Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

Finnish conglomerate Aspo Oyj (HEL:ASPO) reported continued profit improvement in its Q2 2025 financial results presentation delivered on August 18, despite facing challenging market conditions. The company highlighted growth in comparable EBITA while announcing a significant strategic move with the planned divestment of its Leipurin business.

Aspo’s stock closed at €5.80 on the presentation day, trading between its 52-week range of €4.71-€6.16. The company has shown resilience following its Q1 performance, when it reported a 14% increase in net sales and saw its stock rise 7.11% after the earnings announcement.

Quarterly Performance Highlights

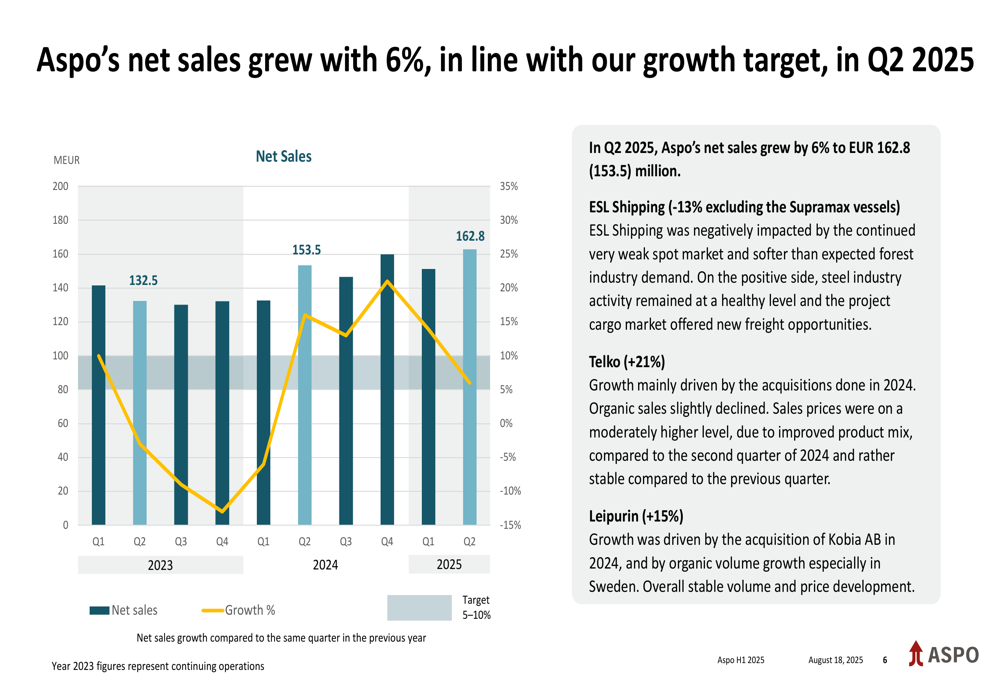

In Q2 2025, Aspo achieved net sales growth of 6% to €162.8 million compared to €153.5 million in Q2 2024. The company’s comparable EBITA increased to €9.2 million from €7.4 million in the same period last year, representing a 24% improvement and pushing the comparable EBITA margin to 5.6% from 4.8%.

For the first half of 2025, Aspo reported even stronger performance with net sales growing by 9.7% and comparable EBITA reaching €18.0 million compared to €12.4 million in H1 2024.

As shown in the following chart of quarterly net sales growth:

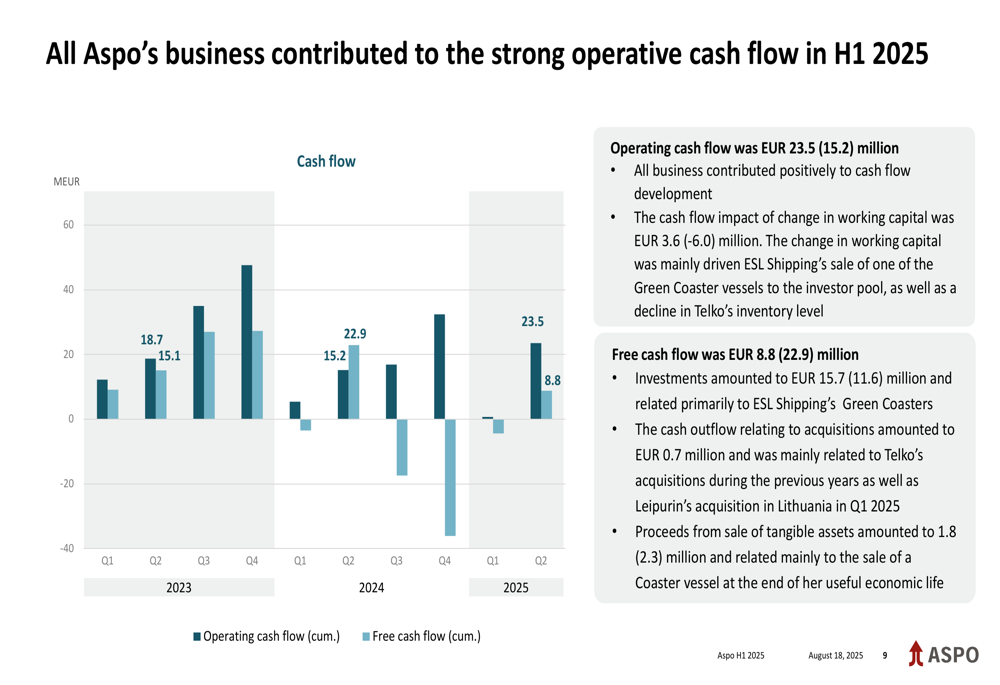

The company’s operating cash flow remained strong at €23.5 million for H1 2025, compared to €15.2 million in the corresponding period last year. Free cash flow was €8.8 million, down from €22.9 million in H1 2024, with the difference primarily attributed to investments of €15.7 million mainly related to ESL Shipping’s Green Coasters.

The following chart illustrates Aspo’s operating and free cash flow development:

Strategic Initiatives

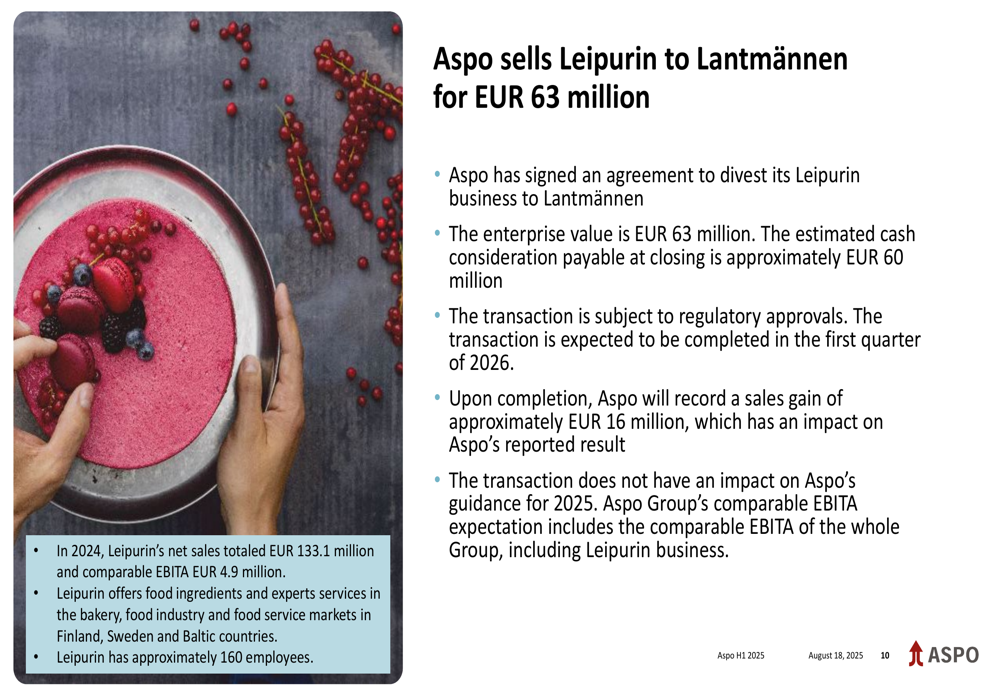

The most significant strategic announcement was the agreement to sell Leipurin to Lantmännen for €63 million. The estimated cash consideration payable at closing is approximately €60 million, with the transaction expected to be completed in Q1 2026 subject to regulatory approvals. Upon completion, Aspo anticipates recording a sales gain of approximately €16 million.

The divestment details are outlined in this slide:

This transaction represents a major step in Aspo’s vision to form two separate companies: Aspo Infra (ESL Shipping) and Aspo Compounder (Telko). The divestment will significantly strengthen Aspo’s balance sheet and enable future growth investments for the Telko business.

CEO Rolf Jansson emphasized that the company’s first priority remains profit generation, focusing on maximizing benefits from acquisitions and capital expenditure investments, along with organic growth and performance improvements. The longer-term financial ambition is to achieve €1 billion in net sales and 8% EBITA by 2028.

Business Unit Performance

Performance varied across Aspo’s business units, with Telko and Leipurin showing strong growth while ESL Shipping faced market headwinds:

ESL Shipping: Net sales decreased by 14% to €94.6 million in H1 2025, impacted by a weak spot market and softer than expected forest industry demand. However, comparable EBITA increased by 4% to €9.1 million, resulting in a comparable EBITA margin of 9.7%. Vessel capacity in Q2 was reduced by 133 planned docking days compared to just 25 days in Q2 2024.

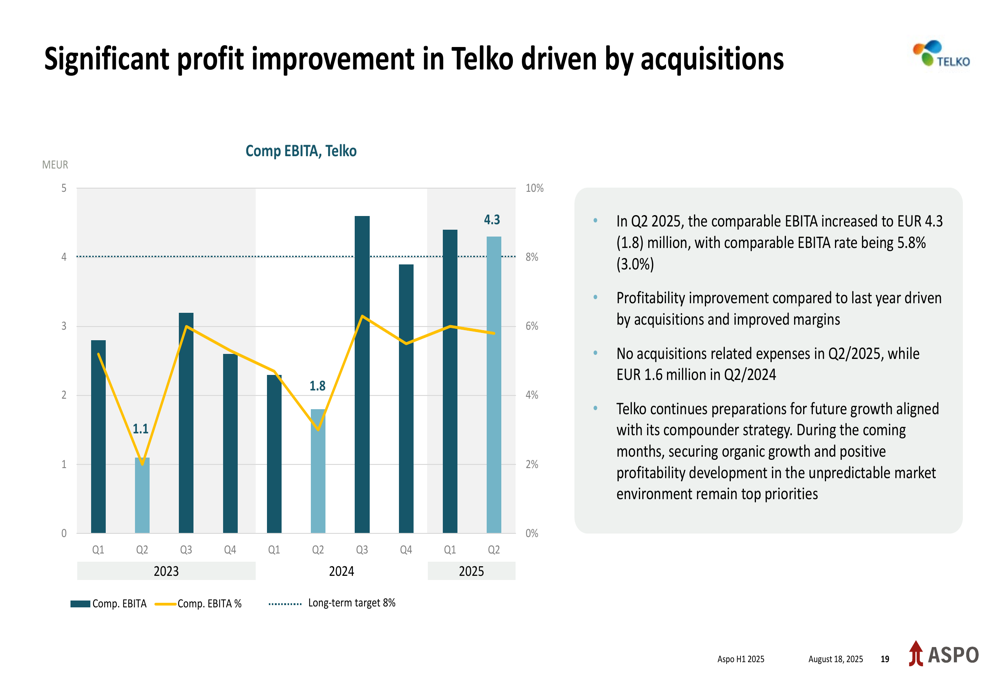

Telko: Net sales increased by 32% to €147.2 million in H1 2025, with comparable EBITA more than doubling to €8.7 million and a comparable EBITA margin of 5.9%. Growth was primarily driven by acquisitions completed in 2024, while organic sales volumes were lower but improved toward the end of Q2. Demand remained modest in most European markets, with uncertainty related to tariffs postponing some customer projects.

The following chart shows Telko’s significant profit improvement:

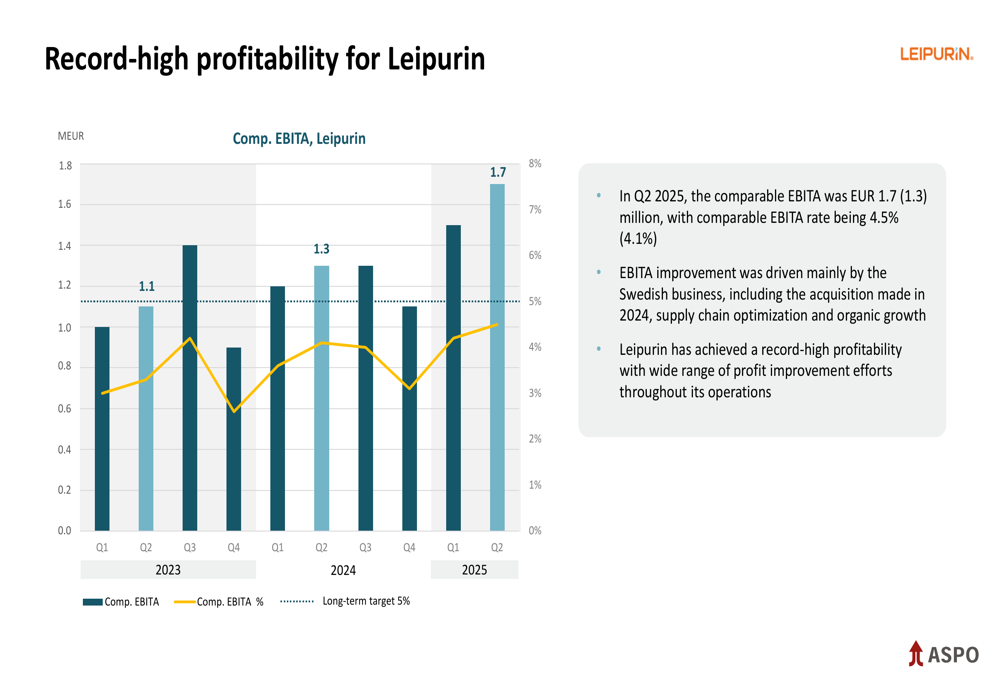

Leipurin: Prior to the announced divestment, Leipurin reported an 11% increase in net sales to €72.2 million in H1 2025, with record-high comparable EBITA of €3.1 million and a comparable EBITA margin of 4.3%. Growth was driven by the acquisition of Kobia AB in 2024 and organic volume growth, especially in Sweden.

The company’s record profitability is illustrated in this chart:

Financial Position & Outlook

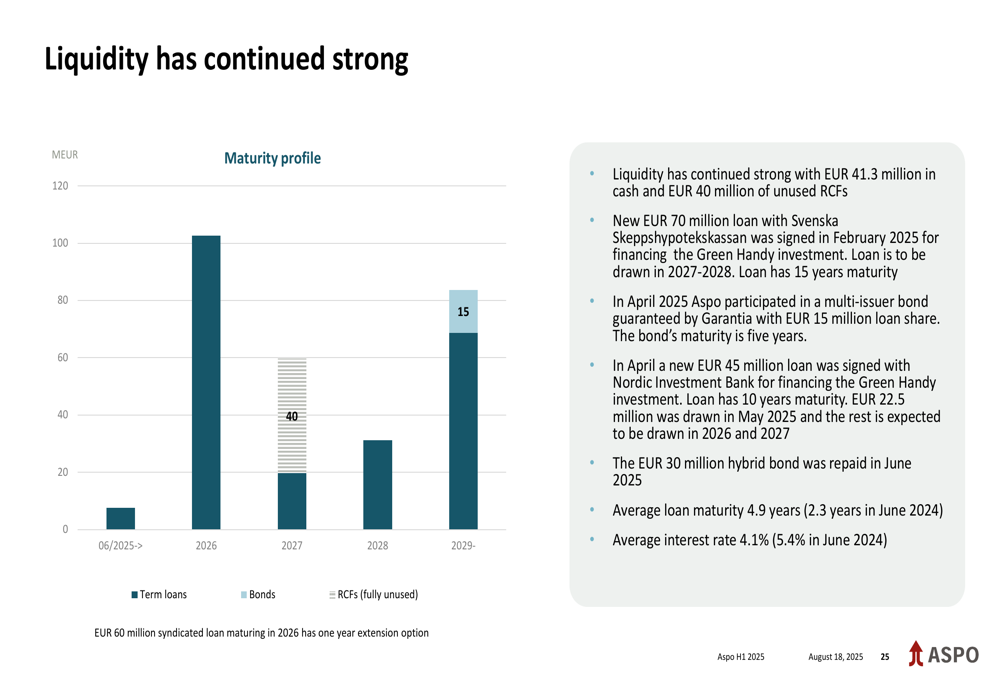

Aspo maintained strong liquidity with €41.3 million in cash and €40 million in unused revolving credit facilities as of Q2 2025, a significant improvement from the €23.9 million cash position reported at the end of Q1.

The following slide demonstrates the company’s liquidity position:

However, the Net Debt to EBITDA ratio increased to 3.7, moving further from the company’s target of below 3.0 and deteriorating from the 3.3 ratio reported in Q1 2025. The equity ratio was 27.6%, down from 36.9% at the end of 2024, impacted by the repayment of a hybrid bond and temporary items.

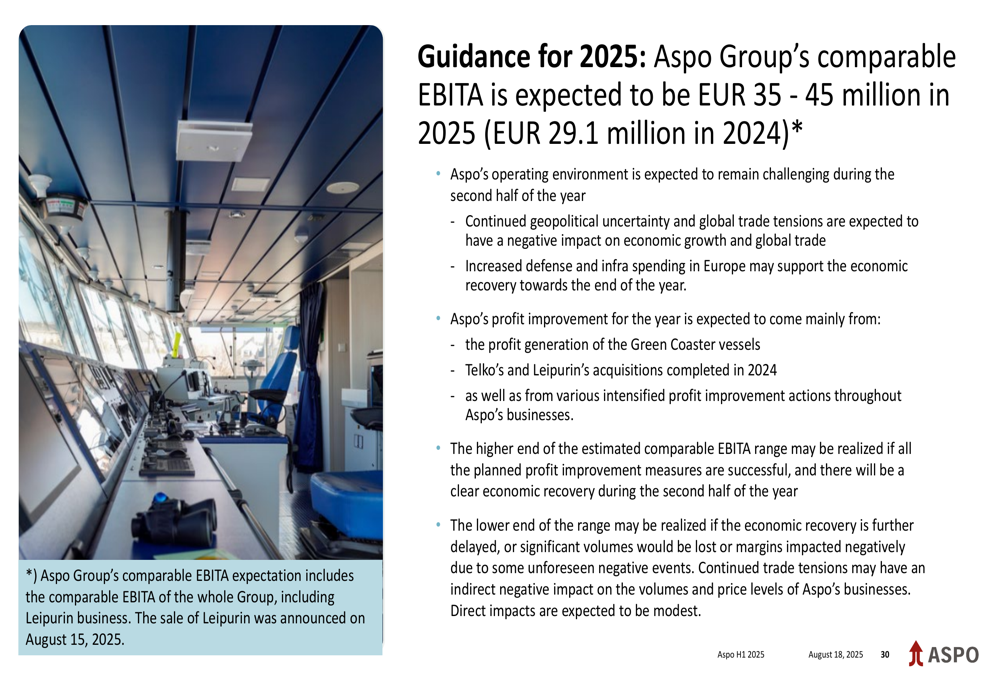

Looking ahead, Aspo maintained its 2025 guidance, expecting comparable EBITA to be in the range of €35-45 million, compared to €29.1 million in 2024. The company anticipates that market conditions will remain challenging during the second half of the year, with fairly low contractual volumes combined with low spot market pricing for ESL Shipping, while Telko and Leipurin markets are expected to remain stable.

The guidance and key profit improvement drivers are summarized in this slide:

Aspo’s presentation highlighted continued progress toward its strategic vision despite market challenges, with the Leipurin divestment representing a significant milestone in the company’s transformation journey. While ESL Shipping faces headwinds, the strong performance of Telko and Leipurin has enabled overall profit improvement, positioning the company to advance toward its long-term financial ambitions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.