Aspire Biopharma faces potential Nasdaq delisting after compliance shortfall

Introduction & Market Context

Atea ASA (OB:ATEA), a leading Nordic IT infrastructure provider, presented its Q2 2025 financial results on July 16, 2025, demonstrating strong growth across most markets despite regional challenges. The company reported significant increases in sales and profitability, maintaining its position as a key player in the Nordic IT sector with a market capitalization of approximately $1.56 billion.

The presentation highlighted Atea’s continued expansion in strategic sectors, particularly defense and cybersecurity, while leveraging opportunities in artificial intelligence and the upcoming Windows 10 end-of-life cycle. The stock responded positively to the results, with a modest 1.02% increase following the announcement, closing at 158.6 NOK.

Quarterly Performance Highlights

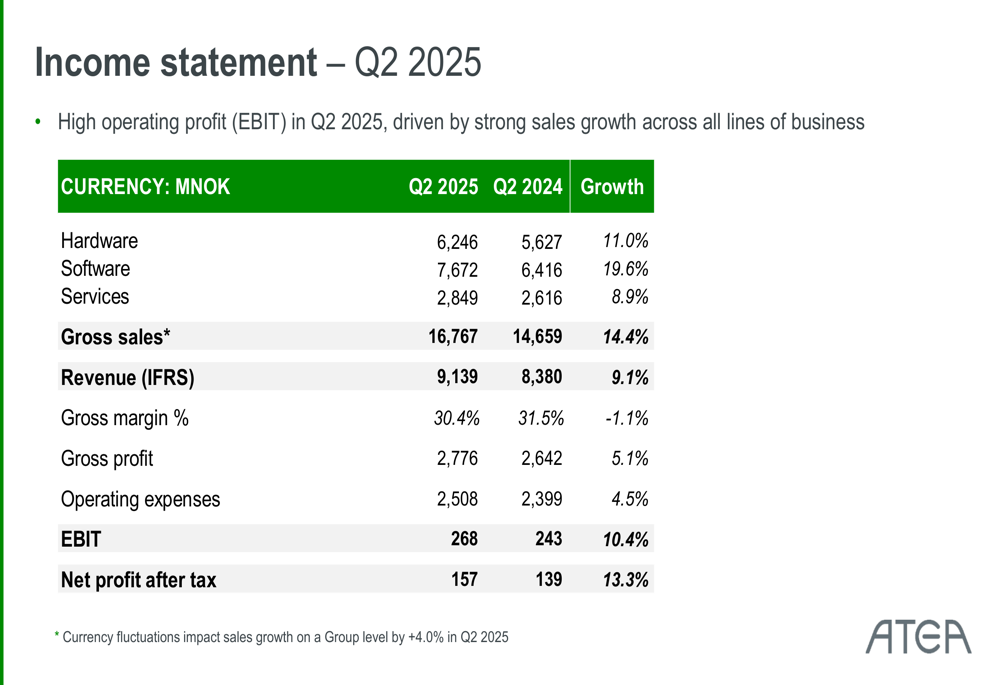

Atea reported robust financial results for Q2 2025, with gross sales reaching NOK 16.8 billion, representing a 14.4% increase compared to the same period last year. Revenue (IFRS) grew by 9.1% to NOK 9.1 billion, while EBIT rose 10.4% to NOK 268 million. Net profit showed the strongest growth at 13.3%, reaching NOK 157 million.

As shown in the following quarterly highlights chart, all key financial metrics demonstrated positive growth compared to Q2 2024:

Breaking down the revenue streams, software sales led the growth at 19.6%, followed by hardware at 11.0% and services at 8.9%. The company’s gross margin decreased slightly by 1.1 percentage points to 30.4%, while operating expenses increased by 4.5% compared to the same period last year.

The detailed income statement provides further insight into the company’s financial performance:

Regional Performance Analysis

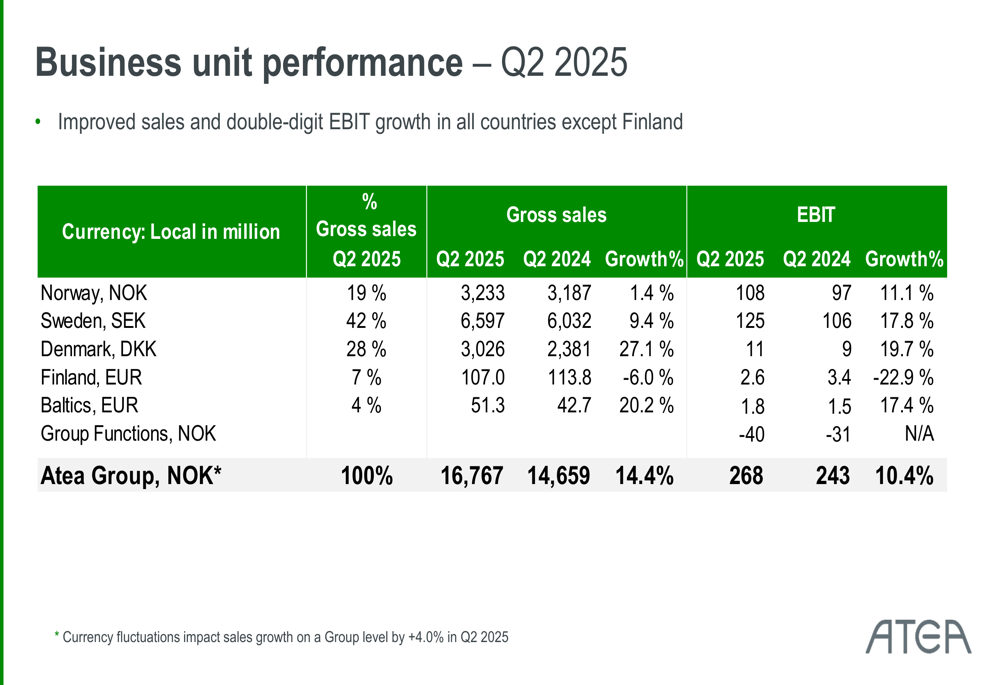

Atea’s performance varied significantly across its regional markets. Denmark emerged as the standout performer with 27.1% growth in gross sales, followed by the Baltics at 20.2% and Sweden at 9.4%. Norway showed modest growth at 1.4%, while Finland was the only region to experience a decline, with gross sales dropping by 6.0% and EBIT falling by 22.9%.

The following business unit performance breakdown illustrates these regional variations:

Sweden remains Atea’s largest market, accounting for 42% of gross sales, followed by Denmark (28%) and Norway (19%). Despite representing only 4% of sales, the Baltics showed strong growth momentum at 20.2%, indicating potential for future expansion in this region.

The company’s workforce remained relatively stable, with a slight decrease from 8,098 to 7,967 full-time employees compared to June 2024. Sweden saw the largest reduction in headcount (-94 employees), while other regions maintained similar staffing levels.

Financial Position & Cash Flow

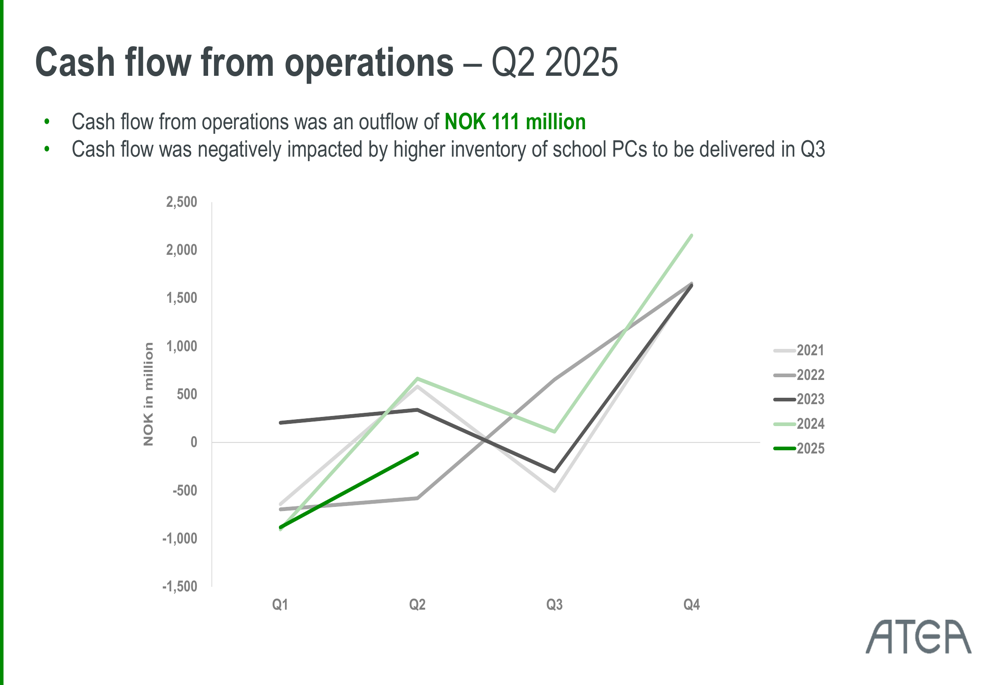

Atea reported a negative cash flow from operations of NOK 111 million in Q2 2025, which the company attributed to higher inventory of school PCs scheduled for delivery in Q3. This represents a departure from the company’s typically positive cash flow pattern in recent years.

The following chart illustrates the company’s cash flow trends:

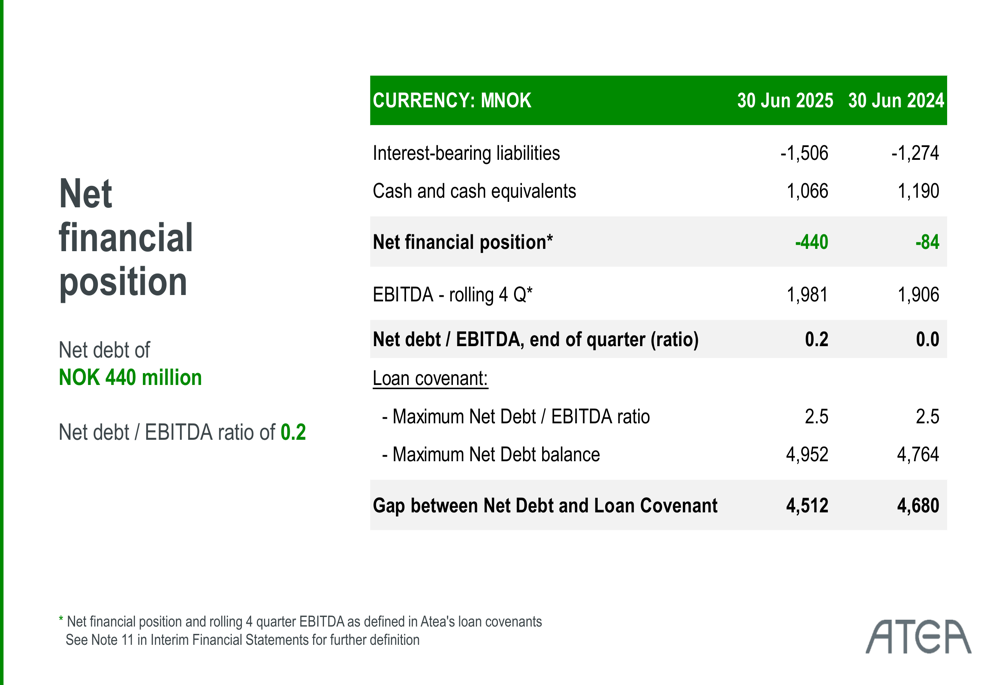

Despite the temporary negative cash flow, Atea maintains a strong financial position with a net debt of NOK 440 million and a low net debt to EBITDA ratio of 0.2, well below its loan covenant maximum of 2.5. This provides the company with significant financial flexibility for future investments and potential acquisitions.

The detailed breakdown of Atea’s financial position shows its solid standing:

Strategic Growth Initiatives

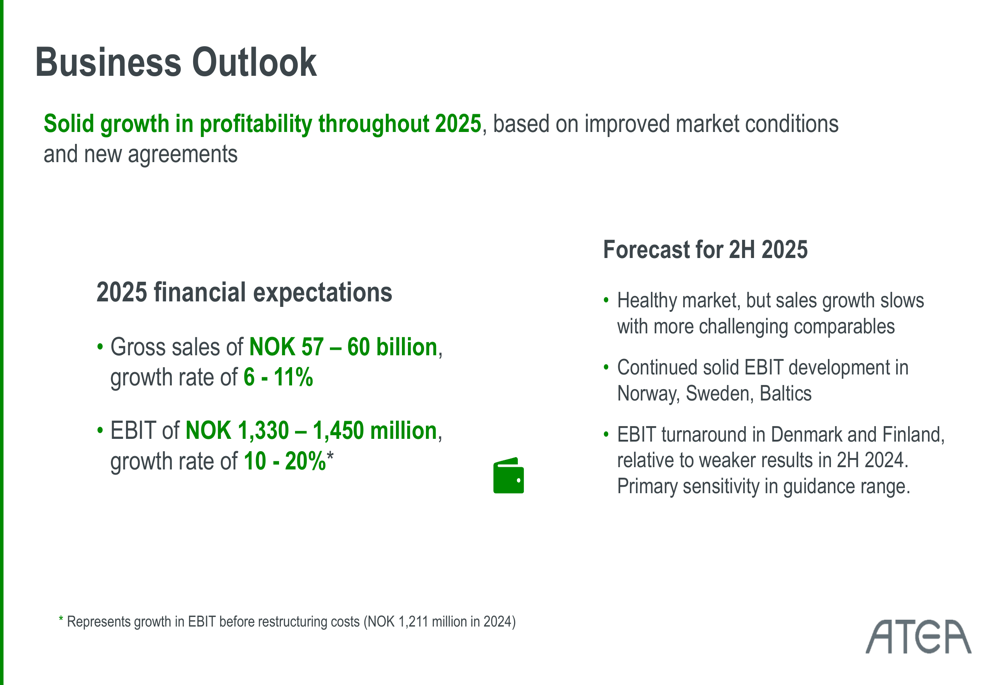

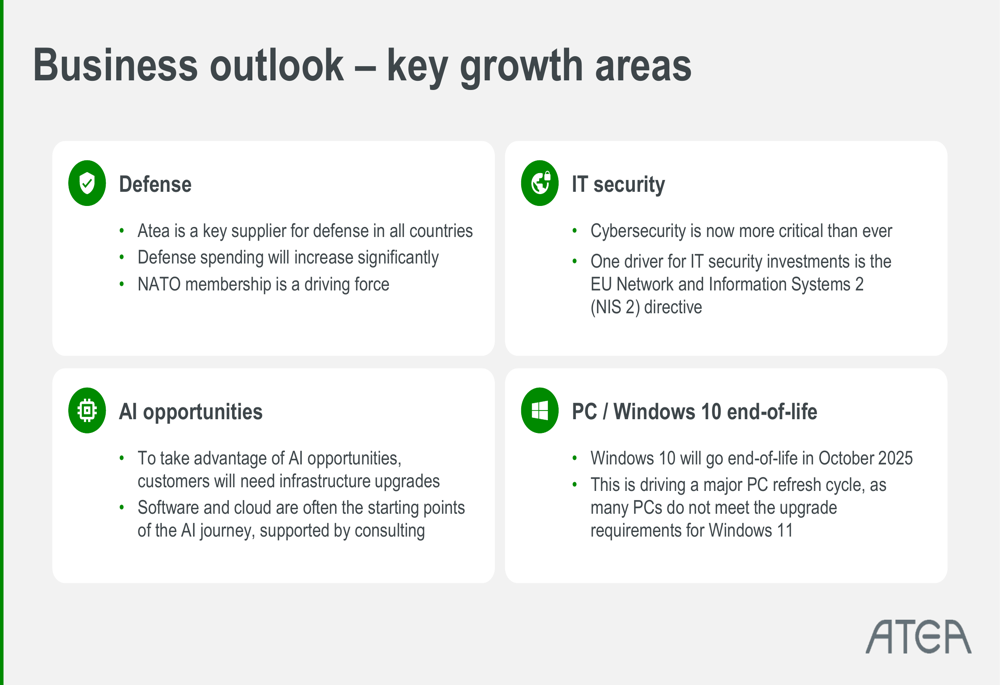

Atea identified four key growth areas that will drive its future performance: defense, IT security, AI opportunities, and the upcoming Windows 10 end-of-life cycle.

The company’s outlook for 2025 remains positive, with expected gross sales of NOK 57-60 billion (representing 6-11% growth) and EBIT of NOK 1,330-1,450 million (10-20% growth). For the second half of 2025, Atea anticipates continued solid EBIT development in Norway, Sweden, and the Baltics, with a turnaround expected in Denmark and Finland.

As shown in the business outlook slide:

Defense has emerged as a particularly strong sector for Atea, growing by 28% in Q2 according to the earnings call. The company is benefiting from increased defense spending across Nordic countries, partly driven by NATO membership. Cybersecurity investments are also accelerating, fueled by the EU Network and Information Systems 2 (NIS 2) directive.

In the AI space, Atea is collaborating with major technology partners like Microsoft and IBM, having sold 38,000 Microsoft Copilot licenses in Q2 alone. The company also expects significant hardware refresh opportunities as Windows 10 approaches its end-of-life in October 2025, as many existing PCs do not meet the requirements for Windows 11.

The following slide details these strategic growth areas:

First Half Performance & Outlook

Looking at the first half of 2025, Atea demonstrated strong overall performance with gross sales of NOK 30.0 billion, up 15.3% from the previous year. Revenue (IFRS) increased by 10.7% to NOK 17.7 billion, while EBIT grew by 10.1% to NOK 549 million.

The H1 2025 summary highlights these achievements:

For the remainder of 2025, Atea expects a healthy market environment, though sales growth may slow due to more challenging comparable periods. The company anticipates continued solid EBIT development in Norway, Sweden, and the Baltics, with improvement expected in the underperforming regions of Denmark and Finland.

While supply chain disruptions and economic fluctuations in Nordic countries remain potential risks, Atea’s diversified business model and strong market position in key growth sectors provide a solid foundation for continued expansion. The company’s low debt levels and healthy financial position further enhance its resilience against potential market challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.