Oil prices rebound sharply on smaller-than-feared OPEC+ output hike

Introduction & Market Context

Ashtead Group PLC (LON:AHT) reported its first quarter fiscal 2026 results on September 3, 2025, showing modest growth in line with expectations. The equipment rental company delivered a 2.4% increase in Group rental revenue compared to the same period last year, while significantly improving its free cash flow generation. The company has raised its full-year free cash flow guidance, demonstrating confidence in its operational efficiency despite maintaining a cautious outlook on rental revenue growth.

Brendan Horgan, Chief Executive Officer, emphasized the company’s strategic positioning: "We delivered solid first quarter results in-line with our expectations and are well-positioned to deliver our full-year outlook." The company continues to advance its Sunbelt 4.0 strategic plan while seeing positive leading indicators in business activity levels.

Quarterly Performance Highlights

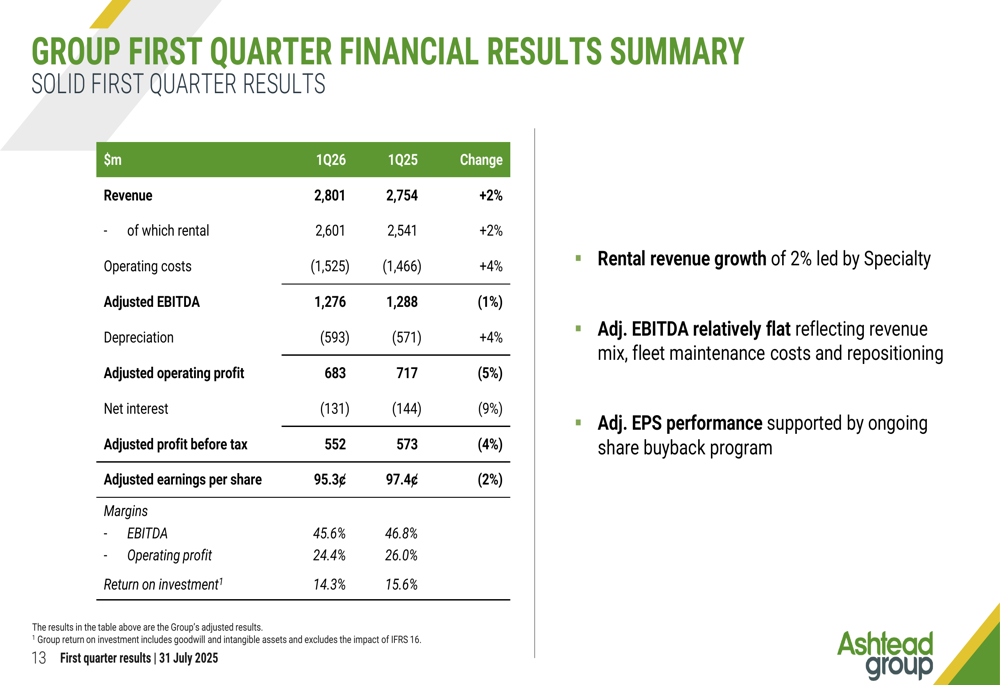

Ashtead reported total revenue of $2,801 million for Q1 FY26, representing a 2% increase from $2,754 million in Q1 FY25. Rental revenue, which constitutes the majority of the company’s income, grew by 2.4% to $2,601 million.

As shown in the following comprehensive financial summary, the company saw a slight decrease in profitability metrics compared to the same period last year:

Adjusted EBITDA decreased by 1% to $1,276 million, with margins contracting to 45.6% from 46.8% in the prior year. Adjusted profit before tax declined by 4% to $552 million, while adjusted earnings per share decreased by 2% to 95.3 cents. The company maintained a strong return on investment of 14.3%.

Performance varied across Ashtead’s business segments. North America General Tool, the company’s largest division, reported modest rental revenue growth of 1%, driven by volume improvement and stable rates. North America Specialty showed stronger performance with 5% rental revenue growth, benefiting from continued demand in project-related activity and expanded scope of value-added services. The UK segment reported 4% rental revenue growth as reported, but declined by 2% at constant exchange rates.

Strategic Initiatives

Ashtead continues to execute its Sunbelt 4.0 strategy, which focuses on five key components: Customer, Growth, Performance, Sustainability, and Investment. The company highlighted significant progress in mega project wins during the quarter, with a growing pipeline of future projects.

The company’s fleet on rent metrics show positive momentum, particularly in North America where large and mega project demand is fueling growth. Ashtead’s diversified business model and deep customer relationships continue to provide resilience, supported by the 401 locations added during Sunbelt 3.0 and 71 locations added during Sunbelt 4.0.

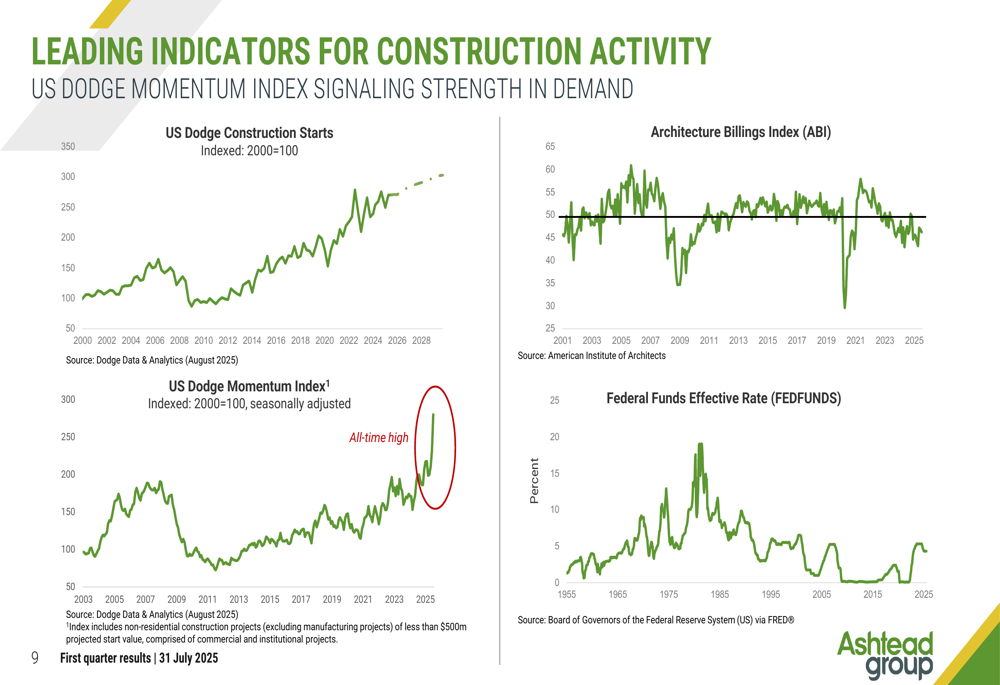

The following chart illustrates positive leading indicators for construction activity, which suggest strength in future demand:

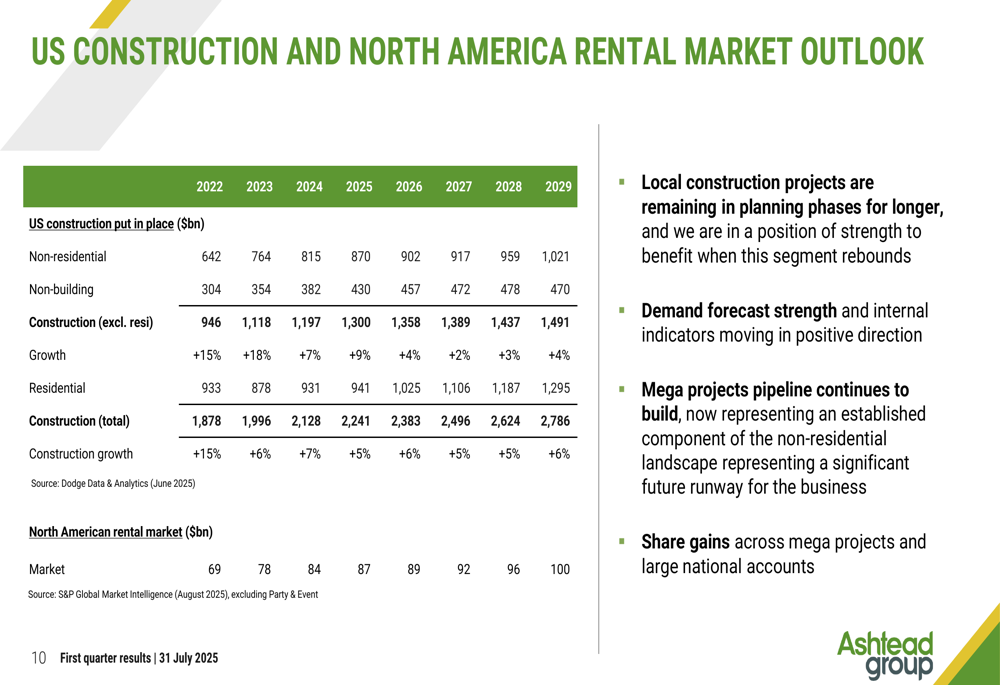

Ashtead’s long-term market outlook remains positive. The US construction market is projected to grow from $1,878 billion in 2022 to $2,786 billion by 2029, while the North American rental market is expected to expand from $69 billion to $100 billion over the same period. This presents significant growth opportunities for the company, particularly in specialty segments.

As shown in the following market outlook data, non-residential construction is expected to be a key growth driver:

Capital Allocation and Financial Position

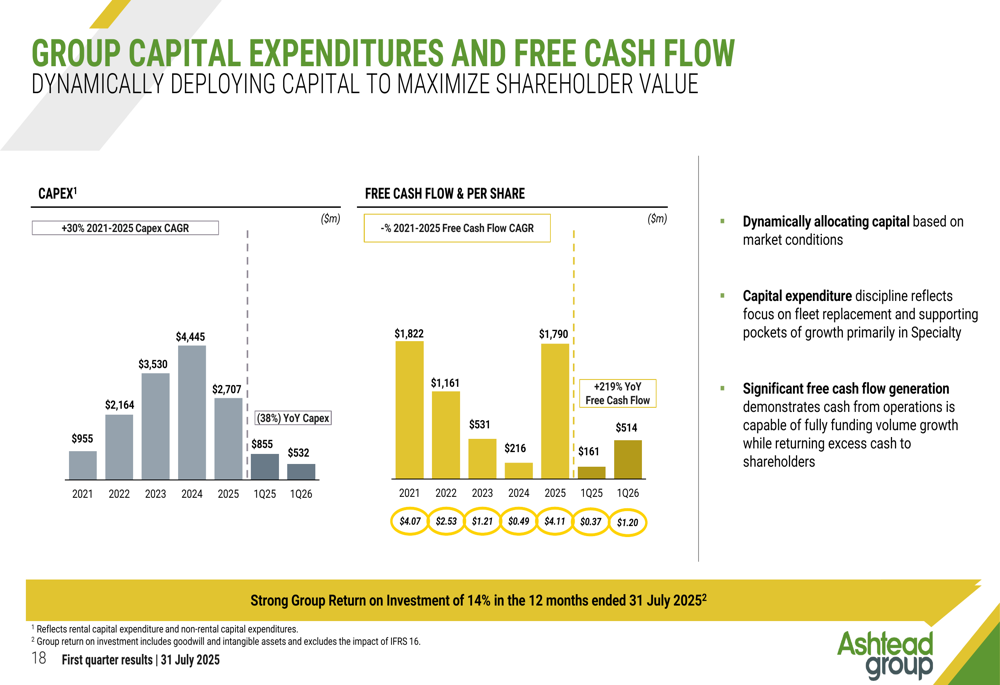

One of the most significant improvements in Ashtead’s Q1 performance was the substantial increase in free cash flow, which reached $514 million compared to $161 million in Q1 FY25. This was achieved through disciplined capital expenditure, which decreased to $532 million from $855 million in the prior year.

The following chart illustrates the company’s capital expenditure and free cash flow trends:

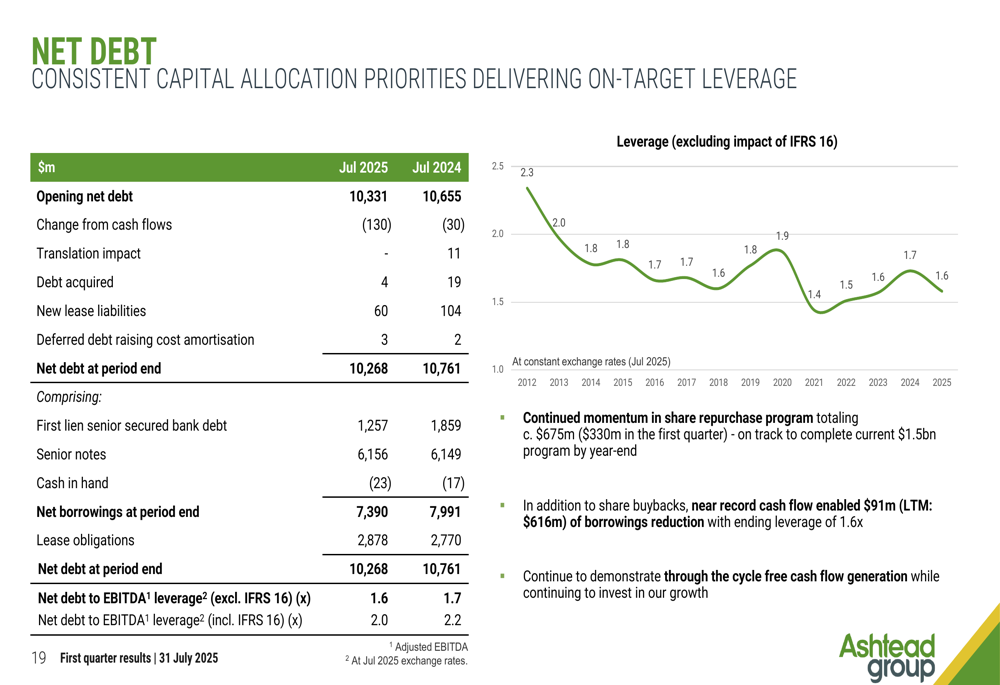

Ashtead maintained a strong balance sheet, with net debt decreasing to $10,268 million at the end of July 2025 from $10,761 million a year earlier. The company’s net debt to EBITDA leverage ratio (excluding IFRS 16) improved to 1.6x from 1.7x in July 2024.

The company’s leverage position remains well within target ranges, as shown in the following chart:

Ashtead’s capital allocation priorities remain consistent, focusing on organic fleet growth, bolt-on acquisitions, and returns to shareholders. The company continues its share repurchase program, demonstrating its commitment to delivering shareholder value.

Forward-Looking Statements

Ashtead reaffirmed its full-year guidance for Group rental revenue growth of 0-4% and capital expenditure of $1.8-2.2 billion. However, the company raised its free cash flow guidance from $2.0-2.3 billion to $2.2-2.5 billion, reflecting improved operational efficiency and cash generation capabilities.

The company also announced that its primary listing is on track to move to the New York Stock Exchange, with an Investor Day planned in New York City in March 2026. This move aligns with the company’s significant North American presence, where it generates the majority of its revenue.

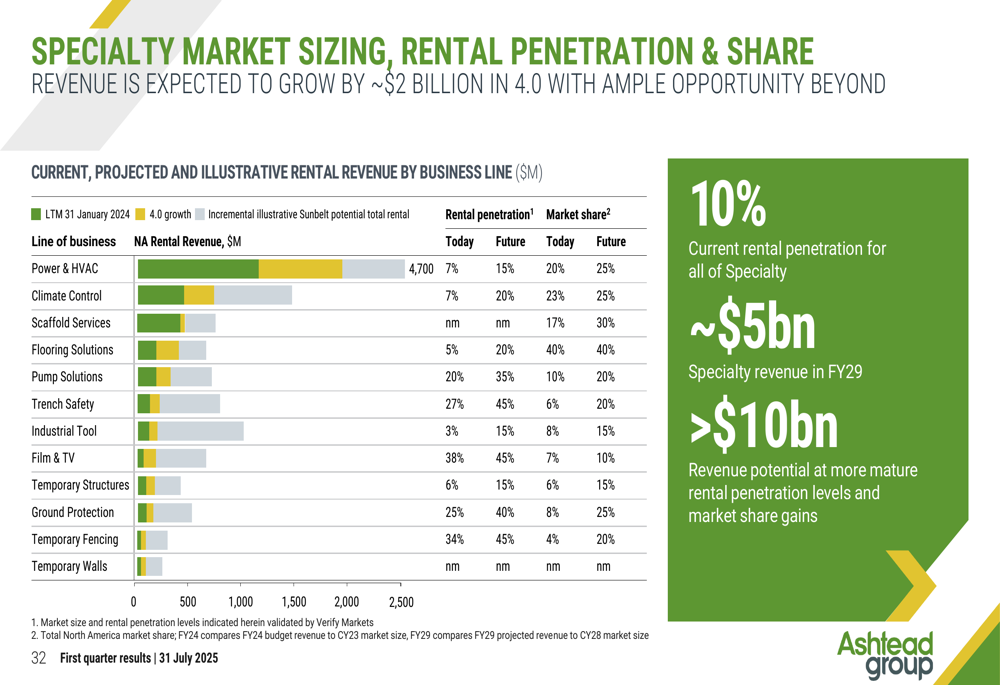

Ashtead highlighted several positive indicators for future growth, including a strong pipeline of mega projects and improving conditions in the local non-residential construction market. The company’s specialty segments continue to present significant growth opportunities, with current rental penetration at only 10% and potential revenue exceeding $10 billion with more mature rental penetration levels.

As illustrated in the following specialty market sizing data, there is substantial growth potential in this segment:

Competitive Industry Position

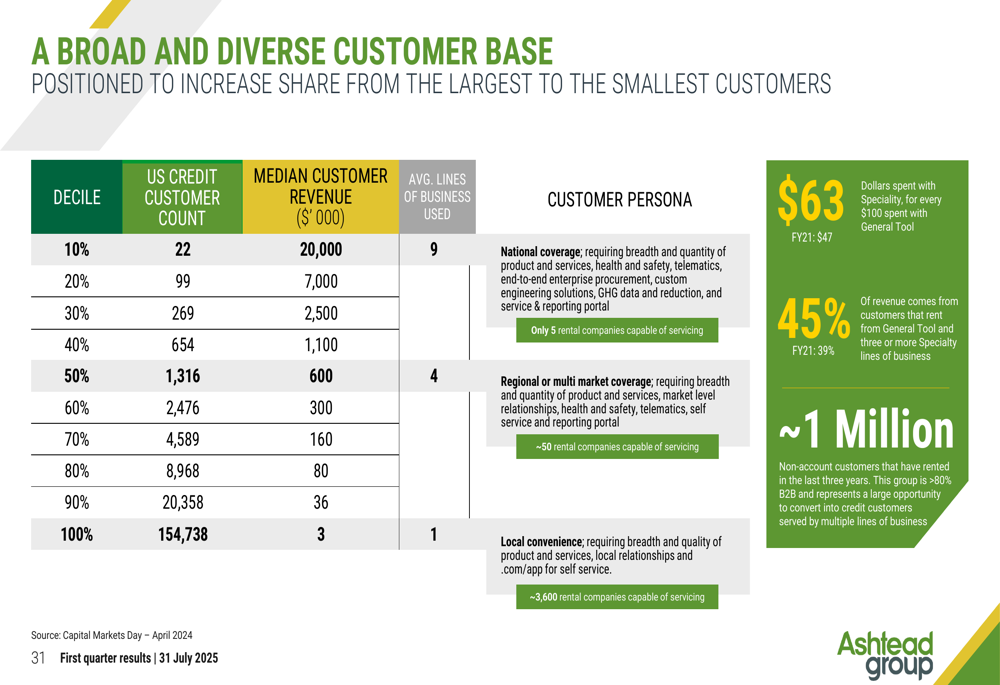

Ashtead maintains a strong competitive position through its broad and diverse customer base. The company is strategically positioned to increase market share across customer segments, from large national accounts to small local businesses.

For every $100 spent with Ashtead’s General Tool segment, customers spend $63 with Specialty, highlighting the company’s success in cross-selling. Additionally, 45% of revenue comes from customers that rent from General Tool and three or more Specialty lines of business, demonstrating strong customer relationships and service integration.

The following customer analysis illustrates the company’s diverse customer base:

Ashtead’s focus on safety continues to yield positive results, with significant improvements in rear-ending collision events since implementing a driver safety profile program and dash camera technology. The company’s professional drivers cover more than one million miles daily, completing more than 30,000 deliveries and pick-ups every day.

In conclusion, Ashtead’s Q1 FY26 results demonstrate the company’s resilience and adaptability in a dynamic market environment. While growth has moderated compared to previous periods, the significant improvement in free cash flow generation and disciplined capital allocation position the company well for sustainable long-term growth. With positive leading indicators in construction activity and a strong pipeline of mega projects, Ashtead remains confident in its ability to deliver on its full-year outlook and create shareholder value through its Sunbelt 4.0 strategic plan.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.