Apple announces iPhone 17 with 48MP cameras and 6.3-inch display

Introduction & Market Context

Avolta AG (SIX:AVOL) released its Q1 2025 Trading Update on May 15, 2025, showing continued growth momentum across most regions and business segments. The global travel retail operator reported solid financial performance with turnover growth and margin expansion, while continuing to reduce leverage and maintain strong liquidity.

On the day of the presentation, Avolta shares closed at CHF 44.70, down 1.12% (CHF -0.5), though the stock remains near its 52-week high of CHF 45.16.

Quarterly Performance Highlights

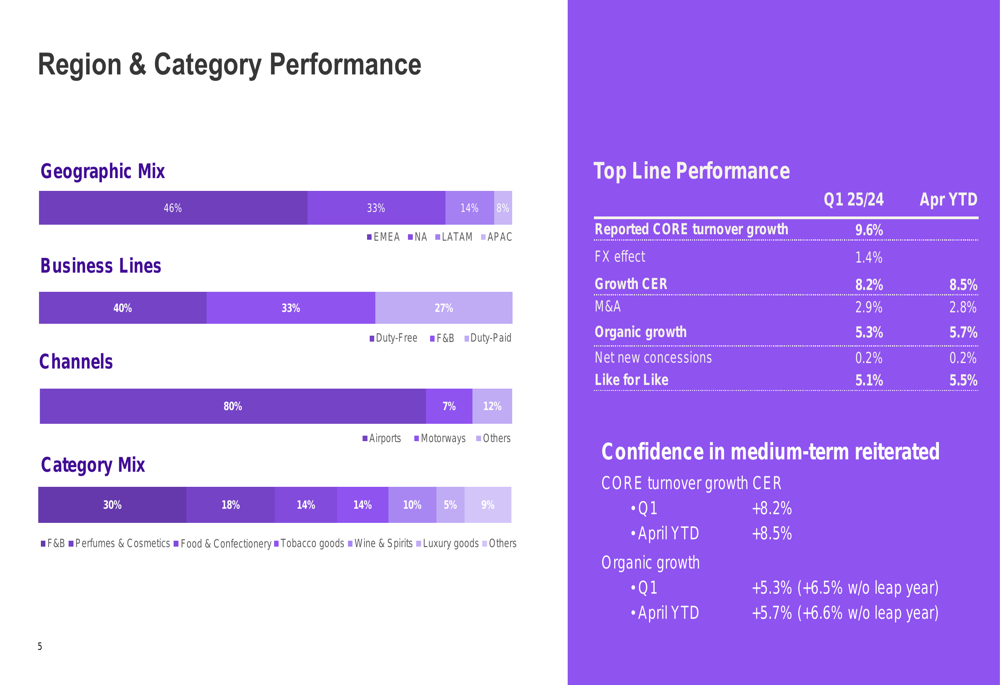

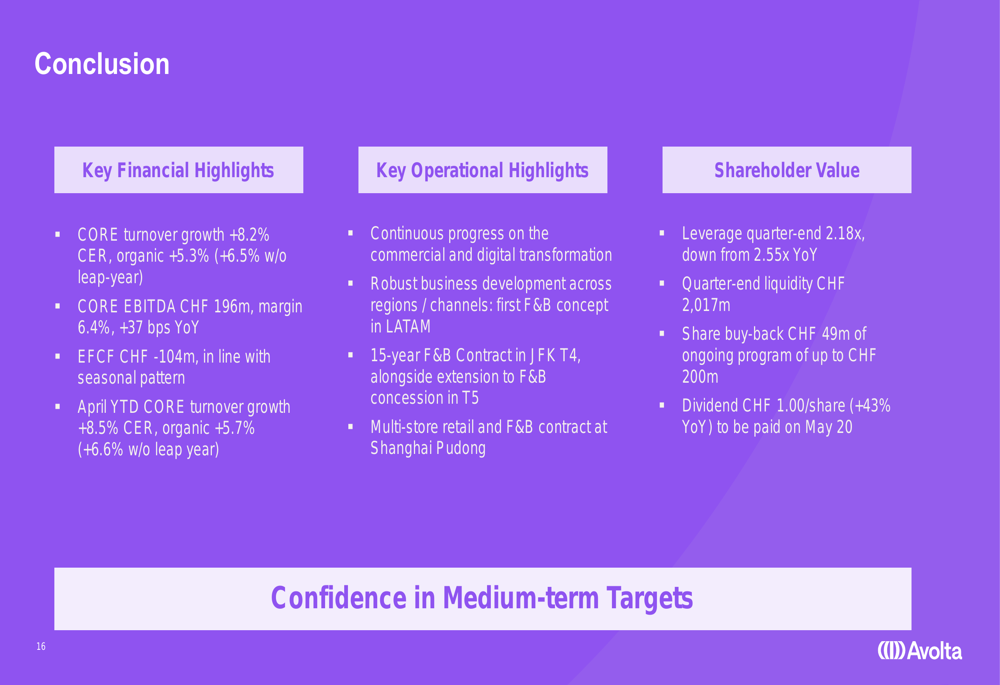

Avolta reported CORE turnover growth of 8.2% at constant exchange rates (CER) for Q1 2025, with organic growth of 5.3%, which rises to 6.5% when adjusted for the leap year effect. This positive momentum continued into April, with year-to-date CORE turnover growth of 8.5% CER and organic growth of 5.7% (6.6% without leap year effect).

As shown in the following key financial figures:

CORE EBITDA reached CHF 196 million, representing a significant 16.3% year-over-year increase. The EBITDA margin expanded by 37 basis points to 6.4%, driven by commercial performance, heightened cost discipline, productivity increases, and active portfolio management.

The company’s Equity Free Cash Flow (EFCF) was negative CHF 104 million, which management noted was in line with typical seasonal patterns, as Q1 and Q4 are typically negative or neutral quarters for cash flow, while Q2 and Q3 represent peak cash generation periods.

Regional Performance Analysis

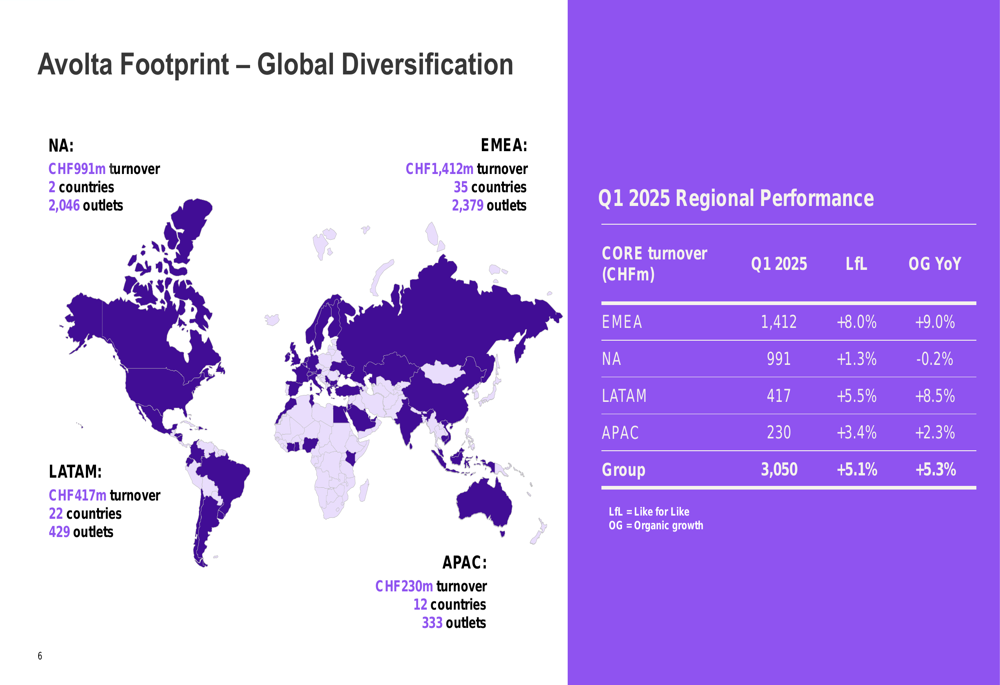

Avolta’s global footprint spans 71 countries with over 5,000 outlets, providing significant geographic diversification. The company’s performance varied by region, with EMEA and LATAM showing the strongest organic growth.

The following breakdown illustrates the company’s global diversification and regional performance:

EMEA (Europe, Middle East, and Africa) remained the largest contributor to turnover at 46% of the total, generating CHF 1,412 million with impressive 9.0% organic growth and 8.0% like-for-like growth. North America, representing 33% of turnover at CHF 991 million, showed modest like-for-like growth of 1.3% but a slight organic decline of 0.2%.

Latin America continued its strong performance with 8.5% organic growth on turnover of CHF 417 million, while Asia-Pacific delivered 2.3% organic growth on CHF 230 million in turnover.

The company’s business mix shows a balanced portfolio across channels and categories:

Strategic Initiatives and Business Development

Avolta highlighted several key business development achievements during Q1 2025, including new contract wins and the expansion of its digital initiatives. The company secured a 15-year food and beverage contract at JFK Terminal 4 in New York, alongside an extension to its existing concession in Terminal 5. Additionally, Avolta won a multi-store retail and F&B contract at Shanghai Pudong Airport in China, scheduled to open in the first half of 2025.

The company opened 32 new stores during the quarter, including its first F&B concept in Latin America at São Paulo/Congonhas Airport. Innovative new concepts included two Fragonard boutiques at Nice International Airport and the Gourmand Barcelona T1.

Digital transformation remains a priority, with the Club Avolta loyalty program recruiting over 1 million new members in Q1 2025 and establishing new partnerships with Finnair and Singapore Airlines (OTC:SINGY). The company also introduced entertainment technology initiatives such as the Club Avolta Racing Simulator and an augmented reality treasure hunt feature in its app.

Financial Position and Capital Allocation

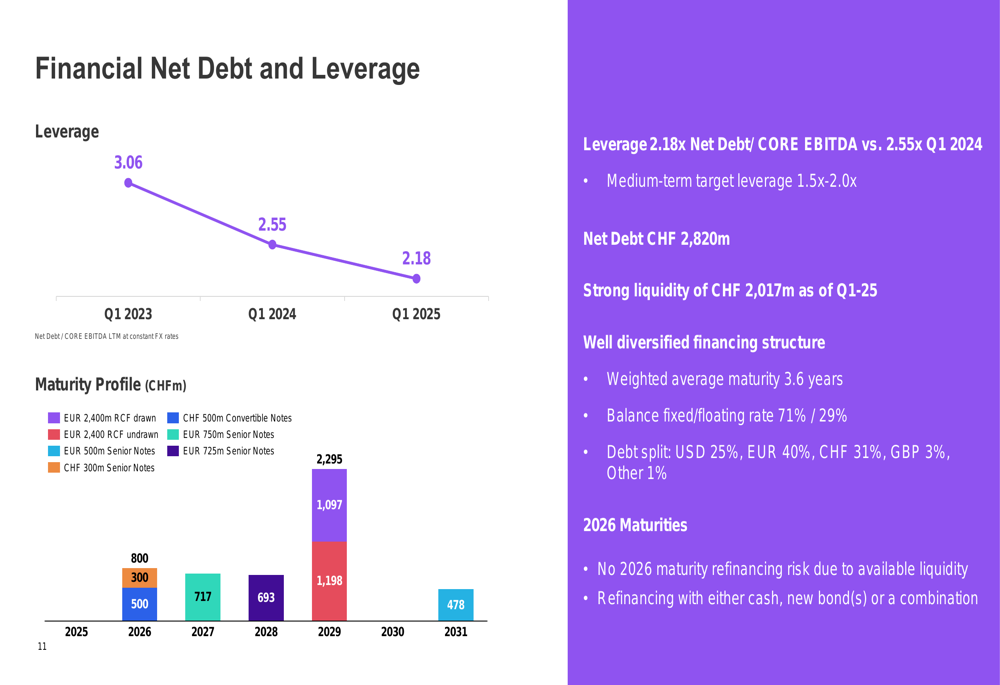

Avolta continued to strengthen its financial position during Q1 2025, reducing its leverage ratio to 2.18x net debt to CORE EBITDA, down from 2.55x in Q1 2024 and 3.06x in Q1 2023. This progress moves the company closer to its medium-term target leverage range of 1.5x-2.0x.

The following chart illustrates this positive trend in leverage reduction:

The company maintained strong liquidity of CHF 2,017 million as of Q1 2025, with a well-diversified financing structure having a weighted average maturity of 3.6 years. The debt is balanced between fixed (71%) and floating (29%) rates, with currency exposure primarily in EUR (40%), CHF (31%), and USD (25%).

Avolta’s capital allocation priorities remain unchanged, focusing on:

1. Investment in organic and inorganic growth through store network upgrades, digital transformation, business development, and selective M&A

2. Balance sheet efficiency with a target leverage ratio of 1.5x-2.0x

3. Capital returns through progressive dividends and share buybacks

The company approved a dividend of CHF 1.00 per share for FY 2024, representing a 43% year-over-year increase, to be paid on May 20, 2025. Additionally, Avolta executed CHF 49 million in share buybacks under its ongoing program of up to CHF 200 million.

Outlook and Forward Guidance

Avolta reaffirmed its medium-term outlook, expressing confidence in achieving:

- Organic growth of 5-7%

- EBITDA margin improvement of 20-40 basis points annually

- EFCF conversion improvement of 100-150 basis points per annum at constant exchange rates

The company highlighted its key upcoming events, including a Capital Markets Day scheduled for June 26, 2025, Half-Year Results on July 31, and a Q3 Trading Update on October 30.

The Q1 2025 performance, with organic growth of 5.3% (6.5% adjusted for leap year) and EBITDA margin expansion of 37 basis points, appears to position Avolta well to achieve its medium-term targets as it continues to expand its global footprint and enhance its digital capabilities in the travel retail sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.