Bank of America just raised its EUR/USD forecast

Introduction & Market Context

Astec Industries Inc (NASDAQ:ASTE) delivered a strong start to 2025, reporting significant earnings growth in its first quarter presentation released on April 29. The company’s shares rose 3.03% in premarket trading to $36.34, building on momentum from its previous quarter’s performance.

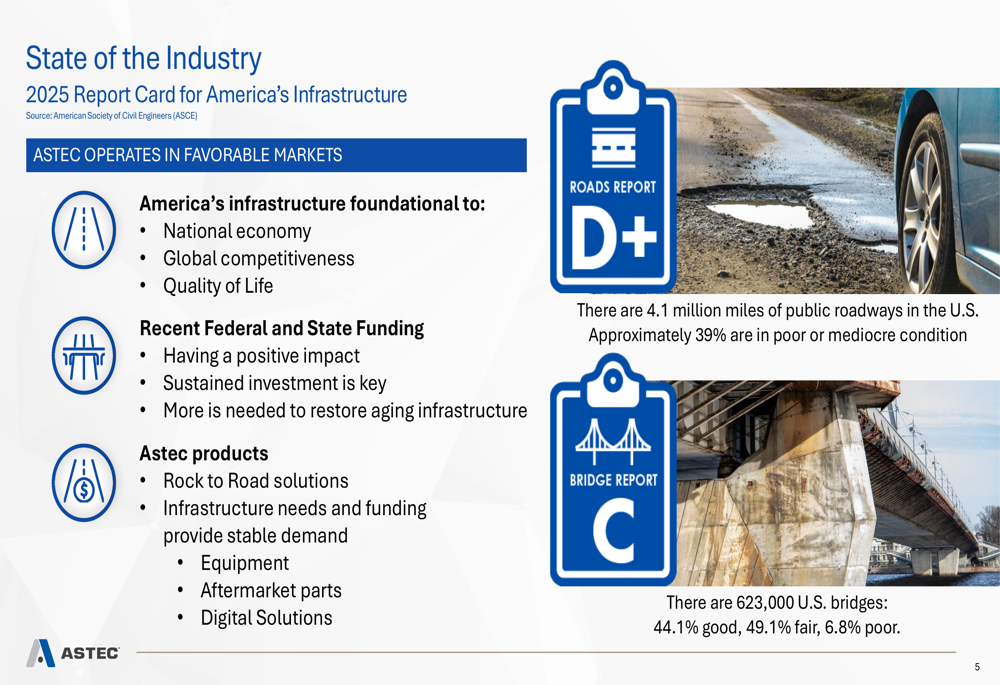

Operating in a favorable infrastructure market, Astec continues to benefit from federal and state funding initiatives aimed at addressing America’s aging infrastructure. The company’s presentation highlighted the 2025 Report Card for America’s Infrastructure from the American Society of Civil Engineers (ASCE), which gave roads a D+ grade and bridges a C grade, underscoring the substantial need for continued investment.

As shown in the following assessment of America’s infrastructure conditions:

Quarterly Performance Highlights

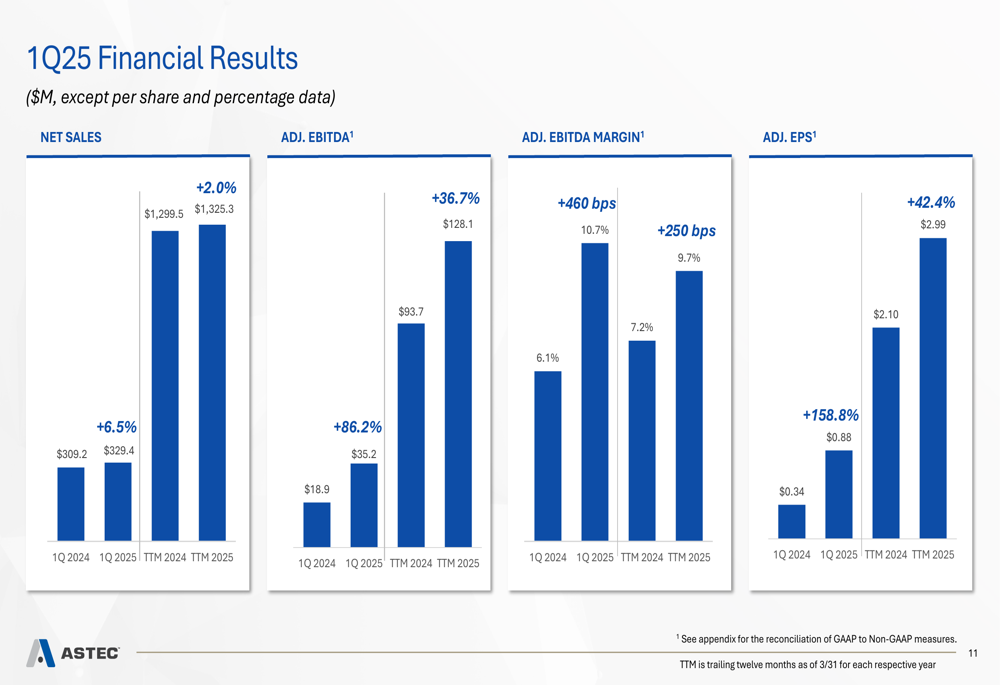

Astec reported impressive financial results for Q1 2025, with adjusted EBITDA surging 86.2% year-over-year to $35.2 million and adjusted EPS jumping 158.8% to $0.88. Net sales increased 6.5% to $329.4 million compared to the same period last year.

The company’s adjusted EBITDA margin expanded significantly to 10.7%, representing a 460 basis point improvement from Q1 2024. Free cash flow reached $16.6 million, representing 116% of net income, demonstrating strong operational efficiency and working capital management.

The following chart illustrates Astec’s key financial metrics for the quarter:

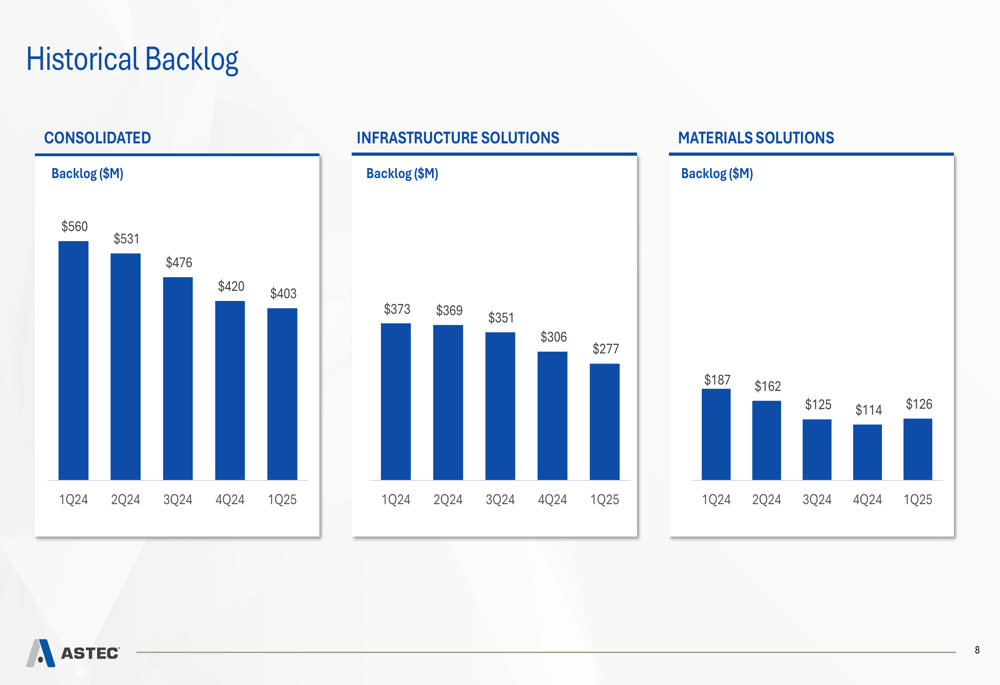

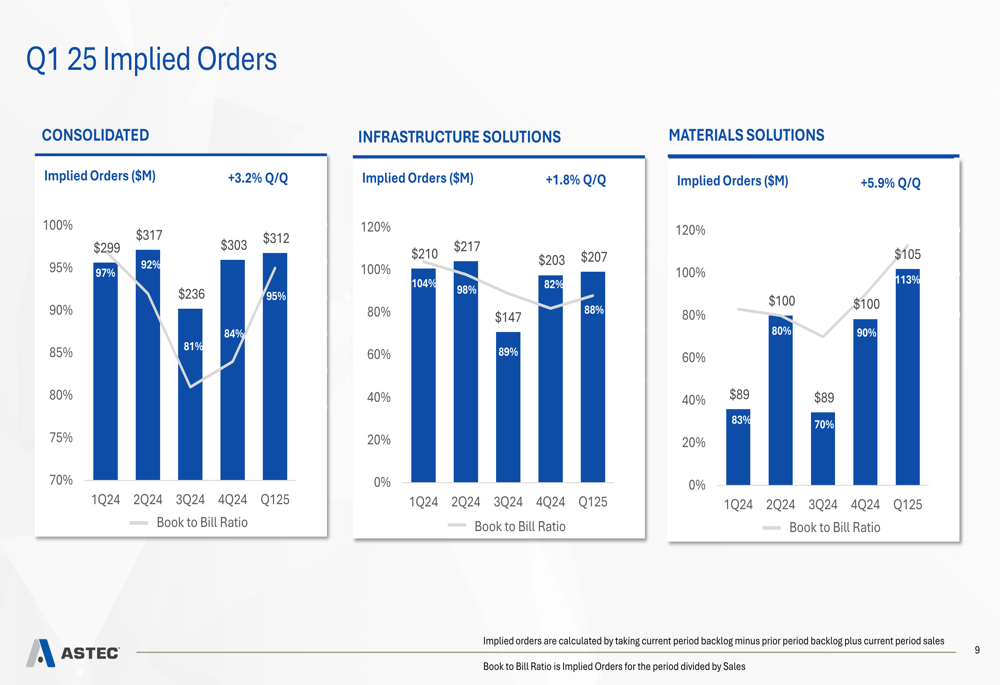

Despite strong financial performance, Astec’s consolidated backlog declined to $402.6 million, down from $560 million in Q1 2024. However, implied orders showed signs of stabilization, increasing 3.2% quarter-over-quarter to $312 million.

The historical backlog trend across segments is illustrated in this chart:

Implied orders, which represent new business coming into the company, showed improvement in Q1 2025 compared to the previous quarter:

Segment Performance Analysis

Astec’s performance revealed a tale of two segments, with Infrastructure Solutions delivering robust growth while Materials Solutions faced challenges.

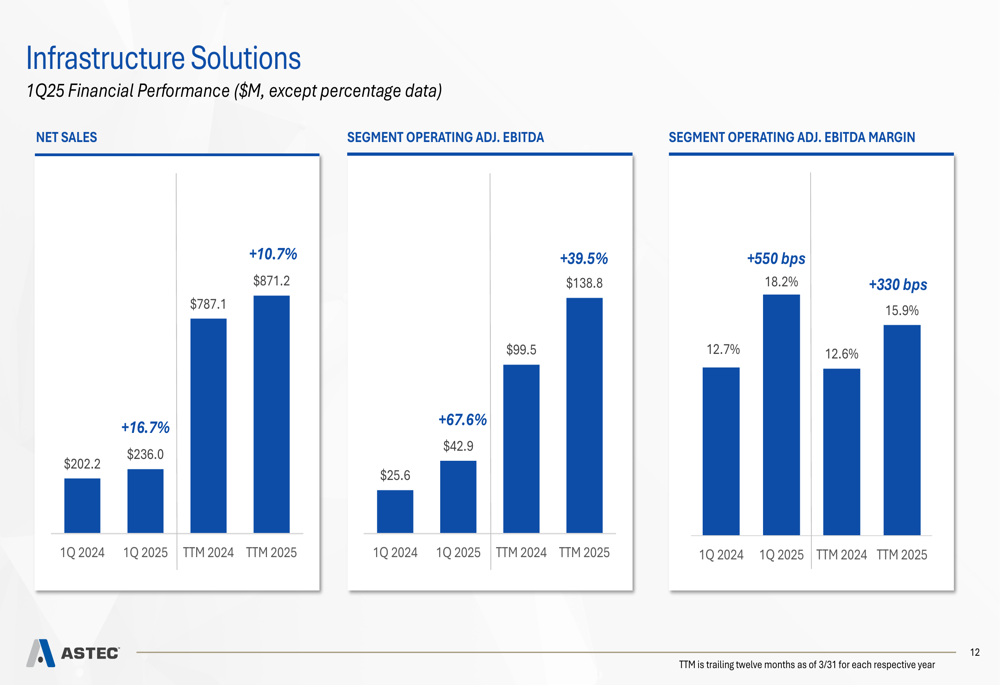

The Infrastructure Solutions segment, which includes asphalt and concrete plants, reported a 16.7% increase in net sales to $236.0 million. More impressively, the segment’s adjusted EBITDA jumped 67.6% to $42.9 million, with margins expanding 550 basis points to 18.2%. Management noted that the asphalt and concrete plant market remains strong, though some softness was observed in mobile paving and forestry.

The segment’s financial performance is detailed in the following chart:

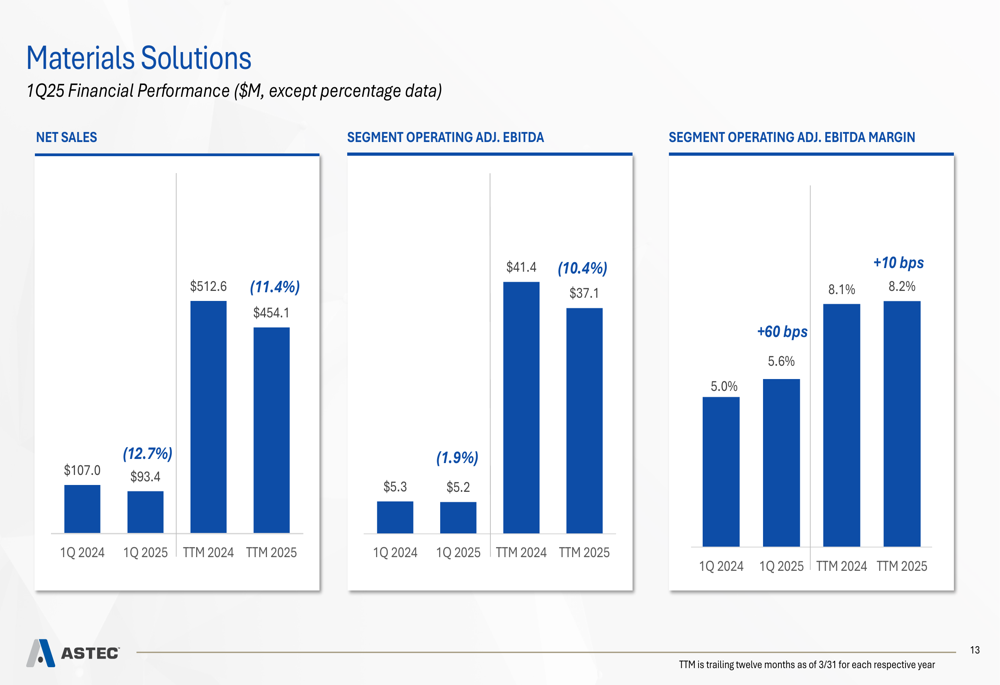

In contrast, the Materials Solutions segment, which includes crushing, screening, and material handling equipment, saw net sales decline 12.7% to $93.4 million. Despite the revenue drop, the segment maintained relatively stable adjusted EBITDA at $5.2 million, with margins actually improving by 60 basis points to 5.6%. Management attributed the segment’s challenges to continued dealer destocking and the impact of higher interest rates, though noted that backlog and implied orders improved in the quarter.

The Materials Solutions segment performance is illustrated here:

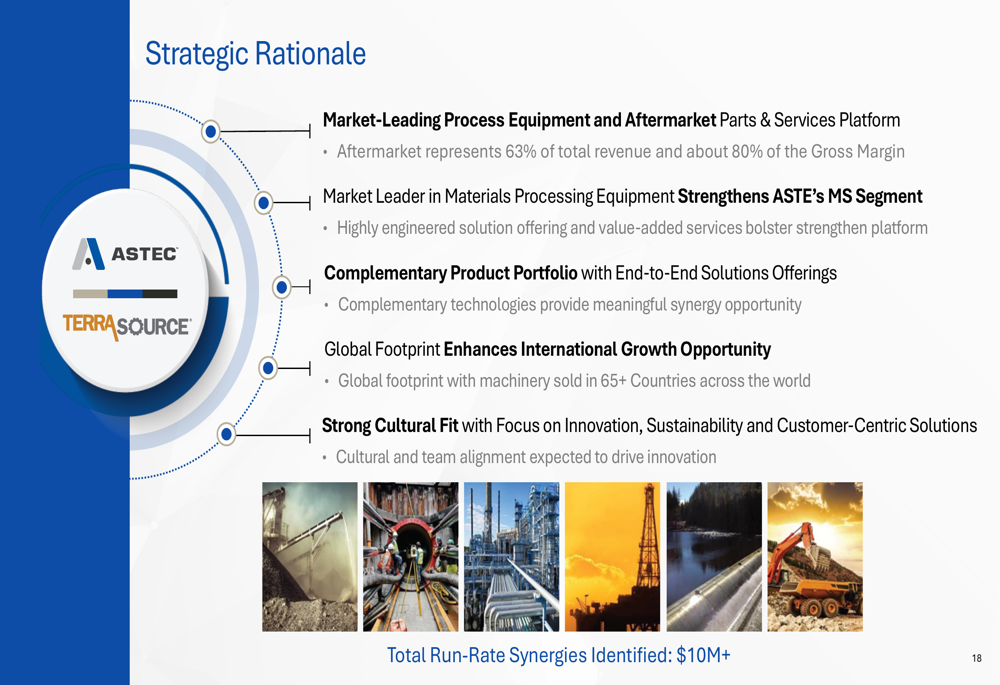

Strategic Acquisition of TerraSource

A major highlight of Astec’s presentation was the announcement of a definitive agreement to acquire TerraSource Holdings, LLC for $245 million in cash. The acquisition represents a strategic move to strengthen Astec’s Materials Solutions segment with complementary product offerings and a strong aftermarket business.

TerraSource is described as a portfolio of 100+ year-old trusted brands with a highly recurring aftermarket profile. The acquisition target generates revenue in excess of $150 million, with aftermarket parts and components representing approximately 52% of revenue and contributing about 80% of gross margin.

The strategic rationale for the acquisition is outlined in this comprehensive overview:

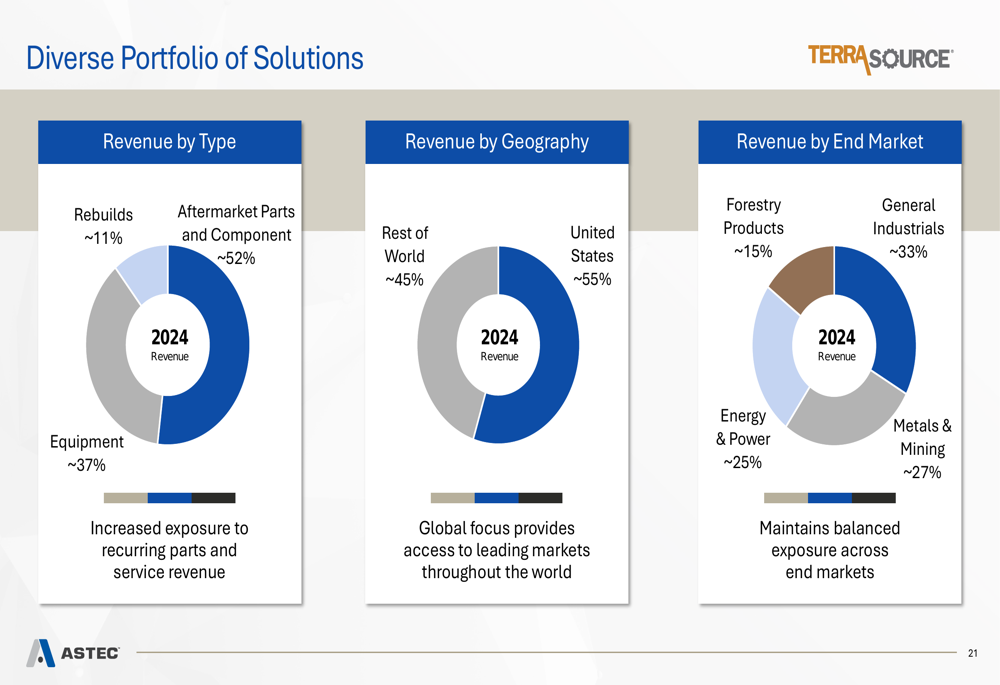

The acquisition is expected to diversify Astec’s revenue streams across various end markets and geographies. TerraSource derives approximately 55% of its revenue from the United States and 45% from international markets, with a customer base spanning forestry products, general industrials, energy & power, and metals & mining sectors.

This diversification is illustrated in the following breakdown:

Astec expects to realize approximately $10 million in annual run-rate synergies by the end of the second year following the acquisition. The transaction will be financed with existing cash and a Term Loan A, with an expected 2025 proforma net leverage ratio of approximately 2.0x net debt to adjusted EBITDA. The acquisition is anticipated to close by early Q3 2025 and is expected to be accretive to adjusted EPS in 2025.

Forward-Looking Statements

Looking ahead, Astec management expressed cautious optimism about the remainder of 2025. The company highlighted several growth drivers, including new product development, expansion of its recurring parts revenue (which consistently represents approximately 30% of total revenue), stable infrastructure funding, and international expansion opportunities.

Management also addressed potential challenges, including the impact of tariffs, for which the company has implemented several mitigation actions including proactive pricing strategies, dual/re-sourcing initiatives, and manufacturing footprint management.

CEO Jaco van der Merwe emphasized the company’s strong position in the infrastructure market during the presentation, noting that federal infrastructure funding and state/local budgets are expected to continue driving demand for Astec’s products and services.

With $238.9 million in total available liquidity as of March 31, 2025, including $90.1 million in cash and cash equivalents and $148.8 million in available credit, Astec appears well-positioned to fund its growth initiatives and navigate potential market challenges while integrating its significant acquisition.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.