Functional Brands closes $8 million private placement and completes Nasdaq listing

Introduction & Market Context

Axcelis Technologies Inc (NASDAQ:ACLS) reported third-quarter 2025 results on November 4, delivering stronger-than-expected performance despite the ongoing cyclical downturn in the semiconductor equipment market. The company’s shares responded positively, surging 7.58% in pre-market trading to $89.01, reflecting investor confidence in Axcelis’ ability to navigate current market challenges.

The semiconductor equipment manufacturer posted revenue of $213.6 million, exceeding analyst expectations of $200.06 million, while non-GAAP earnings per share reached $1.21, significantly above the forecast of $1.00. These results demonstrate Axcelis’ resilience amid what the company describes as a "cyclical digestion period" across its markets.

Quarterly Performance Highlights

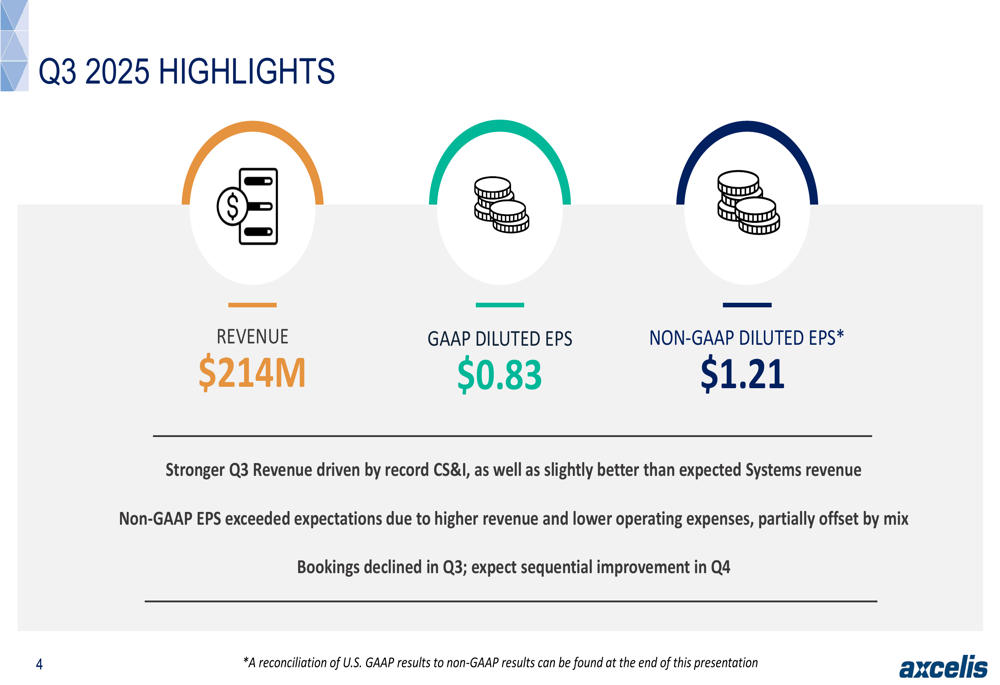

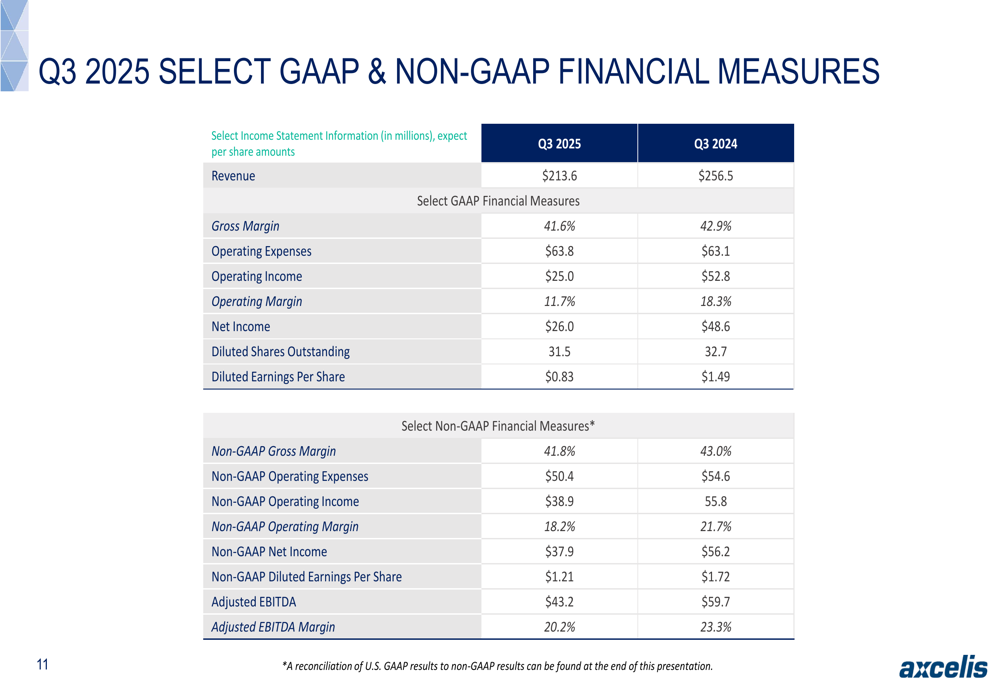

Axcelis reported Q3 2025 revenue of $213.6 million, representing a 9.8% increase from the previous quarter’s $194.5 million, though still below the $256.6 million recorded in the same period last year. The company attributed the sequential improvement to record performance in its Customer Solutions and Innovation (CS&I) segment and better-than-expected systems revenue.

As shown in the following financial summary from the presentation:

The company’s non-GAAP diluted earnings per share of $1.21 exceeded expectations due to higher revenue and lower operating expenses, though this was partially offset by product mix. GAAP diluted EPS came in at $0.83, compared to $1.49 in Q3 2024.

A more detailed breakdown of the company’s financial performance reveals the strength of its business model despite market headwinds:

The company maintained strong cash generation with $45.3 million in cash from operations and free cash flow of $43.3 million. Axcelis ended the quarter with $592.8 million in cash and marketable securities, an increase from $581.0 million in the previous quarter, demonstrating continued financial strength.

Segment Performance

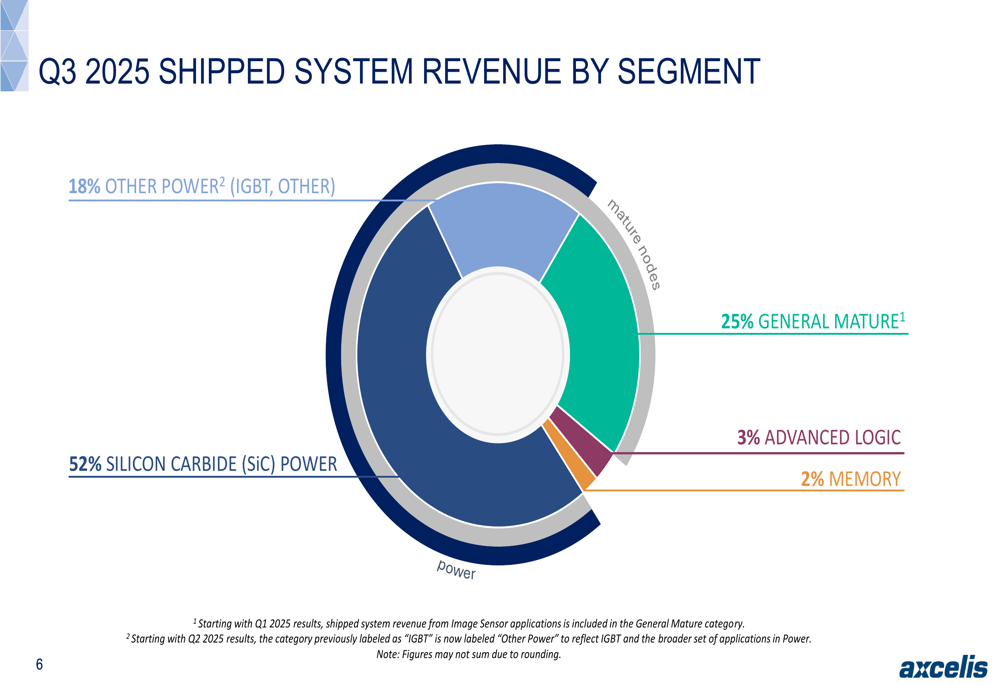

Silicon Carbide power applications dominated Axcelis’ shipped system revenue in Q3, accounting for 52% of the total. This reflects the company’s strong positioning in the growing market for silicon carbide semiconductor devices, which are increasingly used in electric vehicles and other power applications.

The following chart illustrates the company’s revenue distribution by segment:

Mature process technology applications, including both power and general mature segments, accounted for 95% of shipped system revenue in Q3 2025. The company noted sequential growth in Silicon Carbide shipments, with multiple customers building capacity in China. Meanwhile, advanced logic and memory segments represented just 3% and 2% of shipped system revenue, respectively.

Geographically, China remained Axcelis’ largest market at 46% of total revenue, though this represents a decrease from 55% in the previous quarter. The United States accounted for 14%, while South Korea and Europe contributed 10% and 11%, respectively.

Strategic Initiatives

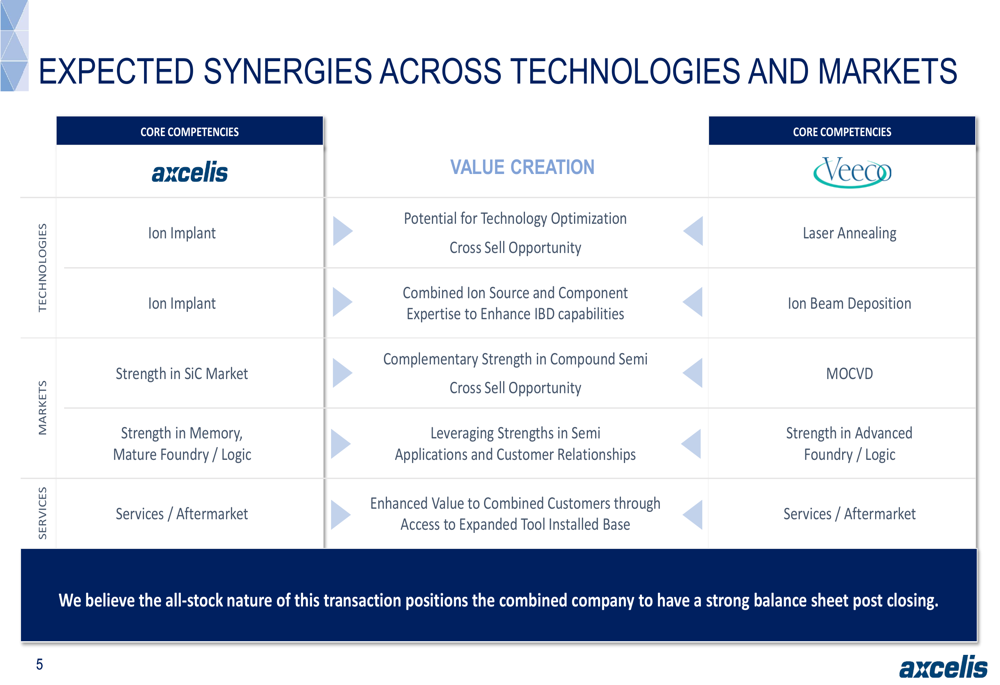

A significant development highlighted in the presentation is Axcelis’ planned merger with Veeco, which aims to create synergies across technologies and markets. The all-stock transaction is expected to position the combined company with a strong balance sheet post-closing.

As illustrated in the following slide, the merger would combine Axcelis’ core competencies in ion implant with Veeco’s expertise in laser annealing, ion beam deposition, and MOCVD:

Despite the challenging market environment, Axcelis emphasized its commitment to product development and customer engagement initiatives. The company highlighted interest in new applications for high-energy products while executing on its strategy in high current. A joint development program with GE Aerospace utilizing the Purion XEmax was also mentioned as a strategic initiative.

Forward-Looking Statements

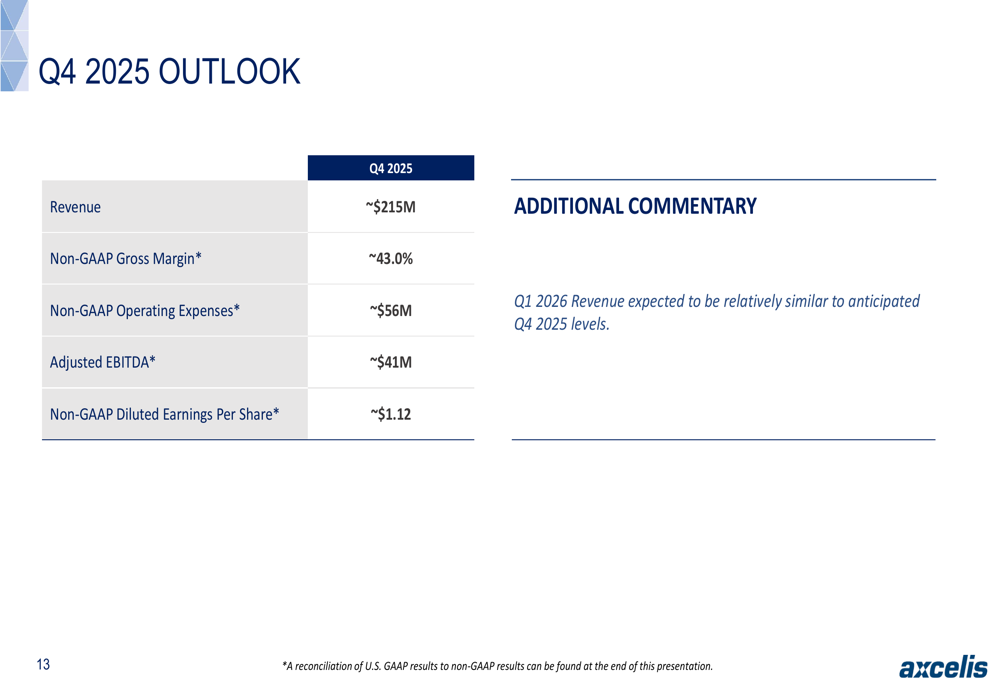

Looking ahead, Axcelis provided guidance for the fourth quarter of 2025, projecting revenue of approximately $215 million and non-GAAP diluted earnings per share of around $1.12. The company also indicated that Q1 2026 revenue is expected to remain relatively similar to Q4 2025 levels.

The outlook details are presented in the following slide:

In the memory segment, Axcelis anticipates sequential improvement in Q4 as customers add capacity for AI-related applications. The company also provided an early positive outlook for 2026, suggesting growth driven by increased investments in DRAM and HBM (High Bandwidth Memory).

"We are navigating the current cyclical digestion period across our markets exceptionally well," said Russell Lowe, President and CEO, according to the earnings call transcript. He emphasized the anticipated growth in the memory market next year, led by increased DRAM and HBM investments, and noted signs of improvement in utilization rates.

Conclusion

Axcelis’ Q3 2025 results demonstrate the company’s ability to outperform expectations despite challenging market conditions in the semiconductor equipment industry. The strong performance in Silicon Carbide applications and record CS&I revenue highlight Axcelis’ strategic positioning in growing market segments.

While systems bookings declined in Q3, the company expects sequential improvement in Q4, and its planned merger with Veeco could create additional growth opportunities. With a strong cash position and consistent free cash flow generation, Axcelis appears well-positioned to navigate the current cyclical downturn and capitalize on anticipated market improvements in 2026.

Investors responded positively to the results, with the stock trading near $89 in pre-market activity, though still below its 52-week high of $102.93, suggesting potential upside if the company continues to execute on its strategic initiatives and market conditions improve as expected.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.