Oil prices push higher amid worries over Russian supply disruptions

Introduction & Market Context

Axactor SE (OB:ACR) presented its Q1 2025 results on May 7, 2025, showcasing a significant rebound in collection performance and achieving an all-time high return on equity. The debt management company’s shares are currently trading near their 52-week high at 5.20 NOK, up 2.77% following the presentation, reflecting investor confidence in the company’s improving financial metrics and strategic direction.

Quarterly Performance Highlights

Axactor reported a strong start to 2025 with collection performance rebounding to 101% in Q1, up from 94% in Q4 2024. This improvement affirms the updated forecast based on current portfolio performance after several quarters of underperformance throughout 2024.

As shown in the following chart of quarterly collection performance:

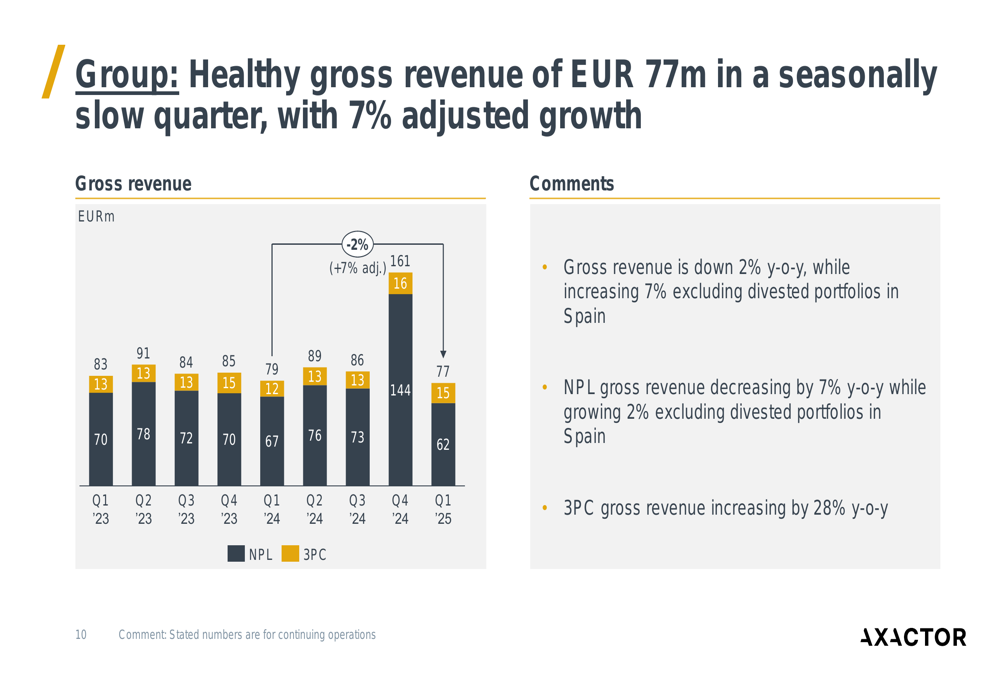

The company delivered healthy gross revenue of EUR 77 million in what is traditionally a seasonally slow quarter. While this represents a 2% year-over-year decline in absolute terms, when excluding divested portfolios in Spain, revenue actually increased by 7% compared to Q1 2024.

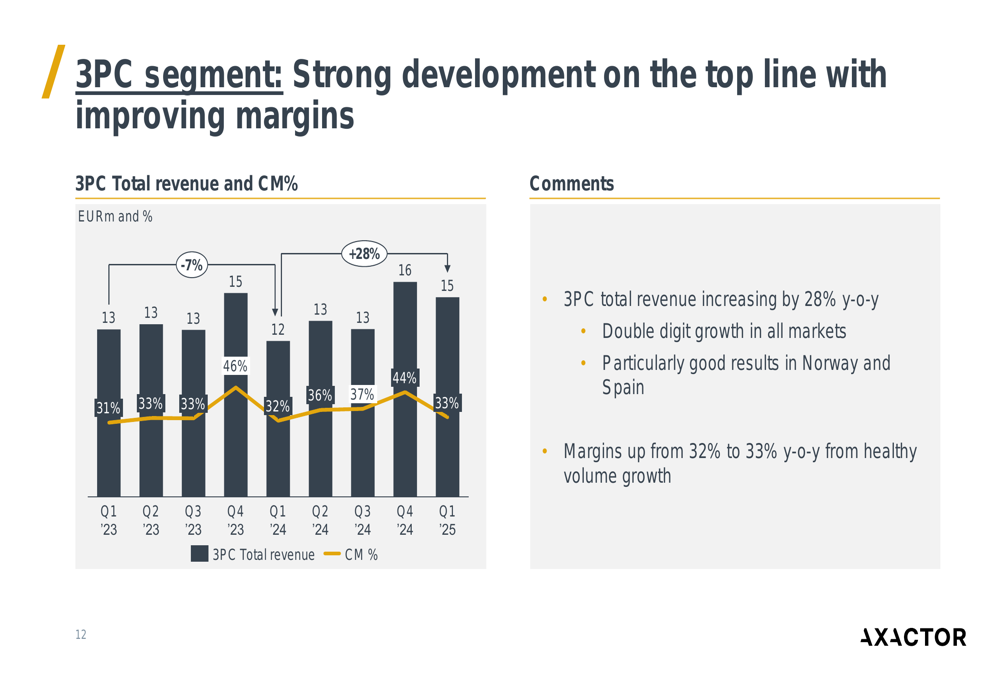

The revenue breakdown between NPL (Non-Performing Loans) and 3PC (Third Party Collection) segments illustrates this trend:

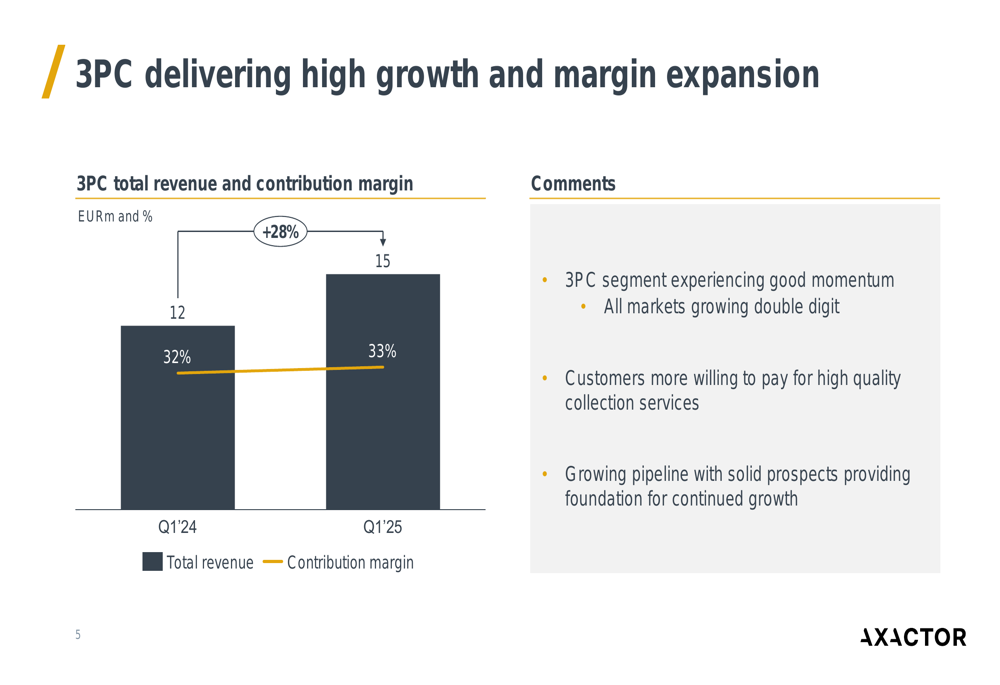

Particularly noteworthy is the performance of Axactor’s 3PC segment, which demonstrated robust growth with revenue increasing by 28% year-over-year while also expanding margins from 32% to 33%. The company noted that all markets in this segment are experiencing double-digit growth, with customers increasingly willing to pay for quality collection services.

Detailed Financial Analysis

Axactor’s EBITDA increased by 23% year-over-year, with a solid EBITDA margin of 50% driven by margin expansion and cost reductions. This improvement in profitability metrics is particularly significant given the seasonally slower first quarter.

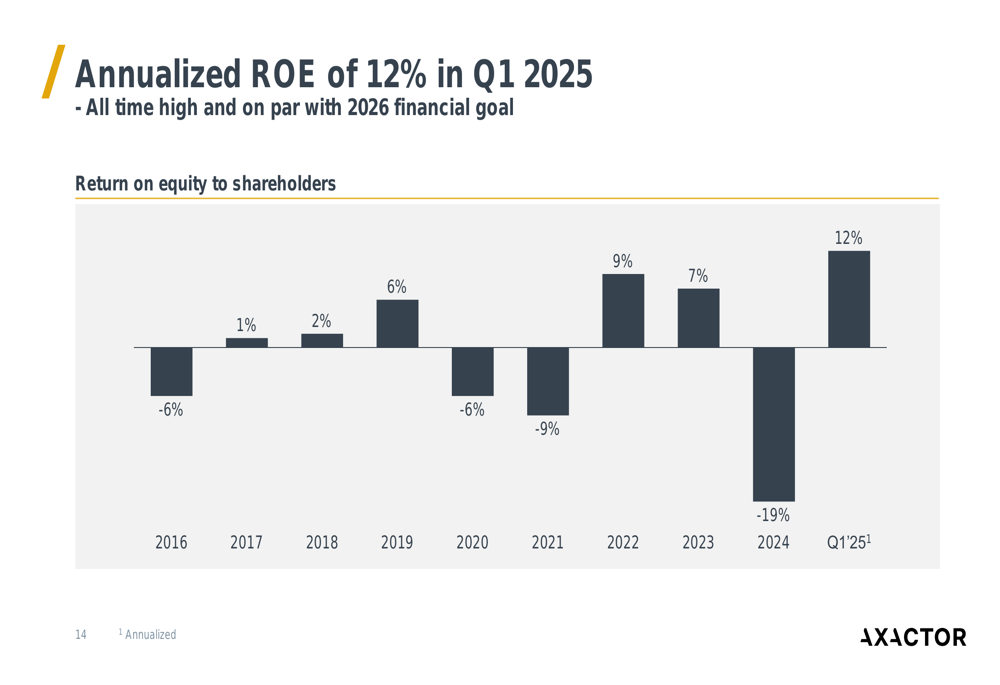

The company achieved an annualized return on equity to shareholders of 12% in Q1 2025, which represents an all-time high and is on par with the company’s 2026 financial goals. This marks a dramatic improvement from the negative 19% ROE reported in 2024.

The historical ROE trend demonstrates this significant turnaround:

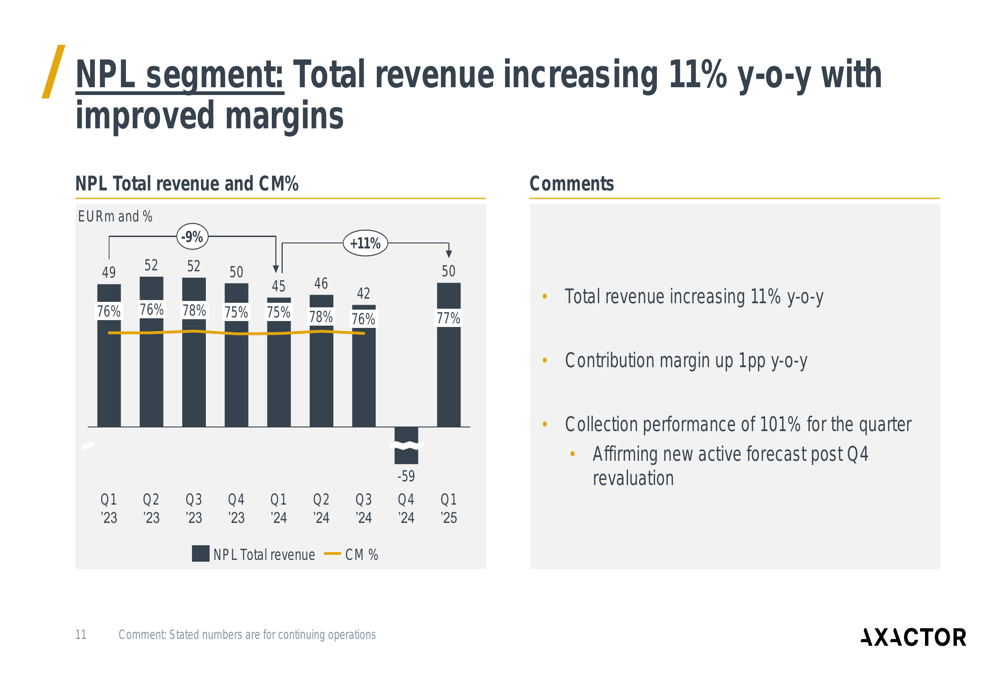

In the NPL segment, total revenue increased by 11% year-over-year with improved margins. Collection performance of 101% for the quarter affirms the new active forecast following the Q4 revaluation.

The 3PC segment continues to be a growth driver for Axactor, with the company reporting that customers are increasingly willing to pay for quality collection services, and there is a growing pipeline with solid prospects.

Strategic Initiatives

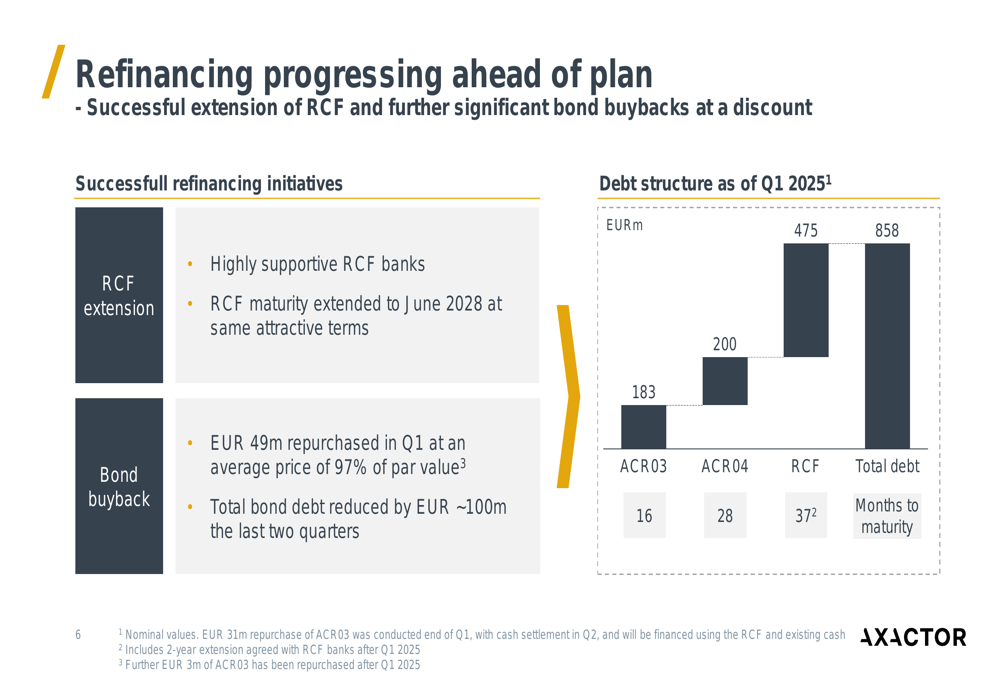

A key focus of Axactor’s strategy has been refinancing and debt reduction. The company reported successful extension of its Revolving Credit Facility (RCF) and significant bond buybacks at a discount. In Q1 2025, EUR 49 million of bonds were repurchased at an average price of 97% of par value, with total bond debt reduced by approximately EUR 100 million over the last two quarters.

The current debt structure and maturity profile is illustrated below:

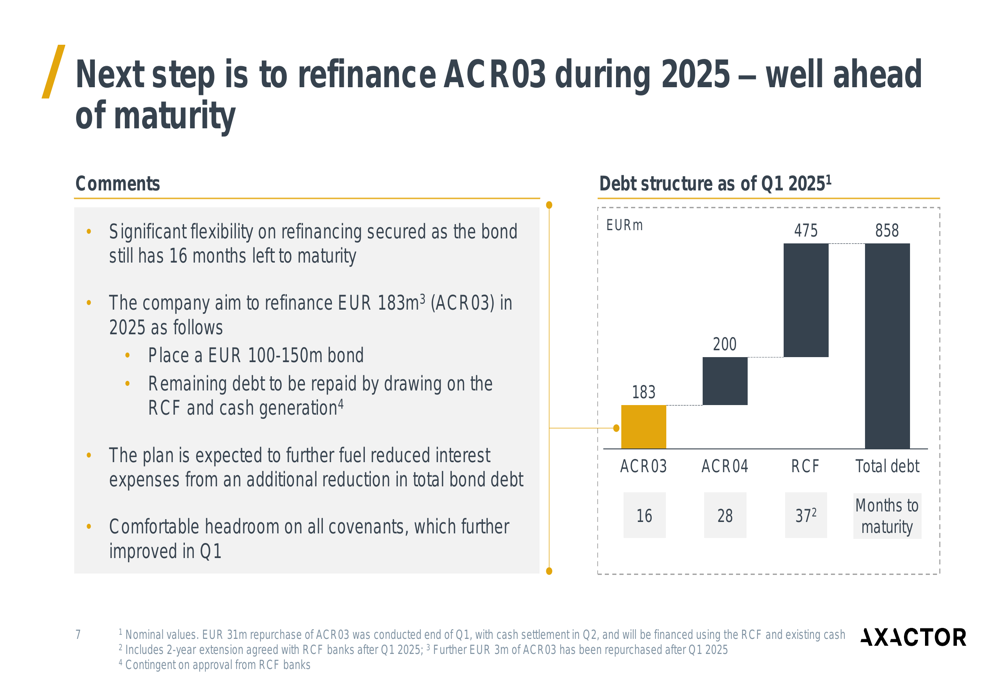

Axactor plans to refinance its ACR03 bond during 2025, well ahead of its maturity. The company aims to refinance the EUR 183 million bond by placing a new EUR 100-150 million bond, with the remaining debt to be repaid by drawing on the RCF and through cash generation.

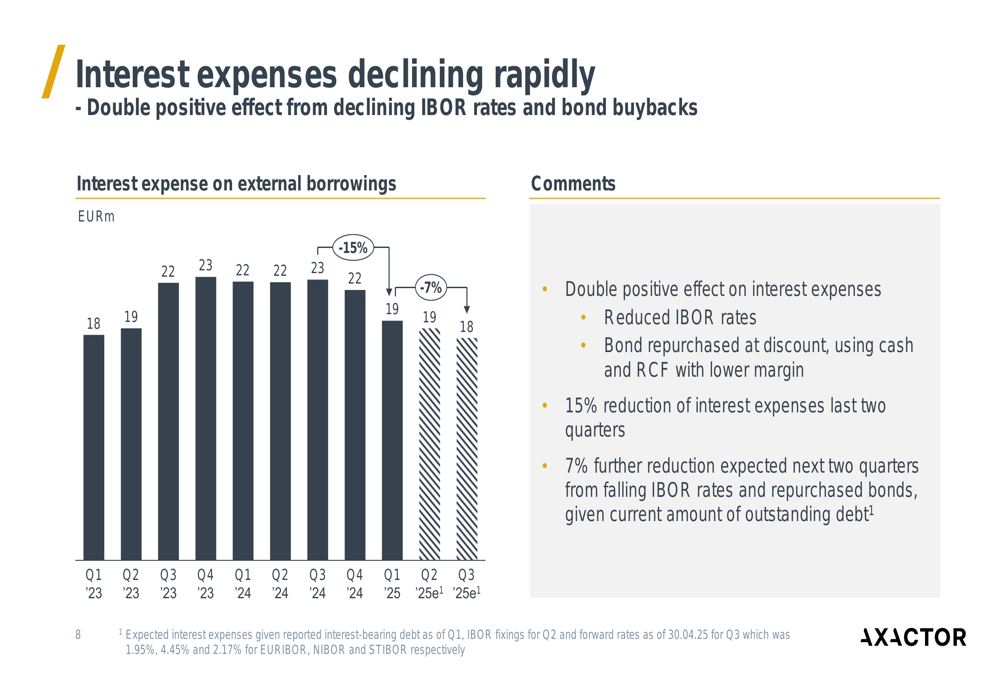

Interest expenses are declining due to falling IBOR rates and the bond buybacks, with a 15% reduction from Q3 2023 to Q1 2025. The company forecasts a further 7% reduction in the next two quarters.

Axactor’s covenant metrics have also improved significantly, with the leverage ratio decreasing to 2.6x in Q1 2025 from 4.0x in Q1 2024, well below the covenant requirement of ≤4.0x. Similarly, the interest coverage ratio improved to 3.8x in Q1 2025 from 3.2x in Q1 2024, above the covenant requirement of ≥3.0x.

Forward-Looking Statements

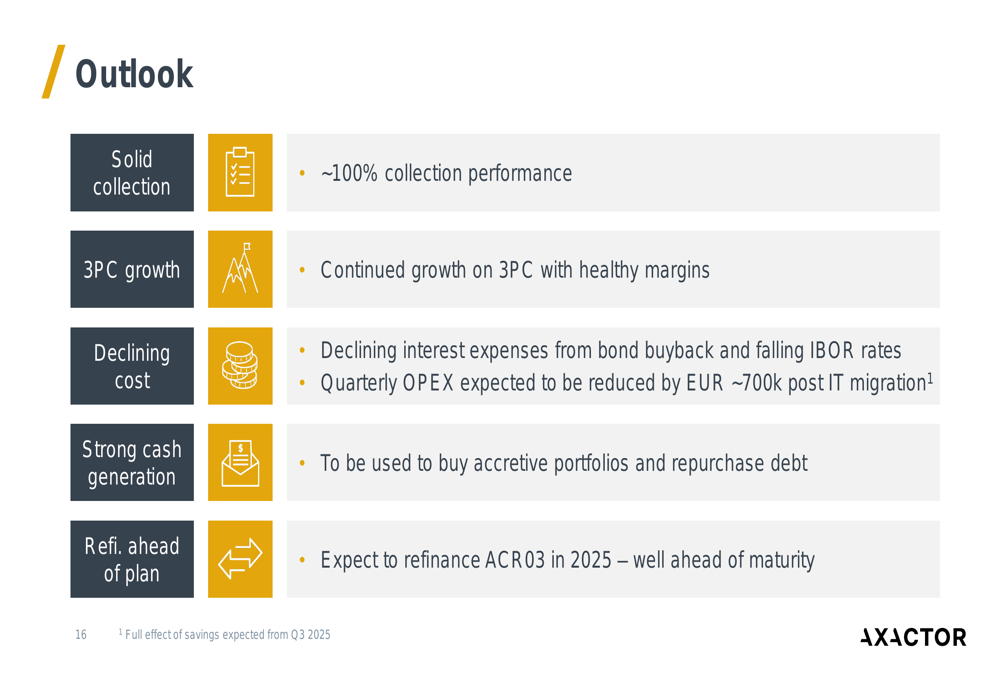

Looking ahead, Axactor provided an optimistic outlook based on its Q1 performance. The company expects collection performance to remain around 100%, continued growth in the 3PC segment with healthy margins, and further declining interest expenses from bond buybacks and falling IBOR rates.

The company also anticipates strong cash generation, which will be used to purchase accretive portfolios and repurchase debt. NPL investment commitments for the next 12 months are relatively modest at EUR 7 million, suggesting a selective approach to new investments.

Axactor expects to complete the refinancing of ACR03 in 2025, well ahead of its maturity, which should further optimize its capital structure and reduce financing costs. Additionally, the company anticipates quarterly operating expenses to be reduced by approximately EUR 700,000 following IT migration, contributing to improved profitability.

With collection performance back on track, growing 3PC revenues, declining interest expenses, and an improved capital structure, Axactor appears well-positioned to continue its positive trajectory through 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.