UBS cuts Shell to “neutral,” warns stock ‘no longer cheap’ after strong rally

Introduction & Market Context

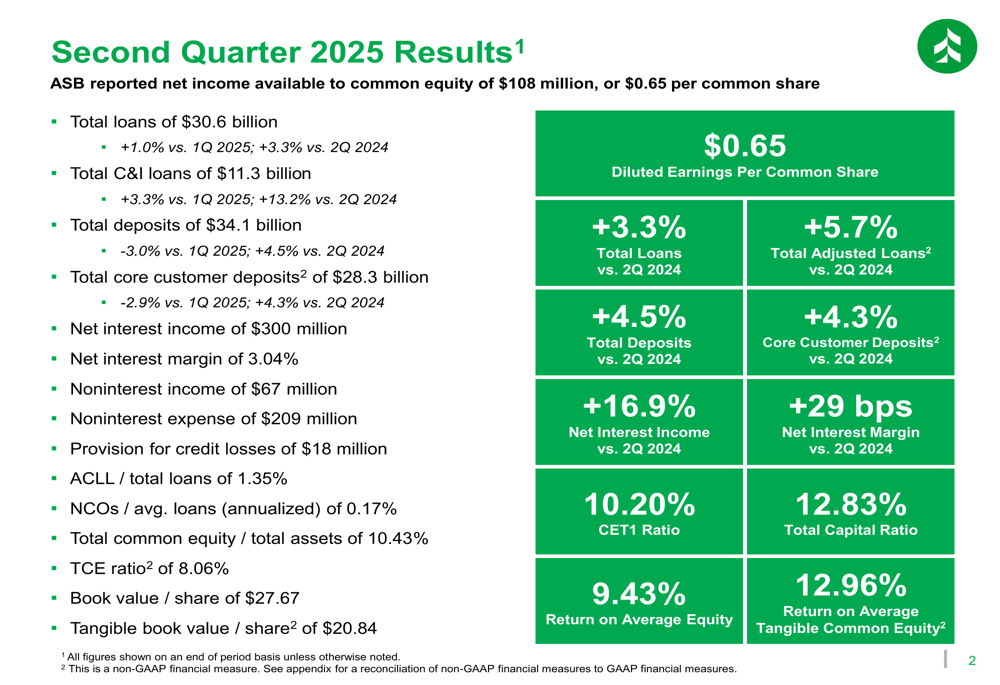

Associated Banc-Corp (NYSE:ASB) released its second quarter 2025 earnings presentation on July 24, 2025, highlighting continued improvement in net interest margin and strategic balance sheet repositioning. The bank’s stock rose 1.35% in after-hours trading to $26.25, building on momentum from its first quarter performance when it exceeded analyst expectations with an EPS of $0.59.

The Q2 results demonstrate the company’s ongoing execution of strategic initiatives aimed at enhancing profitability through growth and balance sheet optimization. These efforts come amid a changing interest rate environment, with the bank taking proactive steps to reduce asset sensitivity and protect net interest income in anticipation of potential rate cuts.

Quarterly Performance Highlights

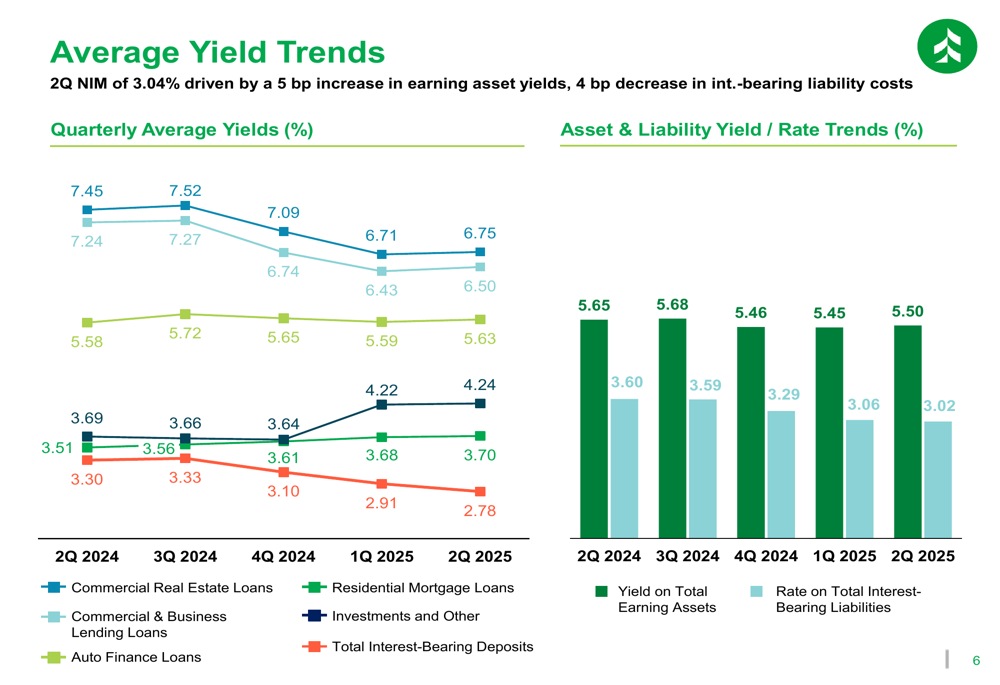

Associated Bank reported significant improvements in key performance metrics for Q2 2025. Net interest income increased by $14 million compared to the previous quarter, reaching $300 million. The net interest margin expanded by 7 basis points to 3.04%, continuing an upward trend from 2.75% in Q2 2024.

As shown in the following chart, net interest income has grown consistently over the past year, with the net interest margin expanding in tandem:

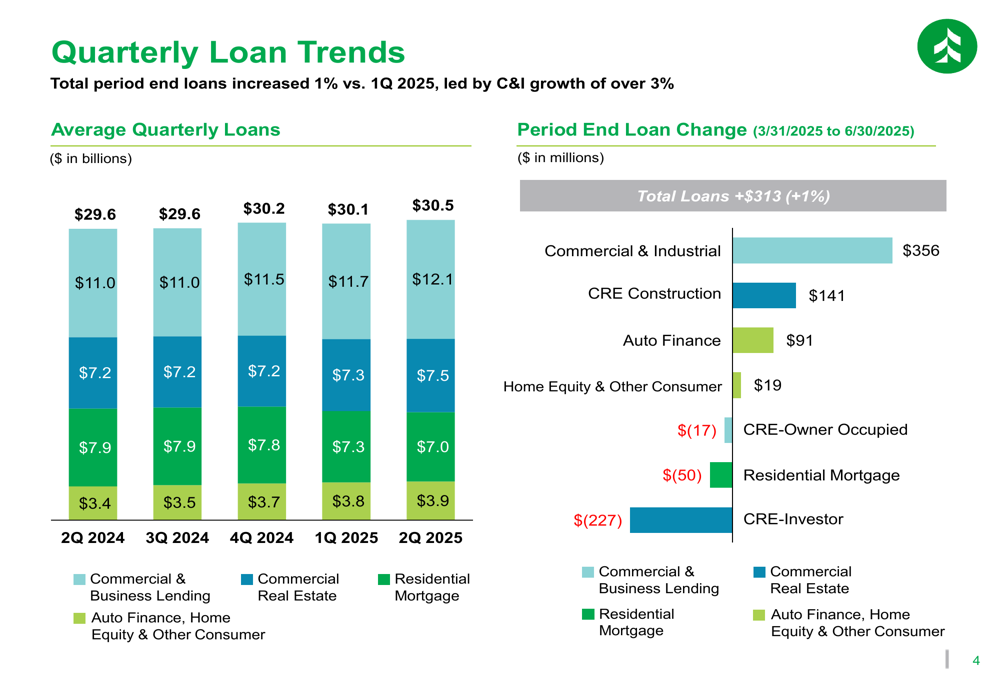

Total (EPA:TTEF) period-end loans increased by 1% compared to Q1 2025, led by Commercial & Industrial (C&I) growth of over 3%. The loan portfolio continued its strategic shift, with C&I loans showing the strongest growth at $356 million for the quarter.

The following chart details the quarterly loan trends and period-end loan changes by category:

On the deposit side, total period-end deposits increased by more than 4% compared to Q2 2024, driven by household growth and relationship deepening efforts. Core customer deposits showed healthy growth, reflecting the bank’s focus on stable funding sources.

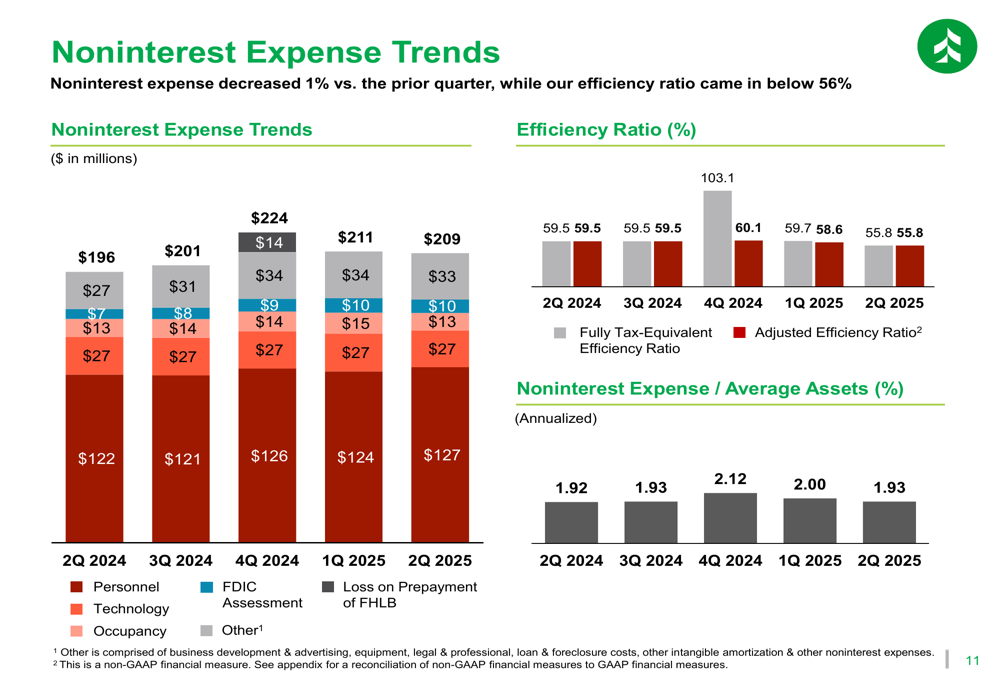

Noninterest income increased by 3% compared to the same period last year, reaching $67 million. Meanwhile, noninterest expense decreased by 1% compared to the prior quarter, with the efficiency ratio improving to below 56%.

Strategic Balance Sheet Repositioning

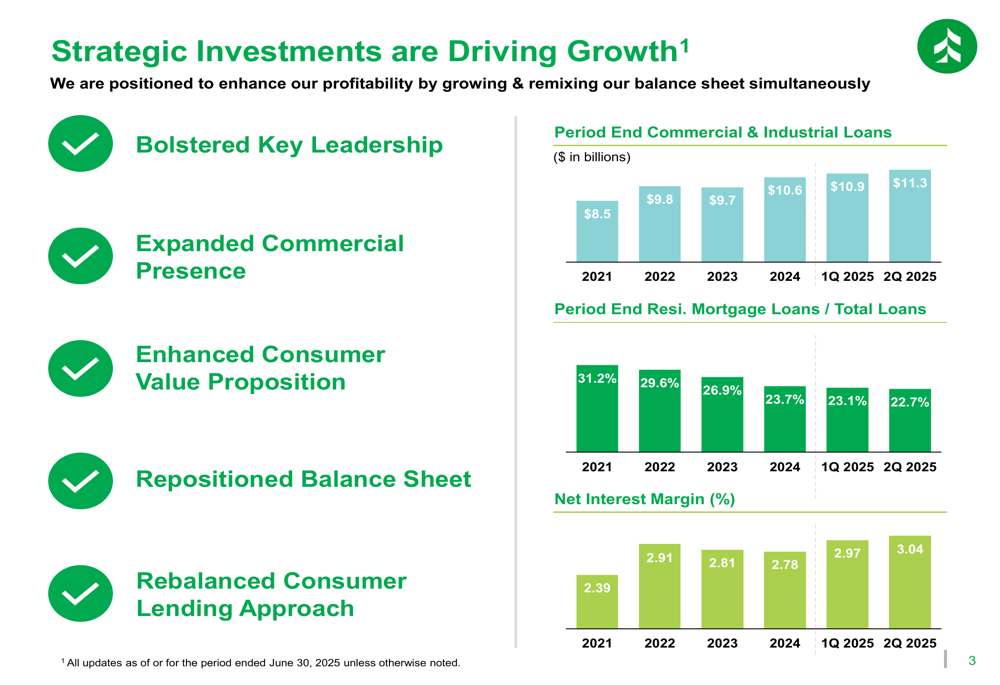

Associated Bank’s strategic investments continue to drive growth and profitability improvements. The bank has successfully repositioned its balance sheet over the past several years, growing C&I loans from $8.5 billion in 2021 to $11.3 billion in Q2 2025, while reducing residential mortgage loans as a percentage of total loans from 31.2% to 22.7% during the same period.

This strategic shift, along with other initiatives including bolstered leadership, expanded commercial presence, and an enhanced consumer value proposition, has contributed to the significant improvement in net interest margin from 2.39% in 2021 to 3.04% in Q2 2025.

The following chart illustrates these strategic initiatives and their impact:

The bank has also taken proactive steps to manage interest rate risk, reducing asset sensitivity to protect net interest income in a falling rate environment. This positioning aligns with market expectations for potential Federal Reserve rate cuts in the coming quarters.

Credit Quality and Capital Position

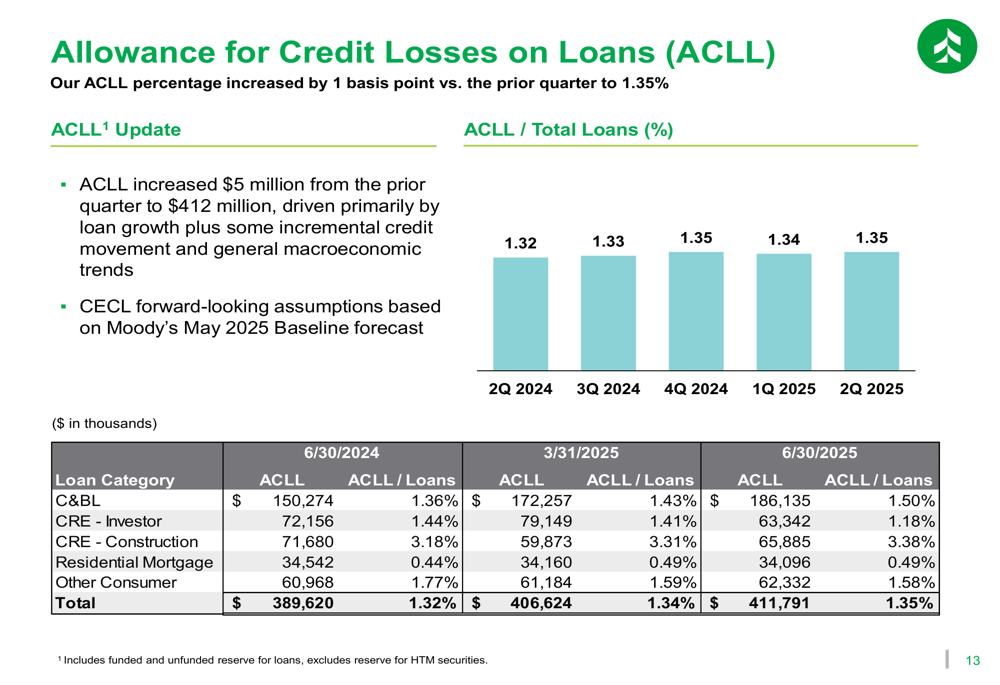

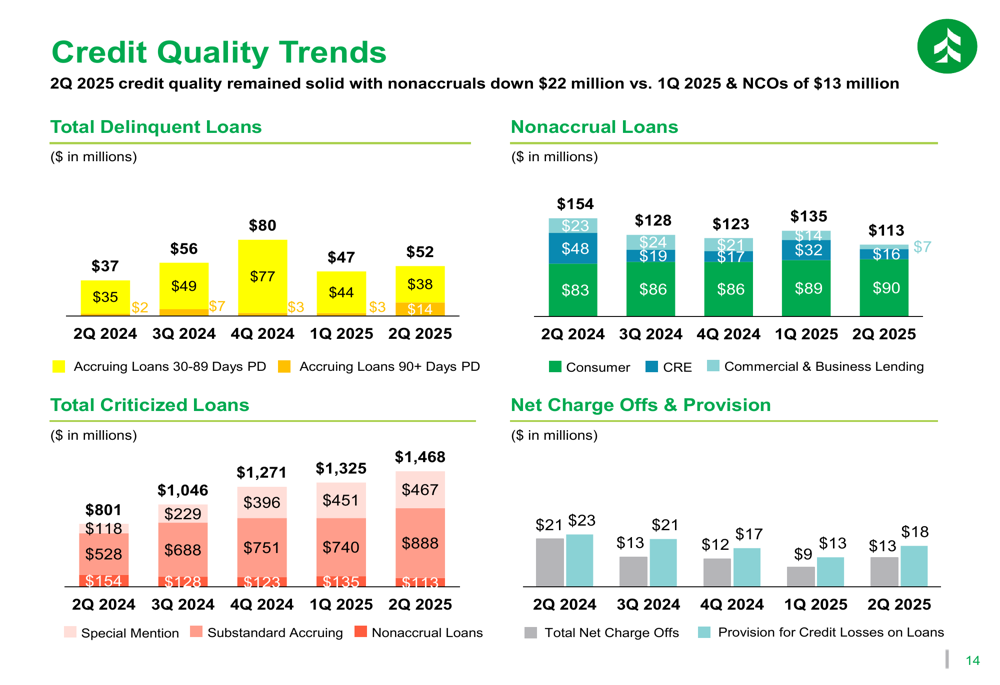

Credit quality remained solid in Q2 2025, with nonaccrual loans down $22 million compared to Q1 2025. Net charge-offs totaled $13 million for the quarter. The allowance for credit losses on loans (ACLL) increased by 1 basis point to 1.35% of total loans.

The following chart shows the stable credit quality trends across various metrics:

Associated Bank maintains a strong capital position, with a Common Equity Tier 1 (CET1) ratio within its target range of 10% to 10.5%. Book value per share increased to $27.67 from $26.85 a year ago, while tangible book value per share grew to $20.84 from $19.28 during the same period.

The bank’s liquidity position remains robust, with total liquidity sources covering 173% of uninsured, uncollateralized deposits as of June 30, 2025.

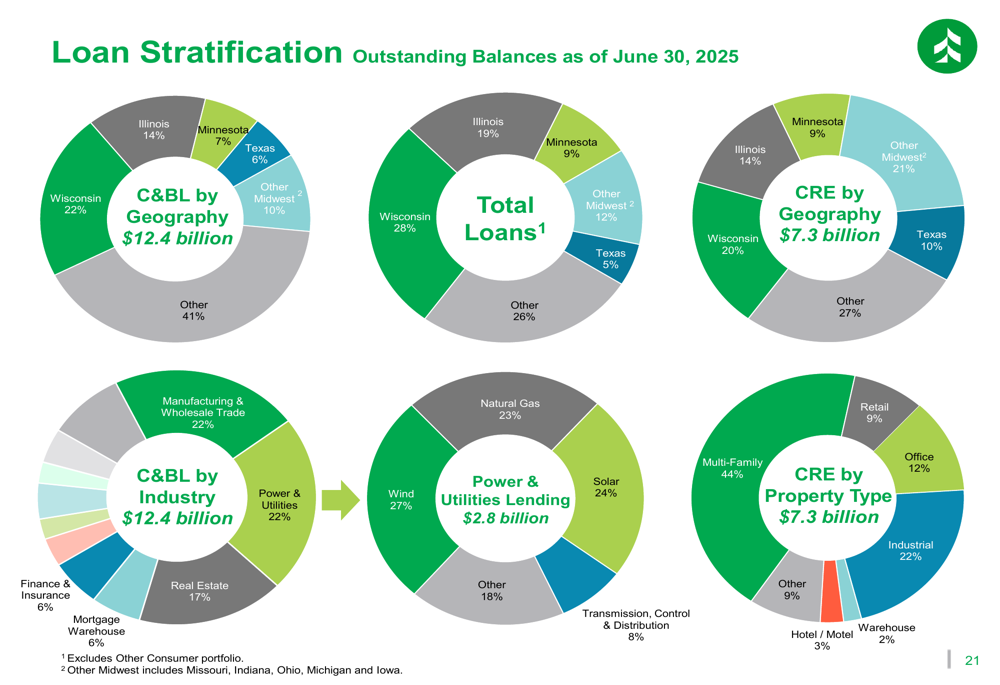

High-Quality Loan Portfolio

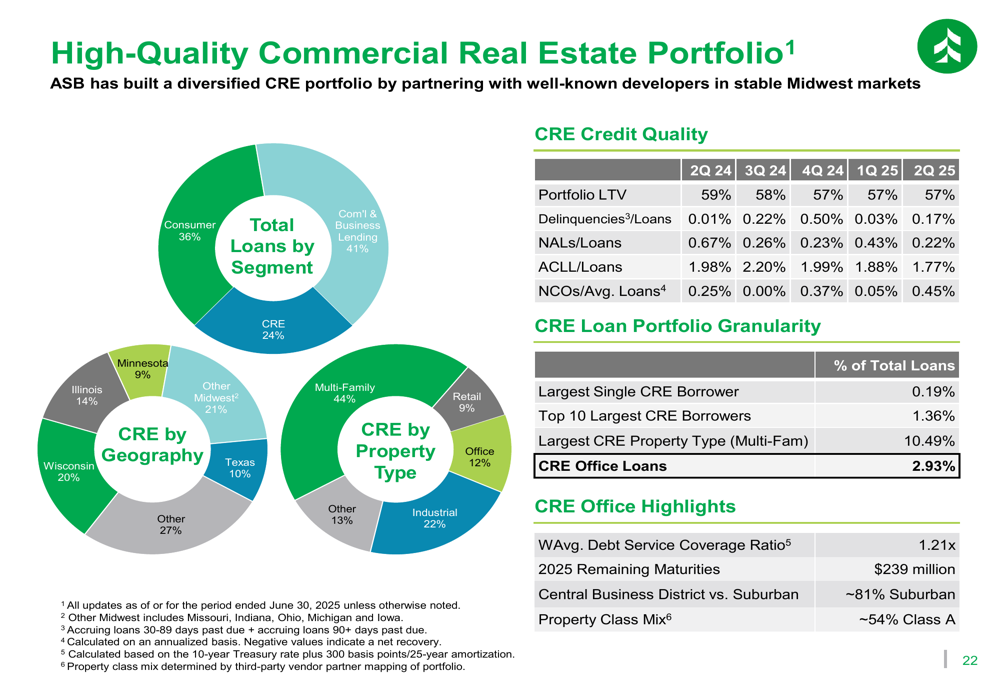

Associated Bank emphasized the quality of both its commercial real estate and consumer loan portfolios. The bank has built a diversified CRE portfolio by partnering with well-known developers in stable Midwest markets, with multi-family representing the largest property type at 44% of the CRE portfolio.

The following details highlight the quality of the commercial real estate portfolio:

On the consumer side, 93% of the $10.9 billion consumer loan portfolio is classified as prime or super prime, with strong weighted average FICO scores across all consumer loan categories. Residential mortgages represent the largest component of the consumer portfolio at $6.9 billion (22.7% of total loans).

Updated Outlook

Based on the strong performance in the first half of 2025, Associated Bank has updated its full-year 2025 guidance. The bank now expects total deposits to grow by 1% to 3%, up from the previous guidance of 1% to 2%. More significantly, net interest income is now projected to increase by 14% to 15%, compared to the previous guidance of 12% to 13%.

The bank maintained its guidance for total loan growth at 5% to 6%, core customer deposit growth at 4% to 5%, and its CET1 capital ratio target of 10% to 10.5%.

The following chart details the updated guidance compared to previous expectations:

Conclusion

Associated Banc-Corp’s Q2 2025 results demonstrate continued execution of its strategic initiatives, with improved profitability driven by net interest margin expansion and disciplined expense management. The bank’s strategic balance sheet repositioning has yielded positive results, as evidenced by the upward revision to its full-year guidance for net interest income growth.

With a strong capital position, stable credit quality, and high-quality loan portfolios, Associated Bank appears well-positioned to navigate the evolving interest rate environment while continuing to grow its business in its core Midwest markets. The increased guidance suggests management’s confidence in the bank’s ability to deliver improved financial performance through the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.