Street Calls of the Week

Introduction & Market Context

Auto Partner SA (APR) presented its H1 2025 financial results on September 18, 2025, reporting record revenue exceeding PLN 2.2 billion despite challenging market conditions. The company’s stock responded positively to the presentation, closing up 6.92% at PLN 18.20.

As one of Poland’s largest auto parts distributors with nearly 10% market share, Auto Partner operates in a mature European automotive aftermarket characterized by aging vehicle fleets. The average age of passenger cars stands at 15.1 years in Poland and 12.3 years across the European Union, creating sustained demand for replacement parts.

The company’s comprehensive overview highlights its extensive operations and market positioning:

H1 2025 Financial Performance Highlights

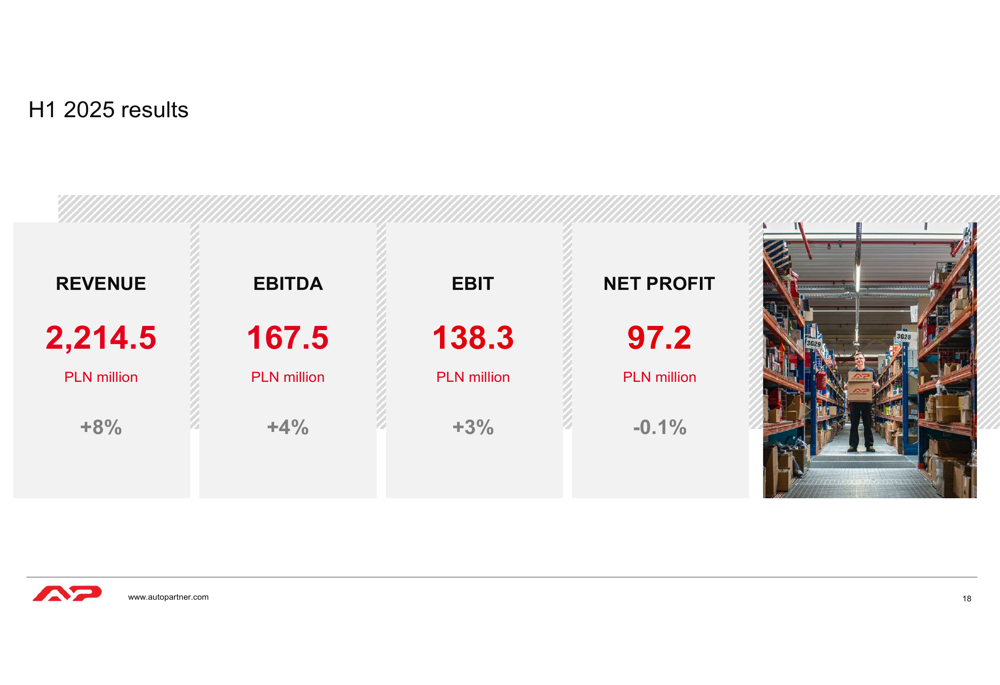

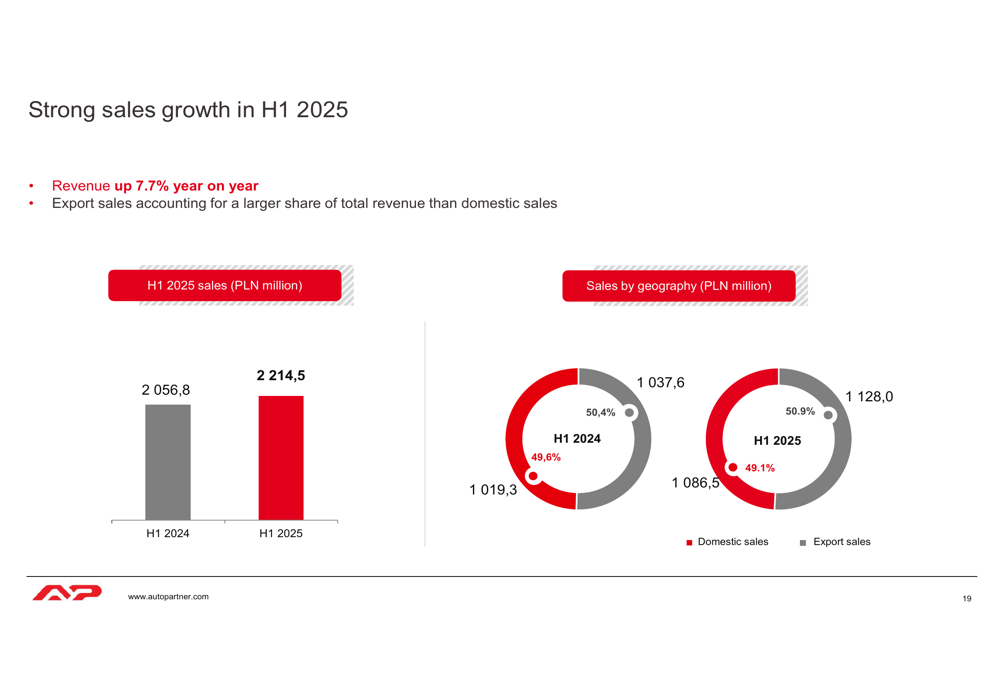

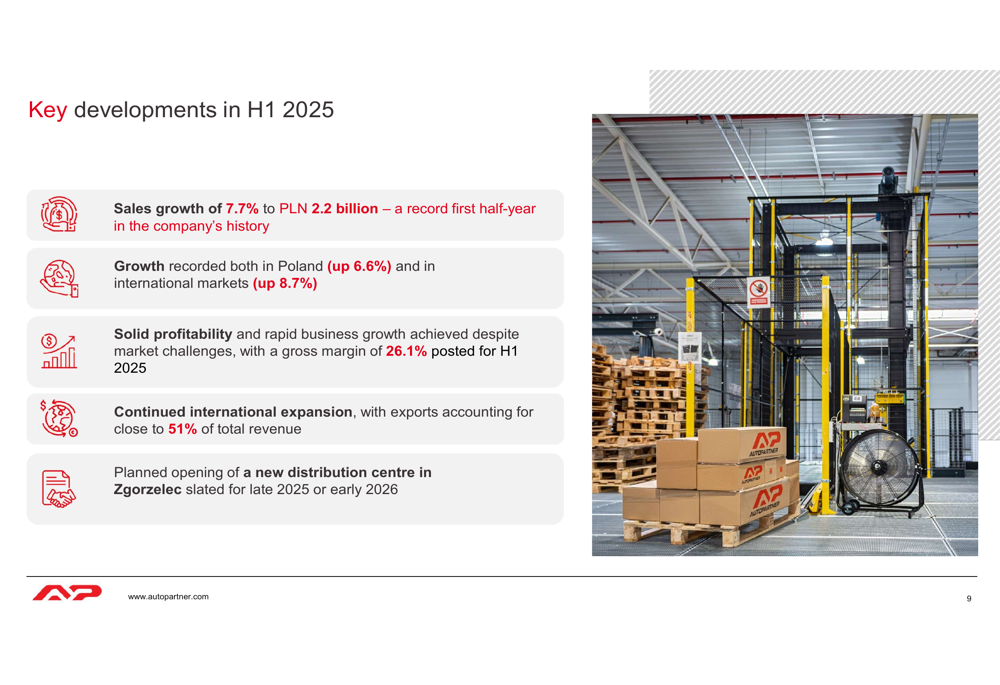

Auto Partner reported strong financial results for the first half of 2025, with revenue reaching PLN 2,214.5 million, representing a 7.7% increase year-over-year. The company maintained solid profitability metrics despite facing cost and wage pressures in the market.

As shown in the following summary of key financial indicators, Auto Partner delivered growth across most metrics:

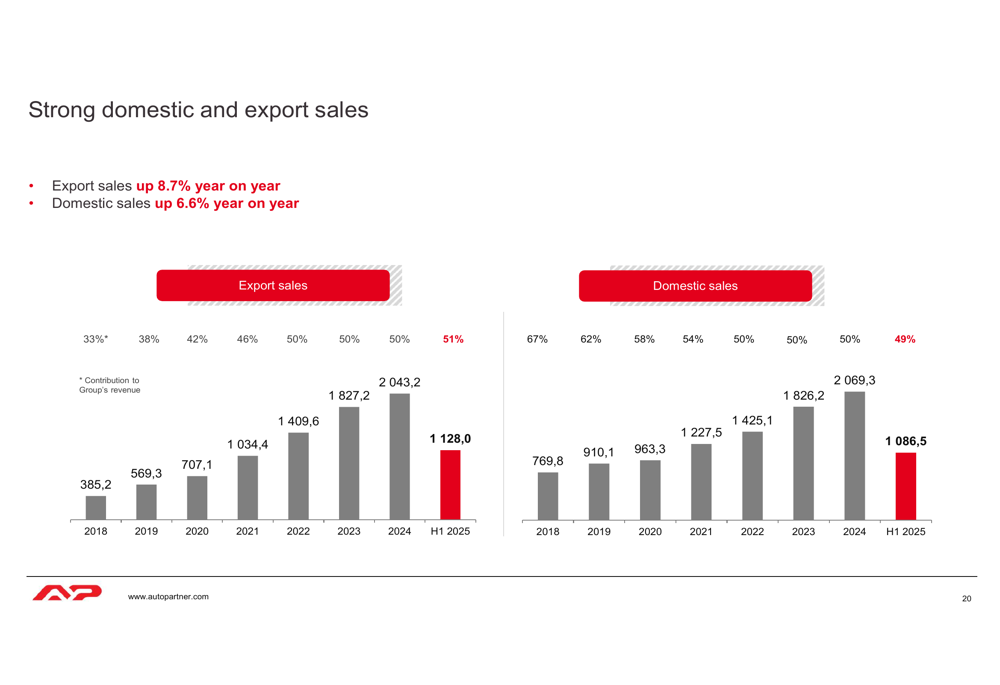

The company’s revenue growth was driven by both domestic and international markets. Notably, export sales now account for 50.9% of total revenue, marking a significant milestone in Auto Partner’s internationalization strategy. Export sales grew 8.7% year-over-year to PLN 1,128.0 million, while domestic sales increased 6.6% to PLN 1,086.5 million.

The following chart illustrates the breakdown of sales by geography:

The company has demonstrated consistent growth in both domestic and export markets over recent years, as shown in this historical comparison:

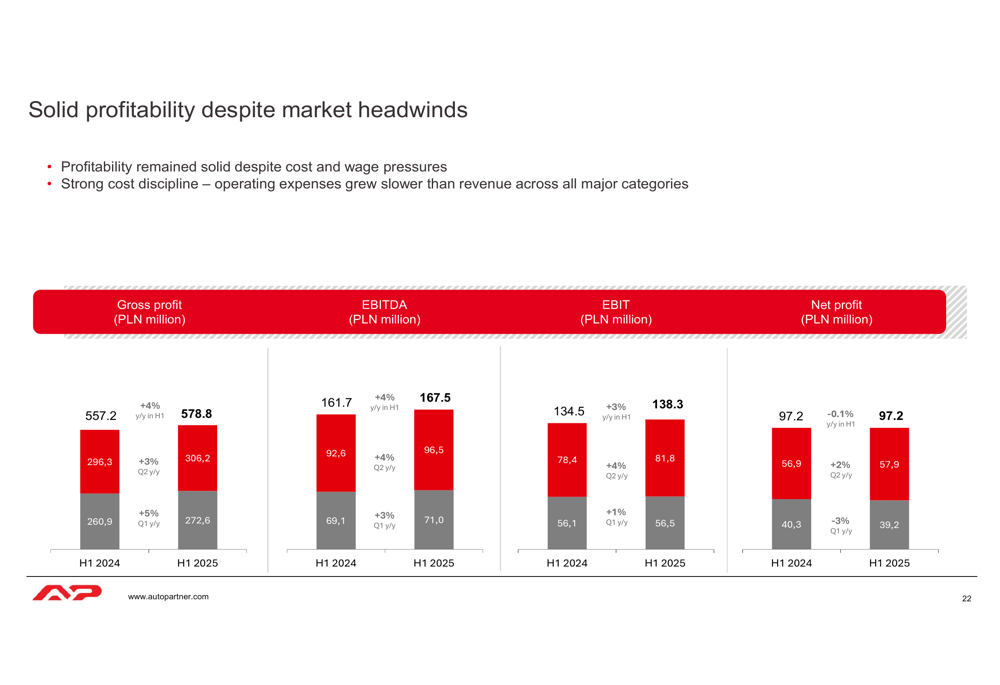

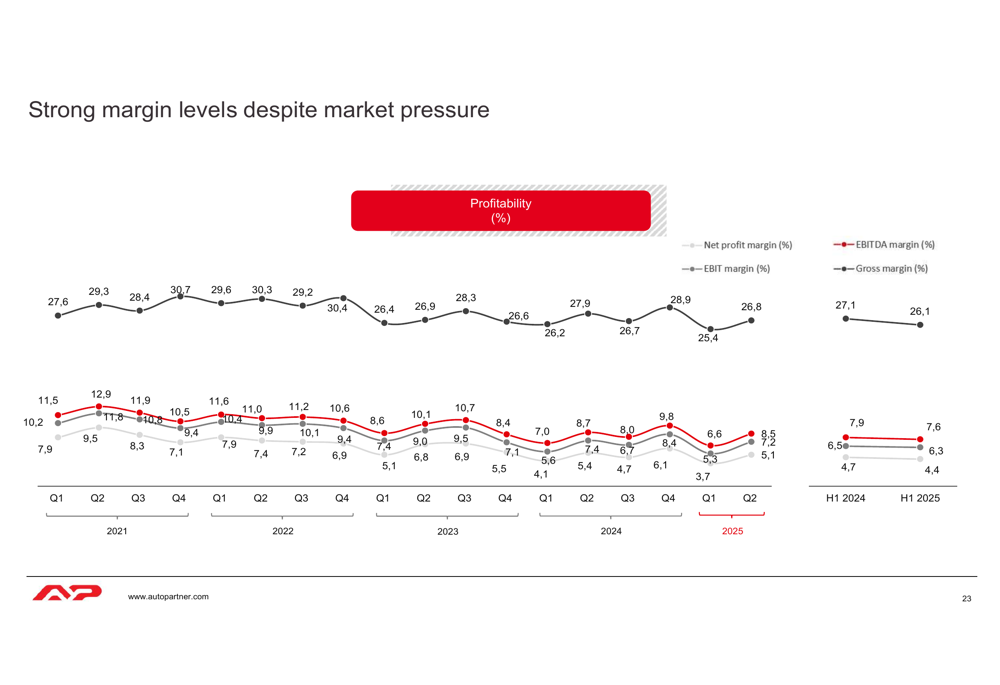

Despite market headwinds, Auto Partner maintained solid profitability levels. Gross profit reached PLN 578.8 million, while EBITDA and EBIT came in at PLN 167.5 million and PLN 138.3 million respectively. Net profit remained essentially flat at PLN 97.2 million (-0.1% year-over-year).

The company’s margin performance remained resilient in the face of market pressures:

International Expansion Strategy

Auto Partner’s international expansion continues to be a key growth driver, with exports now representing 50.9% of total revenue. The company’s distribution network spans across Europe, with particularly strong presence in Central and Eastern European markets.

To support its growth strategy, Auto Partner has signed an agreement for a new warehouse in Germany (4,500 m²) in August 2025. Additionally, the company is planning to open a new distribution center in Zgorzelec, adding 30,000 m² of warehouse space in late 2025 or early 2026.

The following image illustrates Auto Partner’s expanding warehouse footprint:

The new Zgorzelec distribution center represents a significant investment in the company’s logistics infrastructure and is positioned to become Auto Partner’s most advanced and highly automated logistics hub. This expansion will increase the company’s total warehouse capacity by approximately 30% (excluding branch offices).

Operational Efficiency and Margin Management

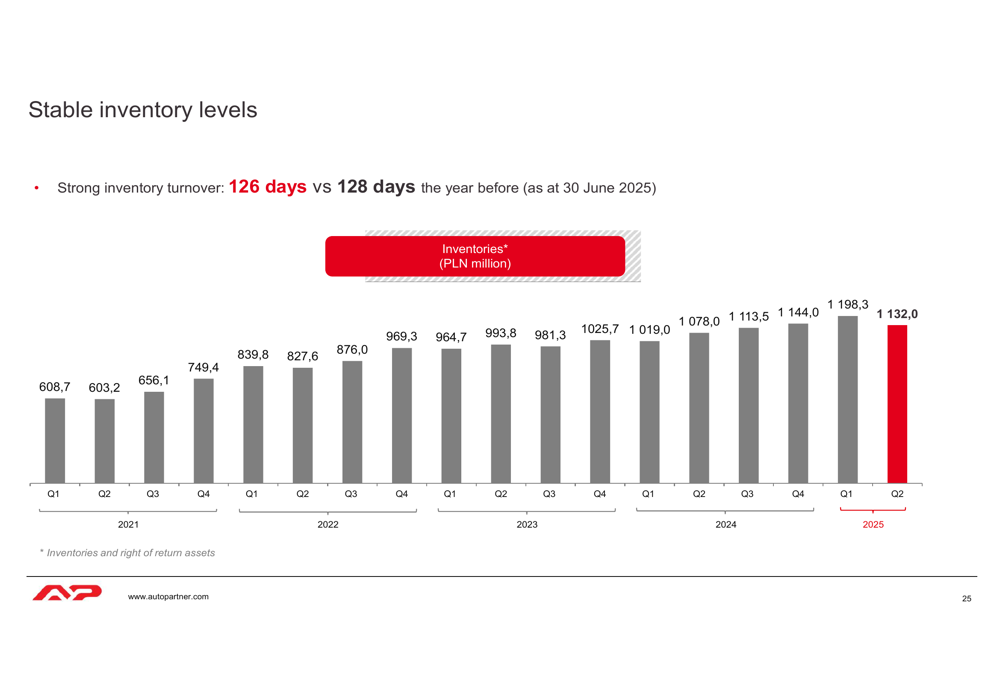

Auto Partner has maintained strong inventory management practices, with inventory turnover improving to 126 days compared to 128 days in the previous year. The company reported stable inventory levels despite the growth in sales volume.

As shown in the following chart, inventory levels have remained well-managed:

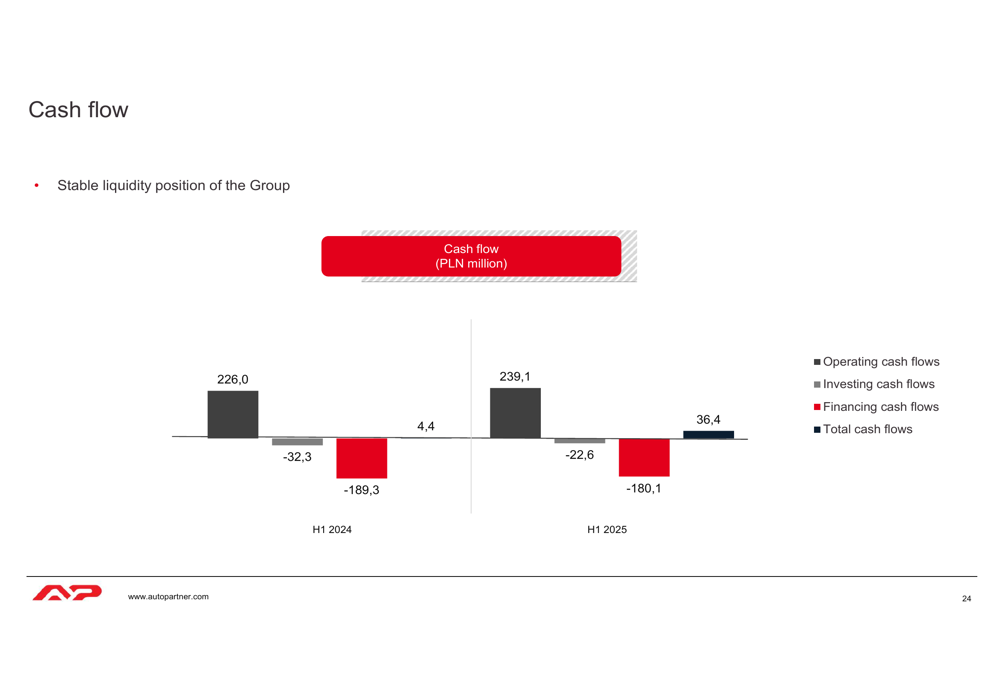

The company’s cash flow position remains healthy, with operating cash flows of PLN 239.1 million for H1 2025. After accounting for investing and financing activities, total cash flow for the period was positive at PLN 36.4 million. The company maintains a low debt level with a net debt/EBITDA ratio of 1.0x.

Auto Partner’s private label and exclusive brands continue to be an important component of its business strategy, contributing approximately 17% of total revenue. The company’s maXgear brand offers over 35,000 product references across 80 product groups, while other brands like ROCKS, Quaro, and RYMEC provide specialized offerings in various automotive categories.

Forward-Looking Statements and Growth Plans

Looking ahead, Auto Partner remains optimistic about the automotive parts distribution market despite challenging conditions. The company plans to focus on margins and cost control while continuing to expand its business scale.

Key developments highlighted for H1 2025 include:

The planned distribution center in Zgorzelec represents a significant step in Auto Partner’s growth strategy. This 30,000 m² facility will increase the company’s warehouse capacity by approximately 30% and is expected to enhance operational efficiency through advanced automation.

Management emphasized that the company’s continued growth is supported by product mix expansion, better alignment with customer needs across different price segments, and steadily optimized customer service. With a strong balance sheet and positive cash flow, Auto Partner appears well-positioned to execute its expansion plans while maintaining financial discipline.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.