Fubotv earnings beat by $0.10, revenue topped estimates

Ashland Global Holdings Inc (NYSE:ASH) presented its third-quarter fiscal year 2025 results on July 30, highlighting sales declines across all segments but demonstrating margin resilience through disciplined cost management and portfolio optimization. The specialty materials company narrowed its full-year outlook while accelerating restructuring initiatives to counter ongoing market challenges.

Quarterly Performance Highlights

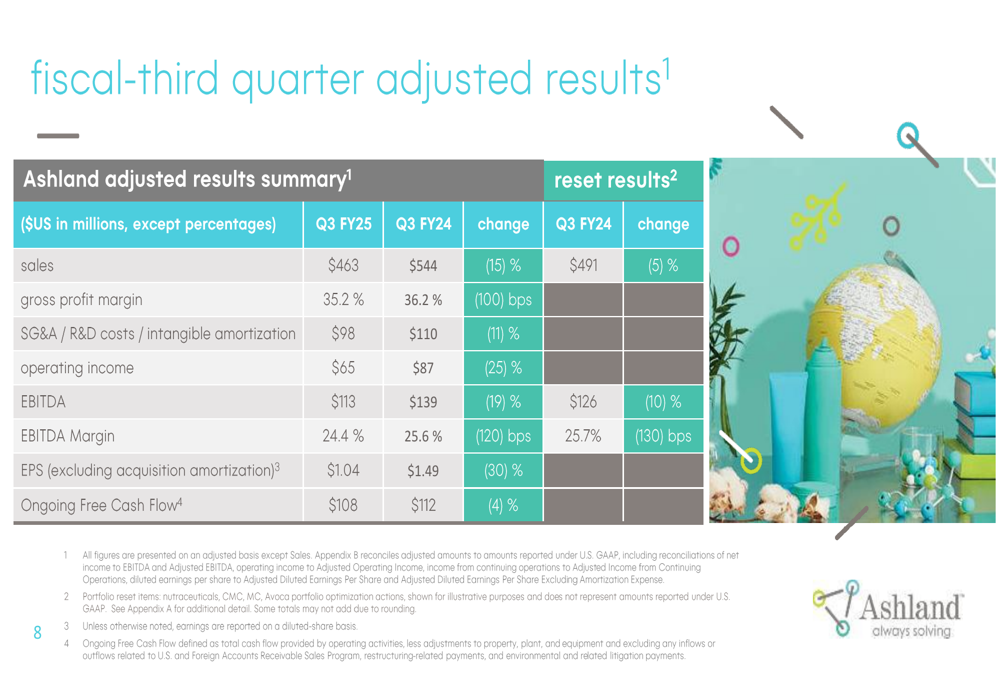

Ashland reported Q3 sales of $463 million, down 15% compared to the prior-year quarter, with adjusted EBITDA of $113 million, a 19% decrease. Despite these declines, the company maintained a healthy adjusted EBITDA margin of 24.4%, down 120 basis points year-over-year. Adjusted earnings per share fell 30% to $1.04, while ongoing free cash flow remained relatively stable at $108 million, down just 4%.

As shown in the following comprehensive financial summary:

The company attributed the sales decline to portfolio optimization efforts, lower volumes in Specialty Additives and Personal Care segments, and moderately lower pricing. When accounting for portfolio reset actions, the sales decline was a more modest 5% year-over-year.

"Our ability to sustain strong margins across segments demonstrates the effectiveness of our disciplined execution and strategic portfolio actions," noted Guillermo Novo, Chair and CEO, during the earnings call.

Segment Performance

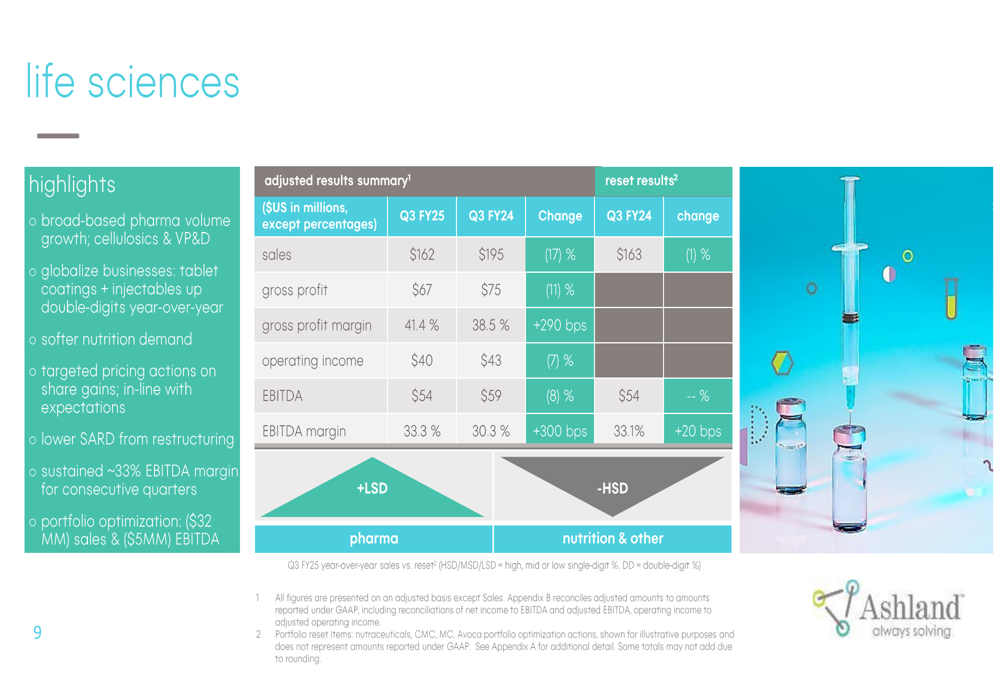

Life Sciences emerged as the strongest performer among Ashland’s business units, maintaining a robust 33.3% EBITDA margin despite a 17% sales decline to $162 million. The segment benefited from broad-based pharmaceutical volume growth, particularly in tablet coatings and injectables, which saw double-digit year-over-year increases.

The following segment breakdown illustrates Life Sciences’ performance:

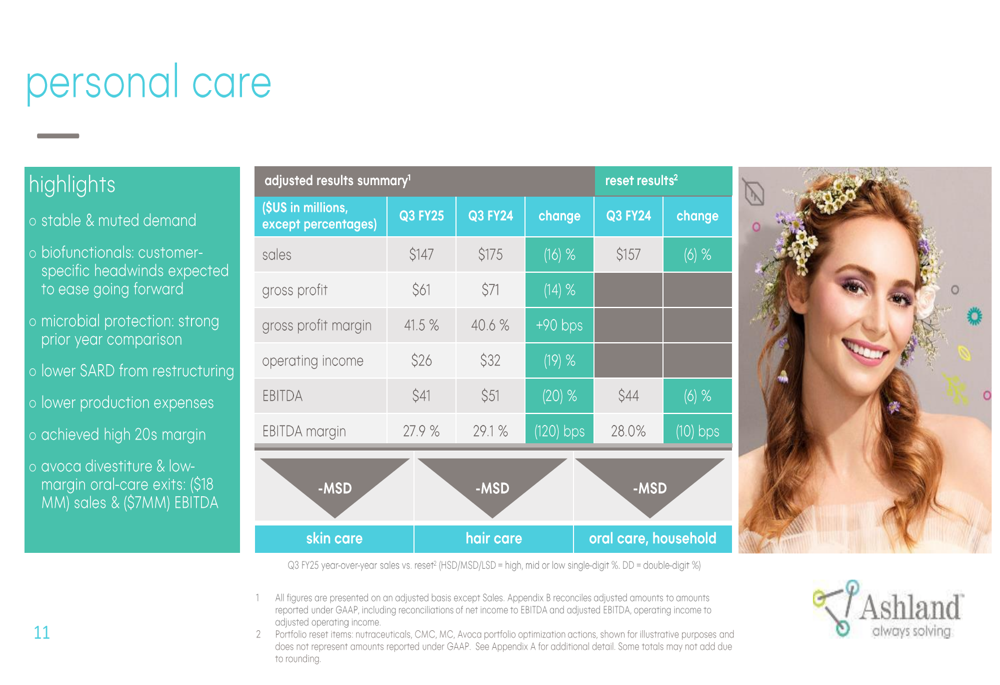

Personal Care reported sales of $147 million, down 16% year-over-year, with an EBITDA margin of 27.9%. The segment faced customer-specific headwinds in biofunctionals, though these are expected to ease going forward. The Avoca divestiture and exit from low-margin oral-care products impacted sales by approximately $18 million.

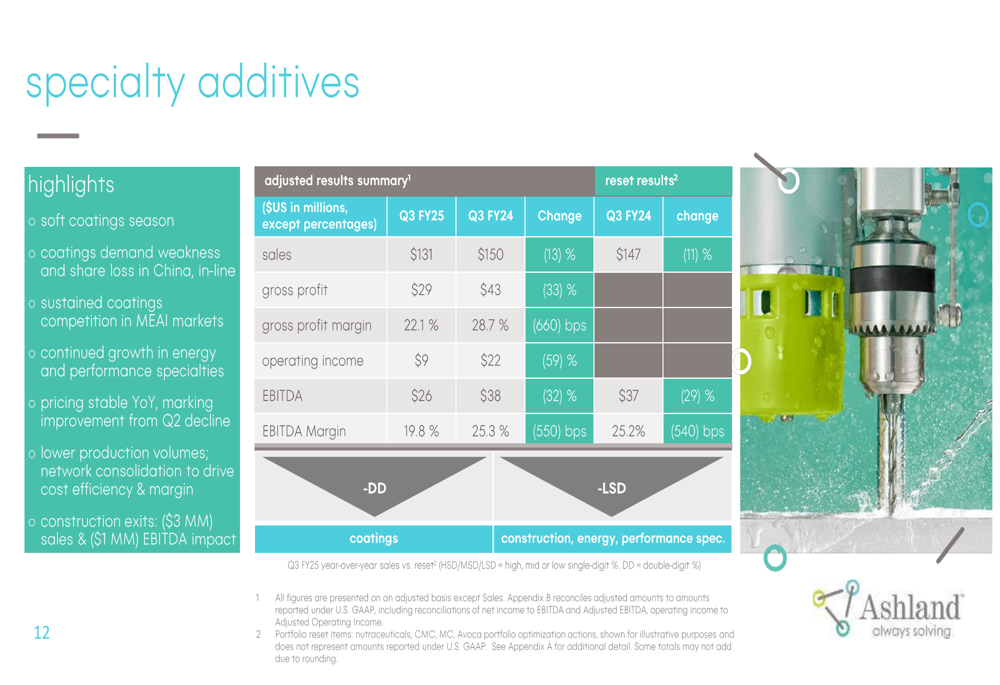

Specialty Additives continued to face challenges with sales declining 13% to $131 million and EBITDA margin dropping to 19.8% from 25.3% in the prior year. The segment was affected by a soft coatings season, demand weakness in China, and sustained competition in Middle East, Africa, and India markets.

Strategic Cost Initiatives

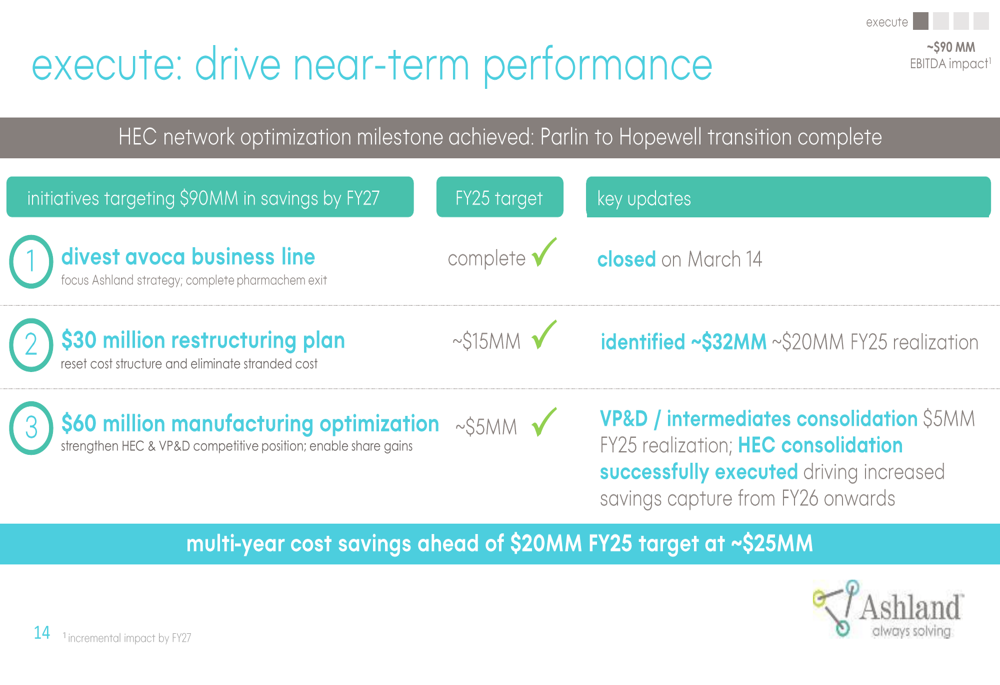

Ashland reported significant progress on its cost-saving initiatives, with multi-year cost savings ahead of the $20 million FY25 target at approximately $25 million. The company has successfully completed key milestones in its restructuring plan and manufacturing optimization efforts.

The following chart details the company’s execution of near-term performance initiatives:

The $30 million restructuring plan is ahead of schedule with approximately $32 million in savings identified, while the $60 million manufacturing optimization program is progressing with the successful execution of the HEC (hydroxyethylcellulose) network consolidation. These initiatives are expected to deliver $90 million in savings by FY27.

Strategic Growth Initiatives

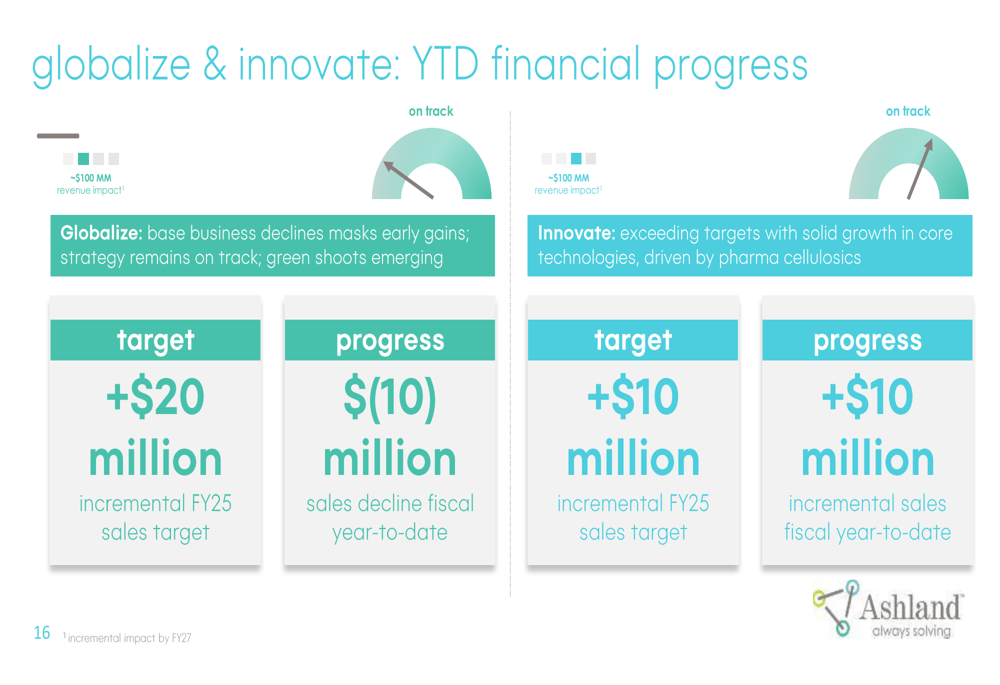

Ashland’s "Globalize" strategy, aimed at expanding its international presence, has shown early gains but remains challenged by base business declines. Meanwhile, the "Innovate" strategy is exceeding targets with solid growth in core technologies, particularly in pharmaceutical cellulosics.

The following chart illustrates the year-to-date financial progress of these strategic initiatives:

"While our Globalize strategy is showing green shoots, the overall base business declines are masking these early gains," explained Novo. "Our Innovate strategy is performing above expectations, driven by strong growth in pharma cellulosics."

Narrowed Outlook

Ashland narrowed its fiscal year 2025 outlook, projecting sales of $1.825-1.850 billion and adjusted EBITDA of $400-410 million. This represents a tightening of the previous guidance range of $1.825-1.900 billion for sales.

The revised outlook reflects several market factors, including muted growth and cautious consumer sentiment, resilient pharmaceutical demand, continued pressure in Specialty Additives and Intermediates, minimal direct FY25 tariff impact, and foreign exchange tailwinds.

Market Context

Ashland’s Q3 results follow a disappointing second quarter where both earnings per share and revenue missed analyst expectations. The stock has been under pressure, trading at $50.18 as of July 29, 2025, near its 52-week low of $45.21 and well below its 52-week high of $98.44.

The company’s focus on margin resilience through cost discipline and portfolio optimization appears to be a strategic response to challenging market conditions. With a net leverage ratio of 2.9x and approximately $0.8 billion in cash and liquidity available, Ashland maintains financial flexibility to navigate current headwinds while pursuing its long-term strategic objectives.

Looking ahead, the company faces risks including potential European and Chinese economic recovery uncertainties, competition from Chinese overcapacity, trade policy changes, raw material cost volatility, and foreign exchange fluctuations. However, its accelerated restructuring efforts and focus on high-margin segments position Ashland to potentially improve performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.