Tyson Foods to close major Nebraska beef plant amid cattle shortage - WSJ

AvalonBay Communities Inc (NYSE:AVB) presented its third-quarter 2025 results on October 30, revealing performance below expectations and a reduced full-year outlook, while highlighting potential tailwinds from reduced supply in 2026 and strong development yields.

Quarterly Performance Highlights

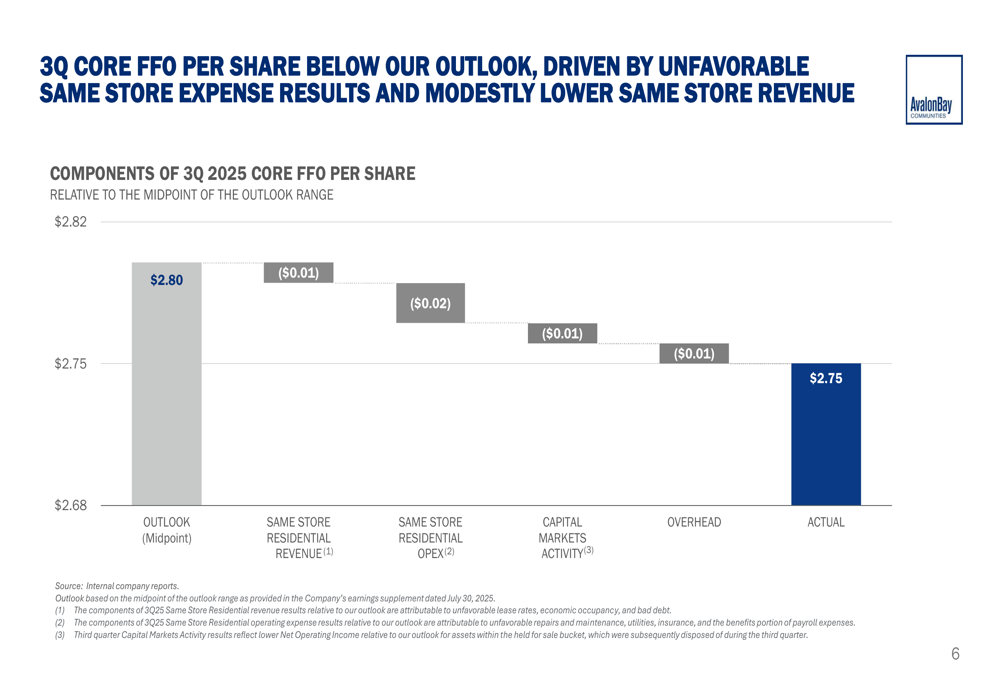

AvalonBay reported Core FFO per share growth of just 0.4% year-over-year for Q3 2025, significantly below the company's expectations. Same Store Residential Revenue Growth came in at 2.3%, also falling short of projections. The company's actual Core FFO per share of $2.75 missed the midpoint outlook of $2.80, driven primarily by unfavorable same-store expense results and lower-than-expected revenue.

As shown in the following breakdown of Q3 Core FFO performance versus outlook:

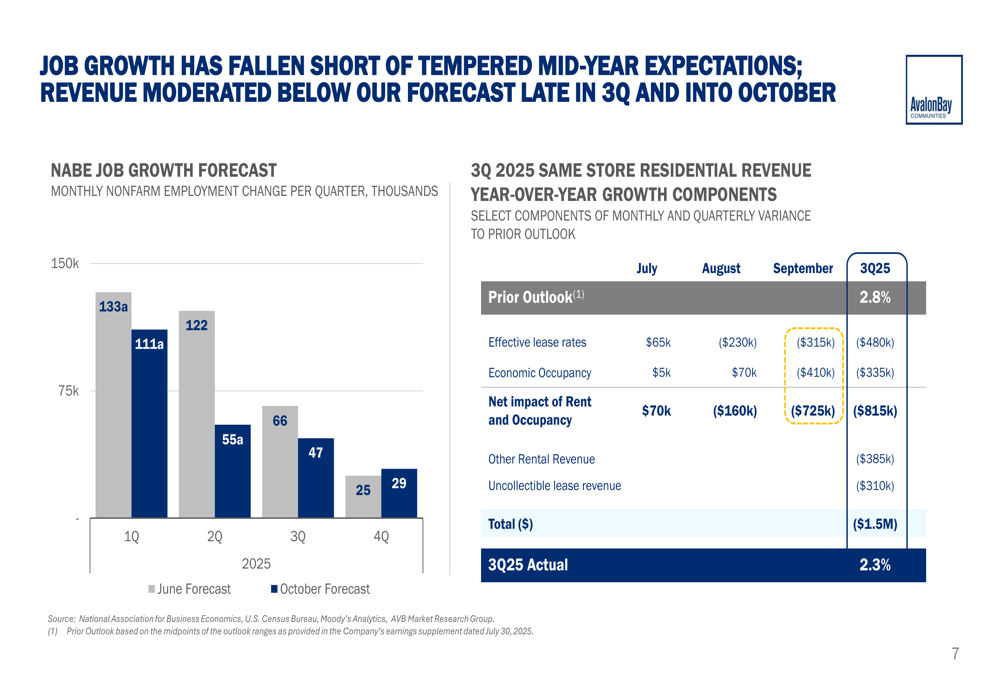

The company's Chief Executive Officer Ben Schall acknowledged the disappointing results, noting that revenue began moderating below forecast late in Q3 and continued into October. This softening was attributed partly to job growth falling short of expectations, as illustrated in the following chart comparing employment forecasts:

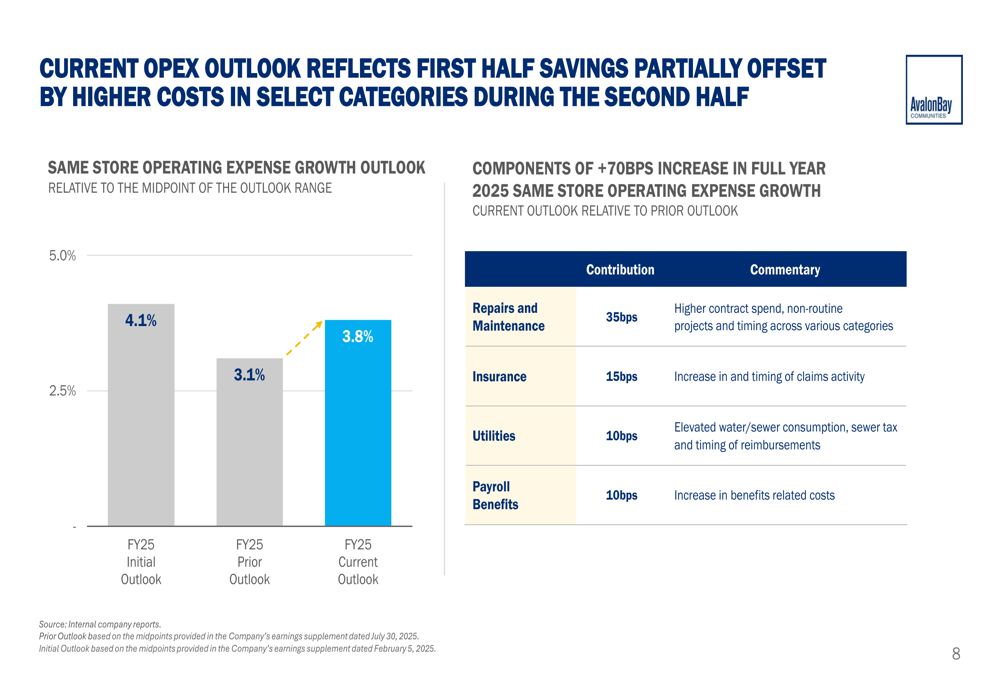

On the expense side, AvalonBay reported higher-than-expected operating costs across multiple categories. The company revised its full-year Same Store Operating Expense Growth outlook upward to 3.8% from the prior projection of 3.1%, citing increases in repairs and maintenance, insurance, utilities, and payroll benefits.

Revised Full-Year Outlook

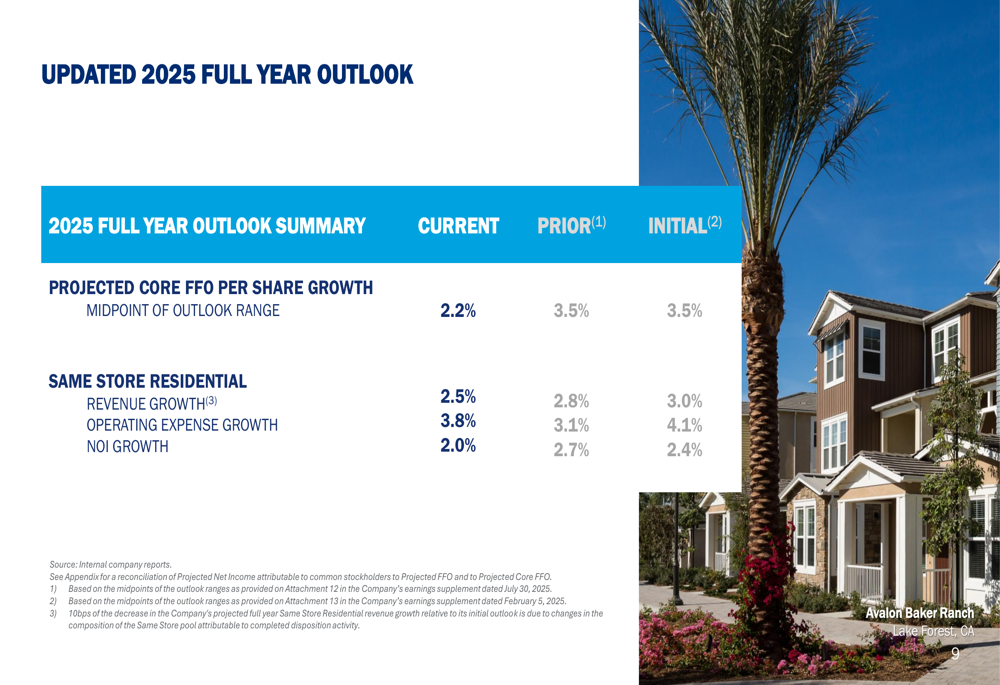

In response to the Q3 performance, AvalonBay significantly reduced its full-year 2025 outlook across key metrics. The company now projects Core FFO per share growth of 2.2%, down from the previous forecast of 3.5%. Same Store Residential Revenue Growth was revised downward to 2.5% from 2.8%, while NOI Growth was cut to 2.0% from 2.7%.

The following chart details these revisions:

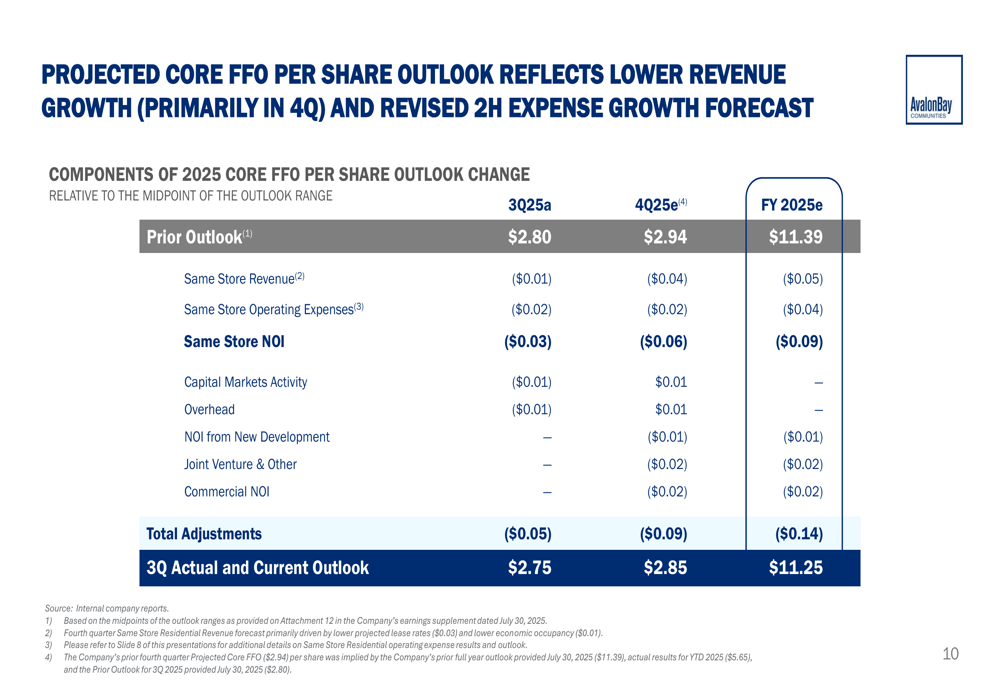

The company provided a detailed breakdown of the components driving the reduction in its Core FFO per share outlook, with Same Store NOI accounting for the largest negative impact at -$0.09 per share for the full year:

This outlook reduction represents a significant shift from the company's Q2 2025 position, when AvalonBay maintained its full-year core FFO guidance at $11.39 per share. The stock, which closed at $176.29 prior to the earnings release, was down 2.72% in premarket trading to $171.49, reflecting investor concerns about the deteriorating outlook.

Regional Performance Variations

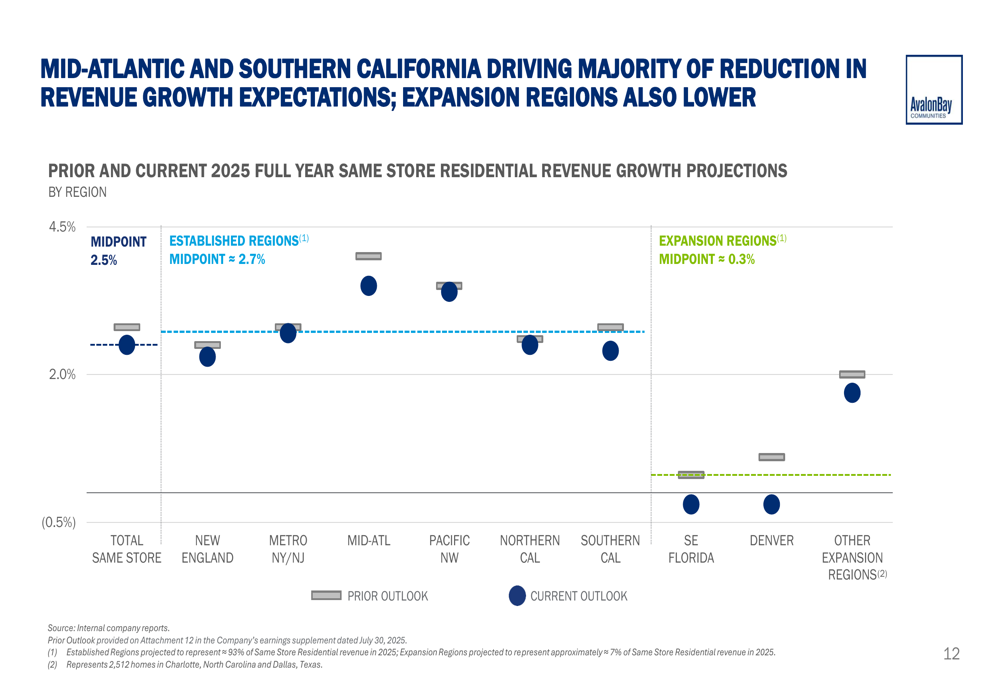

AvalonBay's presentation revealed significant variations in performance across its geographic footprint. While some regions maintained their growth projections, others experienced notable downgrades, with Southern California showing the most pronounced weakness, dropping from 2.0% to just 0.5% expected growth.

The following chart illustrates these regional differences:

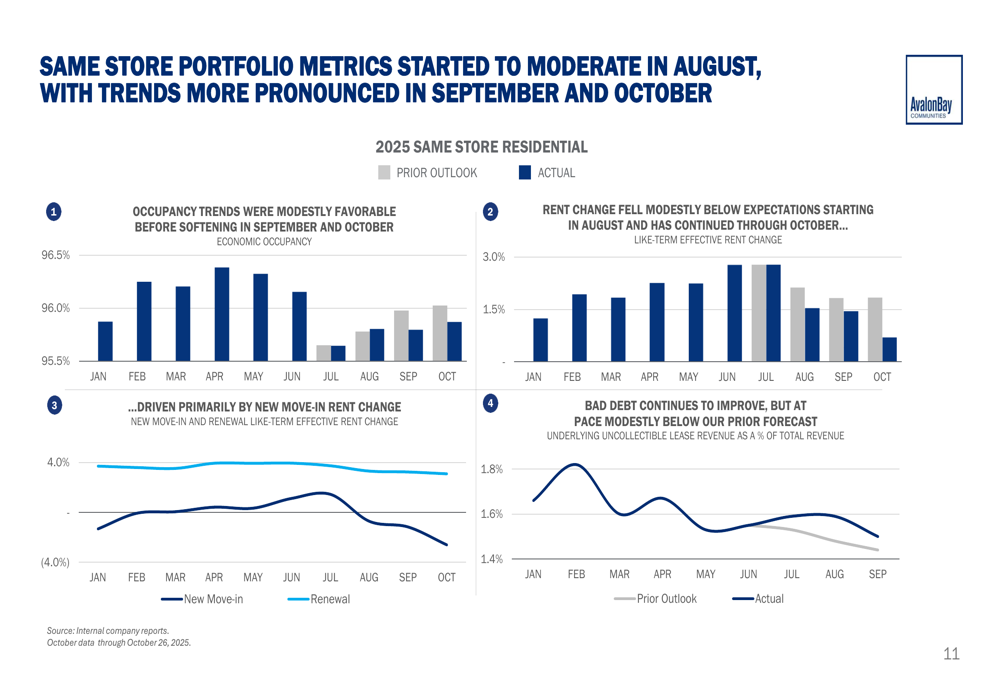

The company's Same Store portfolio metrics began showing signs of moderation in August, with trends becoming more pronounced in September and October. Occupancy trends were modestly favorable, but rent change fell and continues to face pressure.

Development Pipeline and Strategic Initiatives

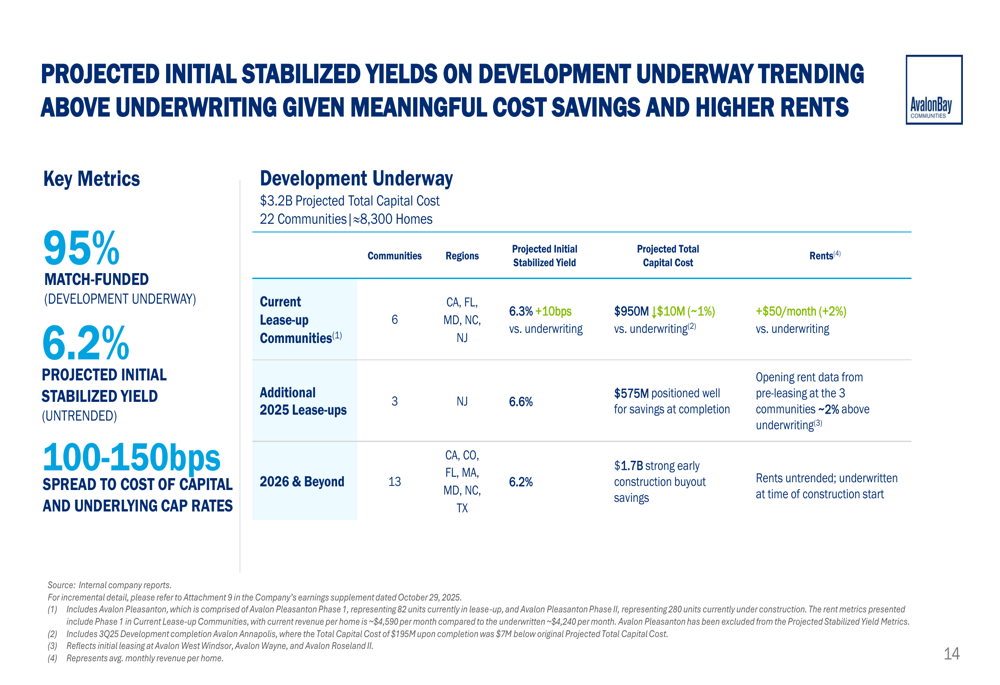

Despite near-term challenges, AvalonBay highlighted several potential tailwinds for 2026 and beyond. The company has approximately $3 billion of development underway, which it expects to provide incremental earnings and value creation upon stabilization. These projects are 95% match-funded with previously sourced capital and are trending above initial yield projections.

As shown in the following development yield data:

The company also pointed to favorable supply dynamics expected in 2026, with historically low levels of new apartment supply anticipated in its established regions. This reduced competition, combined with the increasing gap between mortgage payments and apartment rents, could support stronger revenue growth in the coming years.

Forward-Looking Statements

AvalonBay's key takeaways emphasized both the near-term challenges and longer-term opportunities. While acknowledging that Q3 results fell below expectations and the full-year outlook now reflects lower revenue growth and revised expense forecasts, management expressed confidence in the company's positioning for 2026 and beyond.

The company highlighted its preeminent balance sheet, which has been further strengthened by year-to-date capital markets activities, providing flexibility for capital allocation decisions. Management also noted substantial progress in advancing strategic focus areas in 2025, including increased suburban and expansion region allocations and projecting $9 million of incremental NOI from operating initiatives this year.

Looking ahead to 2026, AvalonBay identified both tailwinds and headwinds. Positive factors include falling construction starts industry-wide and lower competitive new supply expected in approximately 2-3 years. However, the company also acknowledged challenges from an elevated cost of capital and softening revenue environment.

With multifamily construction starts trending downward in 2024 and AvalonBay's development pipeline expected to increase to $3.7 billion, the company appears positioned to capitalize on reduced competition in the development space, potentially supporting stronger performance in future years despite current headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.