Uxin shares drop 45% as predicted by InvestingPro’s Fair Value model

Introduction & Market Context

Astec Industries Inc (NASDAQ:ASTE) presented its third quarter 2025 earnings results on November 5, 2025, showcasing significant year-over-year growth across key financial metrics. Despite beating analyst expectations with adjusted earnings per share of $0.47 (versus forecasted $0.45) and revenue of $350.1 million (versus expected $336 million), the company's stock fell 6.87% during the trading session, following a 2.61% decline in premarket trading.

The company's presentation highlighted its strongest third-quarter adjusted EBITDA margin performance since 2017, amid a generally positive but mixed operating environment characterized by stable infrastructure funding and improving customer sentiment, balanced against challenges from tariffs and specific market segments.

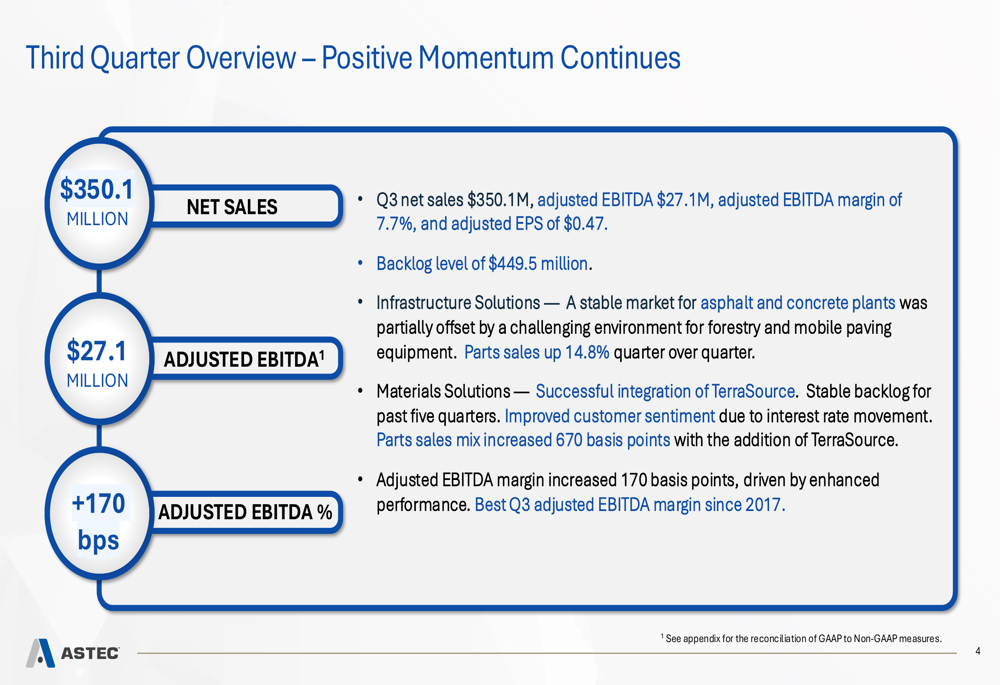

As shown in the following overview of third quarter performance:

Quarterly Performance Highlights

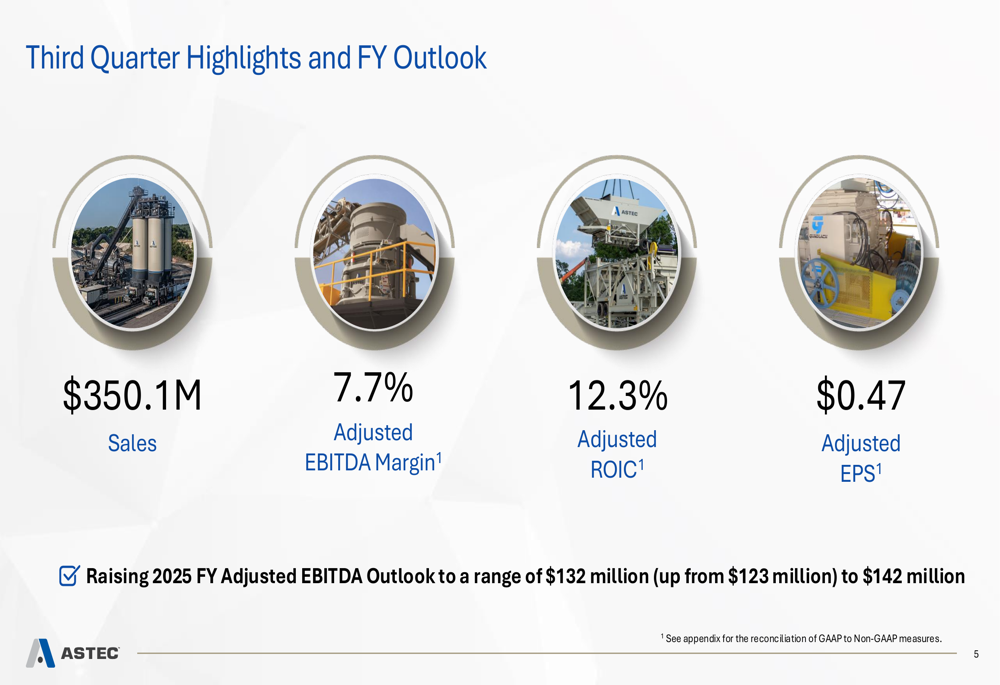

Astec reported Q3 2025 net sales of $350.1 million, representing a 20.1% increase compared to the same period in 2024. Adjusted EBITDA rose significantly to $27.1 million, up 55.7% year-over-year, while adjusted EBITDA margin expanded by 170 basis points to reach 7.7%. Adjusted earnings per share grew 30.6% to $0.47.

The company's backlog stood at $449.5 million, with consolidated organic implied orders increasing 1.9% quarter-over-quarter. These results prompted management to raise its full-year 2025 adjusted EBITDA outlook to a range of $132-142 million, up from the previous guidance of $123 million.

The following slide summarizes the third quarter highlights and updated outlook:

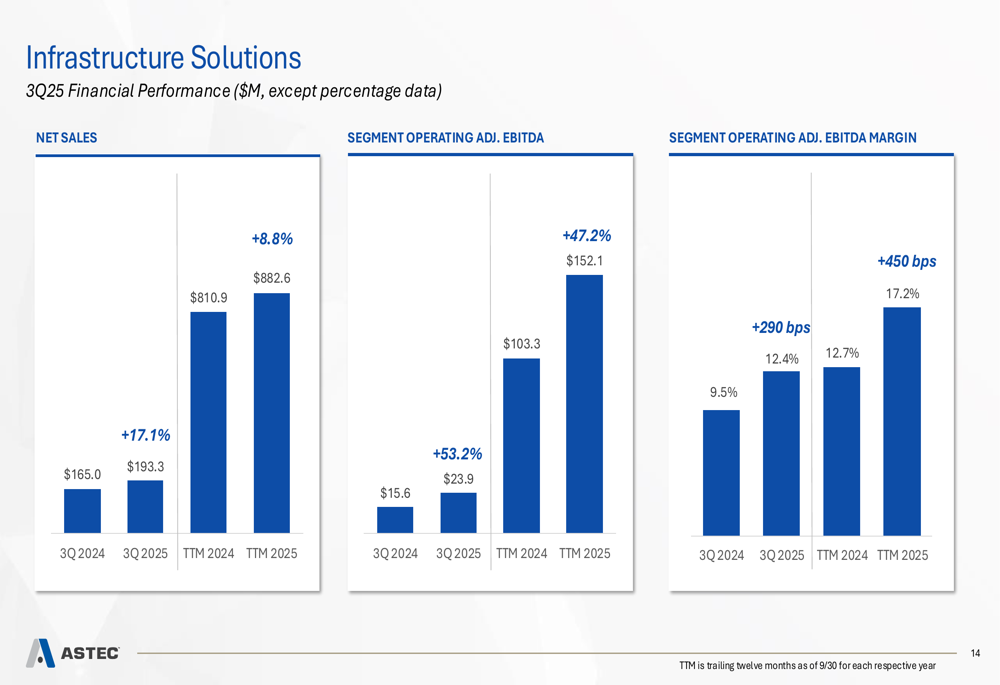

Segment performance was mixed, with Infrastructure Solutions showing particularly strong results. This segment, which includes asphalt and concrete plants, reported sales of $193.3 million (up 17.1%) and segment operating adjusted EBITDA of $23.9 million (up 53.2%), with margins expanding 290 basis points to 12.4%. The company noted that parts sales in this segment increased 14.8% quarter-over-quarter, helping to offset challenges in forestry and mobile paving equipment markets.

The detailed financial performance of the Infrastructure Solutions segment is illustrated here:

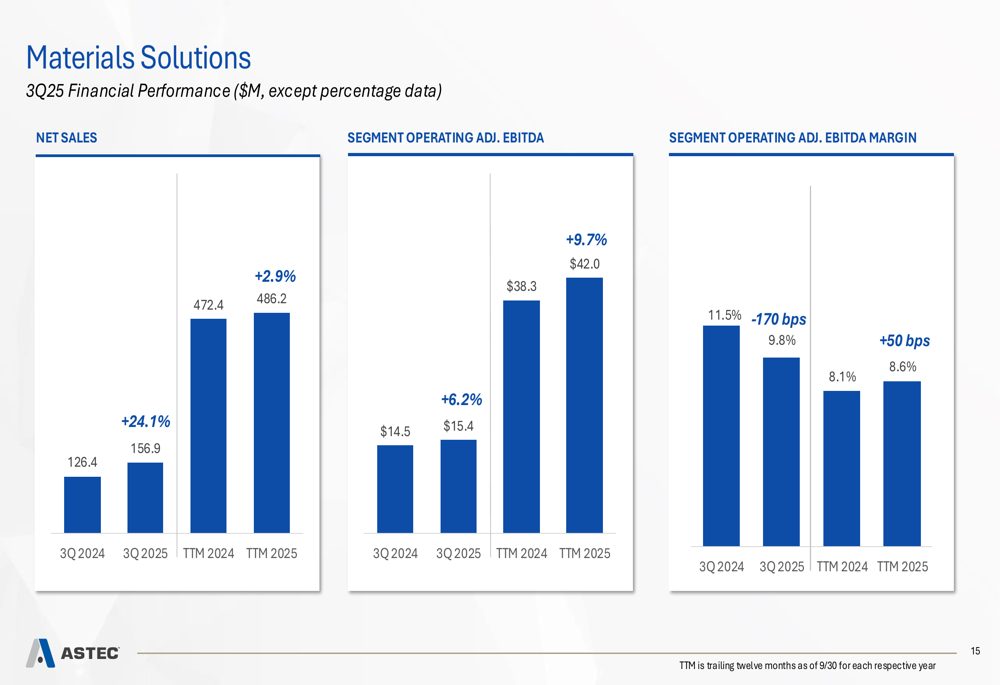

Meanwhile, the Materials Solutions segment, which includes crushing, screening, and material handling equipment, posted sales of $156.9 million (up 24.1%) but experienced a 170 basis point contraction in adjusted EBITDA margin to 9.8%. The segment's operating adjusted EBITDA increased by a more modest 6.2% to $15.4 million. The company attributed part of this growth to the successful integration of TerraSource, which contributed to a 670 basis point increase in parts sales mix.

The following chart details the Materials Solutions segment performance:

Strategic Initiatives

Astec's presentation emphasized several strategic initiatives driving its performance improvement. The integration of TerraSource, acquired earlier in 2025, is progressing according to plan, with completed employee onboarding and ongoing sales channel alignment and cross-selling efforts. The company has identified target projects for new product development and is making investments in high-turn inventory to enhance parts fill rates.

The company also outlined its proactive strategy to mitigate tariff impacts, which includes supplier negotiations, pricing adjustments, dual-sourcing beyond China to include India, and reshoring to the U.S. where feasible. Management acknowledged that "tariff negotiations are fluid and create an element of uncertainty for future periods" but expressed confidence in their ability to neutralize the impact.

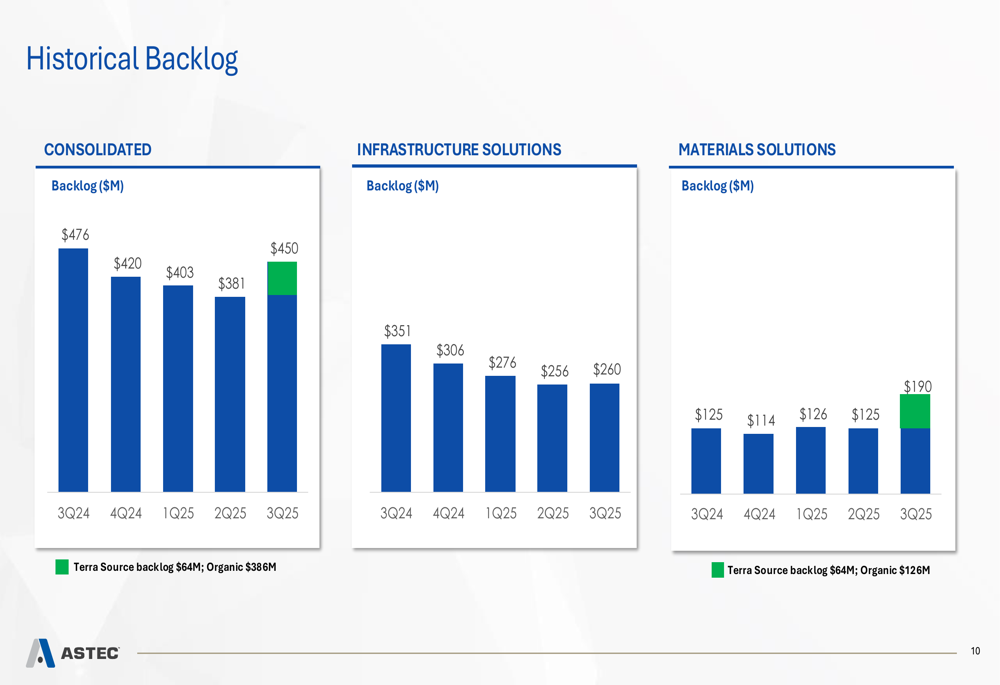

The company's backlog has remained relatively stable over recent quarters, with the addition of TerraSource contributing $64 million to the Materials Solutions backlog in Q3 2025. The consolidated backlog stood at $450 million, compared to $476 million in Q3 2024.

As shown in the historical backlog chart:

Astec maintained a strong financial position with total available liquidity of $312.1 million as of September 30, 2025, including $67.3 million in cash and cash equivalents and $244.8 million in available credit. The company's Net Debt/Adjusted EBITDA ratio was approximately 2.0x, within its target range of 1.5x to 2.5x.

Forward-Looking Statements

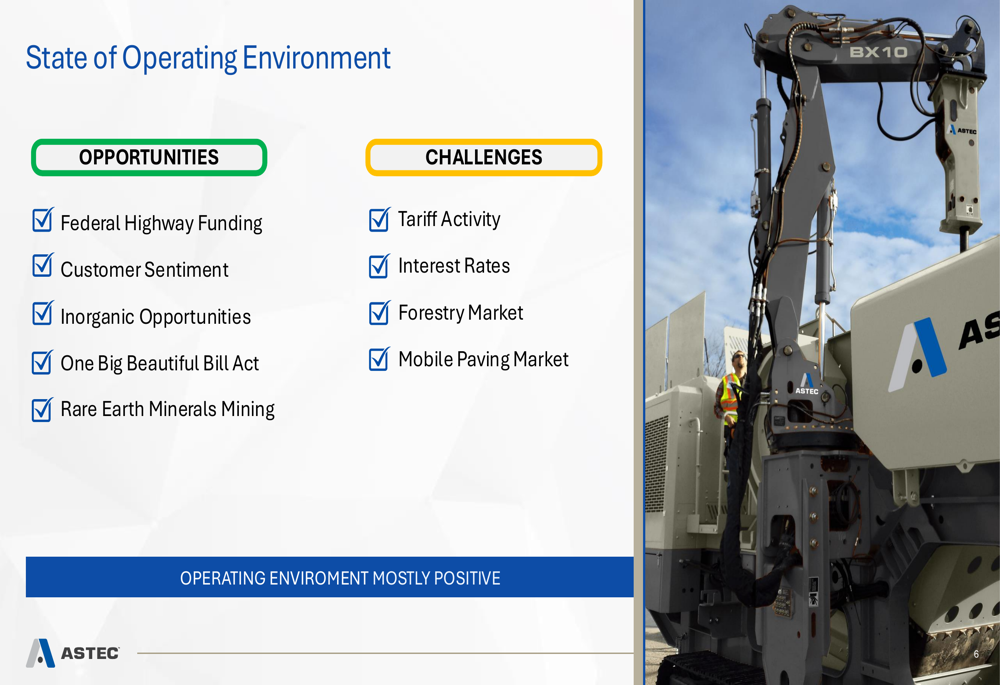

Looking ahead, Astec identified several opportunities and challenges in its operating environment. The Infrastructure Investment Jobs Act continues to provide a stable foundation for demand, with $230 billion (66% of the total $347.5 billion authorized by Congress) committed to support over 105,000 new projects. As of August 30, 2025, $150 billion of work had been performed, representing 44% of the total.

The company's assessment of the operating environment is illustrated in this slide:

CEO Jaco van der Merwe expressed satisfaction with the company's performance, stating, "We are pleased to drive enhanced year-over-year performance, resulting in a 170 basis point increase in our adjusted EBITDA margin, our best since the third quarter of 2017." He also highlighted the company's excitement about underlying market trends and the importance of having parts readily available to meet customer demand.

Despite the positive outlook, investors appeared cautious, as reflected in the stock's decline following the earnings release. The stock traded at $43.22, down 6.87% for the day, and remained below its 52-week high of $50.83, suggesting potential concerns about sustainability of growth or broader market factors affecting the construction equipment sector.

Astec emphasized its investment highlights, including its trusted brand position, operational excellence initiatives, and growth drivers such as recurring parts revenue (consistently representing approximately 30% of total revenue), new product innovations, stable infrastructure funding, international expansion opportunities, and potential for inorganic growth supported by its strong balance sheet.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.