Tonix Pharmaceuticals stock halted ahead of FDA approval news

Introduction & Market Context

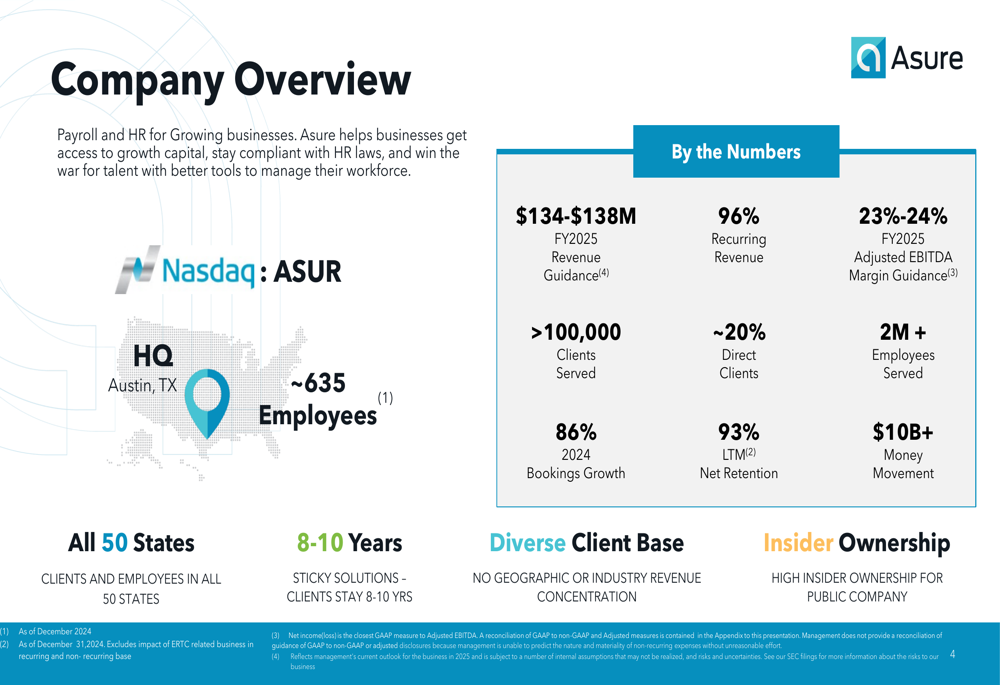

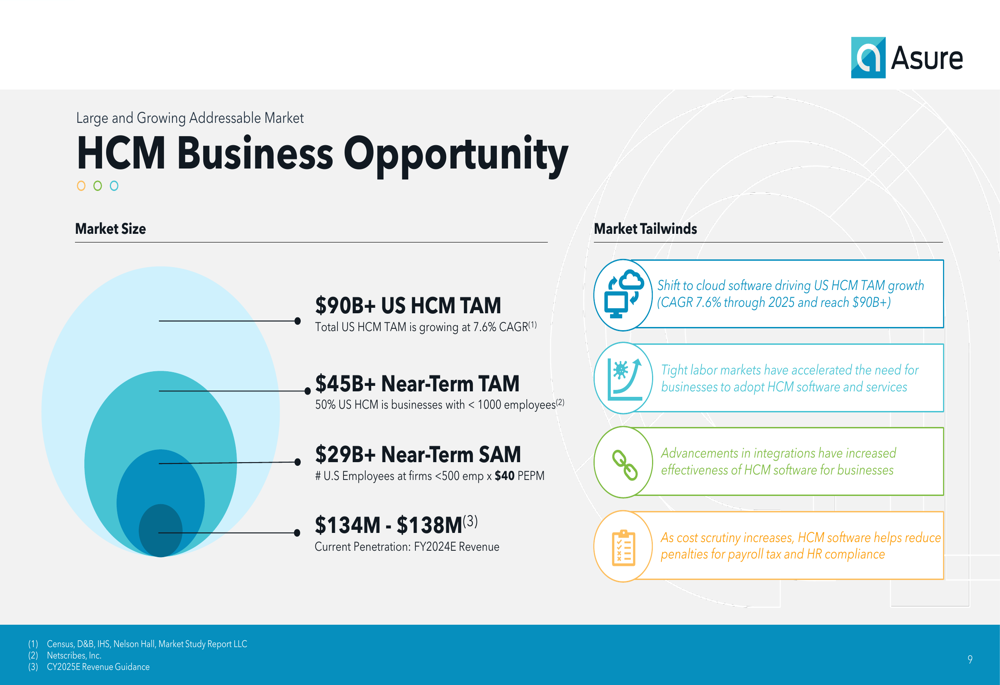

Asure Software Inc (NASDAQ:ASUR), a provider of payroll and HR solutions, presented its Q1 2025 investor slides on May 1, 2025, highlighting revenue growth while continuing to navigate profitability challenges. The company operates in the competitive Human Capital Management (HCM) market, which has a total addressable market of over $90 billion in the US and is growing at a 7.6% CAGR.

The presentation comes as Asure’s stock has faced pressure, with shares down 3.84% in regular trading and an additional 4.28% decline in after-hours trading on May 1, closing at $9.40. This follows a disappointing Q4 2024 earnings report where the company missed EPS expectations.

As shown in the following overview of the company’s position in the market:

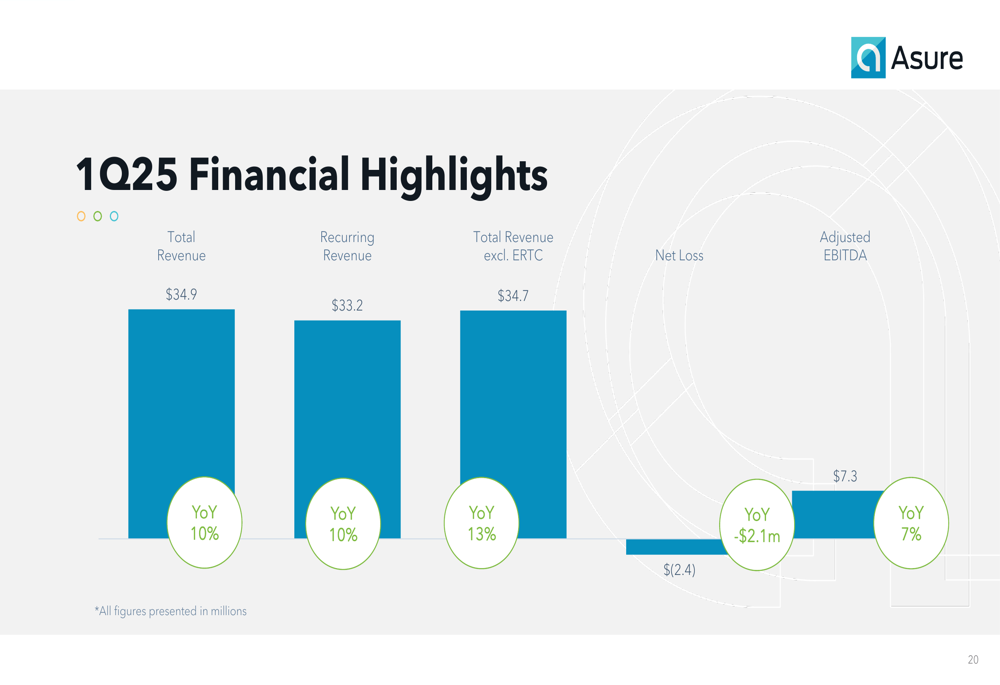

Quarterly Performance Highlights

Asure reported Q1 2025 revenue of $34.9 million, representing a 10% year-over-year increase. Recurring revenue, which now accounts for 96% of total revenue, grew at the same 10% rate to $33.2 million. However, the company posted a net loss of $2.1 million for the quarter.

Chairman and CEO Pat Goepel highlighted the company’s growth in its Payroll Tax Management product and recent acquisitions. He also noted that the contracted revenue backlog rose 339% compared to the first quarter of 2024, signaling potential future revenue growth.

The financial highlights for the quarter demonstrate the company’s revenue growth alongside continued profitability challenges:

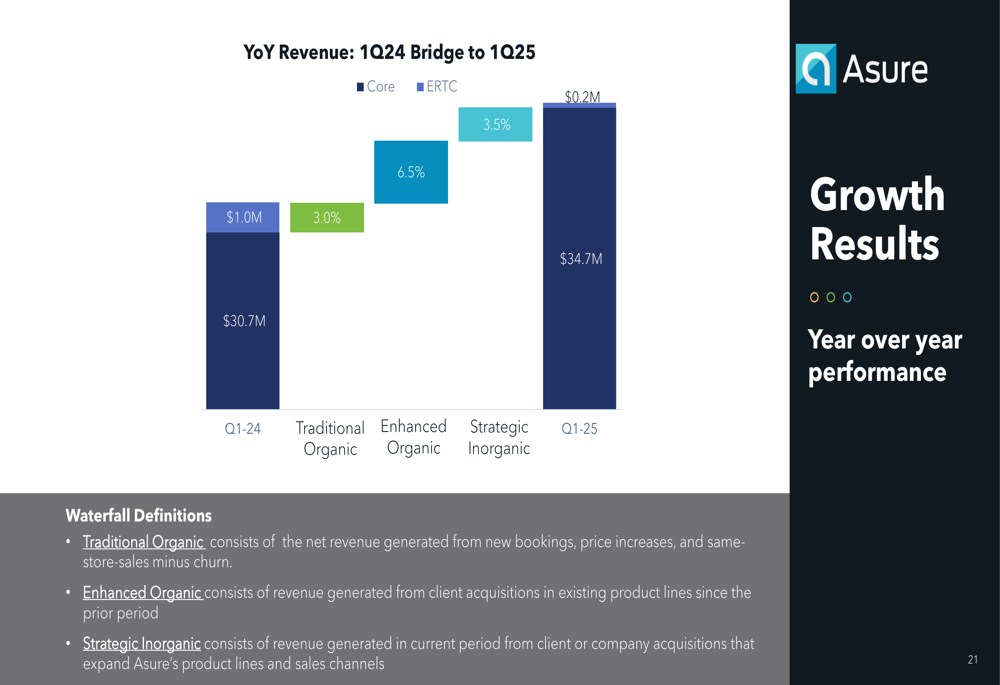

A closer look at the year-over-year revenue bridge reveals the sources of Asure’s growth:

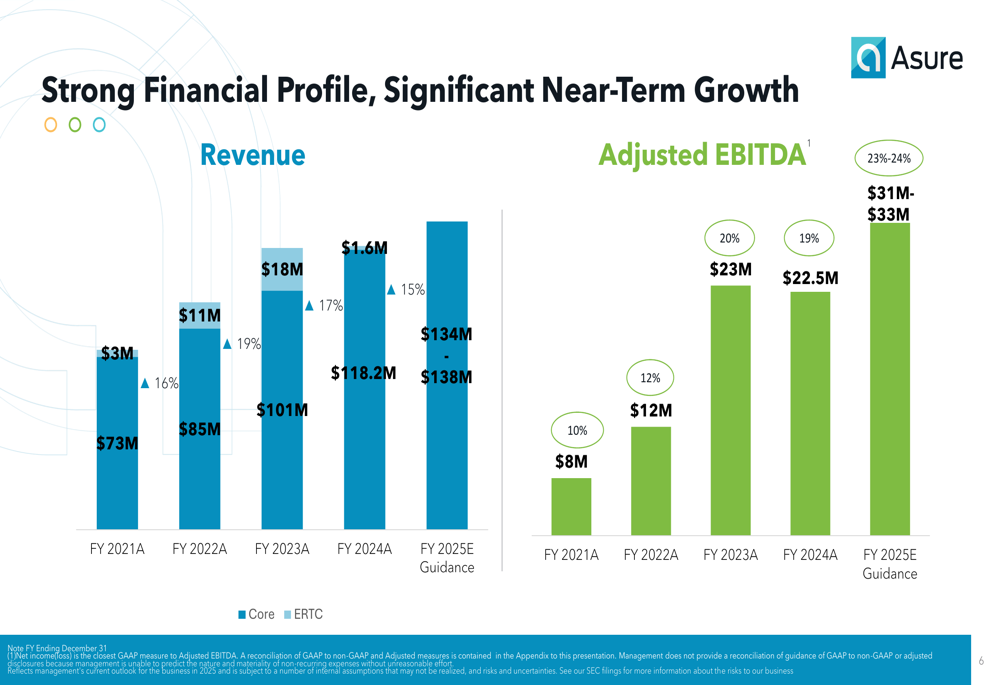

The company’s longer-term financial trajectory shows consistent revenue growth from $73 million in FY 2021 to a projected $134-138 million for FY 2025. Similarly, adjusted EBITDA is expected to grow from $8 million in FY 2021 to $31-33 million in FY 2025:

Strategic Growth Initiatives

Asure outlined a three-pronged approach to growth in its presentation. The strategy encompasses traditional organic growth through sales and marketing, enhanced organic growth by elevating reseller client relationships, and strategic inorganic growth through mergers and acquisitions.

The company recently completed a credit facility for up to $60 million to support potential acquisitions, demonstrating its commitment to the inorganic growth component of its strategy.

As illustrated in the following strategic framework:

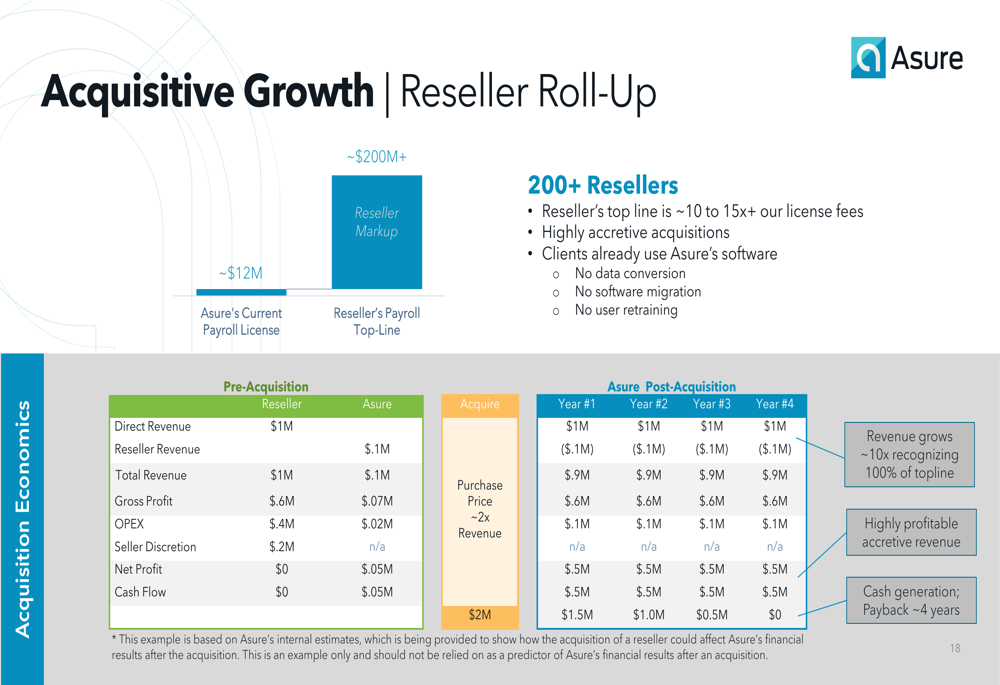

A key element of Asure’s acquisition strategy involves rolling up resellers. According to the company, acquiring resellers can grow revenue approximately 10x by recognizing 100% of topline revenue, resulting in highly profitable accretive revenue with a payback period of around four years:

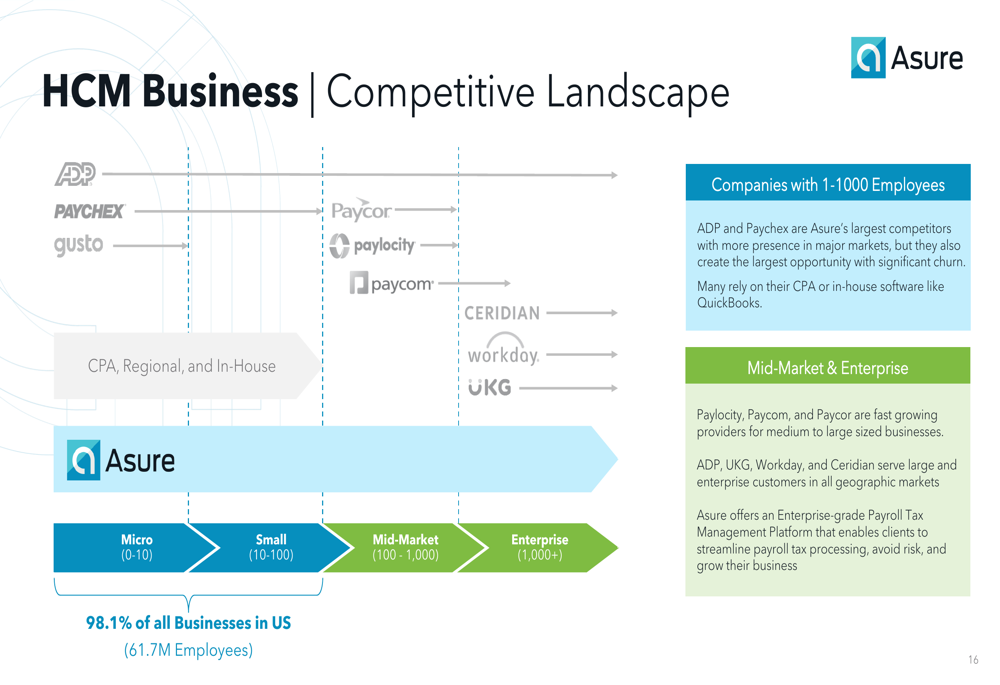

Competitive Industry Position

Asure positions itself in a competitive HCM landscape that includes major players like ADP, Paychex (NASDAQ:PAYX), Paycor (NASDAQ:PYCR), Paylocity (NASDAQ:PCTY), and Paycom (NYSE:PAYC). The company differentiates itself with an Enterprise-grade Payroll Tax Management Platform that enables clients to streamline payroll tax processing, avoid risk, and grow their business.

The company notes that 98.1% of all businesses in the US are small businesses, representing 61.7 million employees, which aligns with Asure’s target market. According to the presentation, approximately 60% of new clients come from trusted advisors (brokers, banks, and CPAs), while 40% come from direct sales and marketing efforts. Notably, ADP and Paychex churn represents over 50% of Asure’s new clients.

The following image illustrates Asure’s competitive positioning:

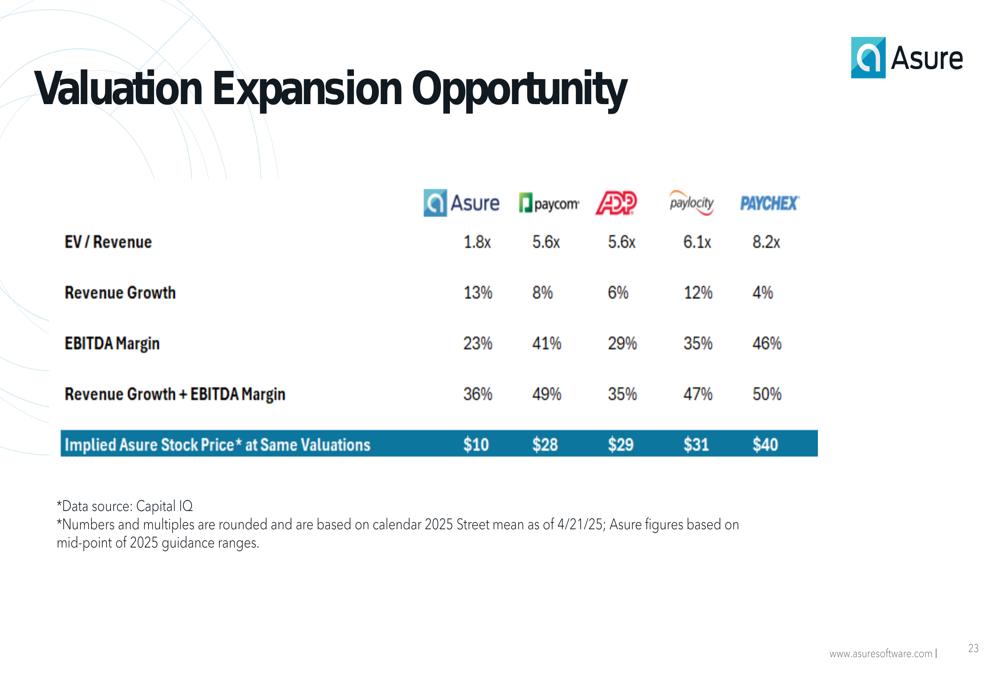

When comparing valuation metrics with competitors, Asure suggests significant upside potential if it were to trade at similar multiples to its peers:

Forward-Looking Statements

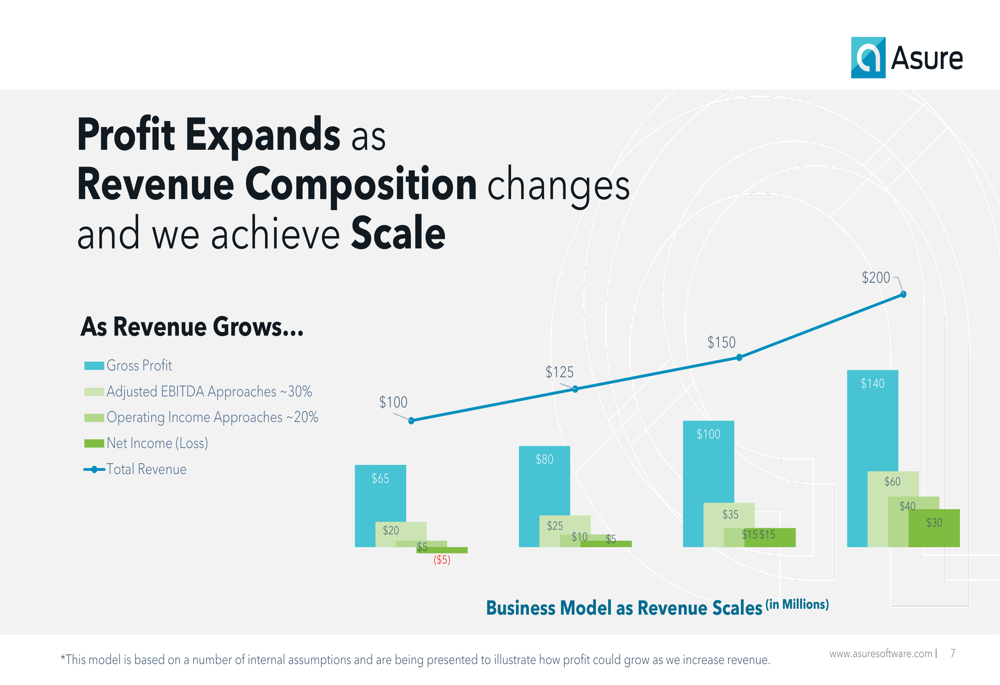

Looking ahead, Asure has provided revenue guidance of $134-138 million for FY 2025, representing mid-teens growth compared to FY 2024. The company is targeting adjusted EBITDA margins of 23-24% for the year.

The company’s long-term model suggests that as revenue scales from $100 million to $200 million, adjusted EBITDA margins could approach 30%, with operating income reaching approximately 20% of revenue and net income turning positive:

Asure also highlighted market tailwinds supporting its growth strategy, including the shift to cloud software, tight labor markets, advancements in integrations, and increasing cost scrutiny driving HCM software adoption:

While Asure’s presentation paints an optimistic picture of growth and future profitability, investors should note the contrast with recent financial performance, including the Q4 2024 earnings miss and continued net losses. The company’s ability to execute on its three-pronged growth strategy while improving profitability will be critical to achieving its ambitious financial targets for 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.