Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

Avery Dennison Corporation (NYSE:AVY) presented its second quarter 2025 financial results on July 22, showing resilience in a challenging environment marked by trade policy uncertainties. The materials and labeling solutions provider maintained stable margins despite experiencing an organic sales decline, as the company navigated tariff impacts particularly affecting its apparel and retail segments.

The company’s stock has been under pressure recently, trading at $179.01 as of July 21, 2025, well below its 52-week high of $233.48 but above its 52-week low of $157.00. Following a slight earnings miss in Q1 2025, investors have been closely monitoring the company’s ability to maintain profitability amid evolving trade policies.

Quarterly Performance Highlights

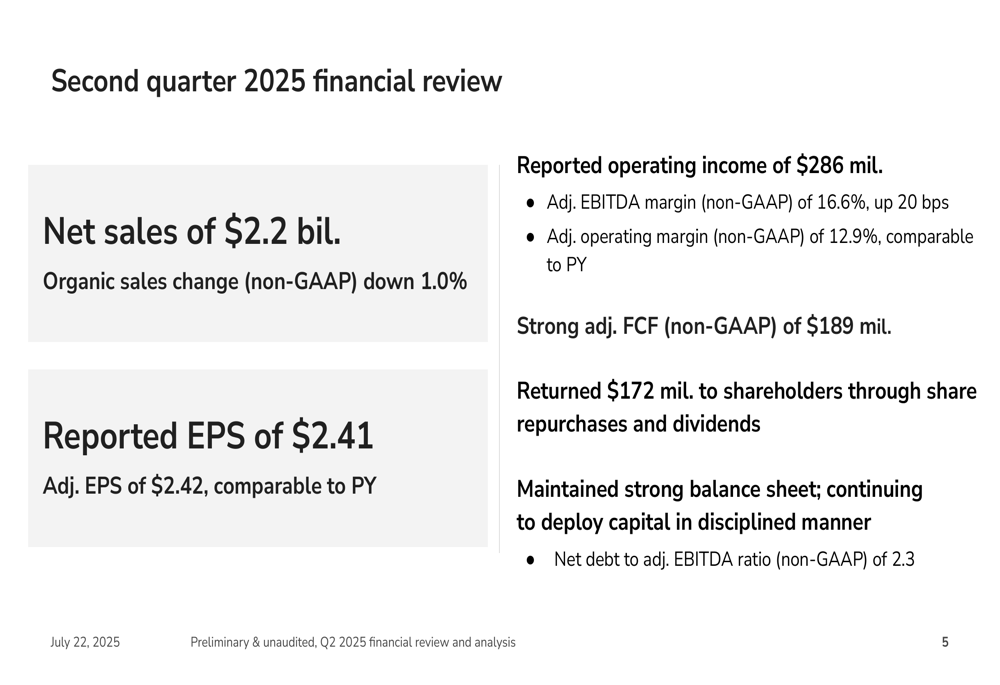

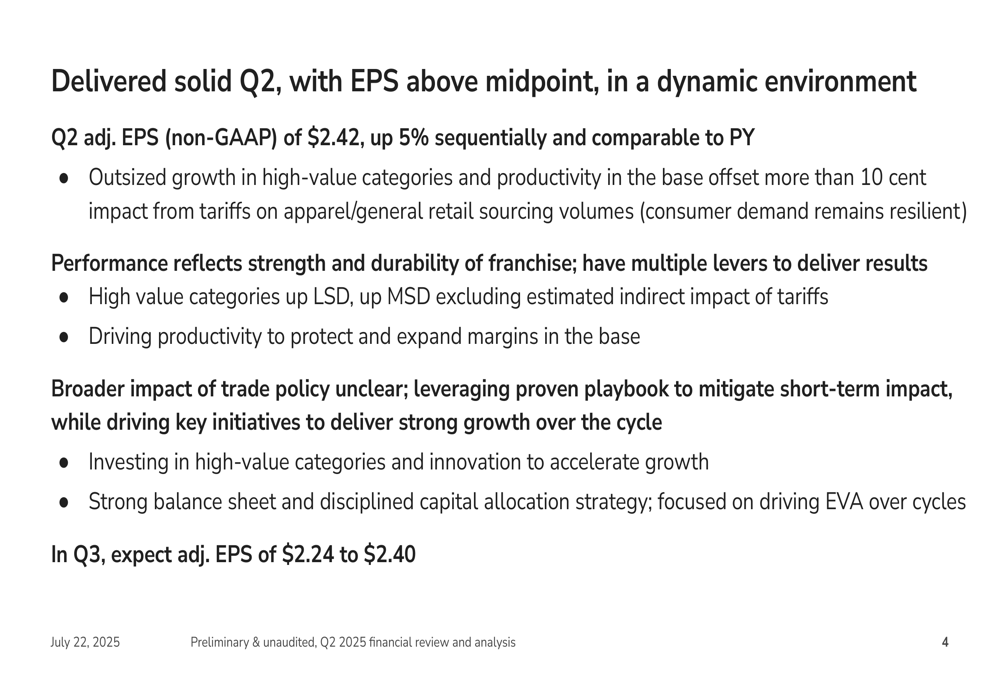

Avery Dennison reported adjusted earnings per share of $2.42 for Q2 2025, comparable to the prior year but up 5% sequentially from Q1. The company generated net sales of $2.2 billion, with organic sales declining 1.0% compared to the same period last year. Despite the sales pressure, Avery Dennison maintained solid profitability with an adjusted EBITDA margin of 16.6%, up 20 basis points year-over-year.

As shown in the following financial review summary:

The company generated strong adjusted free cash flow of $189 million during the quarter and returned $172 million to shareholders through share repurchases and dividends. Avery Dennison maintained a net debt to adjusted EBITDA ratio of 2.3, indicating a solid balance sheet position.

Management highlighted that productivity improvements in base operations helped offset more than 10 cents of EPS impact from tariffs on apparel and general retail sourcing volumes. The company’s Q2 performance demonstrated the strength and durability of its business model in challenging conditions.

Segment Analysis

Materials Group

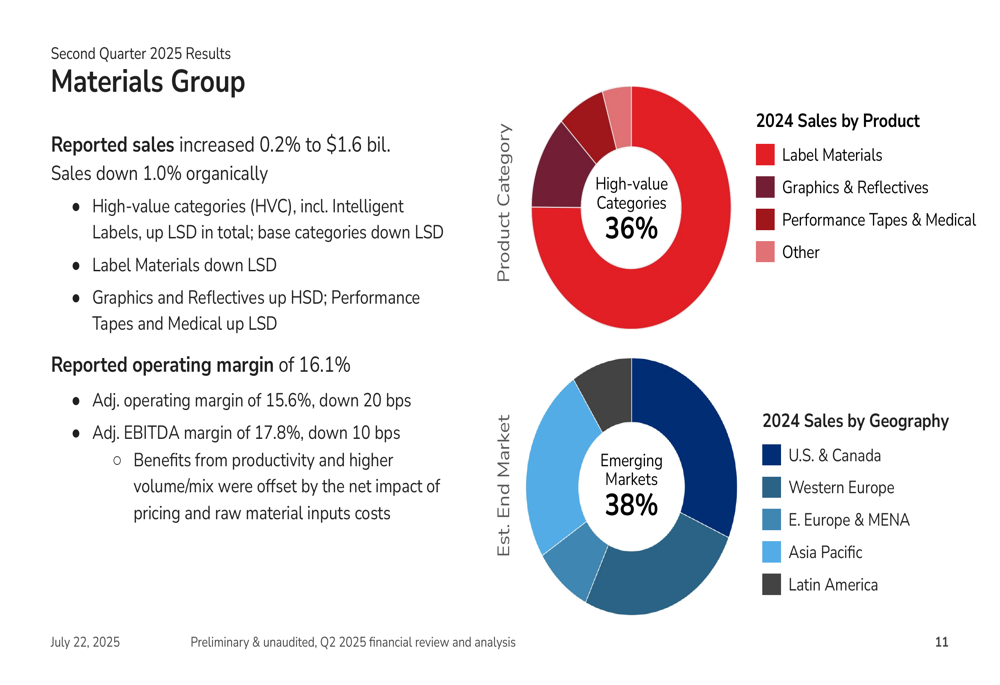

The Materials Group, which accounts for the larger portion of Avery Dennison’s business, reported a 0.2% increase in reported sales to $1.6 billion, though organic sales declined by 1.0%. The segment maintained a strong adjusted EBITDA margin of 17.8%, down only 10 basis points compared to the prior year.

Within the Materials Group, high-value categories including Intelligent Labels showed low-single-digit growth, while Graphics and Reflectives grew at high-single digits. Performance Tapes and Medical (TASE:BLWV) products achieved low-single-digit growth. The segment’s diversification across products and geographies is illustrated in the following breakdown:

Solutions Group

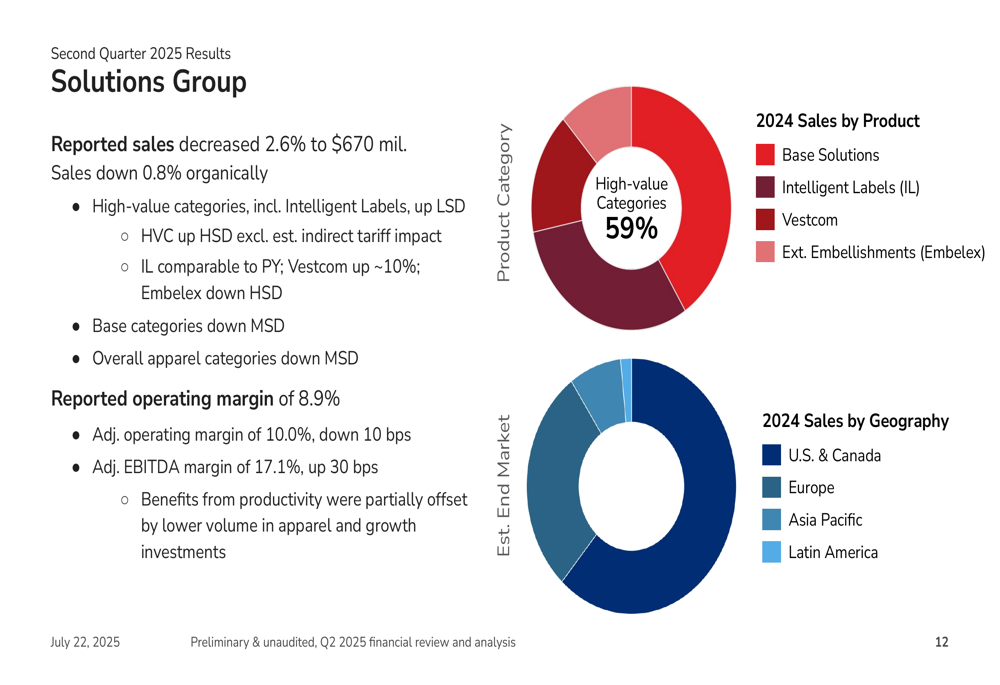

The Solutions Group faced greater challenges, with reported sales decreasing 2.6% to $670 million and organic sales declining 0.8%. Despite these headwinds, the segment improved its adjusted EBITDA margin to 17.1%, up 30 basis points from the prior year.

High-value categories within the Solutions Group grew at low-single digits, with management noting they would have achieved high-single-digit growth excluding the estimated indirect impact of tariffs. Vestcom, a recent acquisition, performed strongly with approximately 10% growth, while Embelex (external embellishments) declined at high-single digits.

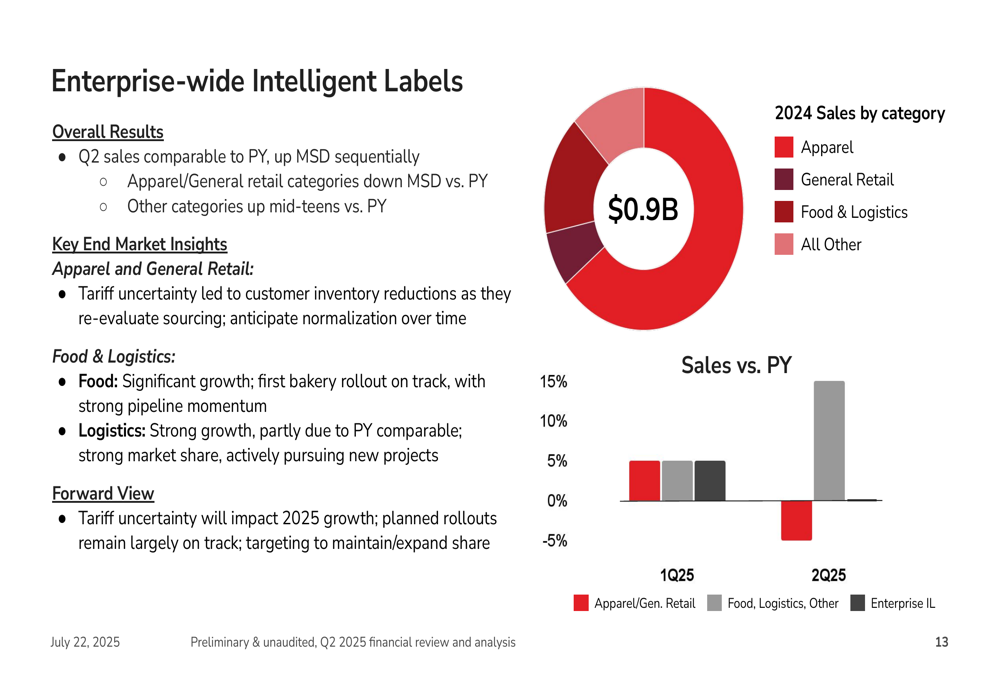

The company’s Intelligent Labels business, a key growth driver spanning both segments, reported Q2 sales comparable to the prior year but up mid-single digits sequentially. While apparel and general retail categories declined mid-single digits year-over-year, other categories grew in the mid-teens, demonstrating the diversification benefits within this strategic platform.

Trade Policy Impacts and Mitigation Strategies

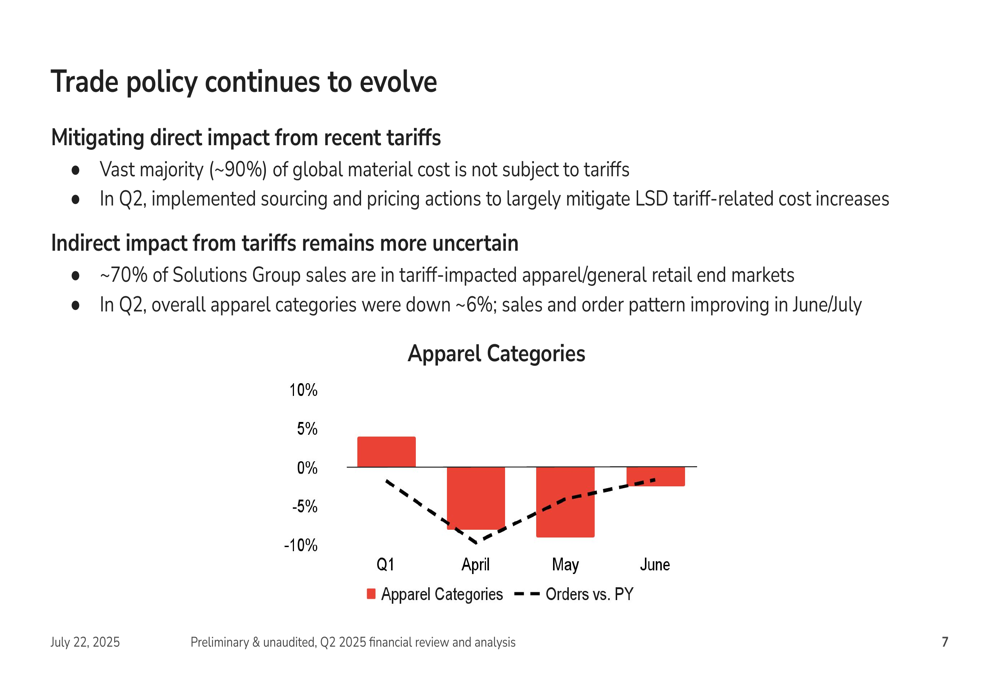

A significant focus of the presentation was the evolving trade policy landscape and its impact on Avery Dennison’s business. Management noted that approximately 70% of Solutions Group sales are in tariff-impacted apparel and general retail end markets, though the vast majority (about 90%) of global material costs are not subject to tariffs.

The following chart illustrates the impact on apparel categories throughout the quarter:

To mitigate these challenges, Avery Dennison implemented sourcing and pricing actions during Q2 that largely offset low-single-digit tariff-related cost increases. The company emphasized its global manufacturing footprint as a strategic advantage, with production facilities spread across North America, Europe, and Asia.

Management acknowledged that the broader impact of trade policy remains unclear but expressed confidence in the company’s proven strategies to navigate these uncertainties while continuing to drive long-term growth initiatives.

Forward Guidance and Outlook

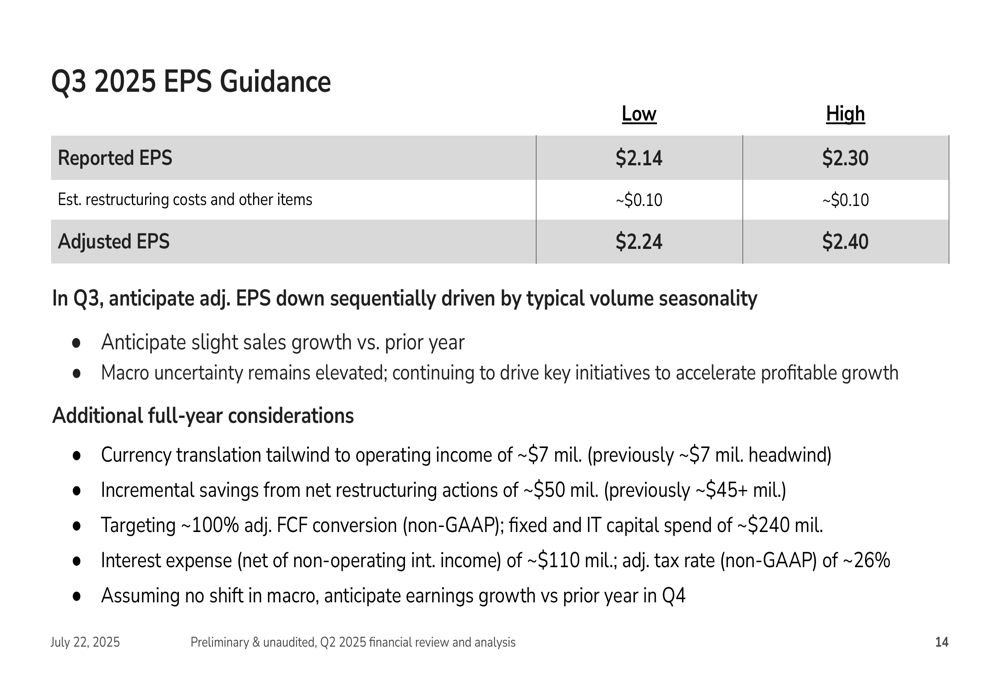

Looking ahead to the third quarter of 2025, Avery Dennison provided adjusted EPS guidance of $2.24 to $2.40, as shown in the following guidance table:

Management anticipates sequential earnings decline in Q3 driven by typical volume seasonality but expects slight sales growth compared to the prior year. For the full year, the company highlighted several considerations, including a currency translation tailwind, incremental savings from restructuring initiatives, and a target of approximately 100% adjusted free cash flow conversion.

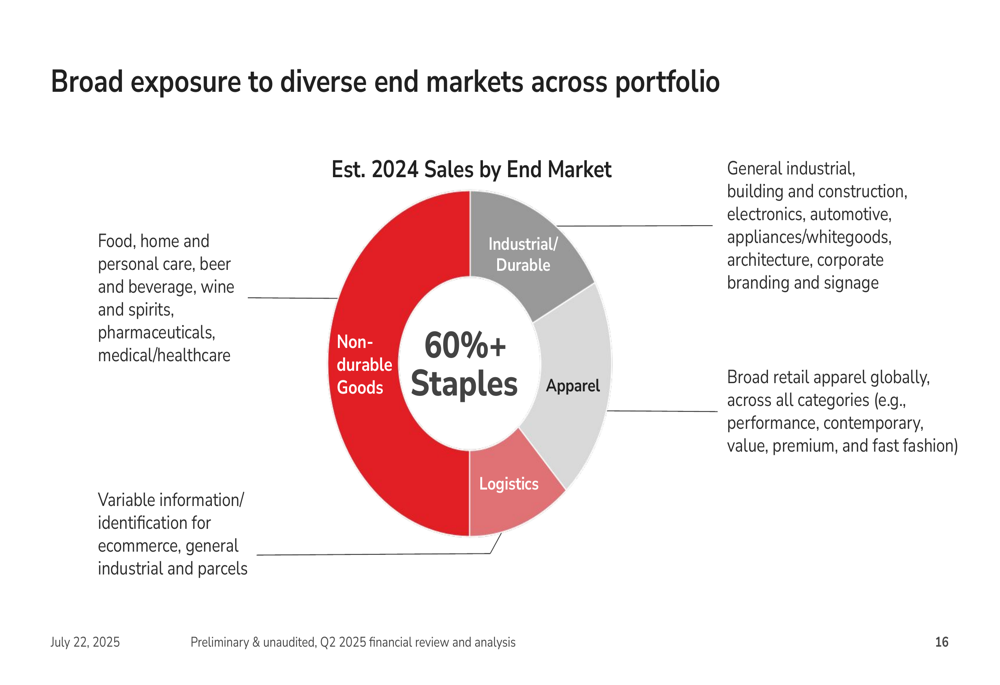

The company’s diversified end-market exposure provides some resilience against economic volatility, with over 60% of sales coming from non-durable goods, many of which are staples like food and healthcare products.

Strategic Positioning

Avery Dennison continues to emphasize its strategic focus on high-value categories, which delivered sales of approximately $1.0 billion in Q2, growing at low-single digits organically and at mid-single digits excluding the estimated impact of tariffs. These high-value offerings now represent a significant portion of the company’s portfolio, accounting for 36% of Materials Group sales and 59% of Solutions Group sales.

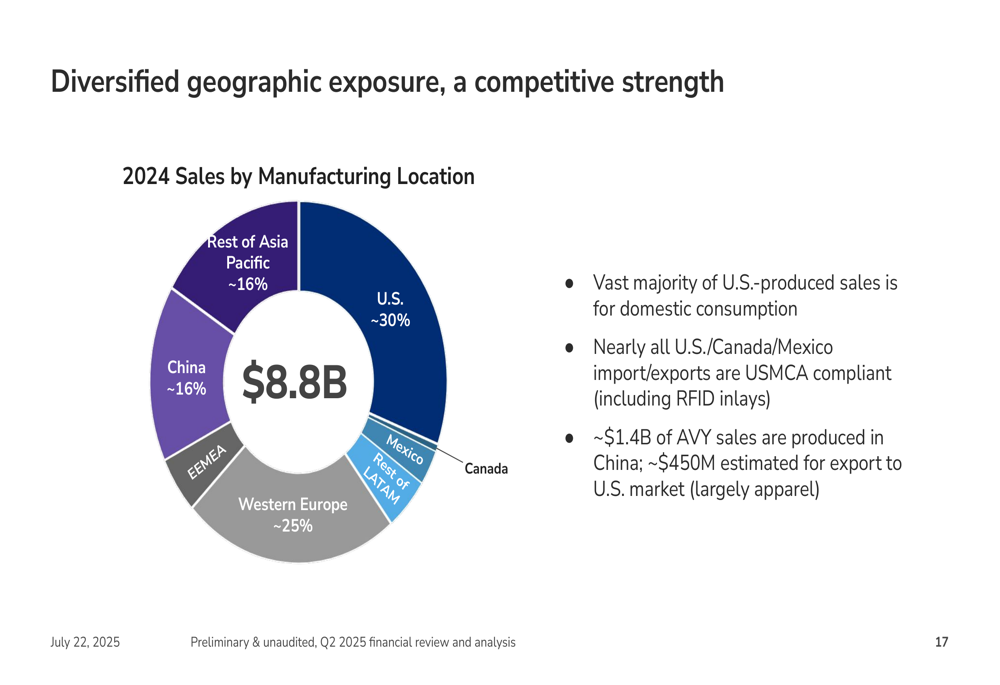

The company’s geographic diversification also serves as a competitive strength, with manufacturing locations spread across multiple regions to serve local markets efficiently and mitigate trade-related risks.

Despite near-term challenges from trade policies and slowing organic growth, Avery Dennison’s Q2 2025 presentation demonstrated the company’s ability to maintain profitability through productivity improvements and strategic focus on high-value categories. With a strong balance sheet and consistent cash flow generation, the company appears well-positioned to navigate current uncertainties while continuing to invest in long-term growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.