Street Calls of the Week

Introduction & Market Context

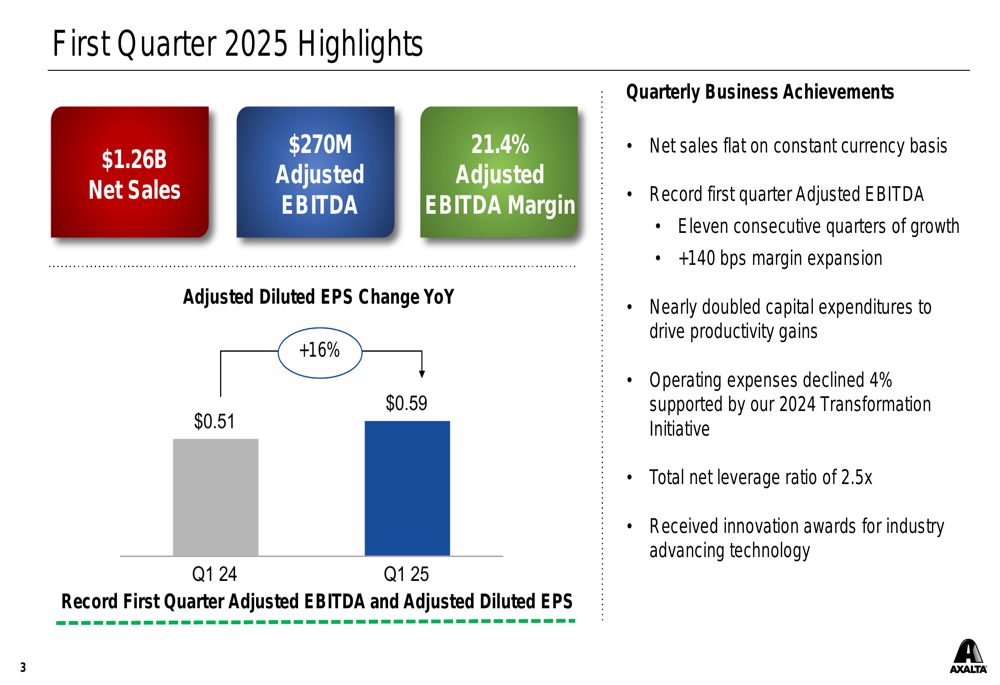

Axalta Coating Systems Ltd (NYSE:AXTA) released its first quarter 2025 financial results on May 7, showcasing the company’s ability to deliver margin expansion and earnings growth despite challenging macroeconomic conditions. The coatings manufacturer reported record first quarter Adjusted EBITDA of $270 million, marking its eleventh consecutive quarter of growth, even as net sales declined 3% year-over-year to $1.26 billion.

The company’s performance reflects its operational efficiency initiatives and strategic positioning in key markets, allowing it to outperform industry trends across several segments despite a soft global manufacturing environment, declining collision claims, and projected decreases in automotive production.

Quarterly Performance Highlights

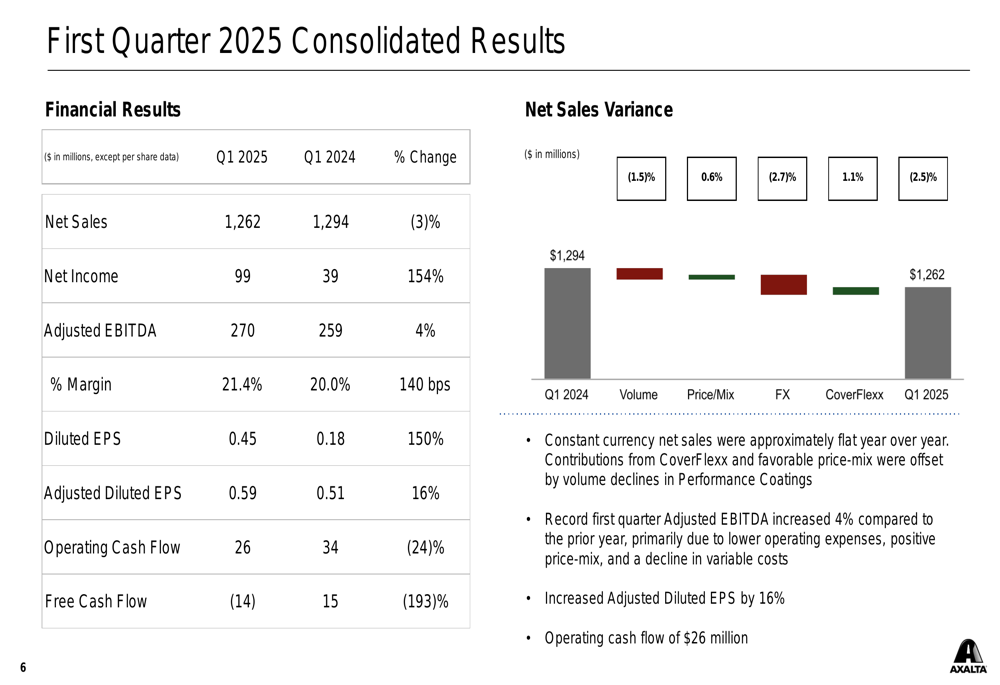

Axalta’s first quarter results demonstrated significant improvement in profitability metrics despite revenue challenges. Net income surged 154% to $99 million compared to $39 million in Q1 2024, while Adjusted EBITDA increased 4% to $270 million, with margins expanding 140 basis points to 21.4%.

As shown in the following financial highlights chart:

Adjusted diluted EPS grew 16% year-over-year to $0.59, up from $0.51 in the prior year period. This earnings growth came despite a 3% decline in reported net sales, as constant currency net sales remained approximately flat year-over-year. The company’s operating expenses declined 4%, supported by its 2024 Transformation Initiative, while capital expenditures nearly doubled to drive productivity gains.

The detailed consolidated results further illustrate Axalta’s financial performance:

Operating cash flow was $26 million, down 24% from the prior year, while free cash flow declined to negative $14 million from positive $15 million in Q1 2024, primarily due to increased capital expenditures. The company maintained its total net leverage ratio at 2.5x.

Segment Analysis

Axalta’s business is divided into two main segments: Performance Coatings and Mobility Coatings, each showing different trends in the first quarter.

The Performance Coatings segment, which includes Refinish and Industrial businesses, reported net sales of $822 million, down 3% year-over-year. However, Adjusted EBITDA increased 1% to $197 million, with margins expanding 100 basis points to 24.1%. Refinish constant currency net sales grew 1% year-over-year, benefiting from approximately 900 net new body shops and growth in accessories and adjacencies, while Industrial net sales declined 6%.

The segment’s performance is detailed in the following chart:

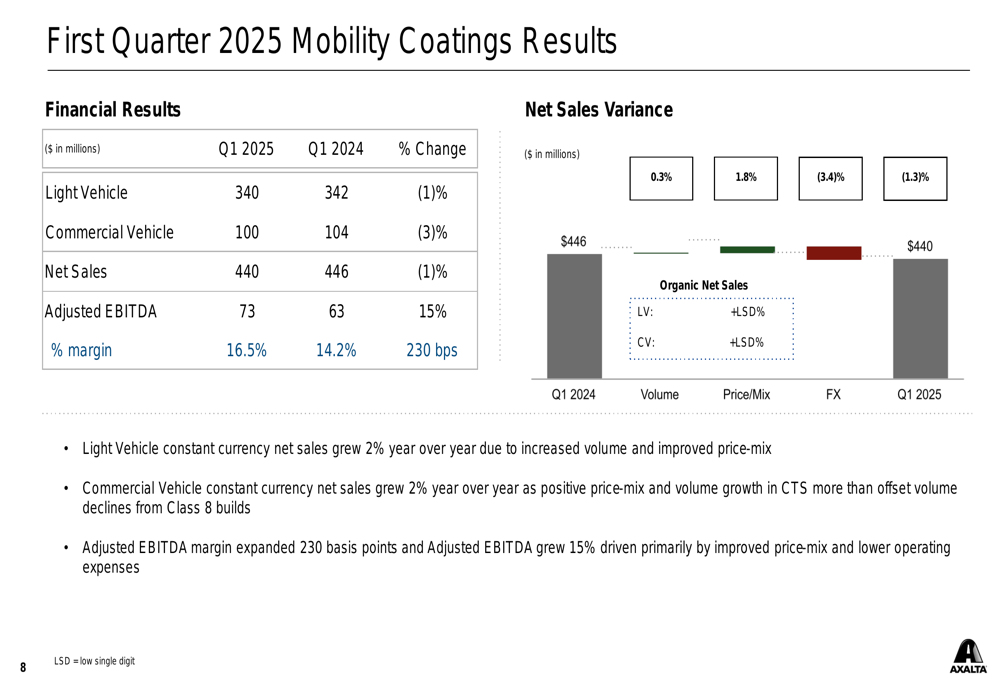

The Mobility Coatings segment, comprising Light Vehicle and Commercial Vehicle businesses, delivered stronger margin improvement despite modest revenue decline. Net sales decreased 1% to $440 million, but Adjusted EBITDA surged 15% to $73 million, with margins expanding 230 basis points to 16.5%. Both Light Vehicle and Commercial Vehicle constant currency net sales grew 2% year-over-year, outperforming their respective markets.

As illustrated in the segment results:

Market Challenges and Mitigation Strategies

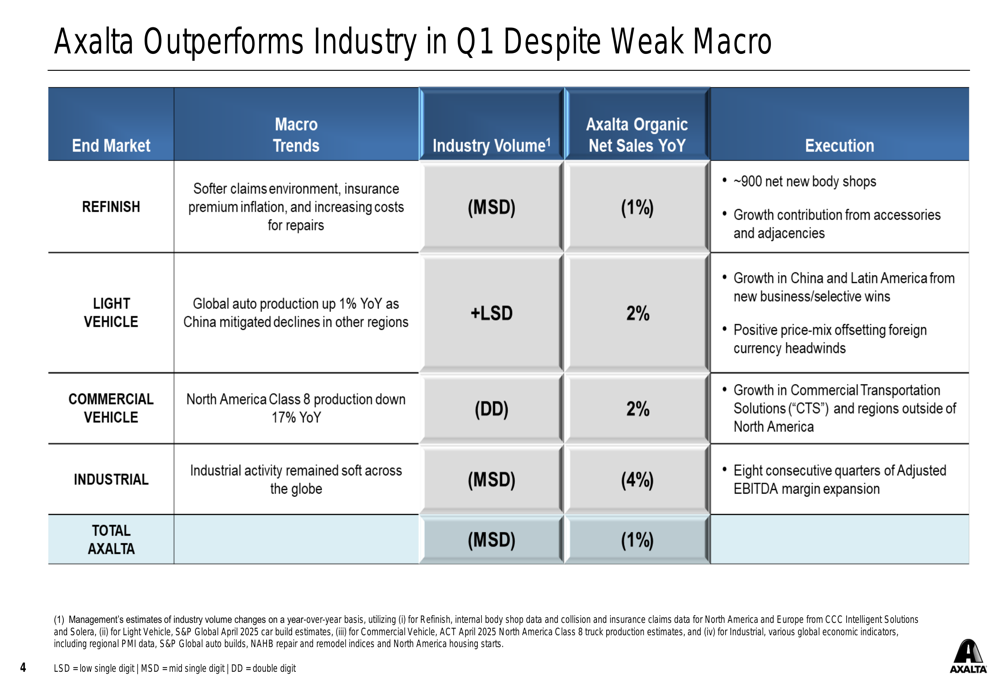

Axalta is navigating several market challenges, including a soft global macro environment and increased tariffs. The company highlighted its ability to outperform industry trends across its end markets despite these headwinds.

The following table illustrates Axalta’s performance relative to industry trends:

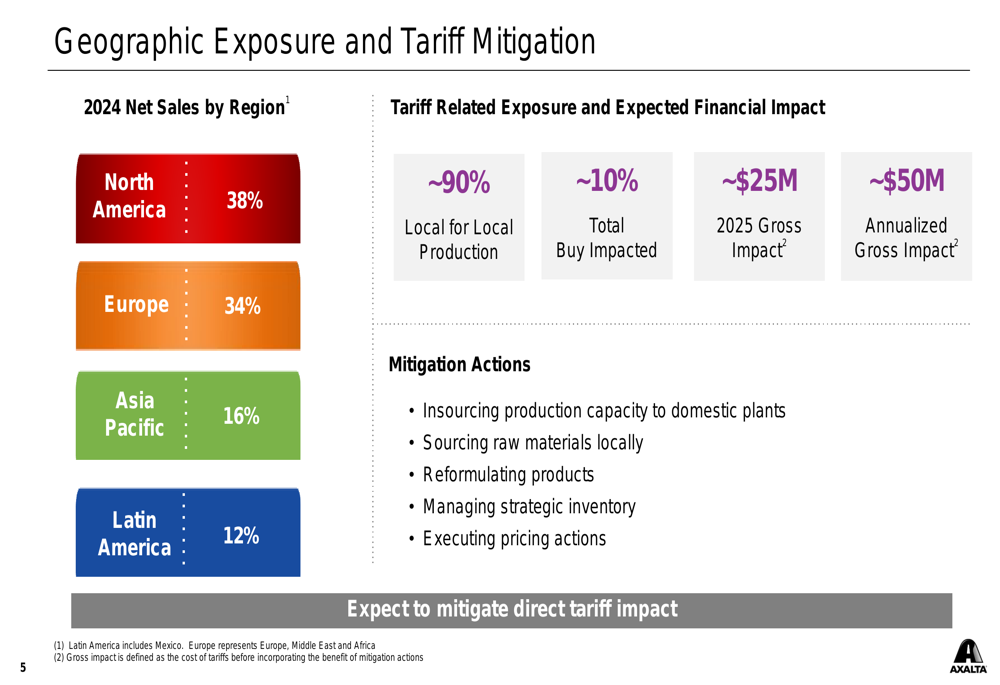

To address tariff-related challenges, Axalta emphasized its geographic diversification and mitigation strategies. With approximately 90% of its production being local-for-local, the company has limited direct exposure to tariffs. Nevertheless, it faces an estimated $25 million gross impact in 2025 and $50 million annualized gross impact from tariffs.

The company’s geographic exposure and tariff mitigation strategies are outlined below:

Looking ahead, Axalta expects the global macro environment to remain challenging, with collision claims projected to decline at mid-single-digit rates in both the US and Europe, US Manufacturing PMI hovering around the neutral 50 mark, global auto builds forecasted to decline from 89.5 million units in 2024 to 87.9 million in 2025, and North American Class 8 truck builds expected to drop from 332,000 units to 255,000 units.

Forward Guidance

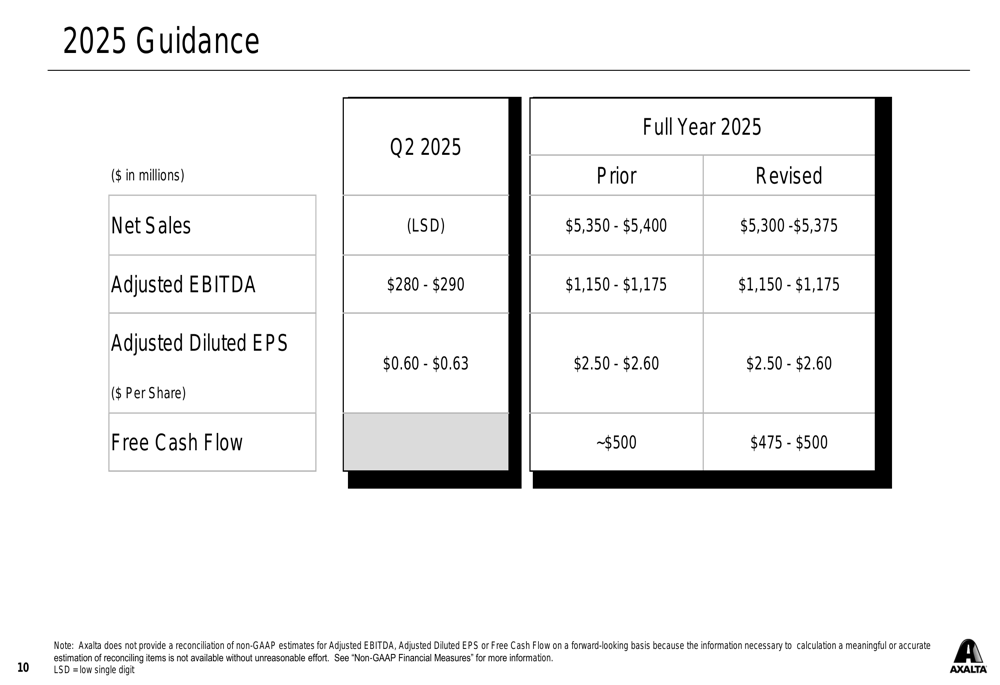

Despite the challenging environment, Axalta maintained its Adjusted EBITDA guidance for the full year 2025 while slightly lowering expectations for net sales and free cash flow. For Q2 2025, the company projects a low-single-digit decline in net sales, Adjusted EBITDA of $280-$290 million, and Adjusted Diluted EPS of $0.60-$0.63.

The detailed guidance is presented in the following table:

For the full year 2025, Axalta revised its net sales guidance to $5,300-$5,375 million from the prior range of $5,350-$5,400 million, while maintaining its Adjusted EBITDA projection of $1,150-$1,175 million and Adjusted Diluted EPS forecast of $2.50-$2.60. Free cash flow guidance was adjusted to $475-$500 million from the previous estimate of approximately $500 million.

Strategic Initiatives

Axalta reported significant progress toward its "A Plan" targets, which focus on safety, cultural transformation, operational efficiency, and growth initiatives. Key achievements include reducing safety incidents by 50% year-over-year in Q1, reducing operating expenses by 4%, executing supply chain network optimization, and growing adjacencies in the Refinish business.

The company’s progress on strategic initiatives is summarized in the following chart:

Additional strategic highlights include commercializing a $70 million Mobility business win in Brazil, expanding margins in the Industrial segment, receiving technology innovation awards, and commencing customer demo trials of Axalta NextJet™. These initiatives support the company’s focus on operational excellence and profitable growth despite market challenges.

Executive Summary

Axalta’s Q1 2025 results demonstrate the company’s resilience and operational efficiency in a challenging macroeconomic environment. While net sales declined 3% year-over-year, the company achieved record first quarter Adjusted EBITDA, significant margin expansion across segments, and 16% growth in Adjusted Diluted EPS.

The company’s ability to outperform industry trends in key segments, combined with its strategic focus on cost management, productivity improvements, and targeted growth initiatives, positions it well to navigate ongoing market challenges. While slightly revising its full-year net sales and free cash flow guidance, Axalta maintained its Adjusted EBITDA and EPS projections, reflecting confidence in its operational strategies and margin improvement initiatives.

As global manufacturing activity remains soft and automotive production forecasts trend downward, Axalta’s emphasis on local-for-local production, tariff mitigation strategies, and continued execution of its transformation initiatives will be critical to sustaining its performance trajectory through 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.