Five things to watch in markets in the week ahead

Introduction & Market Context

Atlantic Sapphire (OB:ASA) presented its 2024 annual report and company update on April 23, 2025, highlighting significant operational improvements amid persistent financial challenges. The land-based salmon producer’s stock has fallen 8.31% to 6.29 NOK following the presentation, reflecting investor concerns despite operational progress.

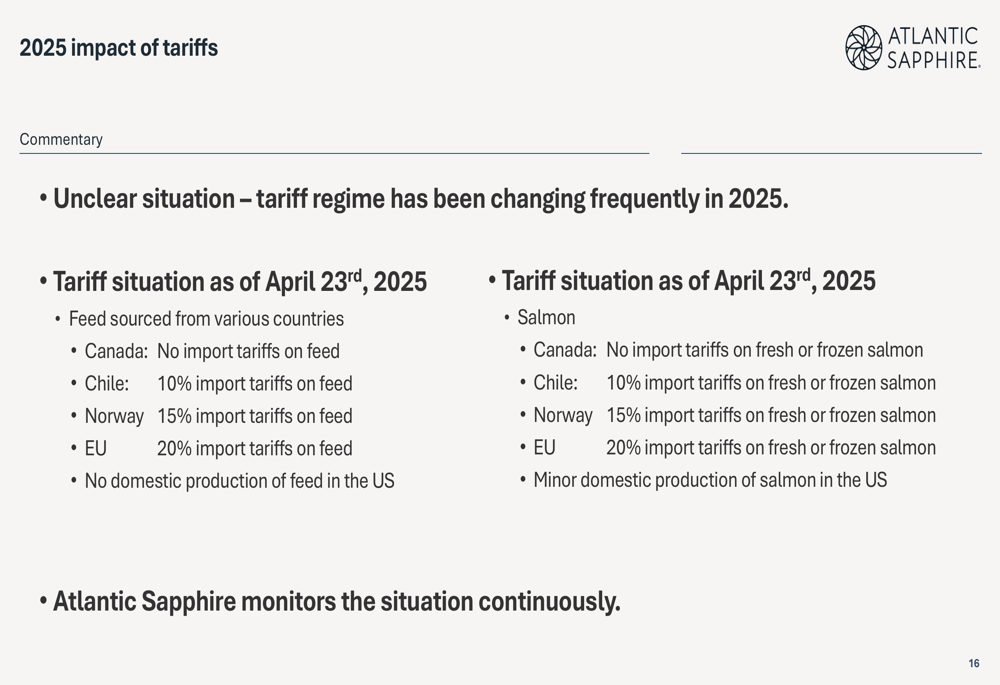

The company operates in a unique position within the U.S. salmon market, benefiting from its domestic production capabilities while imported salmon faces varying tariffs between 10-20% from major producing countries like Norway, Chile, and the EU. Only Canadian imports remain tariff-free, giving Atlantic Sapphire a competitive advantage in the premium segment.

Operational Performance Highlights

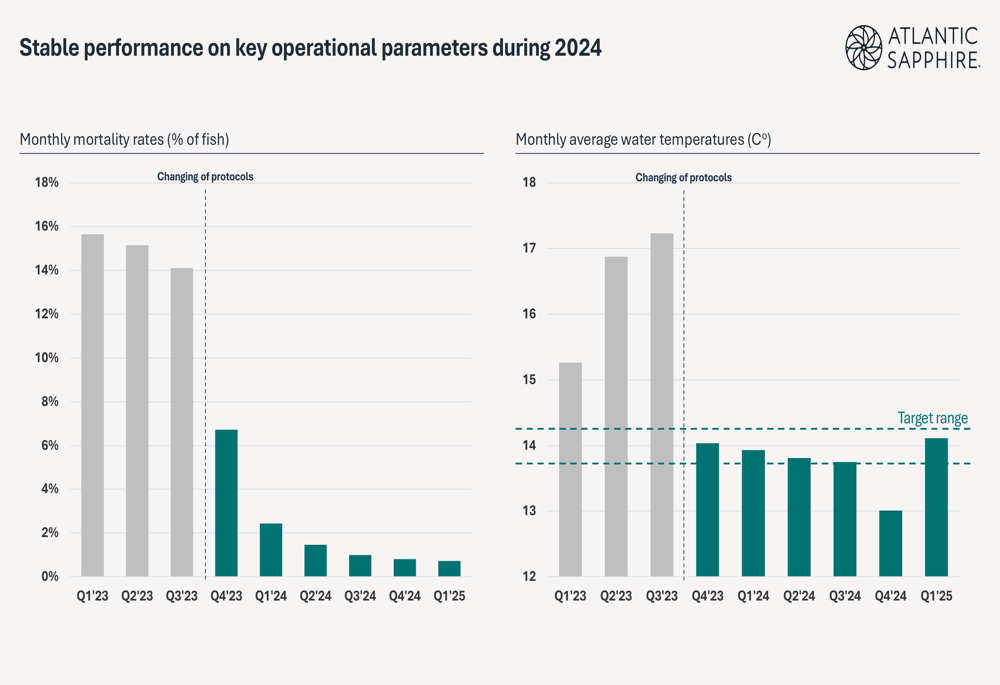

Atlantic Sapphire reported substantial operational improvements throughout 2024, with mortality rates dropping dramatically from 16% in Q1 2023 to just 1.3% by Q4 2024. Water temperatures have stabilized between 13.8°C and 14°C since Q4 2023, remaining within the target range for optimal salmon growth.

As shown in the following chart of mortality rates and water temperature stability:

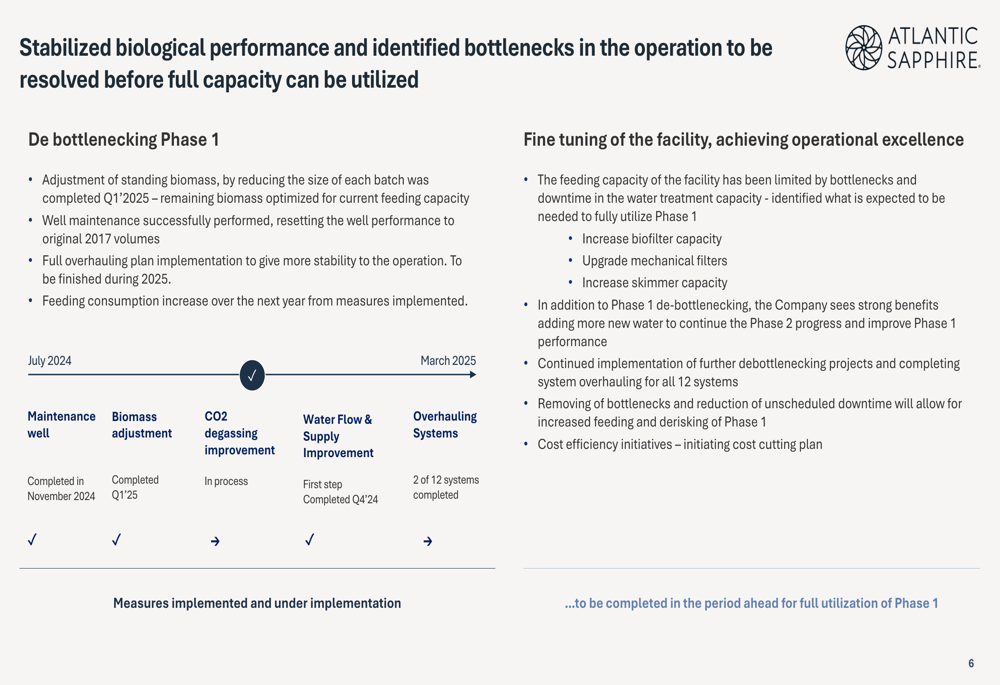

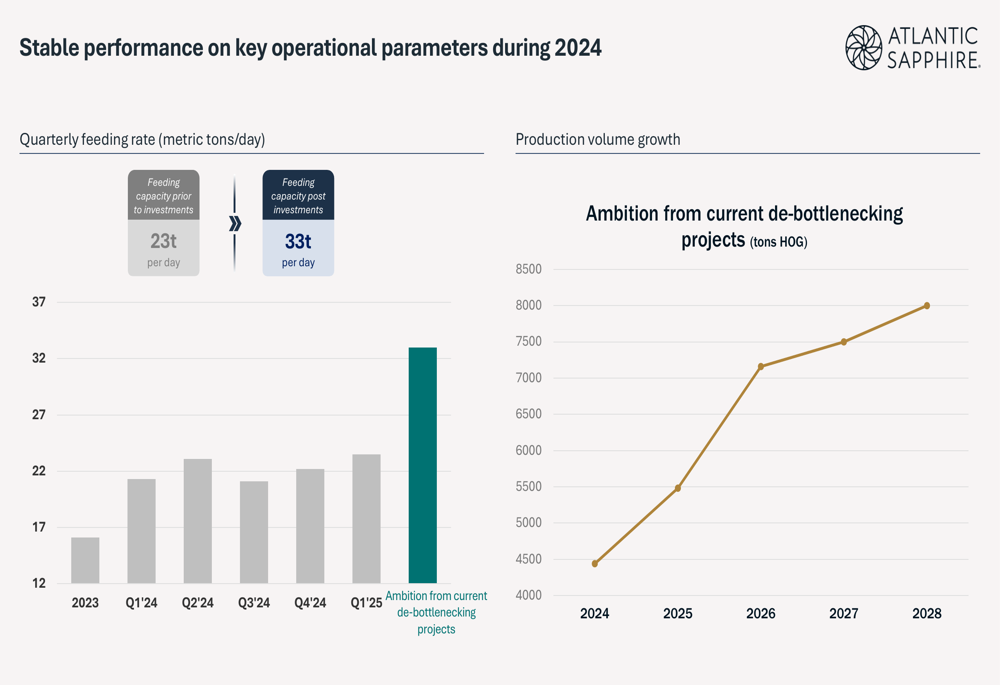

The company has successfully implemented several operational improvements, including well maintenance, biomass adjustments, and CO2 degassing improvements. These measures have enabled Atlantic Sapphire to increase its daily feeding rate from 23 tons to 33 tons post-investments, a crucial metric for production growth.

The following slide illustrates the company’s debottlenecking initiatives and operational improvements:

These operational enhancements have translated into tangible production growth. Harvest volumes reached 4,365 tons HOG (head-on gutted) in 2024, nearly tripling the 1,545 tons produced in 2023. Similarly, biomass gain increased to 5,500 tons RLW (round live weight) from 3,700 tons in the previous year.

The company’s feeding rate improvements and production volume targets are shown below:

Financial Results Analysis

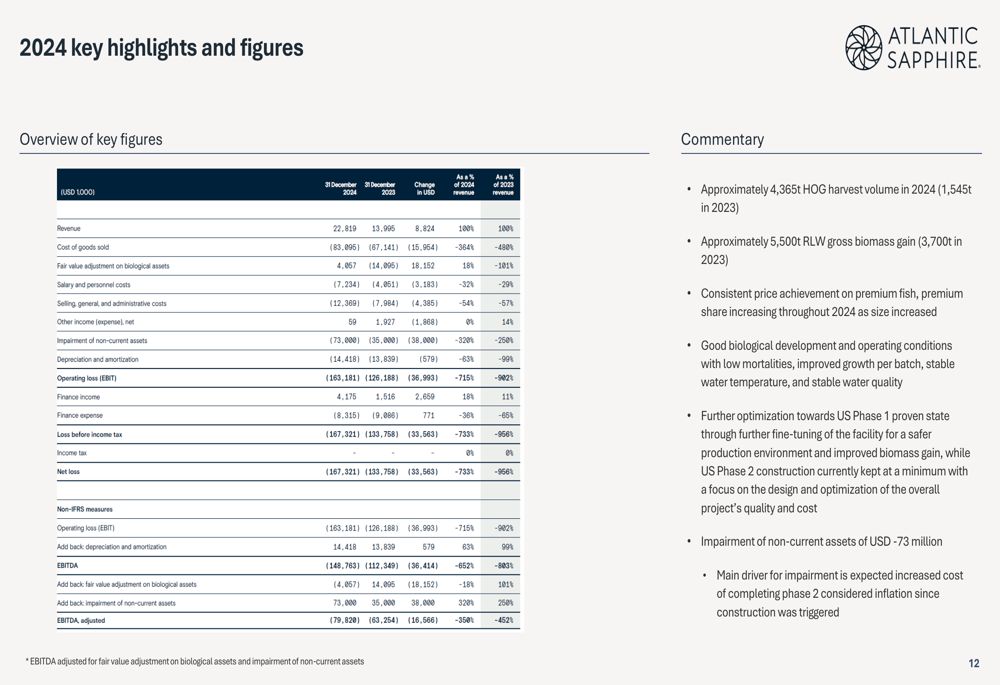

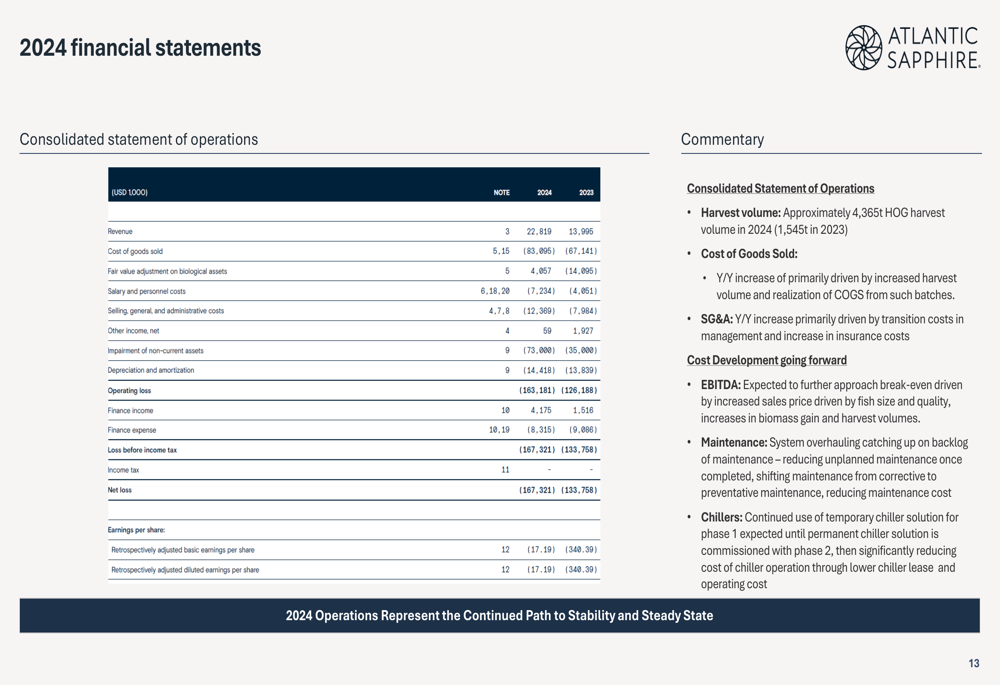

Despite operational improvements, Atlantic Sapphire’s financial results reveal persistent challenges. Revenue increased to $22.819 million in 2024 from $13.995 million in 2023, driven by higher harvest volumes. However, operating losses widened to $163.181 million from $126.188 million, while net losses grew to $167.321 million from $133.758 million in the previous year.

The comprehensive financial overview is presented in this key financial highlights slide:

The company’s financial position shows $29.4 million in operating cash and $15.2 million in restricted deposits. According to the earnings call transcript, Atlantic Sapphire also recorded a $73 million impairment write-down of fixed assets, reflecting adjustments to the carrying value of its production facilities.

The detailed financial statements provide further insight into the company’s performance:

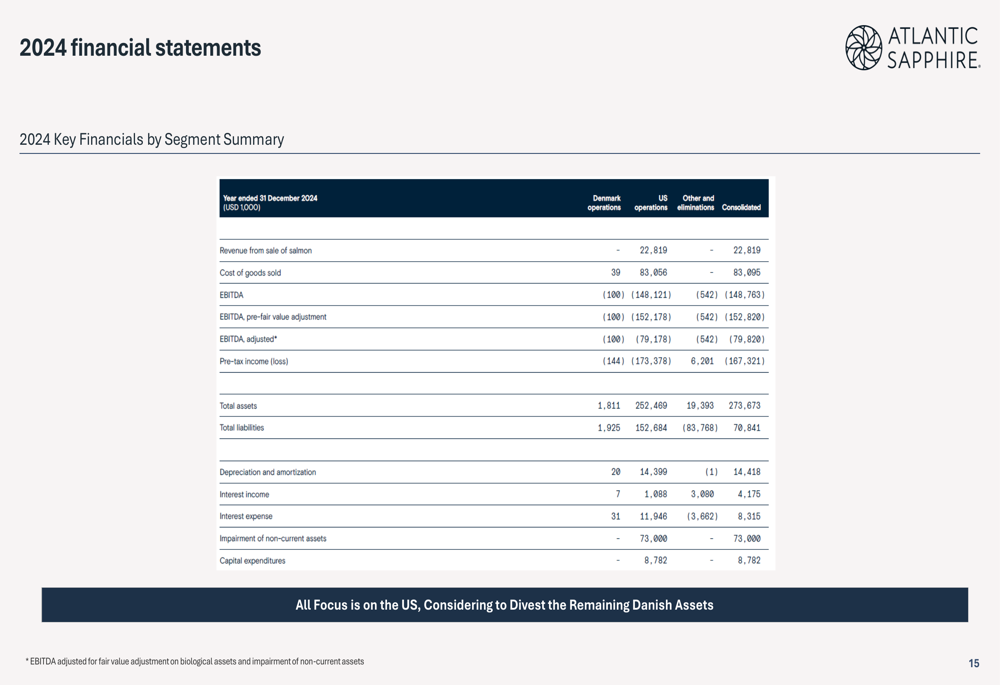

Segment analysis reveals that all revenue ($22.819 million) was generated by U.S. operations, with no revenue contribution from Denmark. This aligns with the company’s strategic shift to focus entirely on its U.S. business, with management considering divesting the remaining Danish assets.

The segment breakdown is illustrated in the following financial summary:

Strategic Roadmap and Outlook

Atlantic Sapphire has outlined a clear strategic roadmap divided into four stages. Having moved beyond the initial "commissioning" phase (2017-Sep 2023) and "industrialization" phase (Oct 2023-Jun 2024), the company is currently in the "de-bottlenecking and optimization" phase, aiming to grow production while improving efficiency.

The strategic roadmap with specific targets is shown below:

In the medium term, Atlantic Sapphire targets an EBITDA of $1.5-2.0 per kilogram and annual harvest volumes of 8,250-8,750 tons. The long-term vision (Stage 4) aims for "operational excellence" with EBITDA of approximately $5 per kilogram and annual harvest of 25,000 tons.

According to CEO Pedro Kurar, quoted in the earnings call: "Today, we are in the stage of optimizing phase one by maximizing harvest biomass at high average weight." CFO Gunnar Sinderenberg added, "We are expecting projects to be executed and also harvest volume to increase."

Competitive Positioning and Market Factors

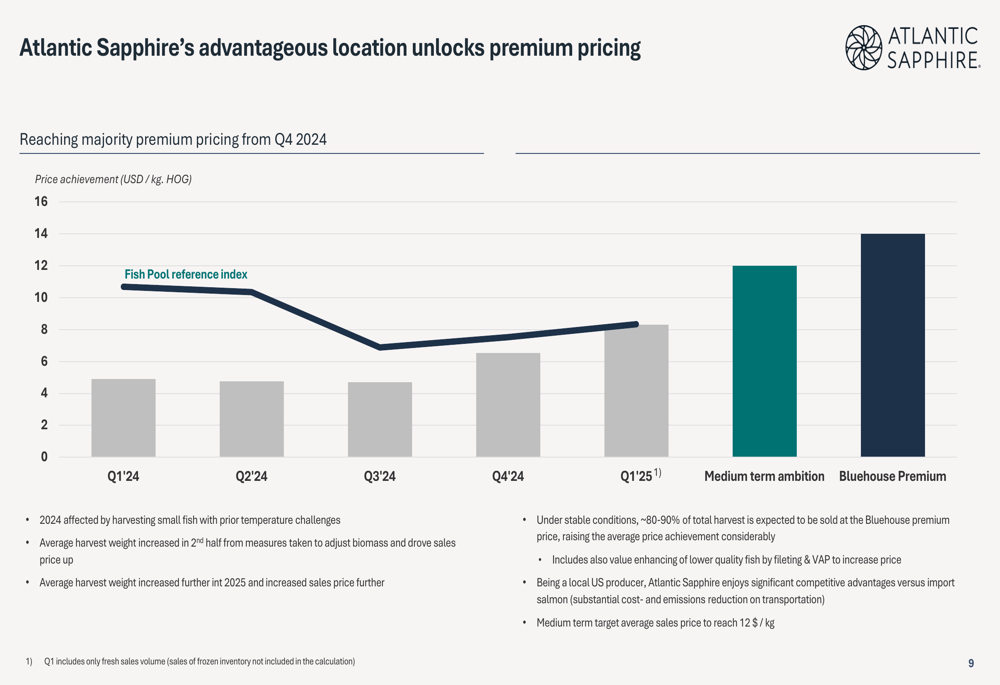

Atlantic Sapphire’s U.S. location provides significant pricing advantages, allowing the company to command premium prices compared to imported salmon. The company has seen improving price achievement throughout 2024 and into early 2025, particularly as average harvest weights have increased.

The price premium dynamics are illustrated in this chart:

The company expects that under stable conditions, approximately 80-90% of its total harvest will be sold at premium "Bluehouse" prices. This premium positioning is further strengthened by the current tariff environment, which imposes 10-20% tariffs on salmon imports from major producing countries.

The tariff situation affecting both salmon and feed imports is detailed below:

While Atlantic Sapphire has made significant operational strides and outlined an ambitious path to profitability, investors appear concerned about the widening losses and the timeline to positive cash flow. The company’s focus on operational excellence and strategic positioning in the premium U.S. market represents its best path forward amid these financial challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.