Street Calls of the Week

Introduction & Market Context

Astrana Health Inc (NASDAQ:ASTH) released its second quarter 2025 earnings presentation on August 7, highlighting strong revenue growth but showing concerning trends in profitability metrics. The healthcare company, which focuses on value-based care arrangements, continues to expand its footprint while increasing its exposure to full-risk contracts.

The presentation comes at a challenging time for Astrana, with its stock trading near 52-week lows at $21.46, down significantly from its high of $63.20. The company’s shares fell 1.6% on the day of the earnings release, reflecting ongoing investor concerns following a disappointing Q1 2025 performance where the company missed both revenue and EPS expectations.

Quarterly Performance Highlights

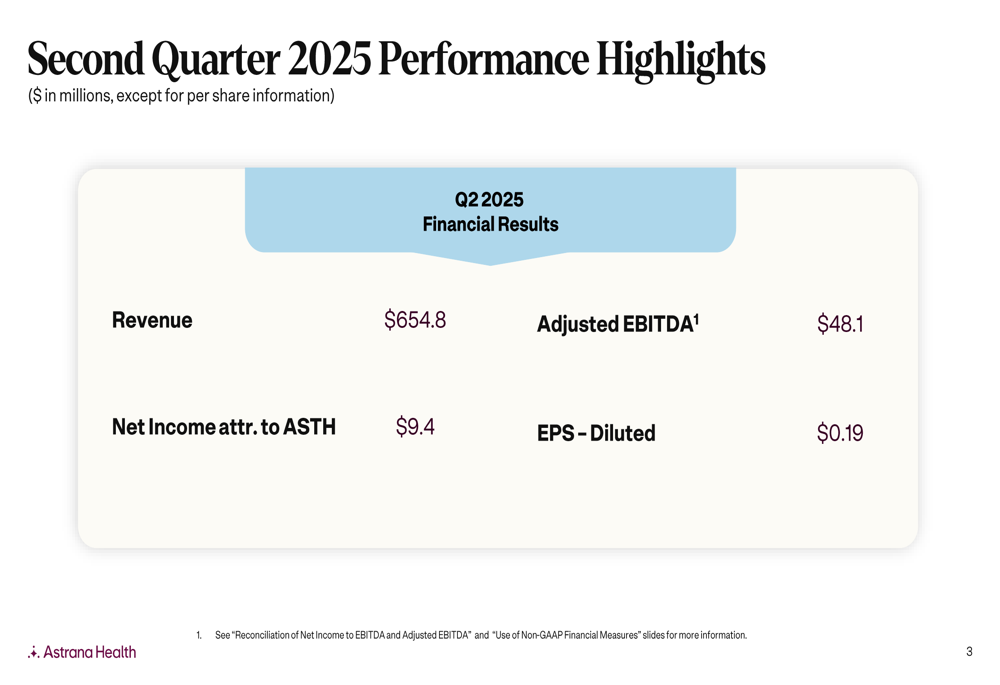

Astrana reported Q2 2025 revenue of $654.8 million, representing approximately 35% year-over-year growth compared to Q2 2024’s $486.3 million. However, profitability metrics showed concerning trends, with net income attributable to Astrana Health declining to $9.4 million from $19.2 million in the prior year period.

Diluted earnings per share fell to $0.19, less than half of the $0.40 reported in Q2 2024. Adjusted EBITDA remained relatively flat at $48.1 million compared to $47.9 million in the same quarter last year, though the adjusted EBITDA margin contracted to 7% from 10% a year ago.

As shown in the following performance highlights:

The company’s Care Partners segment, which represents the bulk of Astrana’s business, generated $631.4 million in revenue, a 36% increase year-over-year. Meanwhile, the Care Delivery segment grew 10% to $38.4 million, and Care Enablement increased 13% to $40.9 million.

Strategic Initiatives & Risk Progression

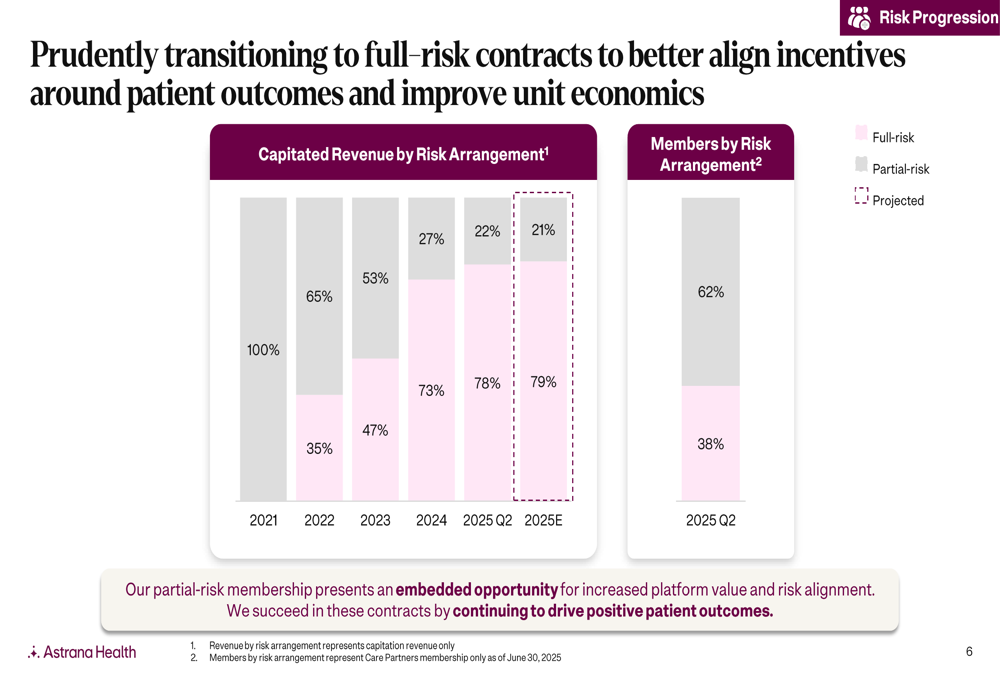

A central element of Astrana’s strategy is its continued shift toward full-risk value-based care arrangements. The company reported that 78% of its capitated revenue now comes from full-risk contracts, up from 60% a year ago and 75% in Q1 2025. This progression reflects Astrana’s commitment to assuming greater responsibility for total cost of care.

The following chart illustrates this strategic shift toward full-risk contracts:

Astrana recently completed its acquisition of Prospect, expanding its value-based care membership to over 1.6 million patients. The company expects to achieve $12-15 million in operating expense synergies from this transaction within 12-18 months.

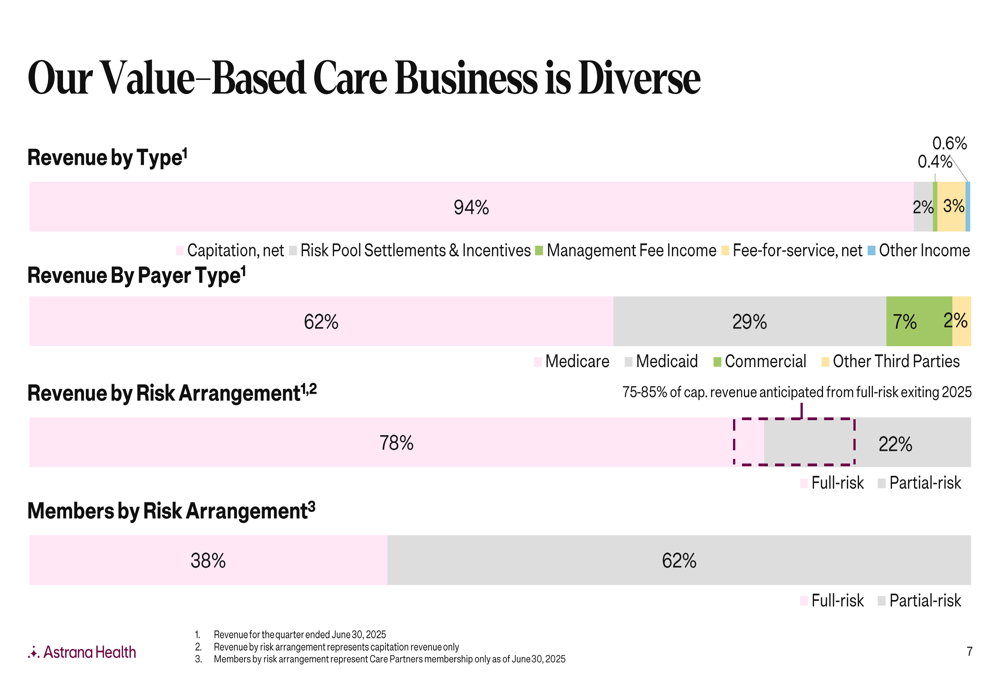

The company’s revenue mix demonstrates its focus on capitated arrangements and Medicare patients:

Astrana’s geographic footprint now spans 16 markets across the United States, with a network of more than 20,000 providers. The company highlighted its approximately 4.5% blended utilization trend across all lines of business, suggesting effective cost management despite taking on increased risk.

Detailed Financial Analysis

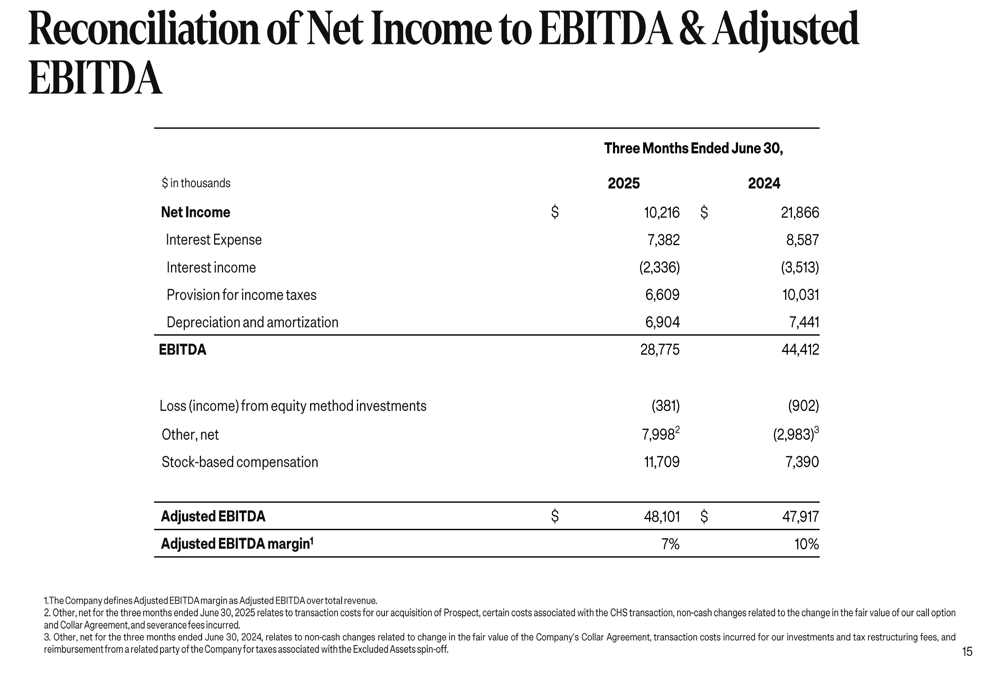

While Astrana’s top-line growth remains impressive, the company’s declining profitability metrics warrant closer examination. The reconciliation of net income to EBITDA and adjusted EBITDA reveals several adjustments that impact the company’s reported performance:

Net income for Q2 2025 was $10.2 million, less than half of the $21.9 million reported in Q2 2024. Despite this significant decline, adjusted EBITDA remained relatively flat year-over-year, primarily due to larger adjustments for provider bonus payments and losses from recently acquired IPAs.

The company’s balance sheet shows $342.1 million in cash and investments as of June 30, 2025, an increase from $290.8 million at the end of 2024. Total (EPA:TTEF) stockholders’ equity grew to $771.5 million from $716.7 million over the same period.

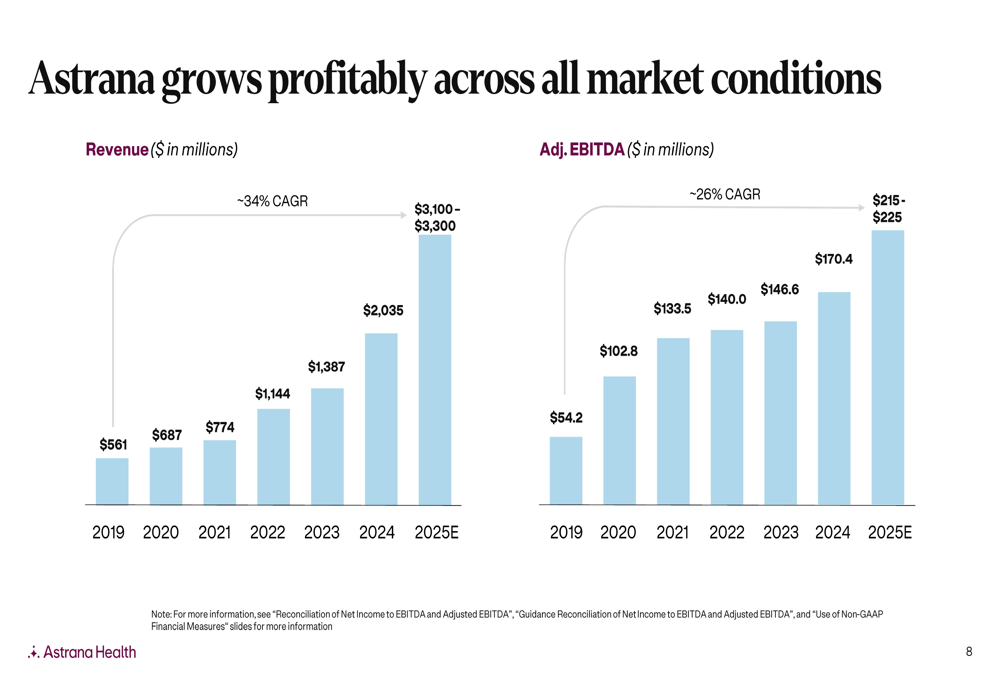

Astrana’s long-term growth trajectory remains impressive, as illustrated in the following chart:

Forward-Looking Statements & Guidance

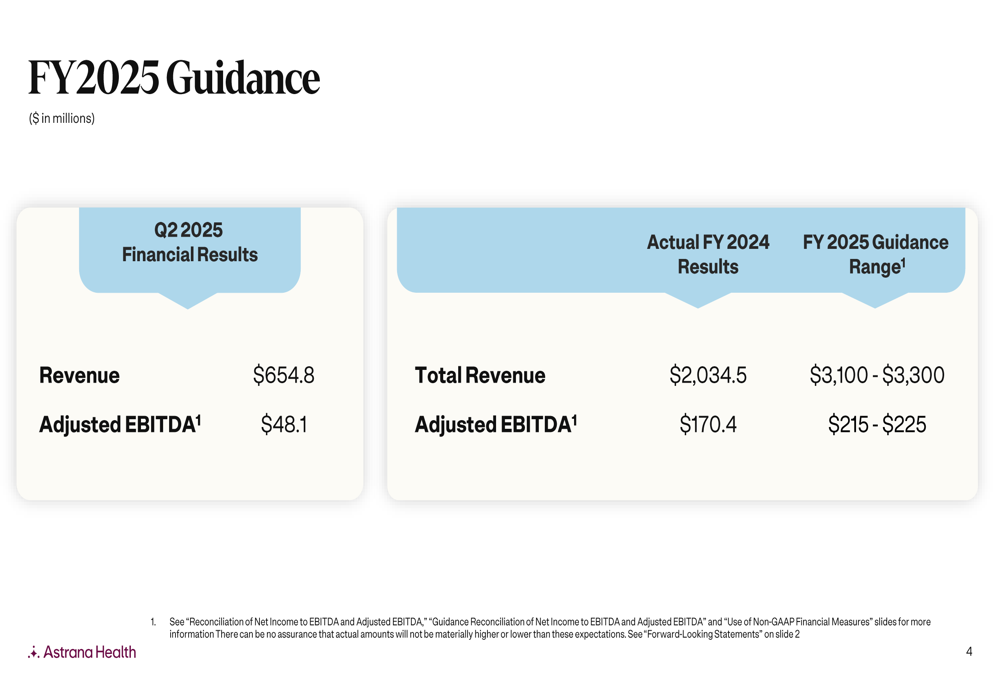

Astrana maintained its full-year 2025 guidance, projecting total revenue of $3.1-3.3 billion and adjusted EBITDA of $215-225 million. This represents significant growth from 2024’s actual results of $2.03 billion in revenue and $170.4 million in adjusted EBITDA.

The following slide details the company’s guidance compared to recent results:

The guidance implies continued strong revenue growth but also suggests that profit margin pressures may persist. The company expects to continue its shift toward full-risk arrangements, anticipating that 75-85% of capitation revenue will come from full-risk contracts by the end of 2025.

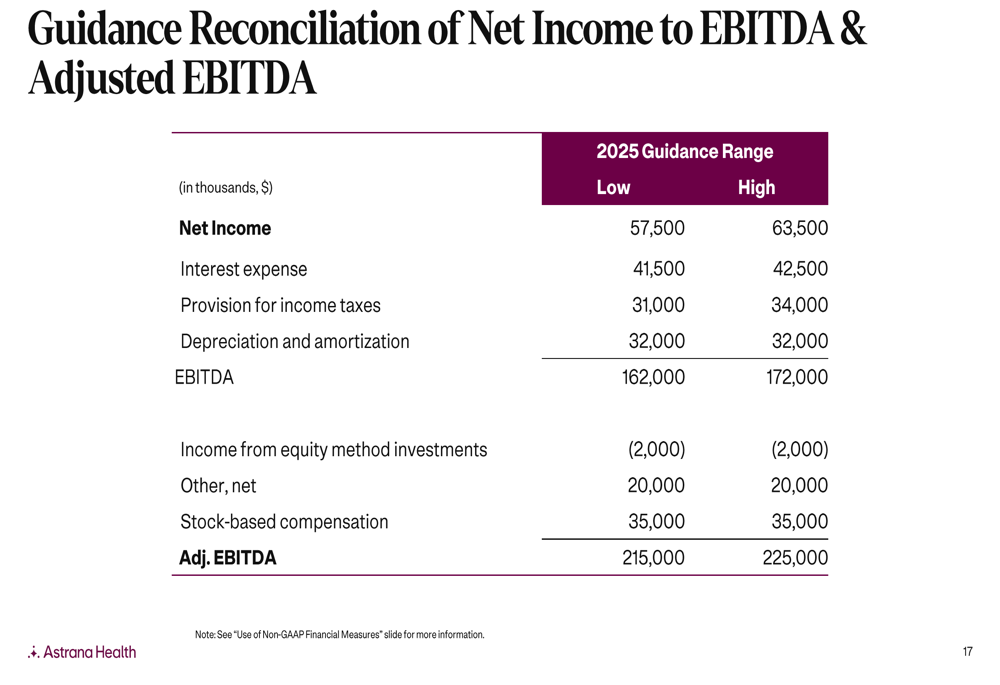

Astrana’s reconciliation of its 2025 guidance shows the bridge from projected net income to adjusted EBITDA:

The company faces several challenges going forward, including integration of the Prospect acquisition, managing the increased risk from full-risk contracts, and addressing the declining profit margins that have concerned investors. Following a disappointing Q1 2025 where EPS of $0.14 fell well short of the $0.30 forecast, Astrana will need to demonstrate improved execution to rebuild investor confidence.

Despite these challenges, management remains focused on its long-term strategy of expanding value-based care arrangements while managing costs effectively. The company’s continued investment in its Care Enablement suite aims to drive operating leverage across the business as it scales.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.