Eos Energy stock falls after Fuzzy Panda issues short report

Introduction & Market Context

ATI Inc. (NYSE:ATI) presented its third quarter 2025 earnings results on October 28, 2025, showcasing strong financial performance driven primarily by its expanding Aerospace & Defense (A&D) business. The company’s stock responded positively, surging 10.35% to $101.20 following the announcement, approaching its 52-week high of $103.64.

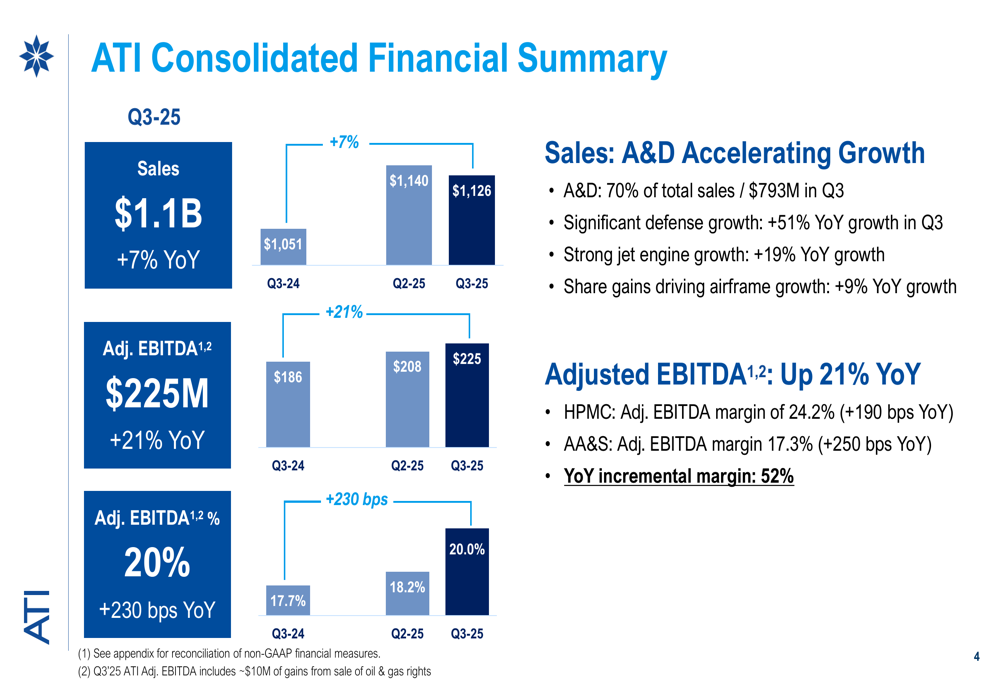

The specialty materials manufacturer reported adjusted earnings per share of $0.85, exceeding analyst expectations and representing a 42% year-over-year increase. Total sales reached $1.1 billion, up 7% compared to the same period last year, with A&D now accounting for a record 70% of the company’s business.

Quarterly Performance Highlights

ATI’s third quarter results demonstrated significant improvement across key financial metrics. The company achieved $225 million in adjusted EBITDA, a 21% year-over-year increase, while expanding its adjusted EBITDA margin to 20%, representing a 230 basis point improvement from Q3 2024.

As shown in the following consolidated financial summary:

The company’s performance was driven by accelerating A&D growth, particularly in defense (+51% YoY), jet engines (+19% YoY), and airframes (+9% YoY). This favorable mix shift, combined with operational improvements, resulted in a year-over-year incremental margin of 52%.

ATI’s business is organized into two primary segments: High Performance Materials & Components (HPMC) and Advanced Alloys & Solutions (AA&S). Both segments delivered strong results as illustrated in their respective financial summaries:

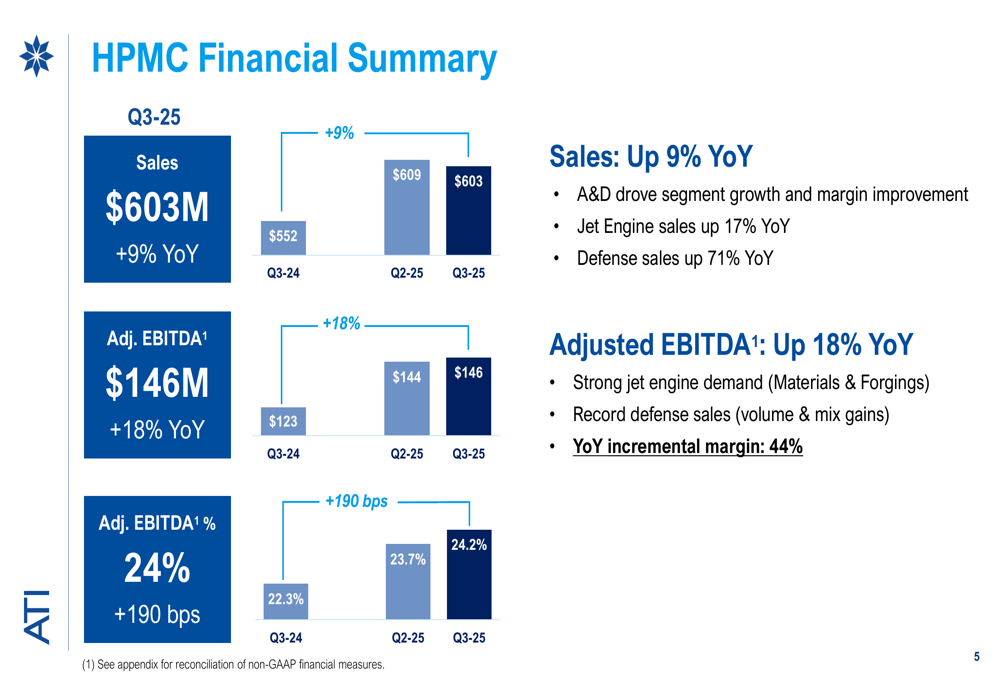

The HPMC segment, which primarily serves the jet engine and defense markets, posted sales of $603 million (+9% YoY) and adjusted EBITDA of $146 million (+18% YoY). The segment’s adjusted EBITDA margin expanded to 24.2%, a 190 basis point improvement year-over-year.

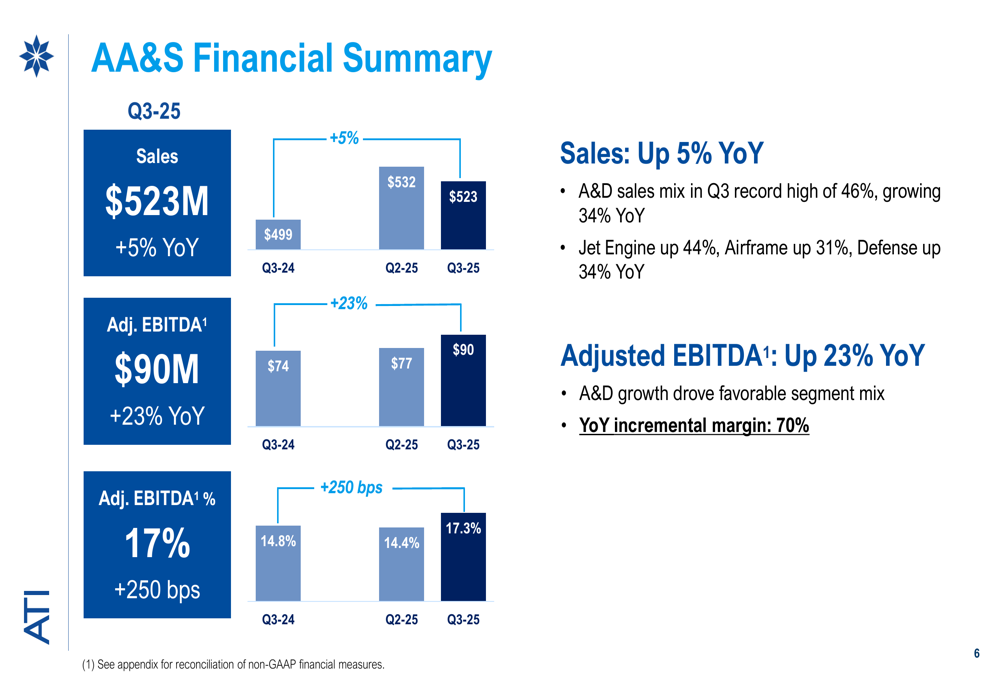

Similarly, the AA&S segment reported sales of $523 million (+5% YoY) and adjusted EBITDA of $90 million (+23% YoY). The segment achieved a record high A&D sales mix of 46%, growing 34% year-over-year, which helped drive margin expansion to 17.3%, a 250 basis point improvement.

Aerospace & Defense Growth

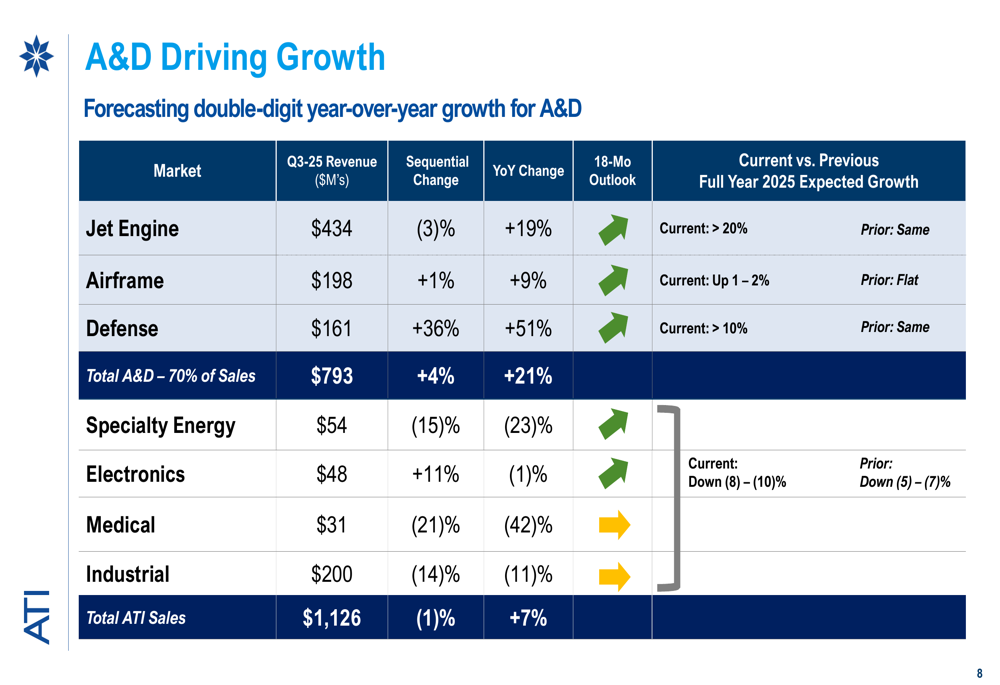

ATI’s strategic focus on high-value A&D markets continues to yield results, with these segments now representing 70% of total sales. The company highlighted its strong positioning across three key A&D markets:

In the jet engine market, which represents 39% of ATI’s revenue, the company is benefiting from next-generation engine requirements and maintenance, repair, and overhaul (MRO) activities, which account for approximately 50% of total engine sales. ATI maintains a competitive advantage as the sole source producer for five of seven advanced nickel powder and nickel cast and wrought jet engine alloys.

The airframe segment is supported by production rate increases at both Boeing and Airbus, with Boeing raising its rate to 42 and Airbus bringing on new A320 production lines. ATI’s airframe revenue has increased approximately 70% in Q3 2025 TTM compared to 2022, and new long-term agreements extend and expand the company’s presence through 2030.

The defense segment has shown particularly strong growth, with Q3 revenue up 51% year-over-year, marking three consecutive years of double-digit growth. This growth spans multiple applications including naval nuclear, rotary craft, missiles, and armored vehicles.

A detailed breakdown of A&D segment performance shows:

Financial Position and Capital Allocation

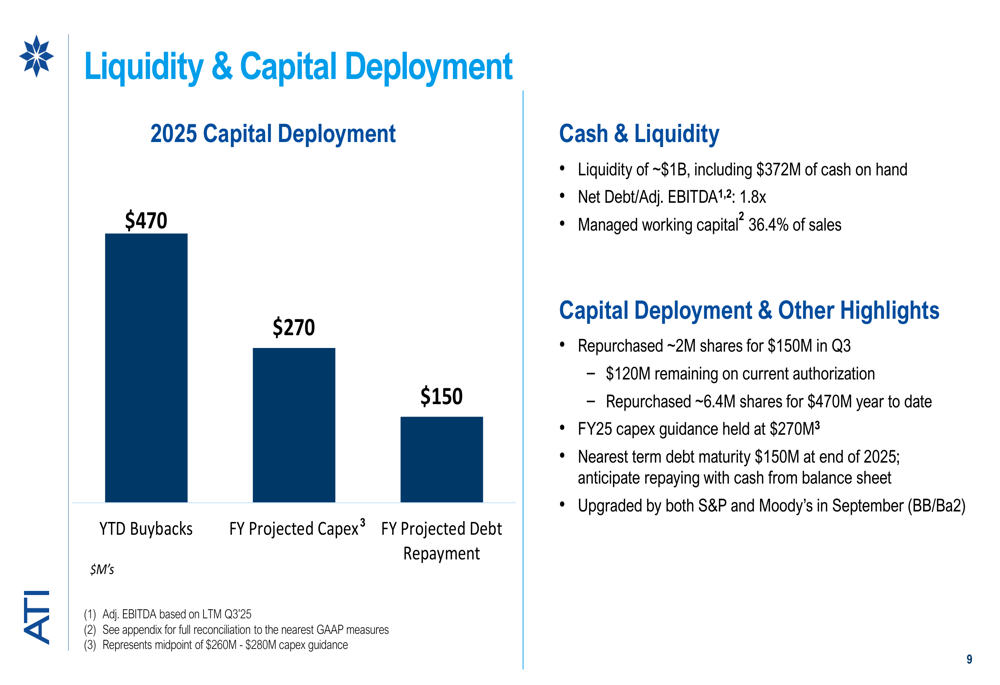

ATI maintained a strong financial position with approximately $1 billion in liquidity, including $372 million in cash on hand. The company’s net debt to adjusted EBITDA ratio stood at 1.8x, reflecting a conservative balance sheet.

The following chart illustrates ATI’s capital deployment strategy:

The company has been actively returning capital to shareholders, with $150 million in share repurchases during Q3 and $470 million year-to-date. Approximately 2 million shares were repurchased during the quarter, with $120 million remaining in the current authorization.

Capital expenditures for fiscal year 2025 are projected at $270 million, while debt repayment is expected to reach $150 million. ATI’s financial strength was further validated by recent credit rating upgrades from both S&P and Moody’s in September 2025.

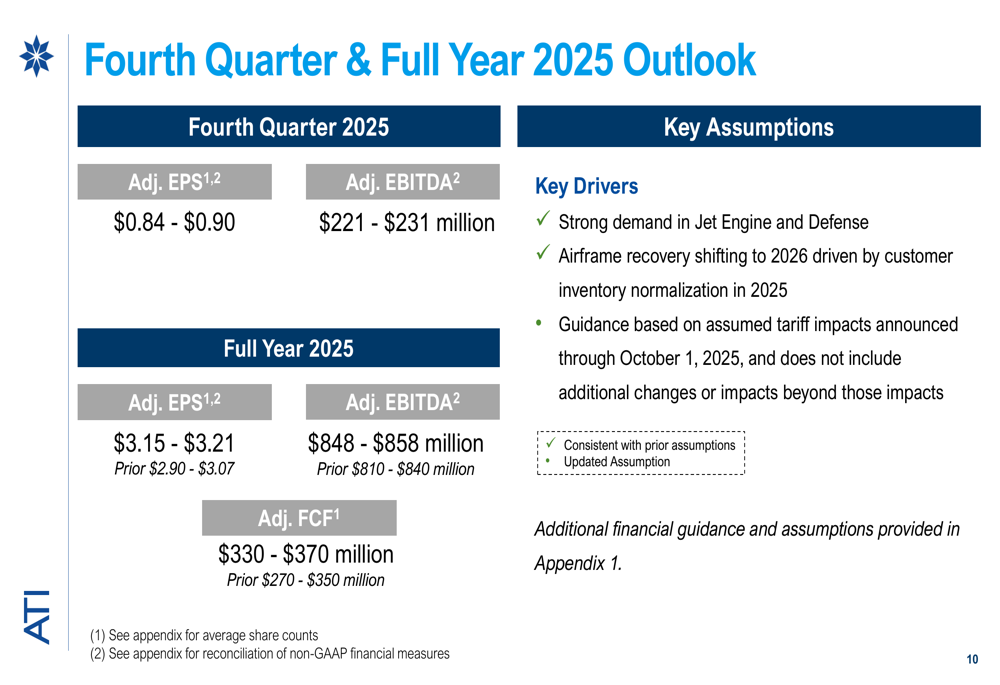

Outlook and Guidance

Based on the strong performance through the first three quarters, ATI raised its full-year 2025 guidance:

For the fourth quarter of 2025, ATI expects adjusted EPS of $0.84-$0.90 and adjusted EBITDA of $221-$231 million. The full-year outlook now projects adjusted EPS of $3.15-$3.21 (previously $2.90-$3.07), adjusted EBITDA of $848-$858 million (previously $810-$840 million), and adjusted free cash flow of $330-$370 million (previously $270-$350 million).

During the earnings call, CEO Kim Fields emphasized the company’s transformation: "Our transformation is working. We’re seeing that in both our margins, our mix and our overall growth. We are more agile, more profitable, and better positioned to deliver long-term value."

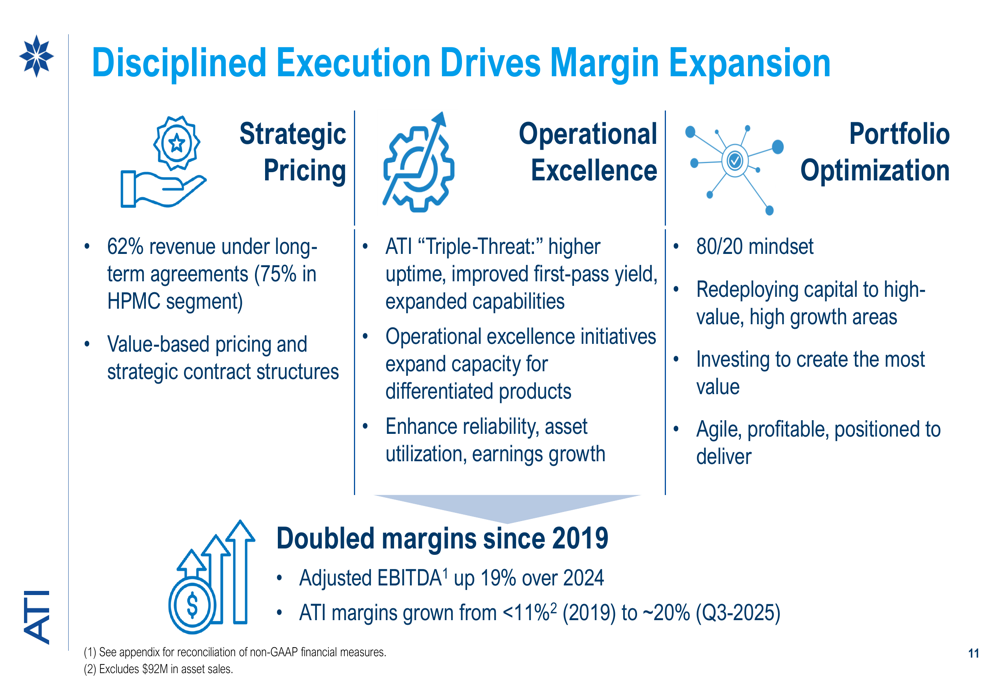

Strategic Initiatives

ATI’s margin expansion from less than 11% in 2019 to approximately 20% in Q3 2025 has been driven by three key strategic initiatives:

Strategic pricing has been a cornerstone of ATI’s approach, with 62% of revenue under long-term agreements (75% in the HPMC segment). These agreements incorporate value-based pricing to capture the premium value of ATI’s specialty materials and components.

The company’s operational excellence program, known as the ATI "Triple-Threat," focuses on enhancing reliability and asset utilization to drive earnings growth. Additionally, portfolio optimization employs an 80/20 mindset to redeploy capital toward the highest-value opportunities.

These disciplined execution strategies have contributed to a 19% increase in adjusted EBITDA over 2024, positioning ATI for continued profitable growth in its core A&D markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.