Nvidia pushes back on AI bubble narrative as Blackwell drives Q3 beat, shares jump

Introduction & Market Context

ATN International Inc. (NASDAQ:ATNI) presented its third quarter 2025 earnings results on November 6, 2025, showcasing improved operational performance driven by strong growth in its US Telecom segment and ongoing cost containment efforts. The telecommunications infrastructure provider, which focuses on rural and underserved markets, reported results that exceeded analyst expectations, triggering a significant market response with shares surging 18.9% during regular trading hours.

The company's presentation highlighted steady progress in executing its strategic transformation while strengthening operations and improving its cost structure. This performance comes amid ongoing challenges in the telecommunications sector, where providers are balancing network investments with financial discipline.

Quarterly Performance Highlights

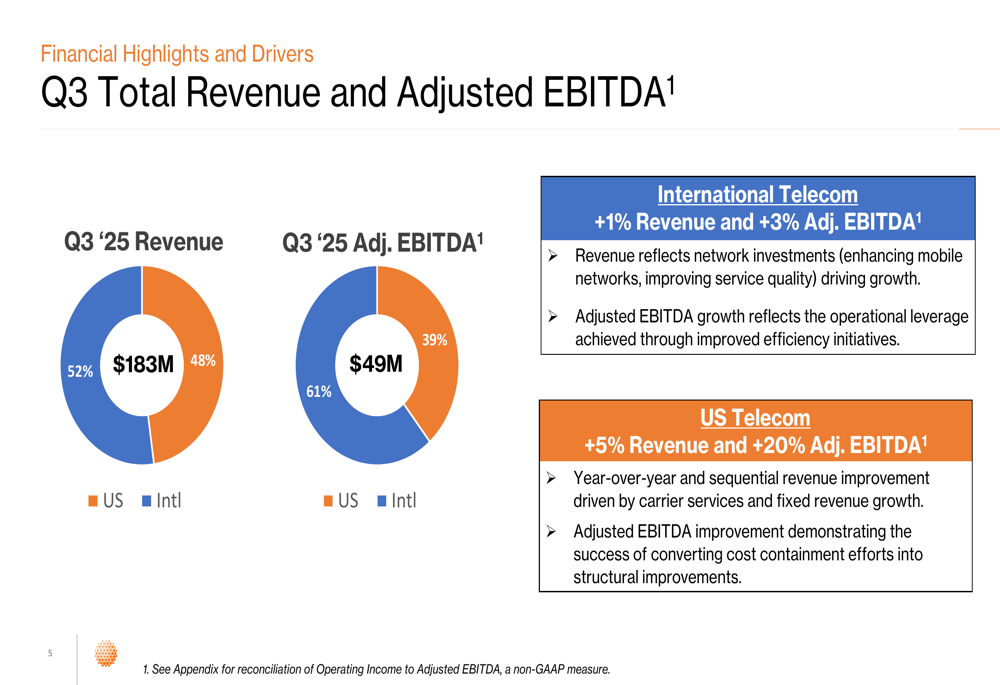

ATN reported Q3 2025 total revenue of $183 million, representing a 3% year-over-year increase. Adjusted EBITDA reached $49 million, showing solid improvement from the previous year. The results exceeded analyst expectations, with earnings per share of $0.18 surpassing the forecast of $0.12 by 50%.

As shown in the following revenue and EBITDA breakdown chart:

The company's revenue mix was relatively balanced between its two main segments, with US Telecom accounting for 52% ($95.16 million) and International Telecom representing 48% ($88.03 million). However, the Adjusted EBITDA distribution showed a stronger contribution from US operations at 61% ($21.16 million) compared to 39% ($18.09 million) from International operations.

CEO Brad Martin commented on the results: "Third quarter results are in line with expectations and demonstrated steady progress executing strategic transformation, strengthening operations, improving cost structure, and positioning the business for sustainable growth towards 2026."

Segment Performance Analysis

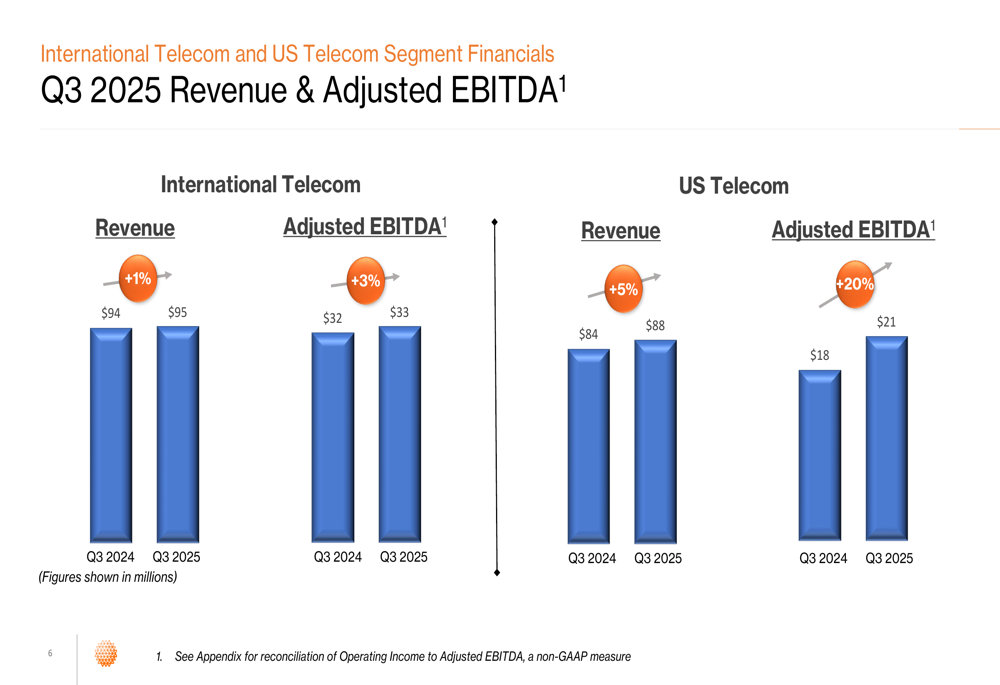

The US Telecom segment delivered particularly strong results, with revenue increasing by 5% year-over-year and Adjusted EBITDA jumping by 20% compared to Q3 2024. This significant improvement in profitability reflects the company's successful cost containment initiatives and operational efficiencies.

The detailed segment breakdown illustrates this performance:

Meanwhile, the International Telecom segment, which serves markets including Bermuda, the Cayman Islands, Guyana, and the US Virgin Islands, showed more modest growth with revenue up 1% and Adjusted EBITDA increasing by 3% year-over-year. This growth was primarily driven by network investments that have enhanced service capabilities.

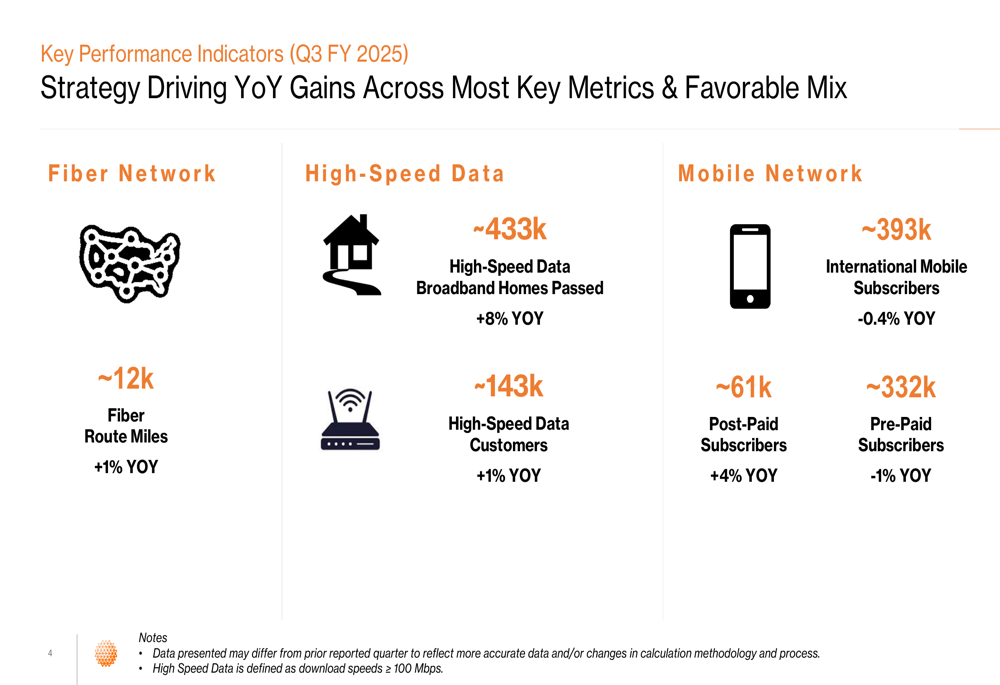

The company's operational metrics showed mixed results across different service categories:

High-speed data continued to be a growth area with broadband homes passed increasing 8% year-over-year to approximately 433,000, while high-speed data customers grew 1% to around 143,000. Mobile subscribers showed divergent trends with post-paid subscribers growing 4% year-over-year to approximately 61,000, while pre-paid subscribers declined 1% to about 332,000.

Balance Sheet and Capital Allocation

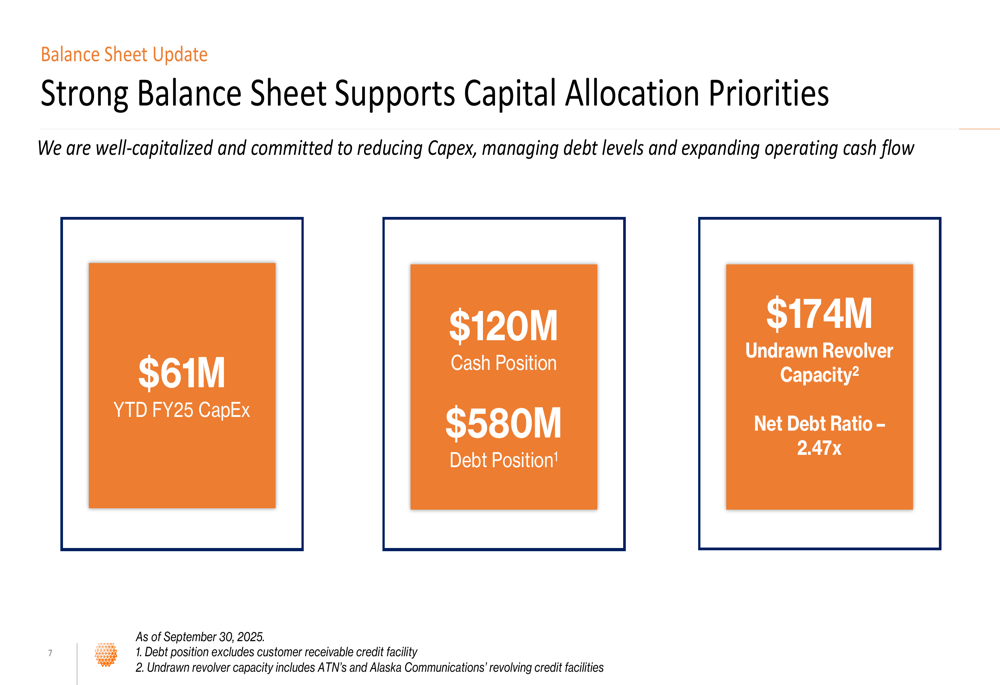

ATN's balance sheet showed improvement during the quarter, with the company making progress on its deleveraging goals. As of September 30, 2025, ATN reported:

The company's net debt ratio improved to 2.47x, down from 2.54x at the end of 2024, reflecting management's focus on strengthening the balance sheet. ATN maintained a solid cash position of $120 million and had $174 million in undrawn revolver capacity, providing financial flexibility for future initiatives.

CFO Carlos Doglioli emphasized the company's financial discipline: "Our refined guidance reflects cost containment efforts and enhanced capital efficiency. We remain confident in our execution capabilities and path toward long-term value creation."

ATN's capital expenditures strategy shows a clear trend toward more disciplined spending:

After completing a significant investment cycle in 2024, the company has scaled back capital expenditures to a projected $90-100 million for 2025, representing approximately 10-15% of revenue. This reduction reflects the completion of major network upgrades and a shift toward monetizing these investments while maintaining more normalized spending levels.

Strategic Initiatives and Outlook

Looking ahead, ATN provided guidance for the full year 2025:

The company expects revenue (excluding construction revenue) to be in line with 2024 revenue of $725 million, while Adjusted EBITDA is projected to be flat to slightly above 2024's $184 million. The net debt ratio is expected to remain flat with slight potential improvement exiting 2025 compared to the 2.54x reported at the end of 2024.

ATN outlined five strategic priorities for 2025, focusing on leveraging its expanded networks, refocusing efforts on business and carrier customers, reducing capital expenditures, advancing cost containment actions, and managing the balance sheet to enhance cash flow and lower leverage.

The company's long-term investment thesis remains centered on its position as a provider of critical communications infrastructure in underserved markets:

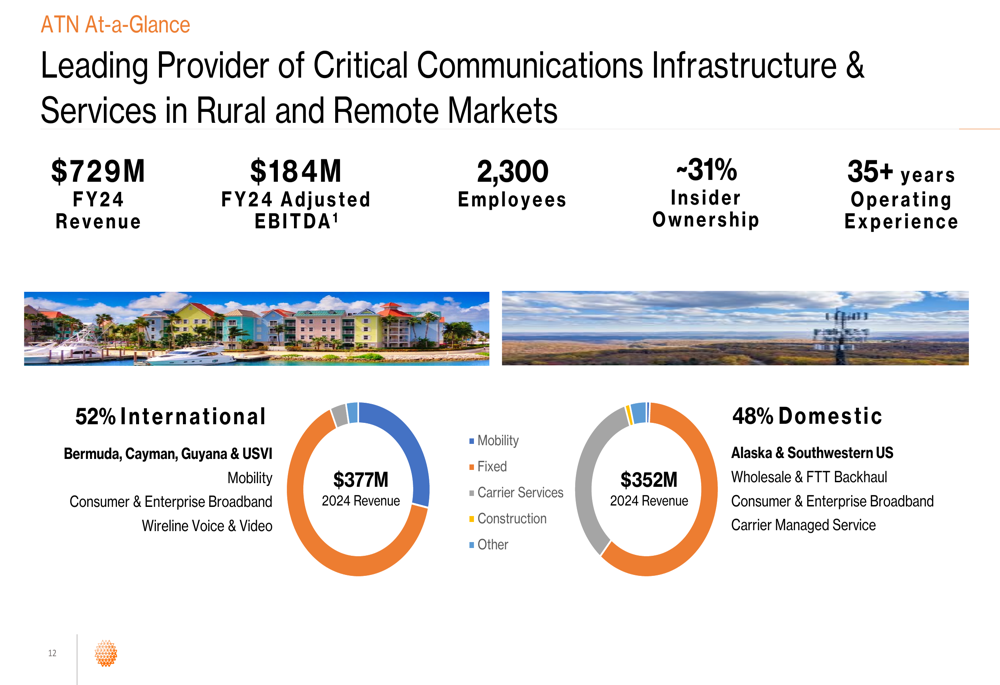

With $729 million in FY24 revenue, $184 million in FY24 Adjusted EBITDA, and a workforce of 2,300 employees, ATN continues to leverage its 35+ years of operating experience and significant insider ownership (approximately 31%) to drive long-term value creation.

The market's strongly positive reaction to the earnings results, with the stock closing up 18.9% at $17.24, suggests investors are encouraged by the company's improved operational efficiency and strategic focus on cost containment while maintaining steady growth in key areas. The premarket trading showed additional gains of 3.52%, indicating continued investor optimism about ATN's performance and outlook.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.