Street Calls of the Week

Introduction & Market Context

AXA (EPA:CS) released its half-year 2025 earnings presentation on August 1, 2025, revealing solid financial performance across its business segments. The French insurance giant reported a 7% increase in revenues compared to the first half of 2024, building on the momentum seen in its Q1 results earlier this year.

The company’s stock closed at €42.63 prior to the earnings release, having gained 0.38% in the most recent trading session. Year-to-date, AXA shares have performed well, trading closer to their 52-week high of €42.79 than their low of €31.05.

Executive Summary

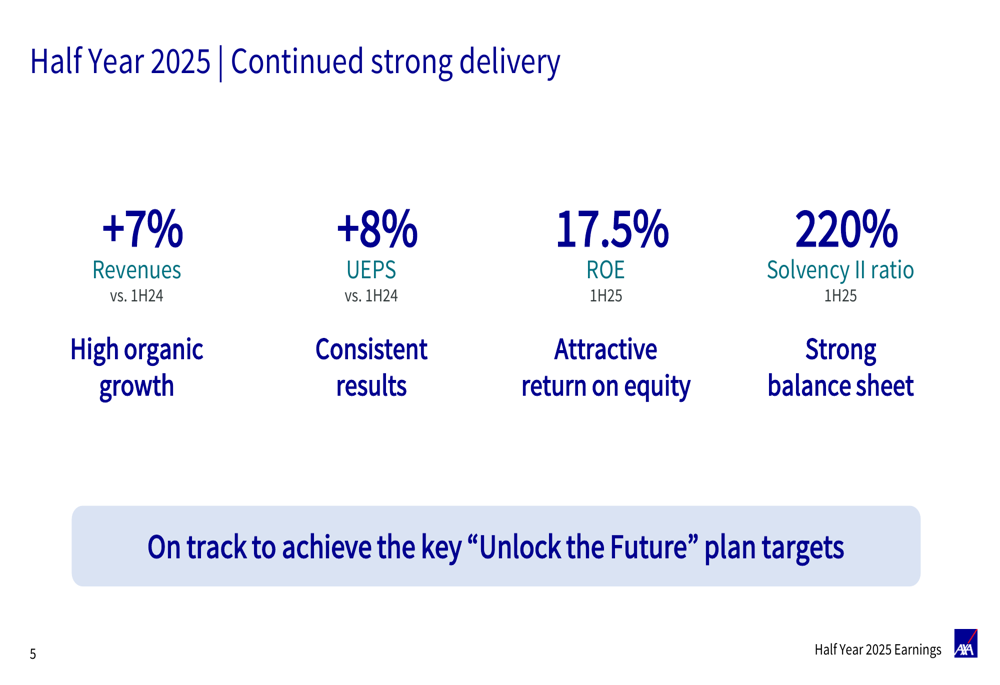

AXA delivered strong financial results for the first half of 2025, with consistent growth across key metrics. The company reported a 7% increase in revenues, an 8% rise in Underlying Earnings Per Share (UEPS), and an attractive Return on Equity (ROE) of 17.5%. The Solvency II ratio stood at a robust 220%, indicating a strong capital position.

As shown in the following summary of key financial metrics:

Thomas Buberl, Group CEO, emphasized that the company is "on track to achieve the key ’Unlock the Future’ plan targets," highlighting AXA’s consistent execution of its strategic initiatives.

The presentation also revealed a significant strategic move with the acquisition of Prima, a leading direct insurance player in Italy, for €0.5 billion for a 51% stake. This acquisition strengthens AXA’s Direct franchise and expands its footprint in the Italian market.

Detailed Financial Analysis

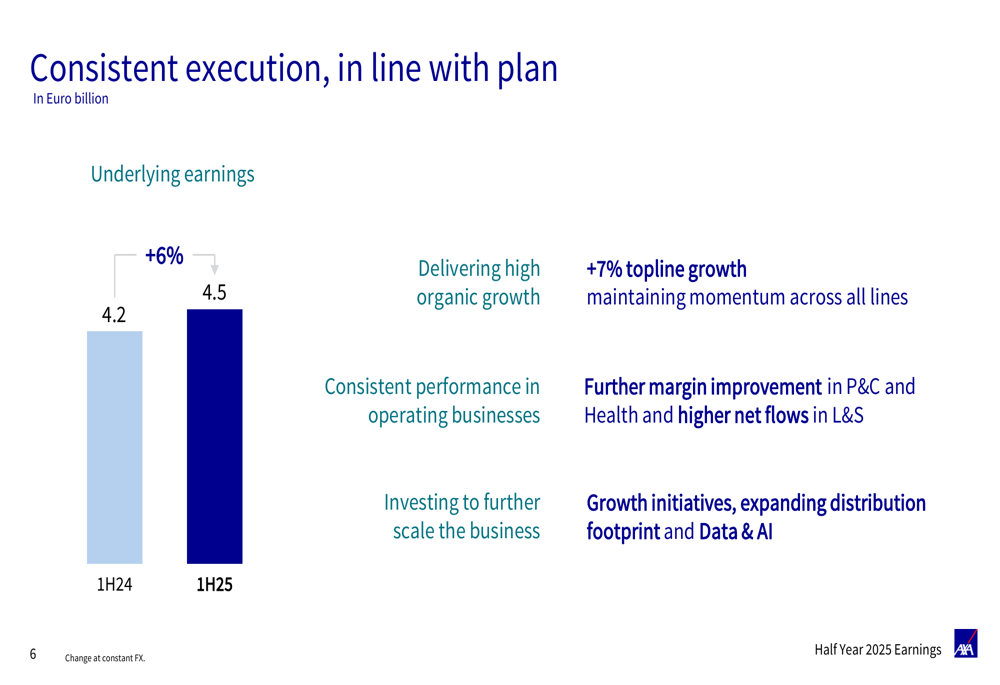

AXA’s underlying earnings increased from €4.2 billion in 1H24 to €4.5 billion in 1H25, representing a 6% growth. This performance was driven by high organic growth, consistent performance in operating businesses, and continued investments in growth initiatives, distribution expansion, and data and AI capabilities.

The following chart illustrates this consistent execution and earnings growth:

Property & Casualty Performance

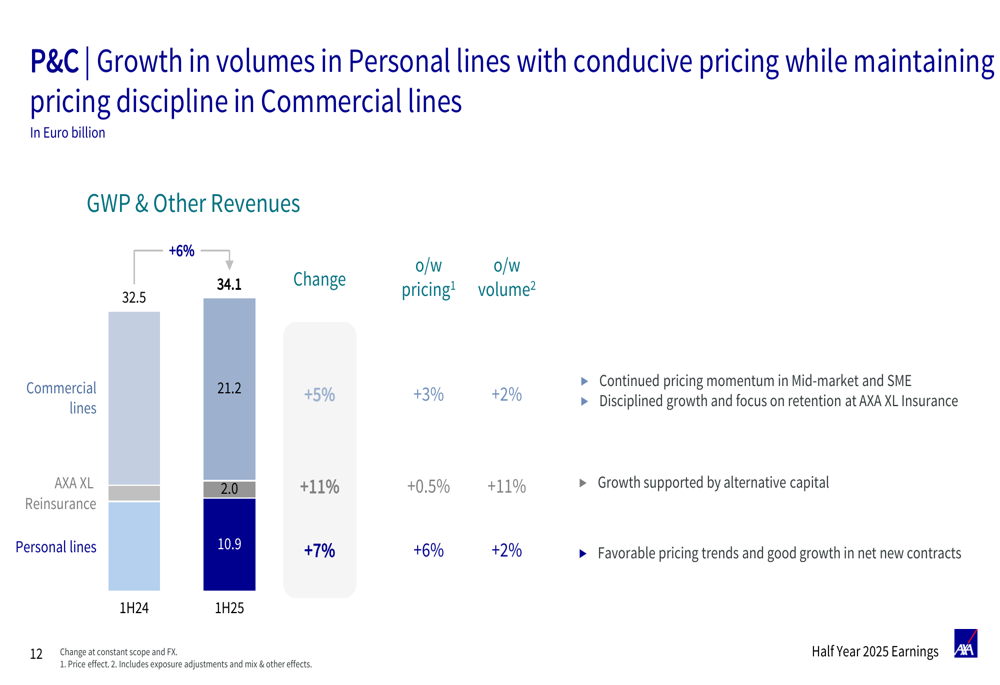

The Property & Casualty (P&C) segment demonstrated strong growth with Gross Written Premiums (GWP) increasing by 6% from €32.5 billion in 1H24 to €34.1 billion in 1H25. Commercial lines grew by 5%, AXA XL Reinsurance by 11%, and Personal Lines by 7%.

The breakdown of this growth is illustrated in the following chart:

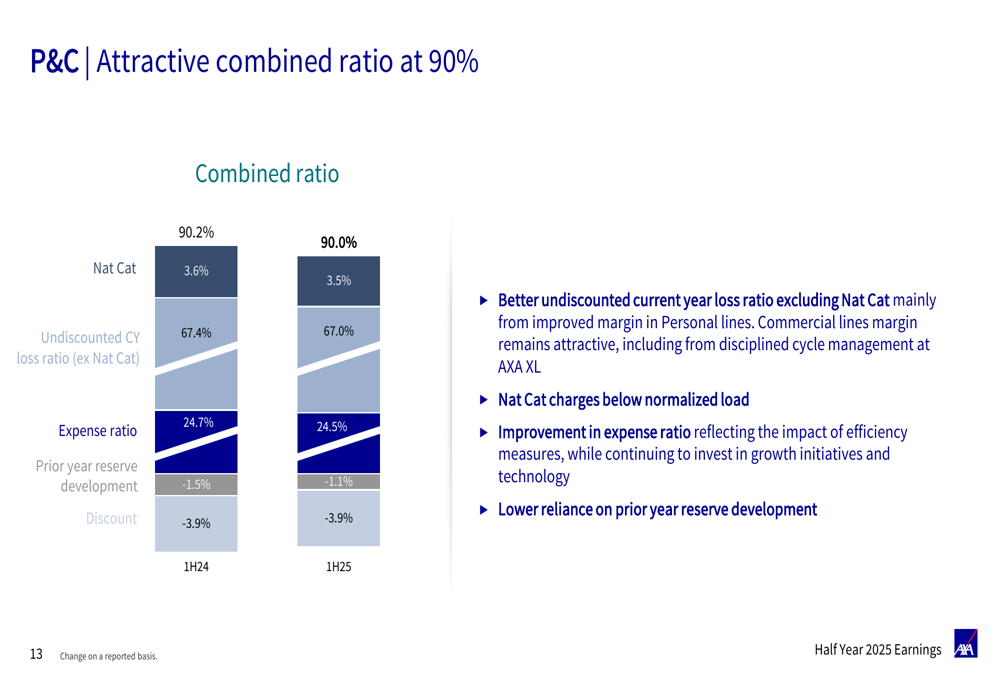

AXA maintained an attractive combined ratio of 90% in its P&C business, reflecting strong underwriting discipline and operational efficiency. The components of this ratio show slight improvements in the undiscounted current year loss ratio (excluding natural catastrophes) from 67.4% to 67.0% and in the expense ratio from 24.7% to 24.5%.

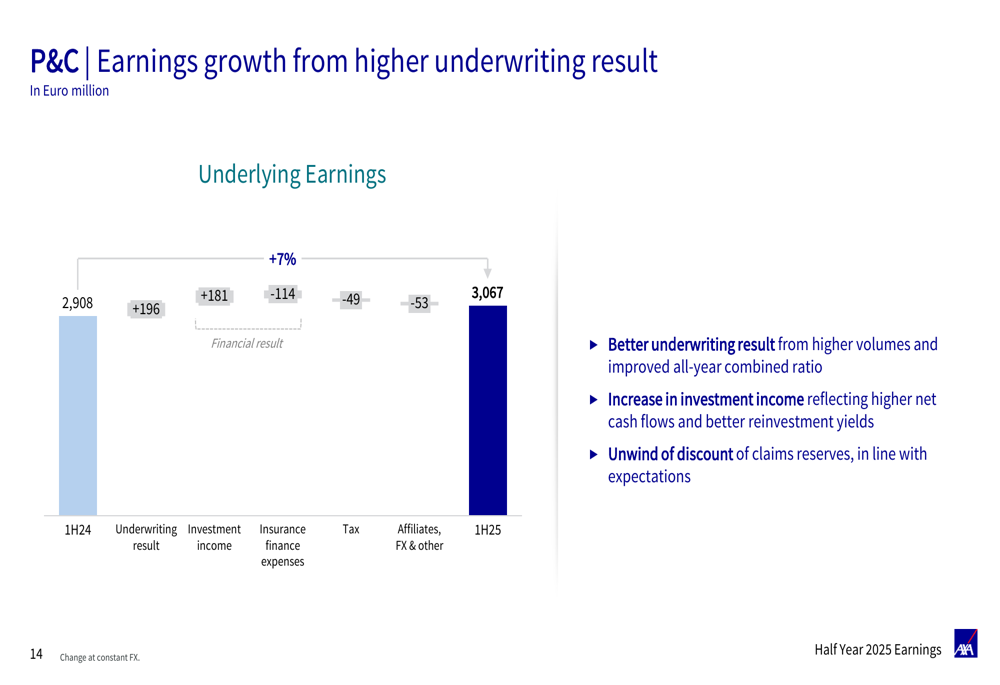

P&C underlying earnings increased by 7% from €2,908 million in 1H24 to €3,067 million in 1H25, primarily driven by improved underwriting results (+€181 million) and higher investment income (+€196 million), partially offset by increased insurance finance expenses, taxes, and other factors.

Life & Health Performance

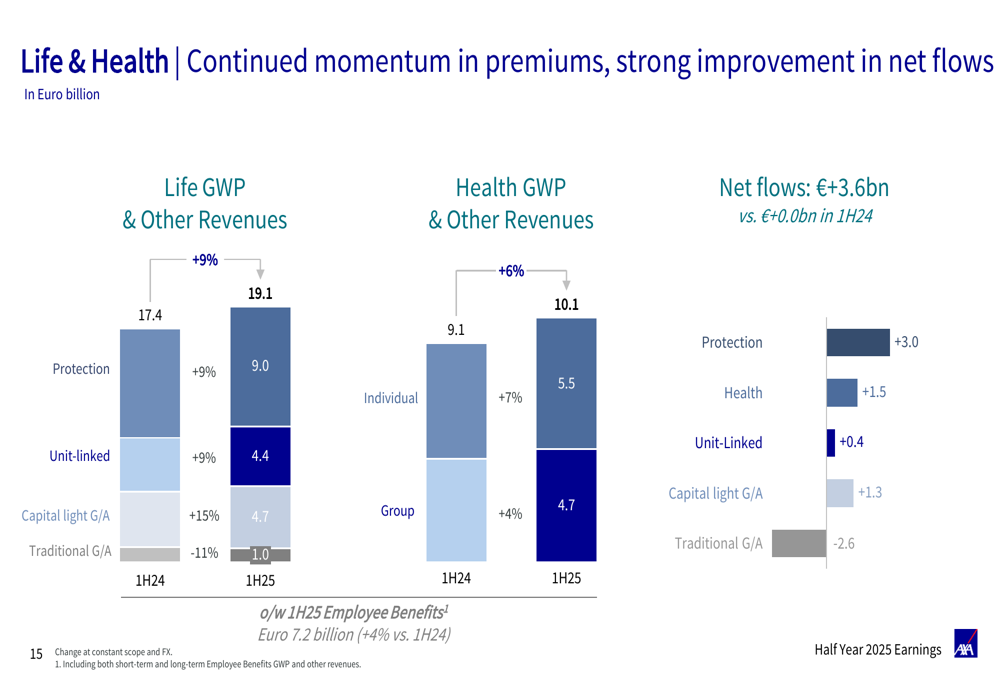

The Life & Health segment also showed strong momentum, with Life GWP increasing from €17.4 billion to €19.1 billion and Health GWP rising from €9.1 billion to €10.1 billion. Net flows improved significantly to €+3.6 billion compared to €0.0 billion in 1H24, with positive contributions from Protection, Health, Unit Linked, and Capital light General Account products, partially offset by outflows from Traditional General Account products.

The following chart illustrates this momentum in premiums and net flows:

Life & Health underlying earnings grew by 5% from €1,725 million in 1H24 to €1,814 million in 1H25, supported by higher technical results from improved short-term performance in Health, reflecting pricing and underwriting actions, as well as claims management initiatives. The Contractual Service Margin (CSM) release was up 2%, and financial results improved due to better reinvestment yields.

Strategic Initiatives

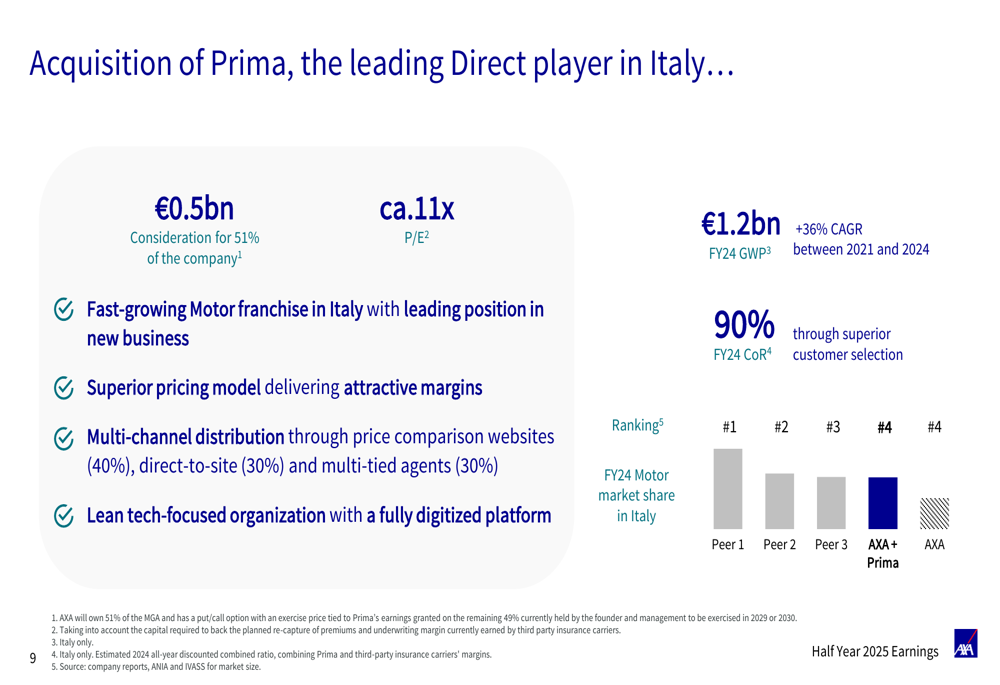

A key highlight of AXA’s presentation was the announcement of the acquisition of Prima, a leading direct player in the Italian insurance market. The deal involves a consideration of €0.5 billion for 51% of the company, with a price-to-earnings ratio of approximately 11x.

Prima is characterized as a fast-growing Motor franchise in Italy with a superior pricing model, multi-channel distribution, and a lean tech-focused organization. The company generated €1.2 billion in FY24 GWP with an impressive 36% CAGR between 2021 and 2024, and achieved a 90% FY24 combined ratio through superior customer selection.

The details of this strategic acquisition are presented in the following slide:

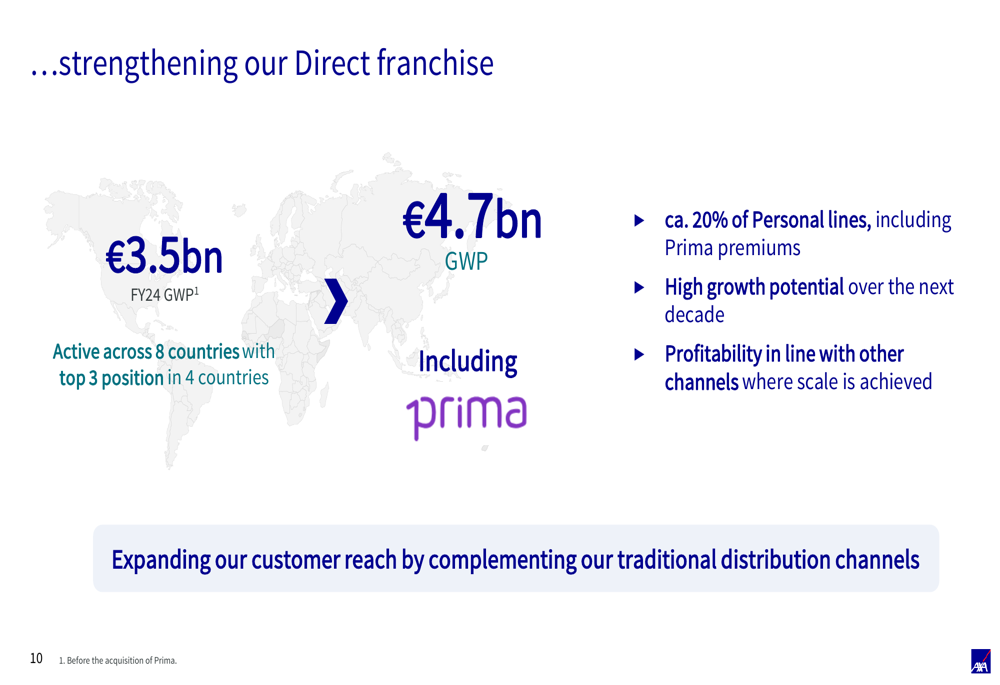

This acquisition significantly strengthens AXA’s Direct franchise, increasing its Direct GWP from €3.5 billion to €4.7 billion. AXA is now active in direct insurance across 8 countries, with a top 3 position in 4 of these markets.

The strategic importance of this acquisition is illustrated in the following chart:

Forward-Looking Statements

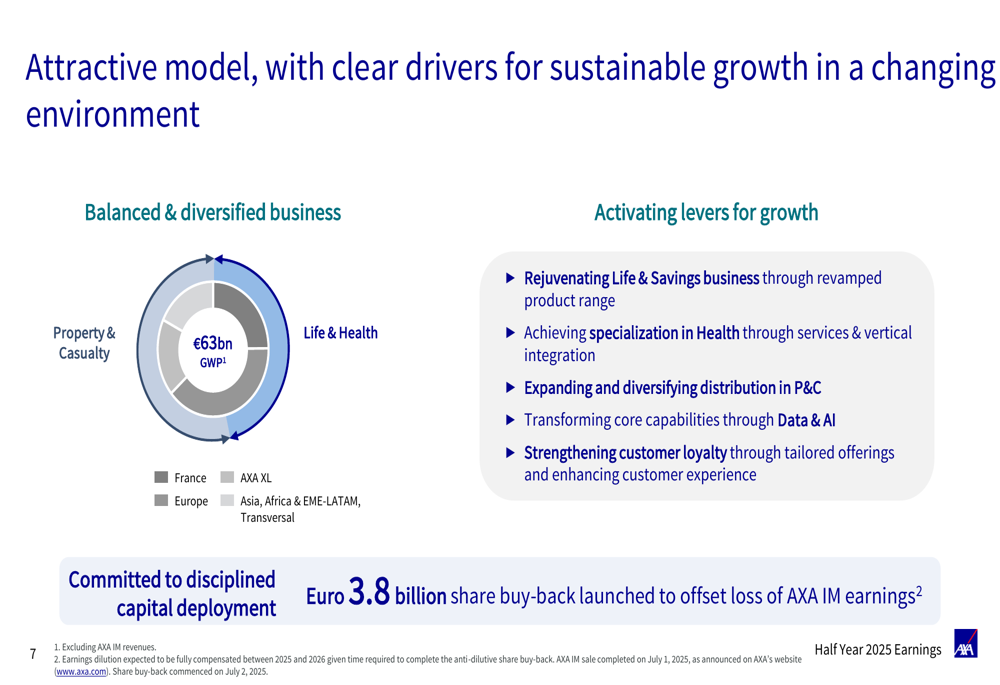

AXA’s management expressed confidence in the company’s outlook, stating they are on track to achieve the key targets of their "Unlock the Future" plan. The company highlighted its balanced and diversified business model as a key strength, with a focus on rejuvenating Life & Savings, specializing in Health, expanding distribution in P&C, transforming core capabilities through Data & AI, and strengthening customer loyalty.

The presentation also noted a disciplined capital deployment strategy, including a €3.8 billion share buyback program launched to offset the loss of AXA IM earnings.

In conclusion, AXA delivered a strong financial performance in the first half of 2025, with consistent growth across business segments and strategic expansion through the Prima acquisition. The company’s robust capital position, attractive returns, and clear strategic direction position it well for continued success in the competitive insurance landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.