Nvidia pushes back on AI bubble narrative as Blackwell drives Q3 beat, shares jump

Introduction & Market Context

ATN International (NASDAQ:ATNI) presented its second quarter 2025 earnings results on August 8, 2025, maintaining its full-year outlook despite mixed performance across its business segments. The telecommunications infrastructure provider, which focuses on rural and remote markets, reported results that management described as "in line with expectations" following a disappointing first quarter that saw the stock drop over 13%.

ATNI shares have partially recovered since the Q1 report, with the stock trading at $16.61 at market close on August 8, 2025, down just 0.12% for the day. The company’s stock remains well below its 52-week high of $33.72, reflecting ongoing investor concerns about the company’s performance and strategic direction.

Quarterly Performance Highlights

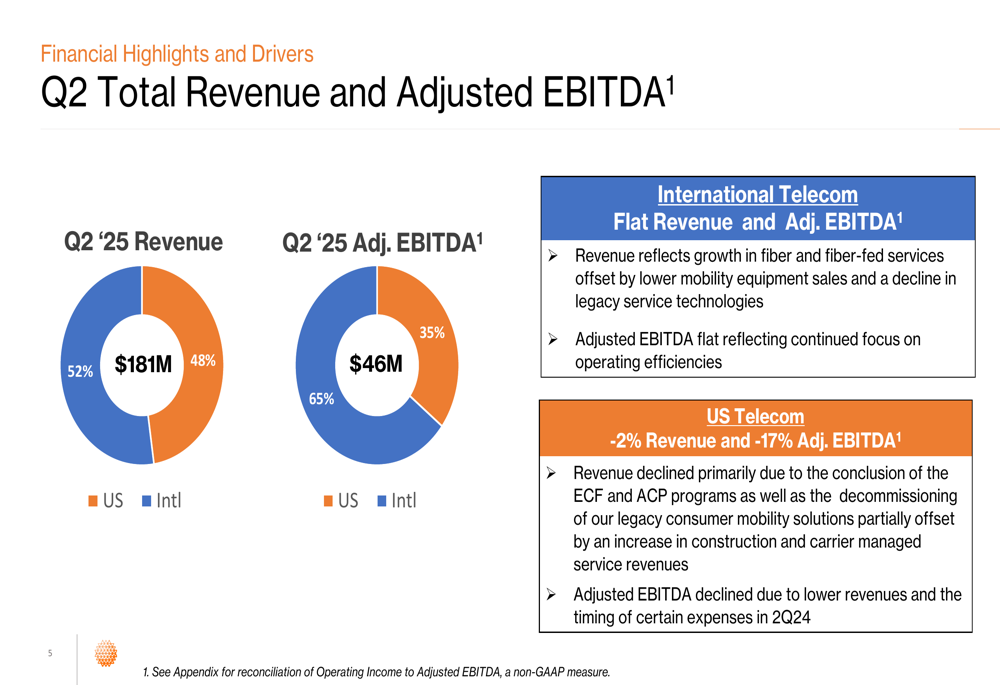

ATN International reported Q2 2025 revenue of $181 million, down slightly from $183.3 million in the same quarter last year. Adjusted EBITDA came in at $45.8 million, compared to $48.7 million in Q2 2024, representing a 5.9% year-over-year decline.

As shown in the following revenue and Adjusted EBITDA breakdown:

The company’s revenue mix was split between US operations (52%) and International operations (48%), while Adjusted EBITDA showed a stronger contribution from International operations (65%) compared to US operations (35%).

Operating income for the quarter fell dramatically to just $233,000 from $24.3 million in Q2 2024, highlighting significant pressure on the company’s profitability despite relatively stable revenue.

Segment Analysis

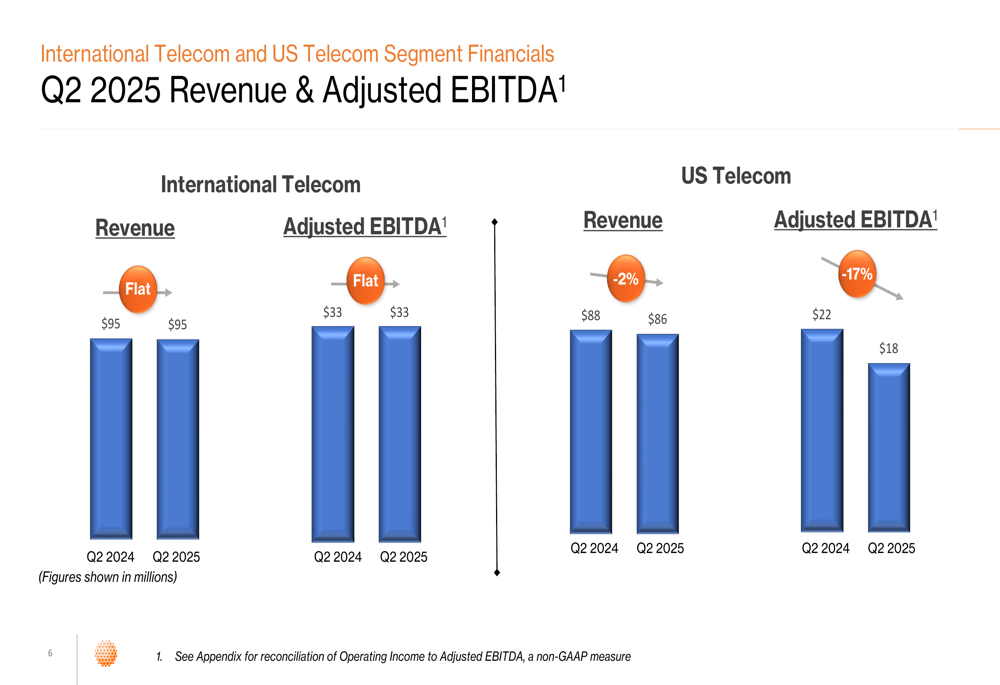

ATN’s performance revealed a stark contrast between its two main business segments. The International Telecom (BCBA:TECO2m) segment, which operates in markets including Bermuda, the Cayman Islands, Guyana, and the US Virgin Islands, demonstrated stability with flat revenue and Adjusted EBITDA year-over-year at $95 million and $33 million respectively.

In contrast, the US Telecom segment, which serves Alaska and the Southwestern United States, showed weakness with revenue declining 2% to $86 million and Adjusted EBITDA dropping 17% to $18 million. Management attributed this decline to "the conclusion of ECF and ACP programs, partially offset by increases in construction and carrier managed services revenues."

The segment performance comparison is illustrated in the following chart:

Key operational metrics showed mixed results. The company’s fiber network expanded modestly to approximately 12,000 route miles, a 1% increase year-over-year. High-speed data homes passed grew 8% to approximately 428,000, while high-speed data customers increased by just 1% to 142,000. Mobile subscribers declined 1% year-over-year to 393,000, with post-paid subscribers growing 4% but pre-paid subscribers declining 2%.

Strategic Initiatives & Capital Allocation

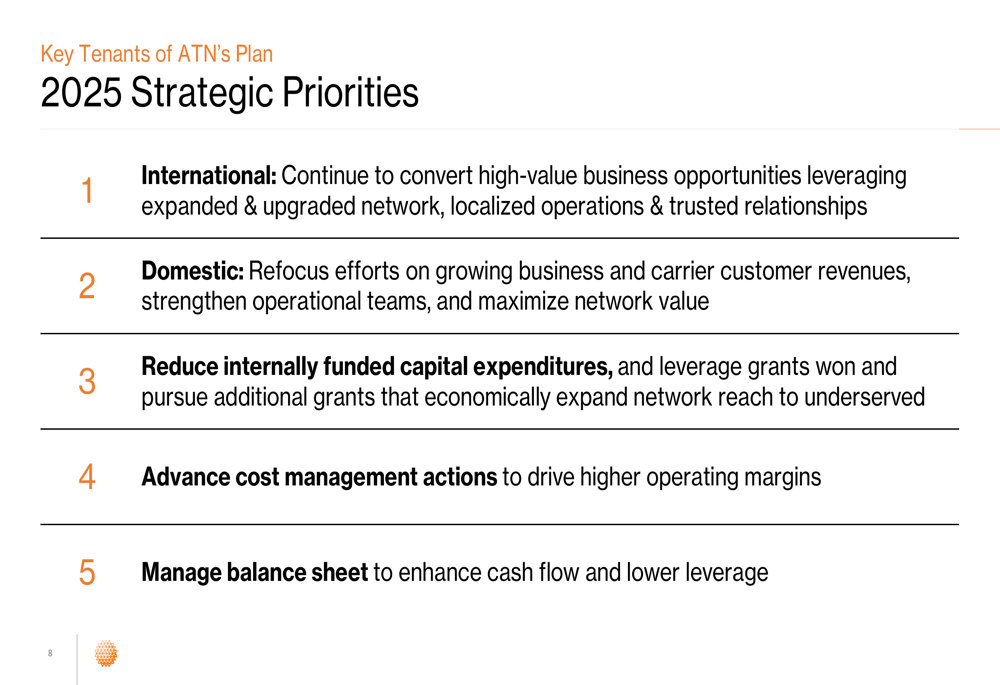

ATN outlined its strategic priorities for 2025, focusing on operational efficiency and targeted growth opportunities:

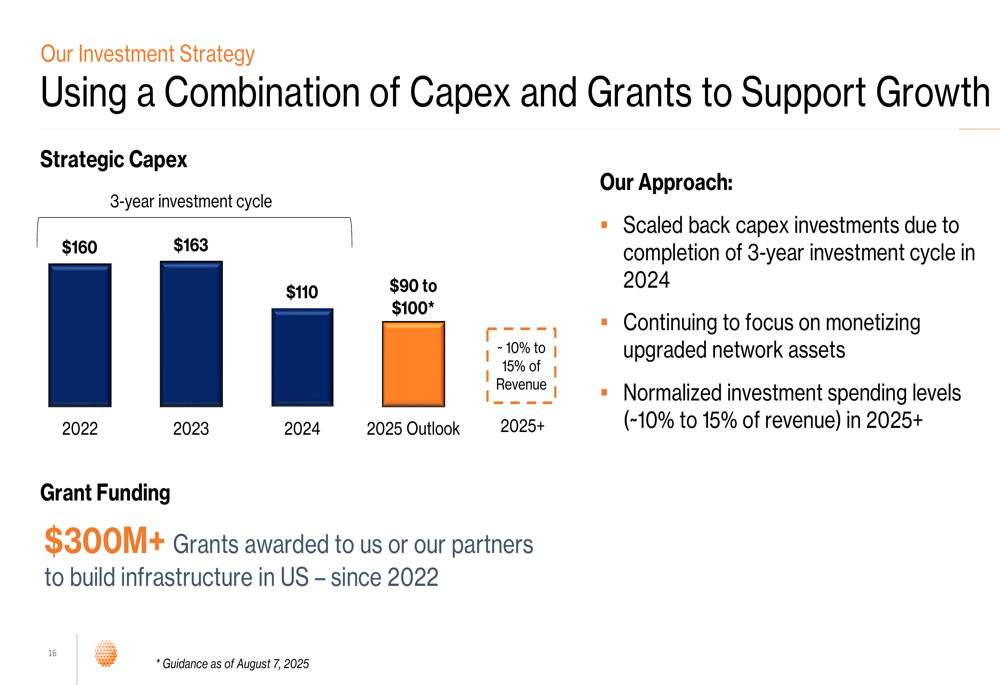

The company’s investment strategy has shifted toward reduced capital expenditure following the completion of a three-year investment cycle in 2024. Capital expenditures are expected to normalize to 10-15% of revenue going forward, down from higher levels in recent years:

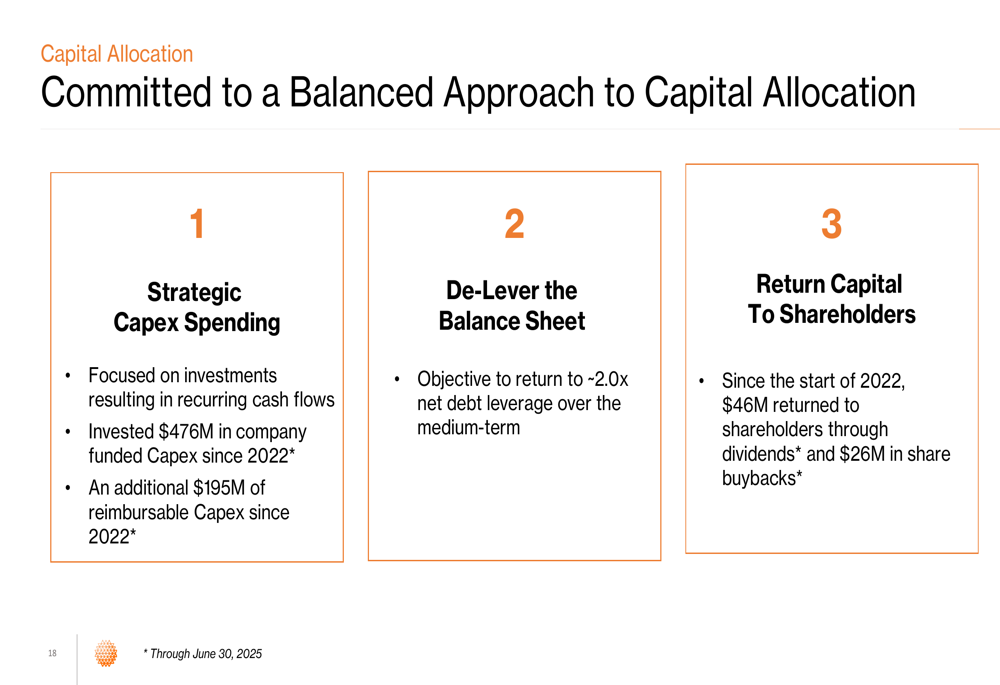

ATN’s capital allocation strategy balances three key priorities: strategic capital expenditure, deleveraging the balance sheet, and returning capital to shareholders. Since 2022, the company has invested $476 million in company-funded capital expenditure, returned $46 million to shareholders through dividends, and spent $26 million on share buybacks.

Balance Sheet & Financial Position

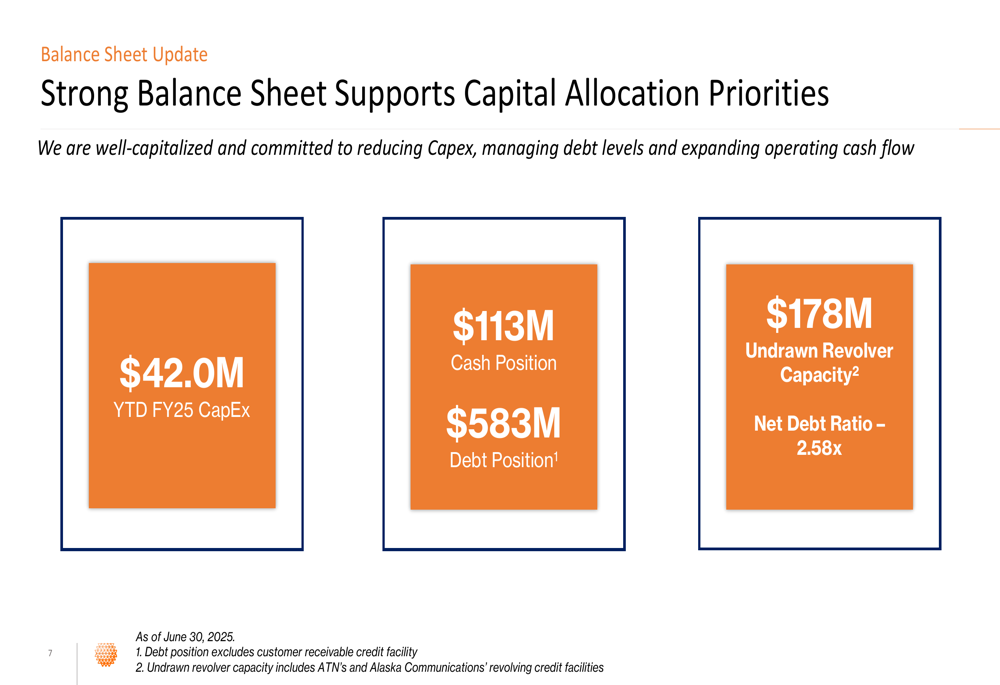

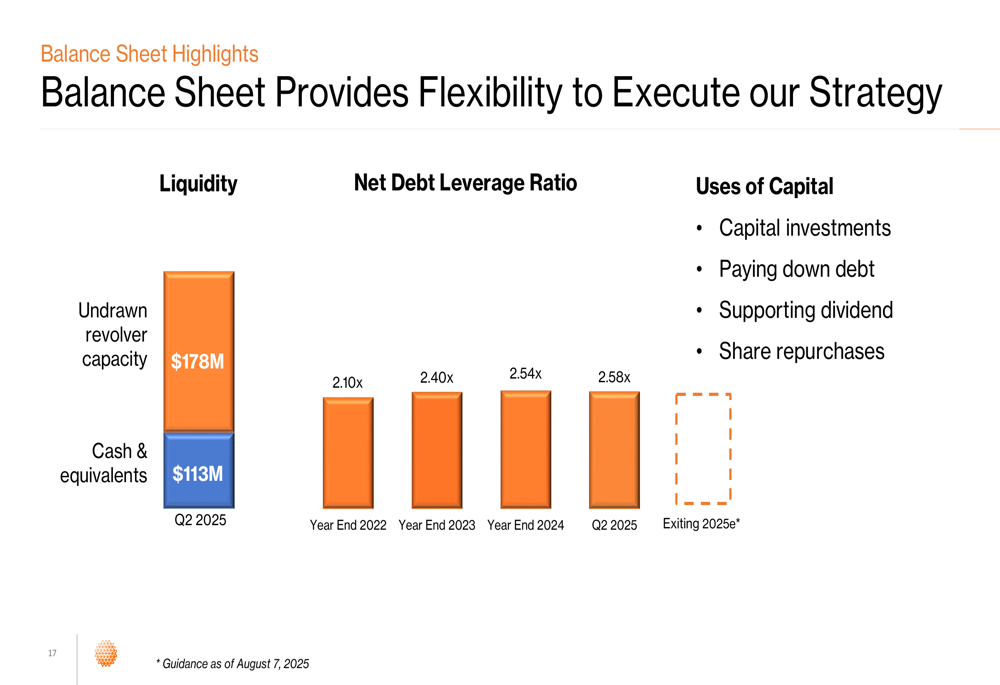

The company’s balance sheet update revealed a cash position of $113 million and debt of $583 million as of June 30, 2025. The net debt ratio stood at 2.58x, slightly higher than the 2.54x reported at the end of 2024:

ATN maintained $178 million in undrawn revolver capacity, providing additional financial flexibility. Management expressed a goal to return to a net debt leverage ratio of approximately 2.0x over the medium term, highlighting the company’s focus on strengthening its financial position:

Forward-Looking Statements

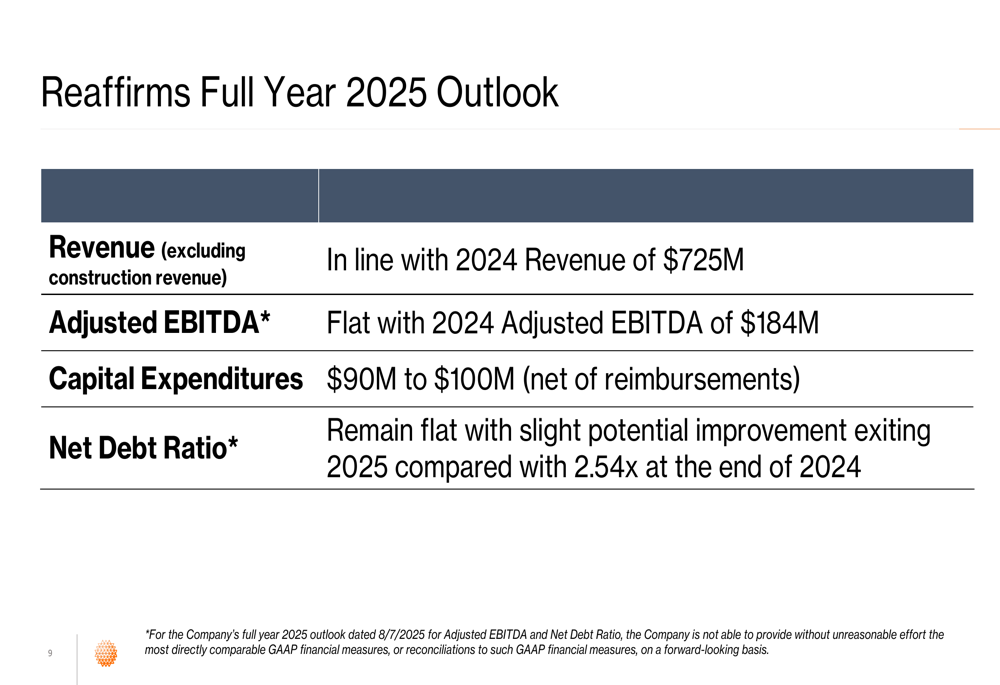

Despite the mixed quarterly performance and significant Q1 miss earlier this year, ATN reaffirmed its full-year 2025 outlook:

The company expects revenue (excluding construction revenue) to be in line with 2024 revenue of $725 million, with Adjusted EBITDA flat compared to 2024’s $184 million. Capital expenditures are projected to be $90-100 million (net of reimbursements), and the net debt ratio is expected to remain flat with slight potential improvement by the end of 2025.

CEO Brad Martin expressed confidence in the company’s direction, stating that the second quarter results "reflect efforts to optimize cost structure and execute on long-term strategy." Similarly, CFO Carlos Doglioli indicated that the company is "executing against clear priorities and confident in meeting the 2025 targets and delivering long-term value to shareholders."

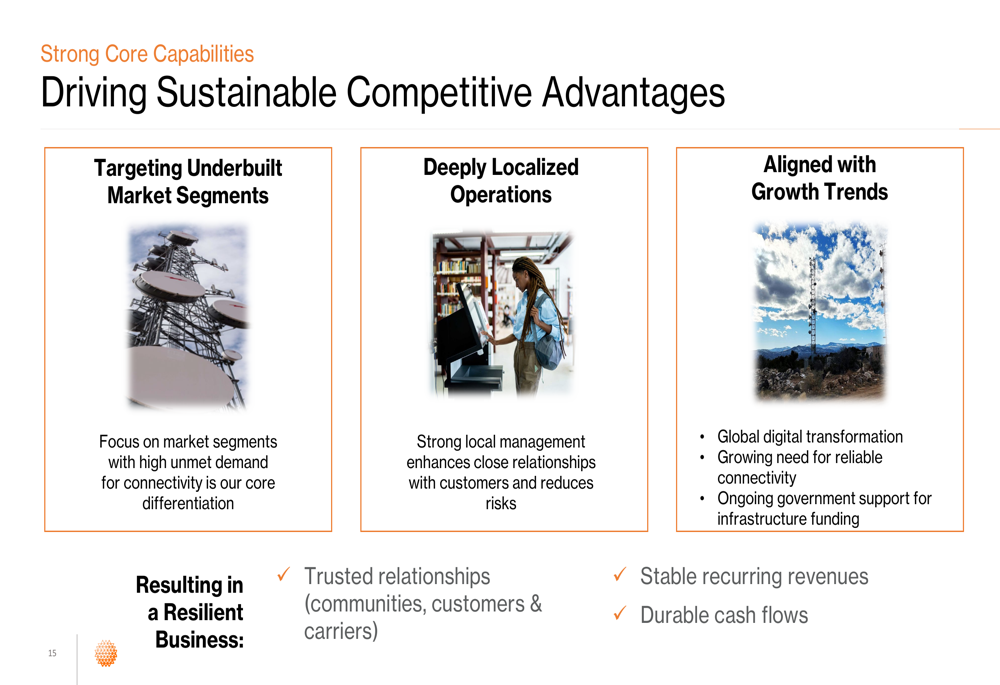

ATN’s core capabilities and market positioning continue to focus on underserved markets with high demand for connectivity, leveraging its localized operations and alignment with global digital transformation trends:

As ATN navigates through what management described in the Q1 earnings call as a "year of transition," investors will be watching closely to see if the company can deliver on its full-year outlook and demonstrate progress on its strategic priorities in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.