Gold prices edge higher with focus on Ukraine-Russia, Jackson Hole

Introduction & Market Context

Aspen Aerogels (NYSE:ASPN) shares surged 16.81% to $9.63 on August 7, 2025, following the release of its Q2 2025 financial results, which showed significant operational improvements despite flat revenue. The stock’s positive momentum continued in premarket trading with an additional 8.01% gain to $8.90.

The thermal barrier and aerogel materials manufacturer has been implementing an aggressive cost-cutting strategy after disappointing Q1 results, which had previously sent shares tumbling near their 52-week low of $4.16. Today’s presentation highlighted the company’s progress in operational efficiency and improved profitability metrics.

Quarterly Performance Highlights

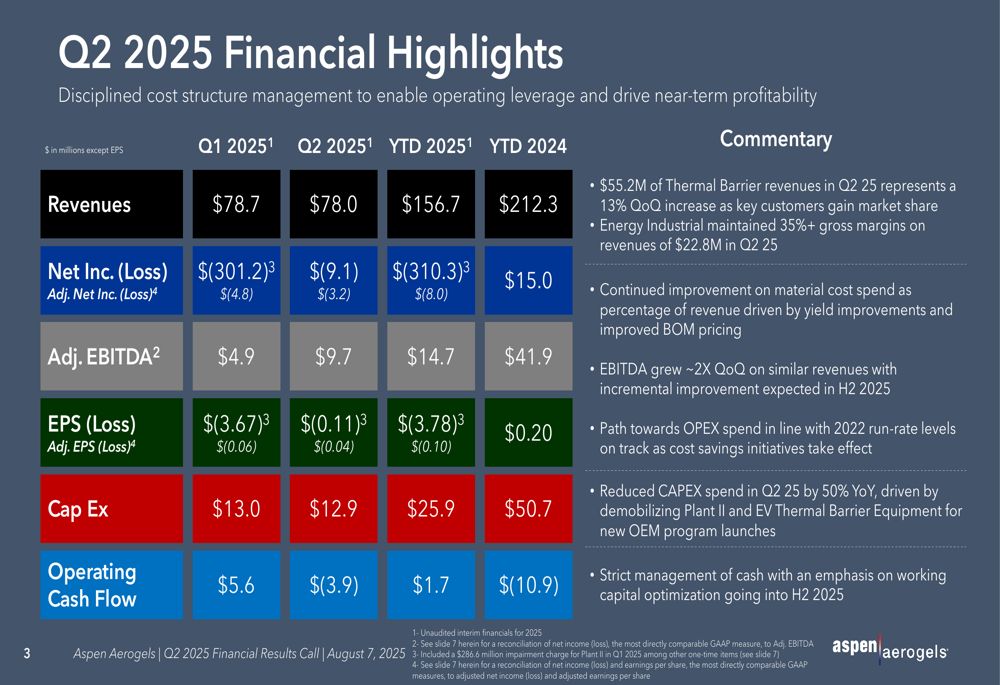

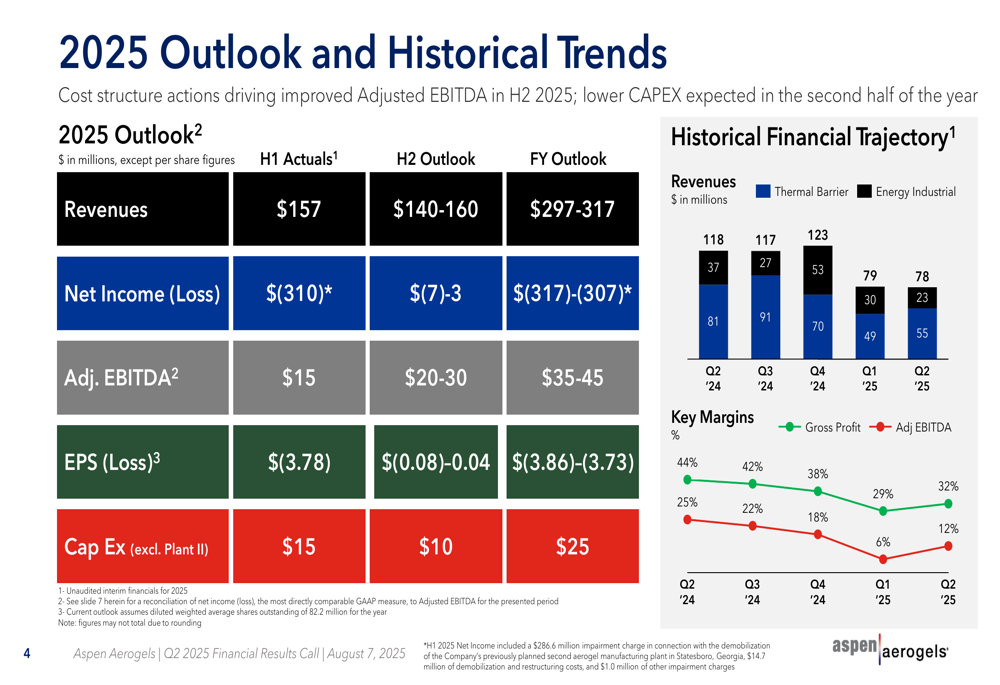

Aspen Aerogels reported Q2 2025 revenue of $78.0 million, virtually unchanged from the $78.7 million in Q1 2025, but representing a decrease from the comparable period in 2024. Despite flat sequential revenue, the company achieved a dramatic improvement in profitability metrics.

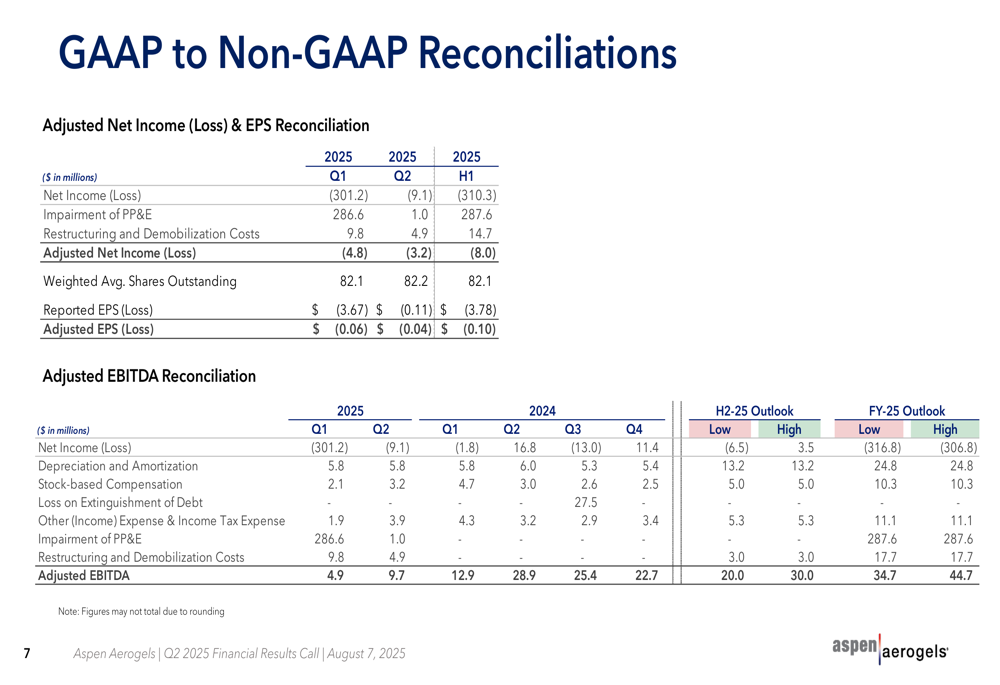

The company’s net loss narrowed significantly to $(9.1) million in Q2 2025 from $(301.2) million in Q1, while Adjusted EBITDA nearly doubled to $9.7 million from $4.9 million in the previous quarter. This improvement demonstrates the effectiveness of the company’s cost reduction initiatives.

As shown in the following financial highlights table:

Thermal barrier revenues, which represent the company’s EV battery products, reached $55.2 million in Q2 2025, a 13% quarter-over-quarter increase. Meanwhile, the Energy Industrial segment maintained strong gross margins above 35% on revenues of $22.8 million.

The company’s gross margin improved from 29% in Q1 2025 to 32% in Q2 2025, while Adjusted EBITDA margin doubled from 6% to 12% in the same period. However, these margins remain below the levels achieved in 2024, as illustrated in the historical trends chart:

Cost Structure Improvements

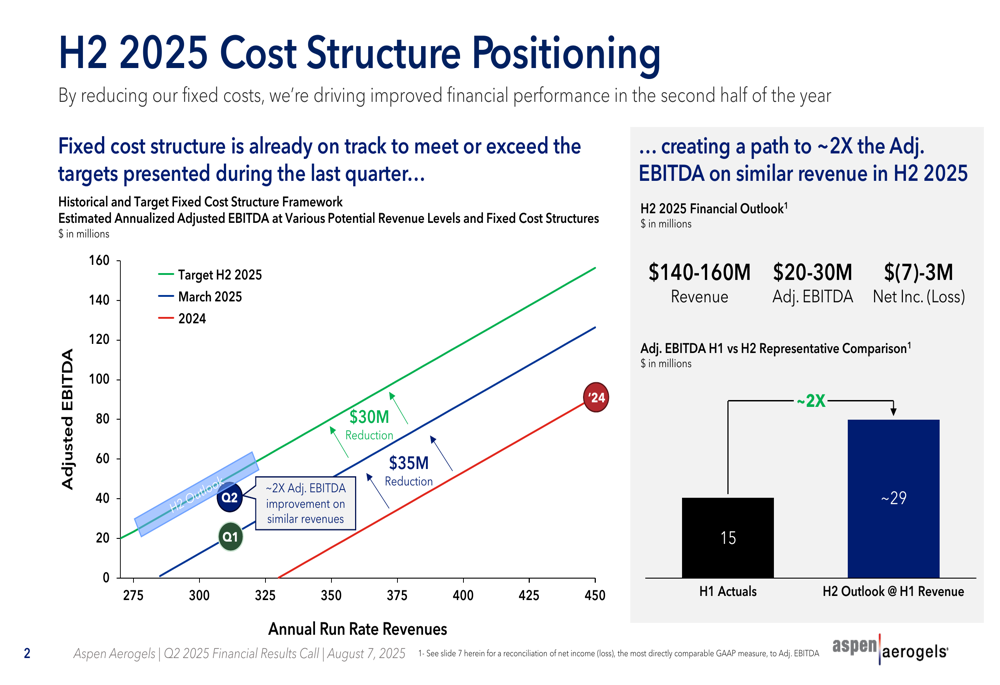

A central theme of Aspen’s presentation was its progress in optimizing its cost structure. The company reported that its fixed cost reduction is on track to meet or exceed previous targets, with a framework showing potential for $30-35 million in reductions.

The improved cost structure is expected to enhance financial performance, with the company highlighting that Adjusted EBITDA grew approximately 2x quarter-over-quarter on similar revenues. Operating expenses have been reduced to levels comparable to 2022, while capital expenditures were cut by 50% year-over-year.

As illustrated in the following cost structure positioning chart:

CFO Ricardo Rodriguez had previously stated during the Q1 earnings call, "We are on a path to put the company’s potential adjusted EBITDA on the green line," referring to the target cost structure. The Q2 results suggest the company is making meaningful progress toward this goal.

Forward Outlook

Aspen Aerogels provided an optimistic outlook for the second half of 2025, projecting revenues between $140-160 million and Adjusted EBITDA between $20-30 million. This represents a significant improvement over the first half of 2025, where the company reported $157 million in revenue and $15 million in Adjusted EBITDA.

For the full year 2025, Aspen expects:

- Revenue: $297-317 million

- Adjusted EBITDA: $35-45 million

- Net Income (Loss): $(317)-(307) million

- EPS (Loss): $(3.86)-(3.73)

- Capital Expenditures: $25 million (excluding Plant II)

The large net loss for the full year is primarily due to the $286.6 million impairment of property, plant, and equipment recorded in Q1 2025, as shown in the GAAP to Non-GAAP reconciliation:

Strategic Initiatives

Aspen Aerogels outlined its strategic roadmap for creating near-term value, focusing on several key initiatives:

1. Demonstrated Operating Execution: The ~2X improvement in Adjusted EBITDA quarter-over-quarter at similar revenue run rates

2. Increasing Flexibility to Meet Demand: Sourcing optimization and diversified raw material supply chain

3. Securing More Commercial Contracts: Working closely with EV OEMs and capitalizing on Subsea and LNG project opportunities

4. Improving Capital Efficiency: Enhanced cost structure and reduced capital expenditure plans

The company’s strategic focus is illustrated in the following summary slide:

CEO Don Young had previously stated, "We believe that electrification through this decade will be a major driver for both our thermal barrier and energy industrial businesses." The Q2 presentation reinforces this strategic direction while emphasizing operational efficiency.

Market Positioning

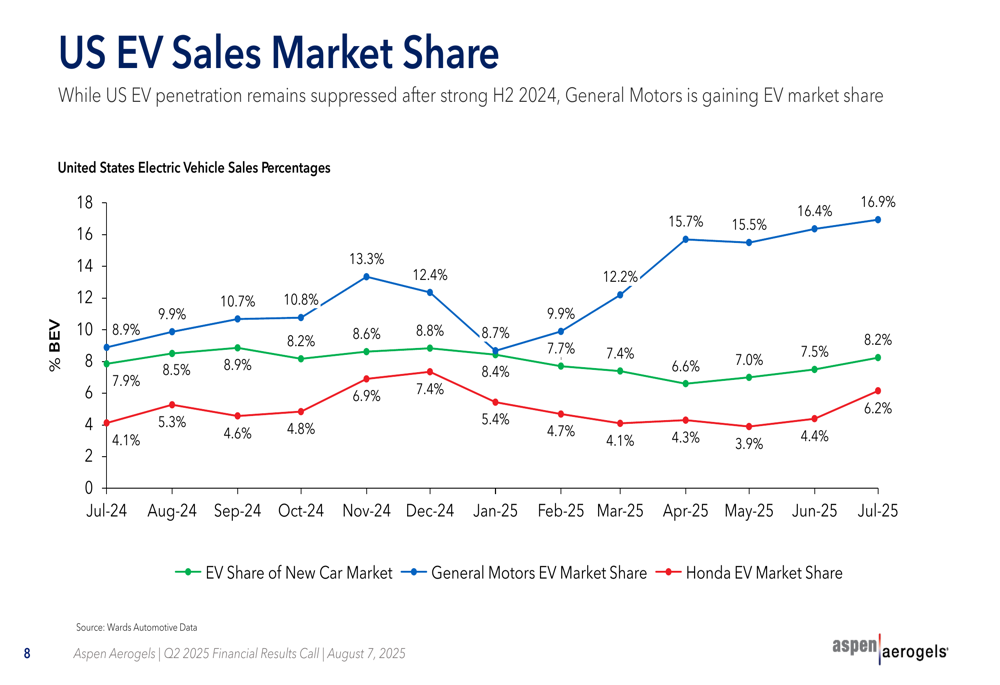

Aspen’s presentation included insights into the US electric vehicle market, noting that while overall EV penetration remains suppressed after strong performance in the second half of 2024, General Motors—one of Aspen’s key customers—is gaining market share.

The data shows GM’s EV market share nearly doubled from 8.9% in July 2024 to 16.9% in July 2025, which could benefit Aspen as a supplier of thermal barrier solutions for EV batteries.

As shown in the following US EV market share chart:

The presentation also provided a detailed forecast for GM’s North American EV production, projecting approximately 241,000 units in 2025, with a slight reduction in the long-term forecast due to changing regulatory and incentive environments.

The GM production forecast by model and quarter is illustrated here:

This forecast is particularly relevant for Aspen as it indicates potential demand for the company’s thermal barrier products, which are used in electric vehicle battery systems to enhance safety and performance.

After a challenging start to 2025, Aspen Aerogels appears to be making significant progress in its operational turnaround, with doubled EBITDA and an improved cost structure positioning the company for stronger performance in the second half of the year. While revenue growth remains a challenge, the focus on profitability and capital efficiency appears to be resonating with investors, as evidenced by today’s strong stock performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.