Asia FX cautious amid US govt shutdown; yen tumbles after Takaichi’s LDP win

Introduction & Market Context

Astec Industries Inc (NASDAQ:ASTE) presented its second quarter 2025 earnings results on August 6, 2025, highlighting improved profitability despite revenue challenges in a mixed operating environment. The company’s stock responded positively to the earnings beat, with pre-market trading showing an 8.94% increase to $44, though it later settled at $39.38, representing a 2.5% decline from the previous close.

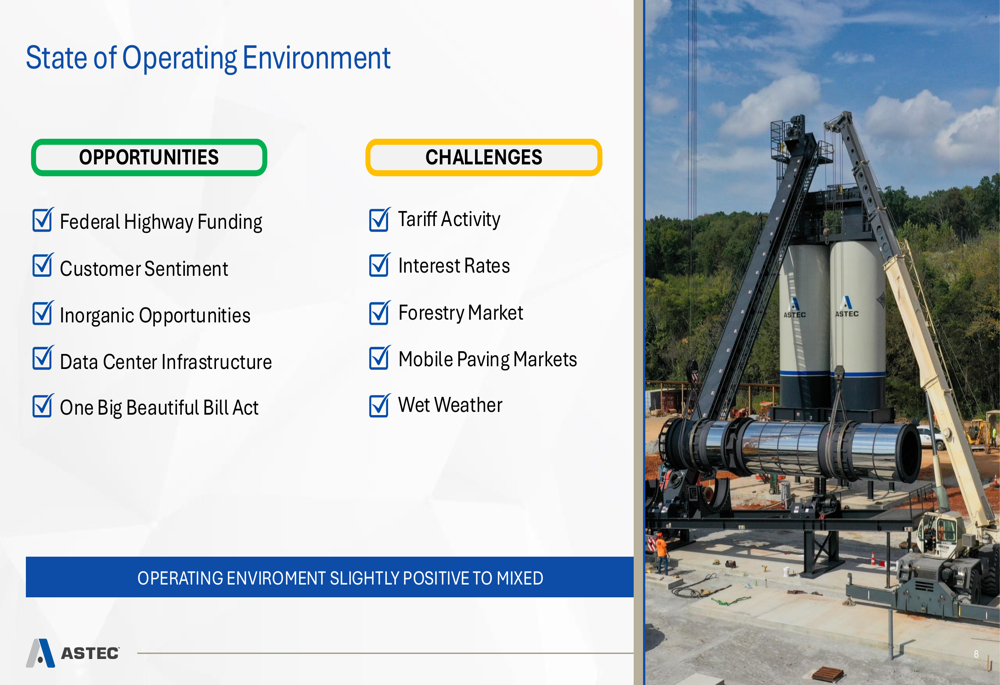

The infrastructure equipment manufacturer operates in what it describes as a "slightly positive to mixed" environment, balancing opportunities from federal infrastructure funding against challenges from interest rates, tariffs, and weather-related delays.

Quarterly Performance Highlights

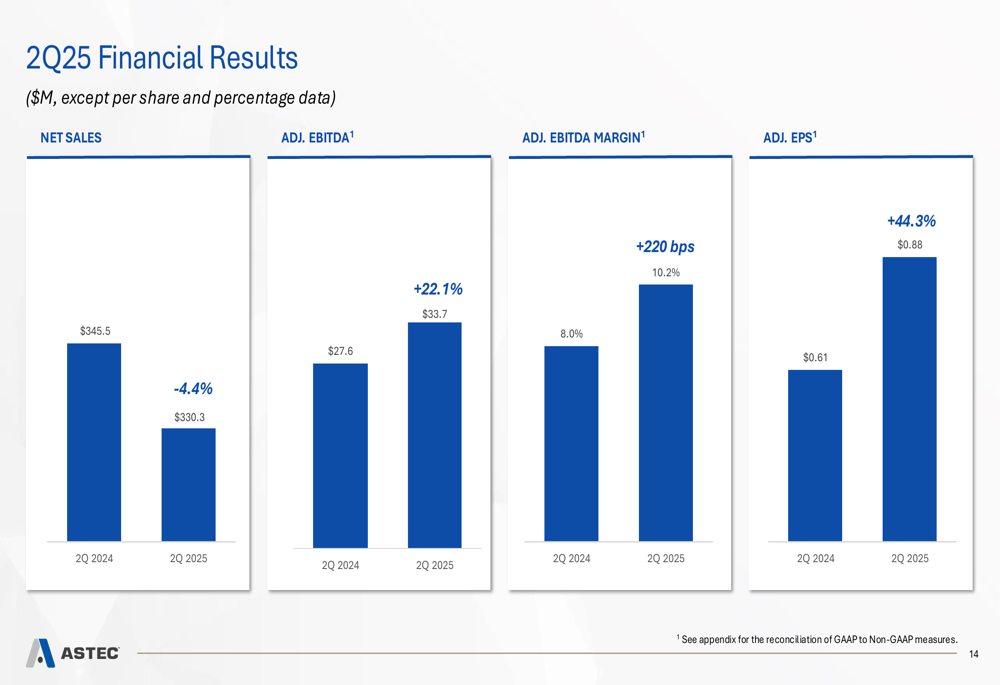

Astec reported second quarter net sales of $330.3 million, a 4.4% decrease from $345.5 million in the same period last year. Despite the revenue decline, the company achieved significant improvement in profitability metrics, with adjusted EBITDA increasing 22.1% to $33.7 million and adjusted EBITDA margin expanding 220 basis points to 10.2%.

As shown in the following chart of quarterly financial performance:

The company’s adjusted earnings per share reached $0.88, representing a 44.3% increase from $0.61 in Q2 2024 and significantly exceeding analyst expectations of $0.56. Free cash flow generation was $9.0 million, representing 53.9% of net income.

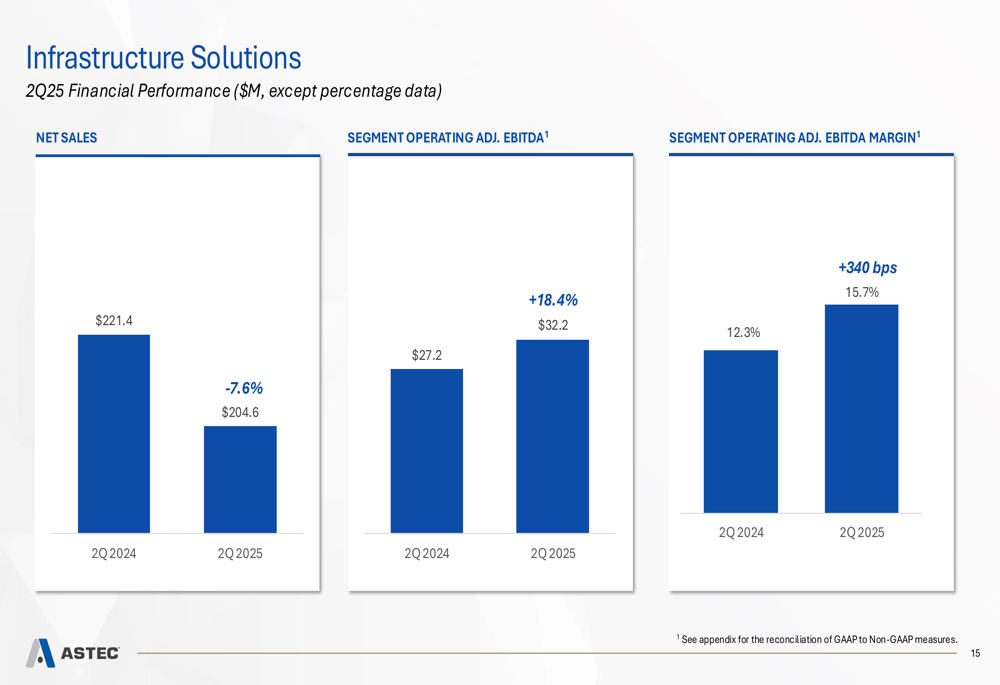

Segment performance showed divergent trends in revenue but consistent improvement in profitability. The Infrastructure Solutions segment, which includes asphalt and concrete plants, saw a 7.6% revenue decline to $204.6 million, but achieved an 18.4% increase in adjusted EBITDA to $32.2 million, with margins expanding 340 basis points to 15.7%.

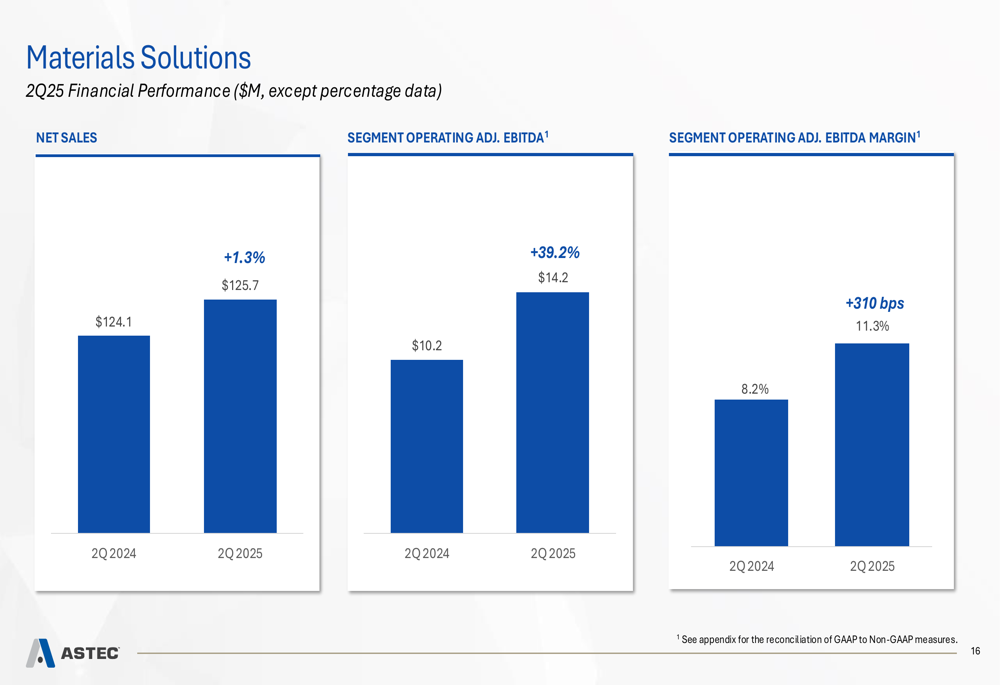

Meanwhile, the Materials Solutions segment, which includes crushing, screening, and material handling equipment, delivered a 1.3% revenue increase to $125.7 million and a 39.2% jump in adjusted EBITDA to $14.2 million, with margins improving 310 basis points to 11.3%.

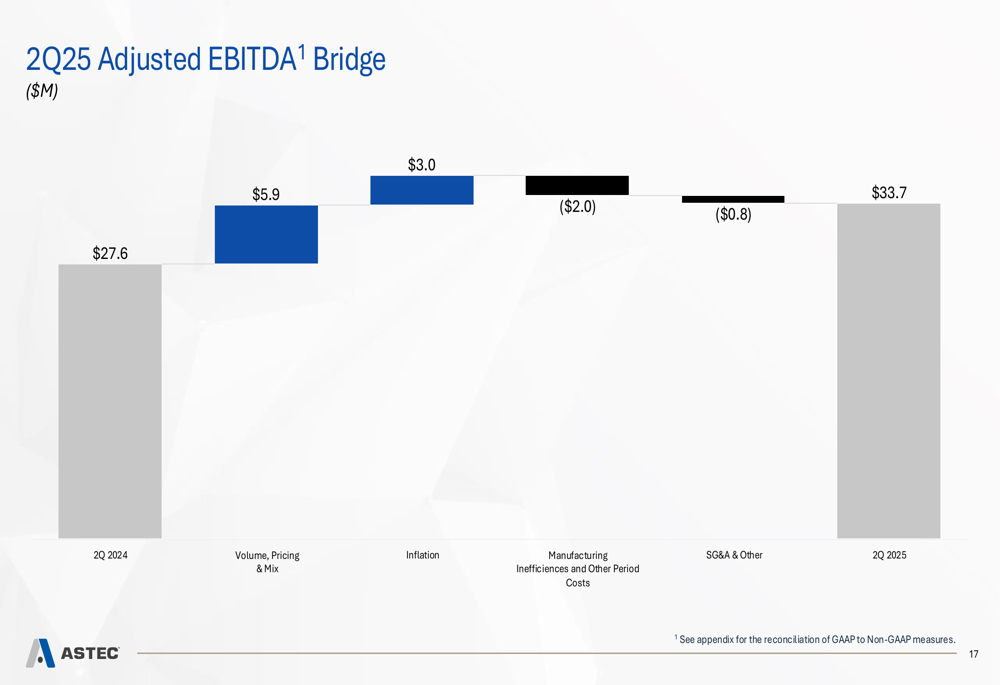

The company’s EBITDA bridge illustrates the factors contributing to the year-over-year improvement:

Strategic Initiatives

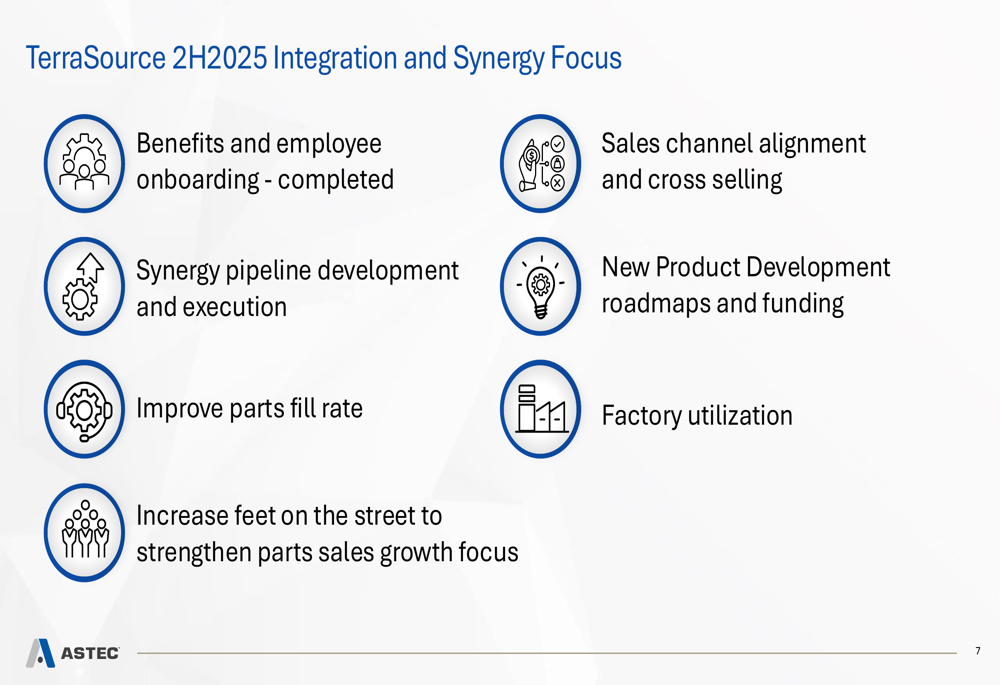

A key highlight of Astec’s presentation was the completed acquisition of TerraSource on July 1, 2025. This strategic addition brings several established brands under the Astec umbrella, including Gundlach Crushers, Peninsula Iron Works, Jeffrey Rader, Pennsylvania Crusher, and Elgin.

The company outlined a comprehensive integration plan for TerraSource in the second half of 2025, focusing on synergy development, sales channel alignment, new product development, and operational improvements:

The acquisition has prompted Astec to update its full-year adjusted EBITDA outlook to $123-142 million, incorporating the expected contribution from TerraSource. This represents an increase from the previous guidance range.

Market Environment and Outlook

Astec’s presentation provided a detailed assessment of the current operating environment, highlighting both opportunities and challenges. The company sees positive momentum from federal highway funding, customer sentiment, and data center infrastructure development, while facing headwinds from tariffs, interest rates, and weakness in specific markets.

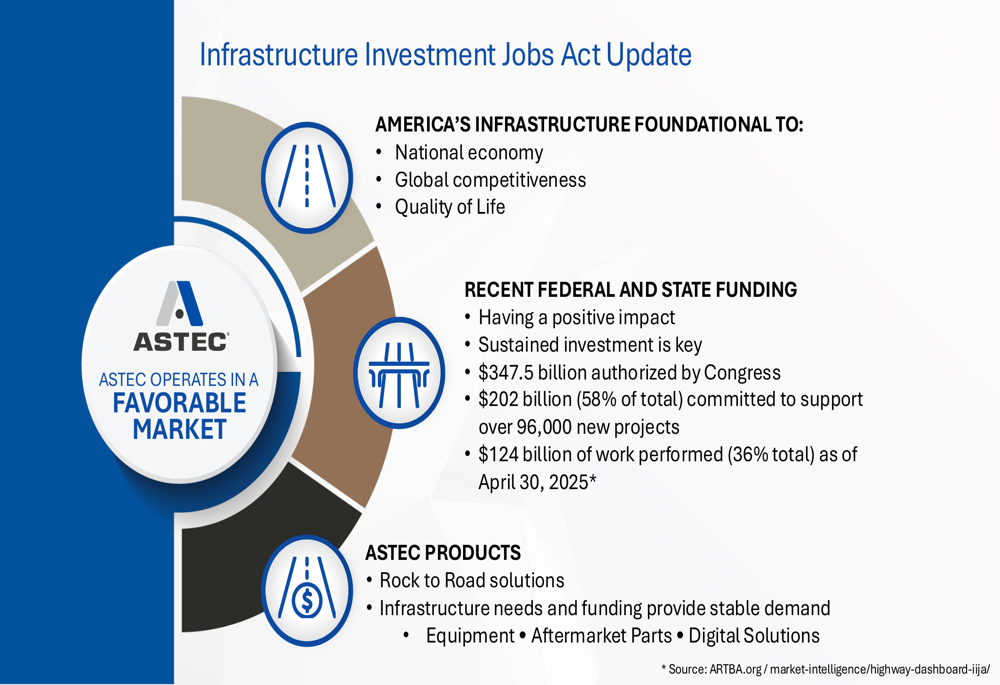

The company emphasized the importance of the Infrastructure Investment Jobs Act, noting that $202 billion (58% of the total $347.5 billion authorized) has been committed to support over 96,000 new projects, with $124 billion of work performed as of April 30, 2025.

To address tariff challenges, Astec has implemented a proactive mitigation strategy that includes procurement team negotiations, pricing strategies, dual sourcing, supply chain alignment, and manufacturing footprint management.

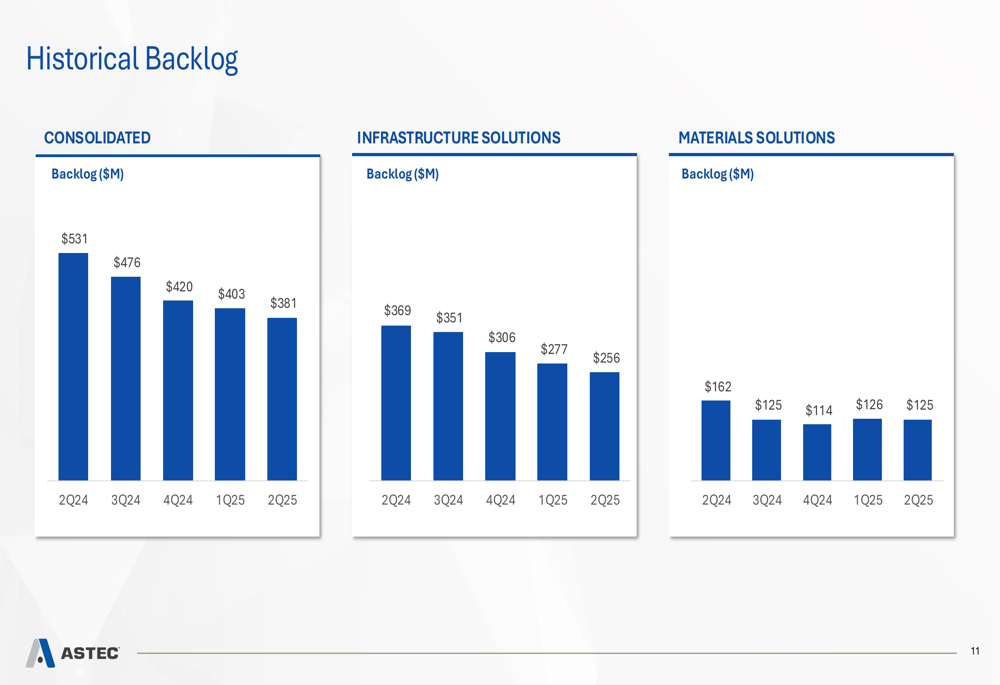

The company’s backlog stood at $380.8 million at the end of Q2 2025, continuing a declining trend over the past five quarters. However, implied orders in the Materials Solutions segment showed a 17.7% sequential improvement, suggesting potential stabilization.

Financial Position

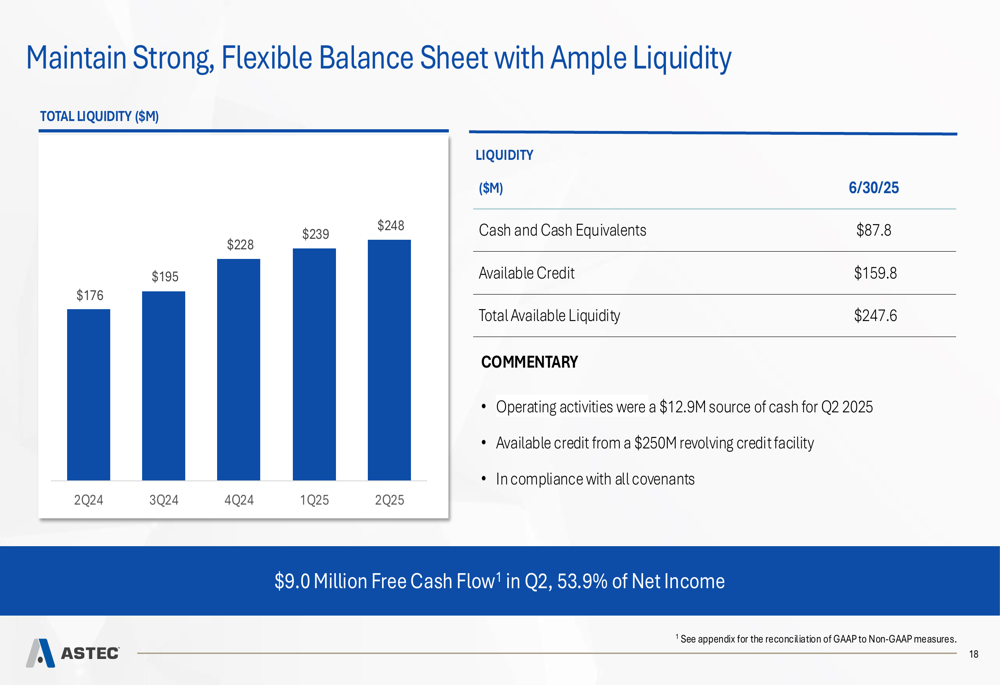

Astec maintained a strong balance sheet with ample liquidity, reporting total available liquidity of $247.6 million as of June 30, 2025, consisting of $87.8 million in cash and cash equivalents and $159.8 million in available credit.

The company generated $12.9 million in cash from operating activities during the quarter and remains in compliance with all debt covenants. This strong financial position provides flexibility for future growth investments while managing leverage.

Investment Highlights

Astec concluded its presentation by highlighting key investment strengths, including its trusted brand, favorable customer sentiment, operational excellence initiatives, and multiple growth drivers. The company emphasized its recurring parts revenue, which consistently represents approximately 30% of total revenue, as well as its new product pipeline and international expansion opportunities.

Looking ahead, Astec remains focused on executing its strategic initiatives while navigating the mixed market environment. The company’s ability to expand margins despite revenue challenges demonstrates operational discipline, while the TerraSource acquisition provides a platform for future growth. With a strong balance sheet and positive free cash flow generation, Astec appears well-positioned to capitalize on infrastructure spending while managing near-term market uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.