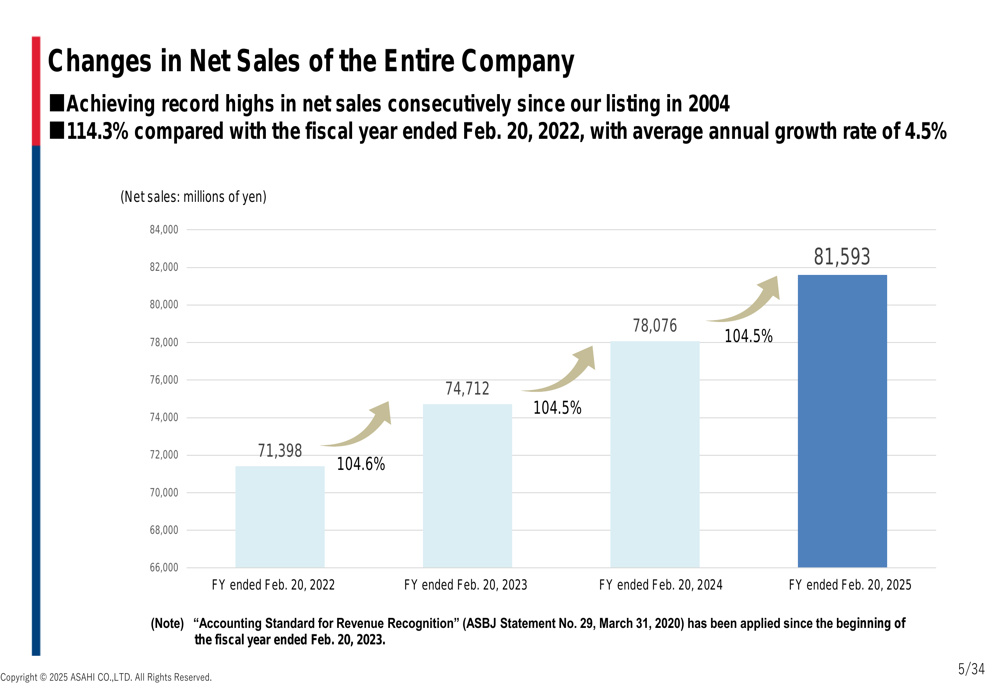

Asahi reported net sales of ¥81,593 million for the fiscal year ended February 20, 2025, representing a 4.5% increase year-over-year. The company has maintained a consistent annual growth rate of 4.5% over recent years, demonstrating stable expansion in a competitive market.

As shown in the following chart of net sales growth over the past four years:

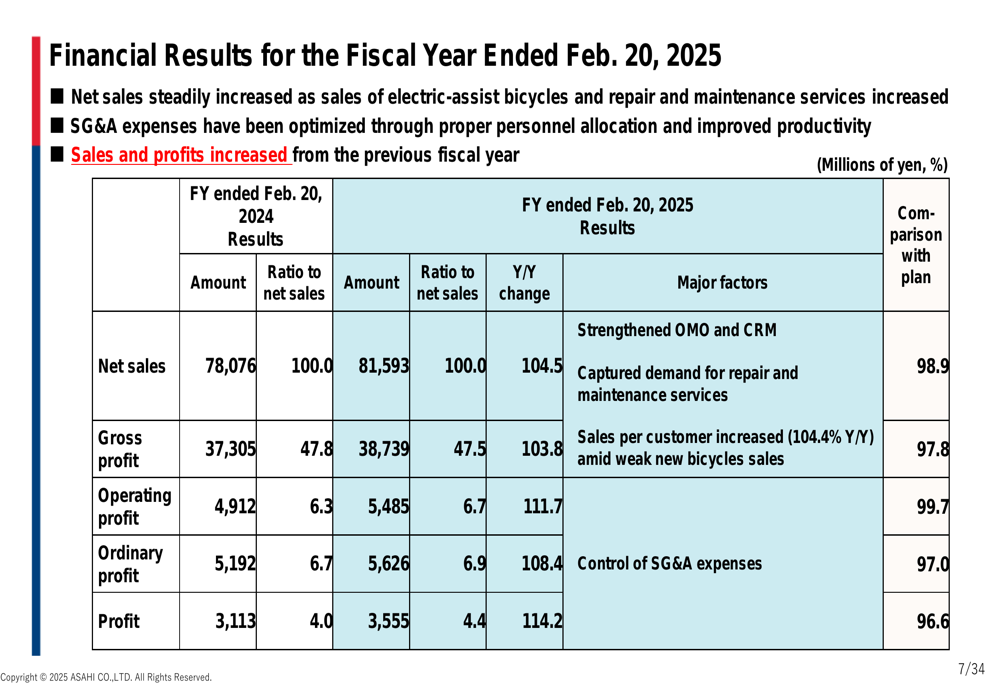

Operating profit rose to ¥5,485 million, an 11.7% increase from the previous year, while ordinary profit grew 8.4% to ¥5,626 million. Net profit showed the strongest growth at 14.2%, reaching ¥3,555 million. The operating profit margin improved from 6.3% to 6.7%, indicating enhanced operational efficiency.

The detailed financial results, including comparisons with the previous fiscal year and the company’s plan, are presented in this comprehensive table:

While net sales fell slightly short of the company’s plan (98.9% of target), operating profit nearly matched expectations at 99.7% of the planned figure. The company attributed the shortfall in sales to specific challenges in the second half of the fiscal year, including the impact of typhoons in September, temporary inventory adjustments in November, and heavy snow in February.

Growth Drivers Analysis

Asahi’s growth was primarily driven by two key segments: e-commerce and electric-assist bicycles. E-commerce sales surged 23.1% to ¥12,705 million, increasing its share of retail sales from 13.6% to 16.0%. Meanwhile, electric-assist bicycle sales grew 10.1% to ¥23,278 million, representing 28.5% of total sales.

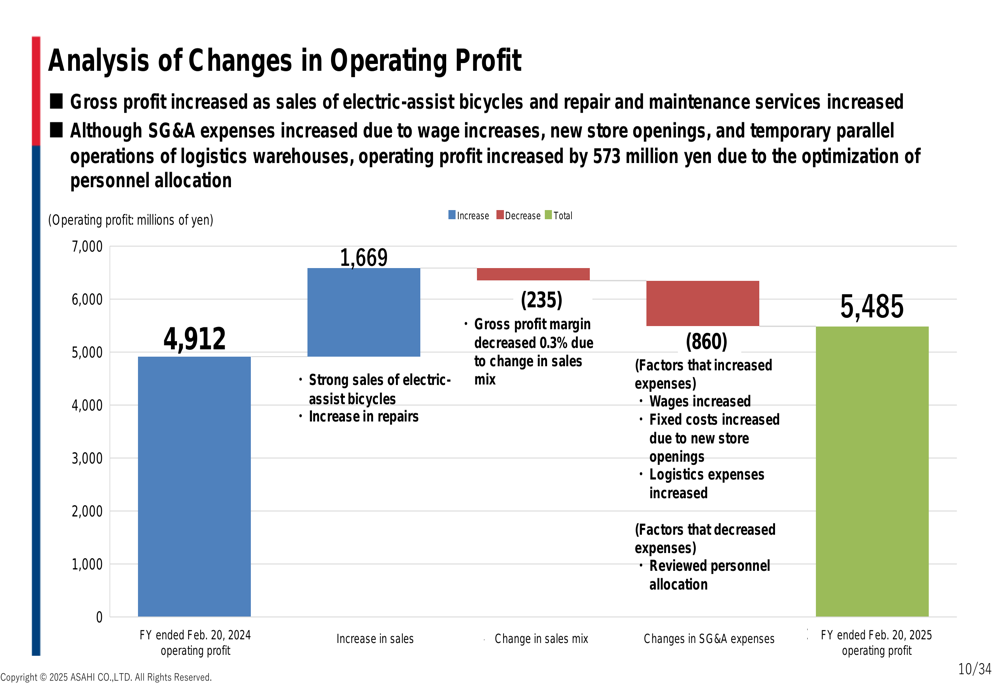

The following waterfall chart illustrates the factors contributing to the company’s operating profit growth:

The increase in sales contributed ¥1,669 million to operating profit, primarily from strong sales of electric-assist bicycles and increased repair services. This was partially offset by a slight decrease in gross profit margin due to changes in sales mix (¥235 million impact) and increased SG&A expenses (¥860 million impact).

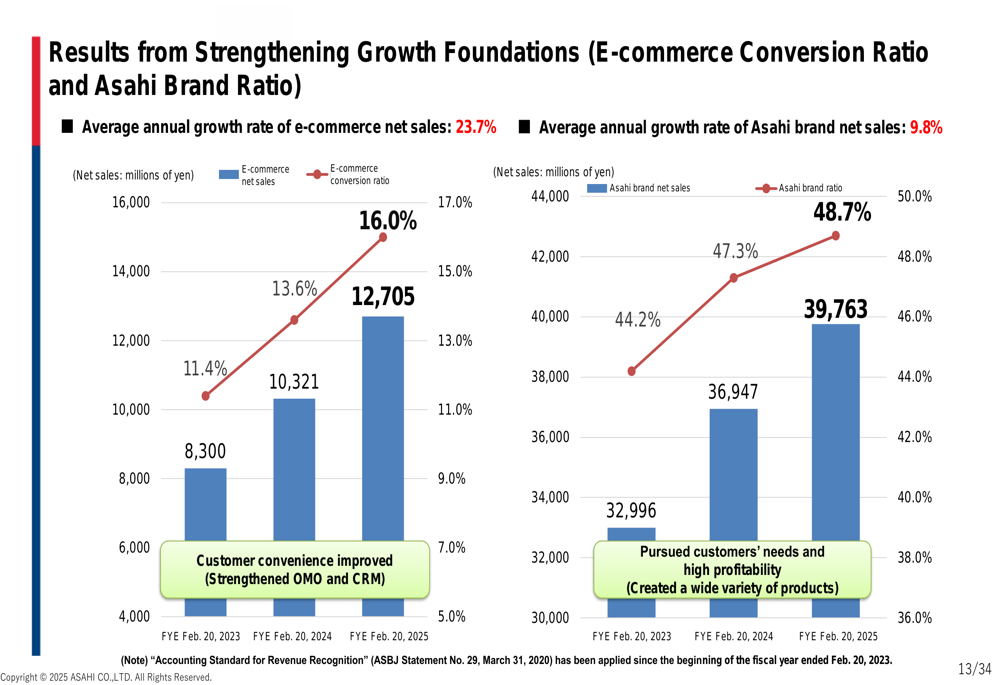

Asahi has been strengthening its growth foundations by expanding both e-commerce and its private label products. The company’s e-commerce conversion ratio and Asahi brand ratio have shown consistent improvement over the past three years:

The e-commerce segment has achieved an impressive average annual growth rate of 23.7%, while Asahi brand products have grown at an average annual rate of 9.8%. The increasing share of private label products has helped the company improve its gross margins and differentiate its offerings in the market.

Strategic Initiatives

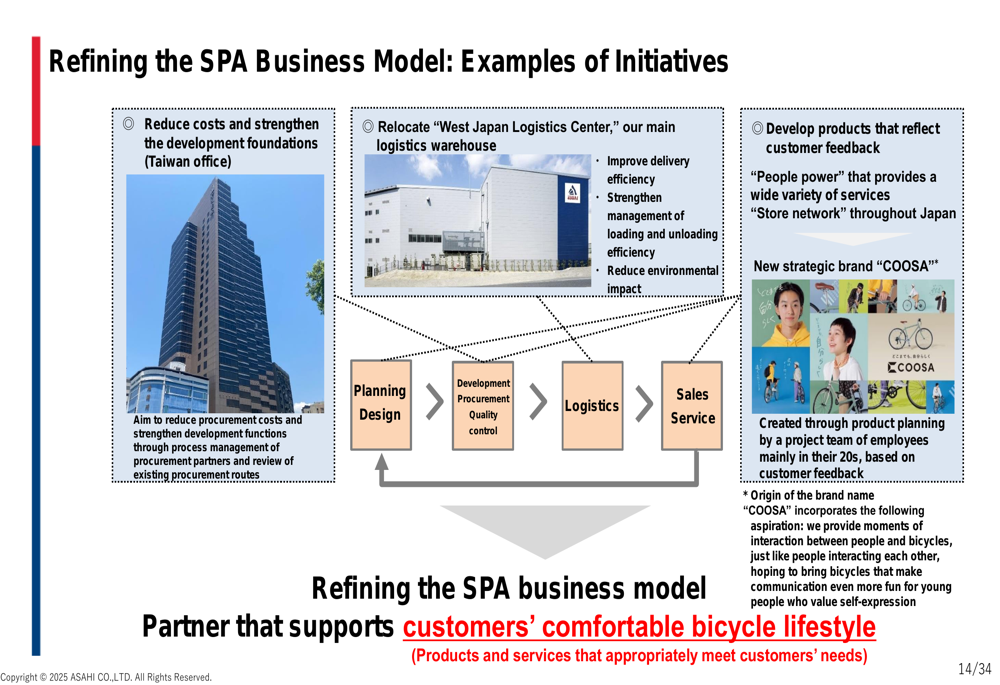

Asahi continues to refine its SPA (Specialty store retailer of Private label Apparel) business model, focusing on developing products that reflect customer feedback. The company has established a Taiwan office to reduce costs and strengthen development capabilities, relocated its West Japan Logistics Center, and created a new strategic brand called "COOSA."

The company’s integrated approach to product development is illustrated in this diagram:

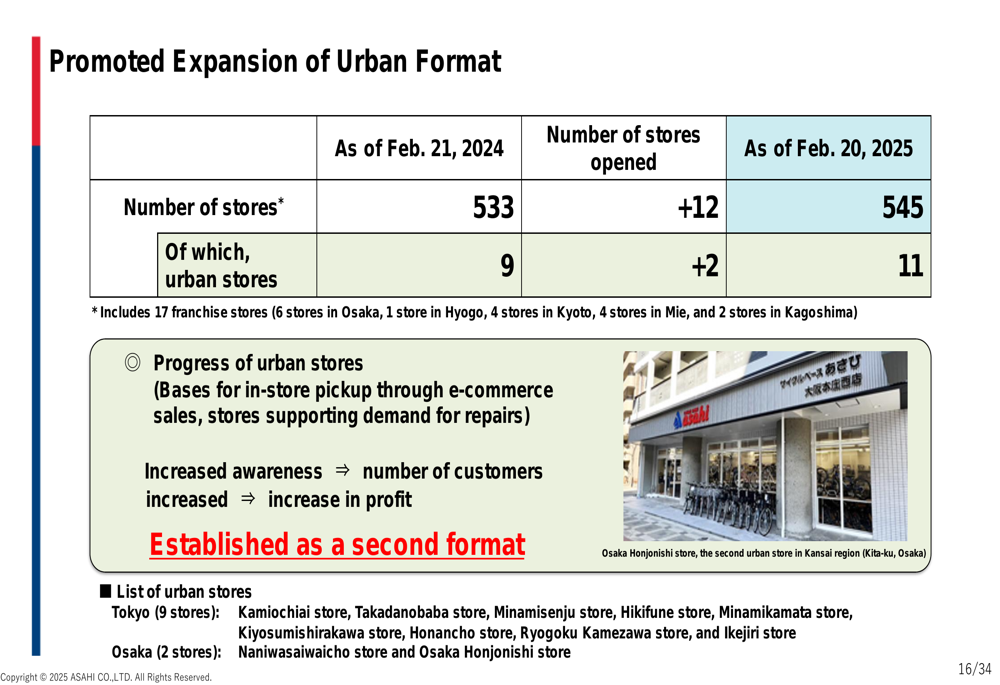

Store expansion remains a key part of Asahi’s strategy, with a particular focus on urban format stores that serve as bases for in-store pickup of e-commerce orders and repair services. As of February 20, 2025, the company operated 545 stores, including 11 urban stores and 17 franchise locations.

The urban store expansion strategy is detailed in this slide:

These urban stores have helped increase brand awareness, attract more customers, and ultimately drive profit growth by supporting the company’s omnichannel approach.

Forward-Looking Statements

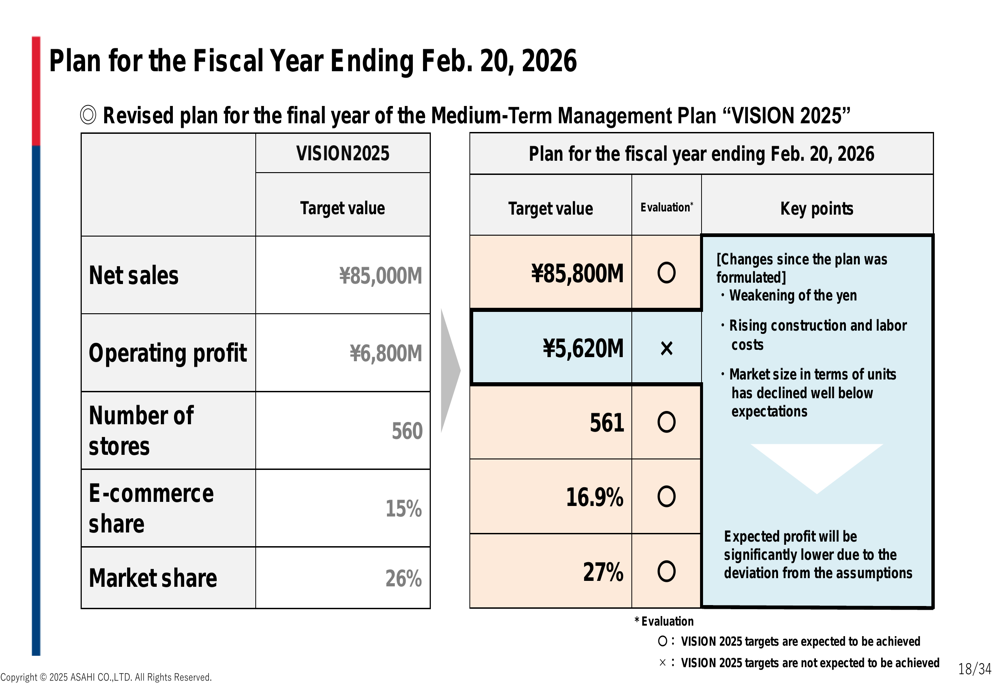

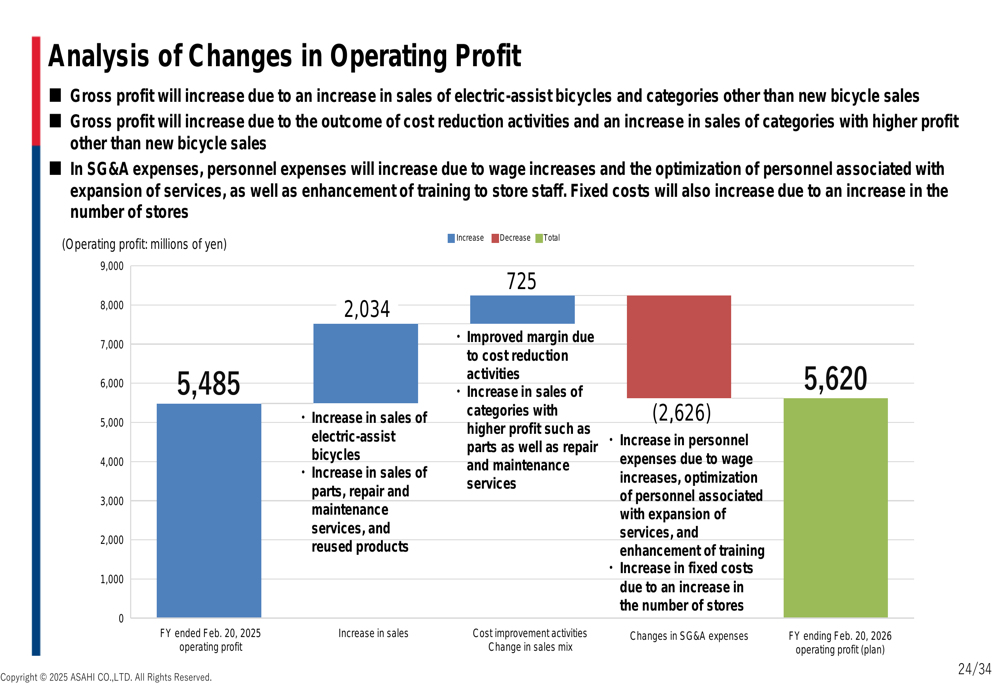

For the fiscal year ending February 20, 2026, Asahi has revised its targets for the final year of its Medium-Term Management Plan "VISION 2025." The company now expects net sales of ¥85,800 million (up from the original target of ¥85,000 million) and operating profit of ¥5,620 million (down from the original target of ¥6,800 million).

The revised plan compared to the original VISION 2025 targets is presented here:

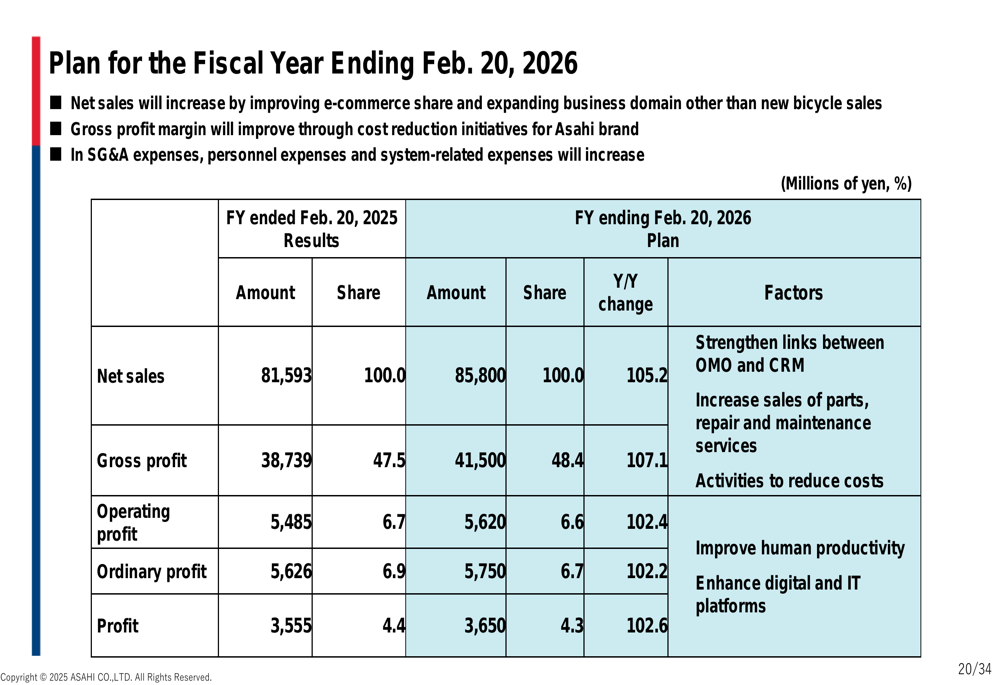

The company’s financial plan for FY 2026 projects a 5.2% increase in net sales and a 2.4% increase in operating profit:

The planned improvement in operating profit is broken down in this analysis:

While increased sales are expected to contribute ¥2,034 million to operating profit and cost improvement activities should add another ¥725 million, these gains will be largely offset by a ¥2,626 million increase in SG&A expenses, resulting in a modest net increase of ¥135 million in operating profit.

Asahi expects to continue growing its e-commerce share to 16.9% in FY 2026 and increasing its market share to 27%. The company will focus on strengthening links between its OMO and CRM strategies to improve customer lifetime value, while also enhancing its expertise in repair and maintenance services to capitalize on the trend toward longer bicycle ownership cycles.

As the bicycle market continues to evolve, with electric-assist models gaining popularity and consumers keeping their bicycles longer, Asahi appears well-positioned to leverage its omnichannel approach and strong brand presence to maintain its growth trajectory in the coming fiscal year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.