How are energy investors positioned?

Introduction & Market Context

Axos Financial Inc. (NYSE:AX) released its third-quarter fiscal 2025 earnings presentation on April 30, 2025, showcasing improved credit quality metrics and continued loan growth across specialized lending categories. The digital financial services provider closed the trading day at $63.94, down 0.72%, with shares trading at $63.48 in after-hours.

The company’s presentation comes amid a challenging environment for financial institutions, with Axos positioning itself to navigate interest rate uncertainties through a diversified deposit base and loan portfolio with significant variable-rate exposure.

Quarterly Performance Highlights

Axos reported net income of $105.2 million for the quarter ended March 31, 2025, with basic earnings per share of $1.84. This represents a slight improvement from the $1.82 EPS reported in the previous quarter.

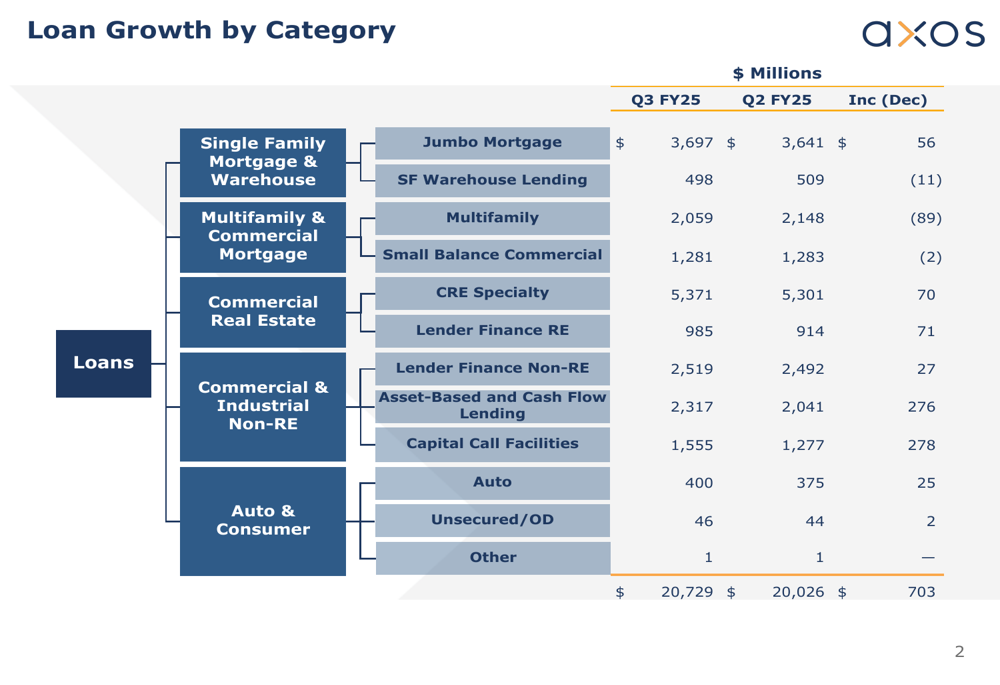

Total (EPA:TTEF) loans reached $20.73 billion, increasing by $703 million from the previous quarter, driven primarily by growth in commercial lending categories. The company maintained a strong capital position while improving its credit quality metrics.

Loan Portfolio Growth and Composition

The company’s loan portfolio showed significant growth in specialized commercial lending segments. Capital Call Facilities increased by $278 million and Asset-Based and Cash Flow Lending grew by $276 million quarter-over-quarter, highlighting Axos’s focus on these higher-yield categories.

As shown in the following breakdown of loan growth by category:

The loan portfolio demonstrates Axos’s strategic emphasis on commercial lending, with Commercial & Industrial Non-RE loans and Commercial Real Estate loans comprising the largest segments at $6.39 billion and $6.36 billion respectively.

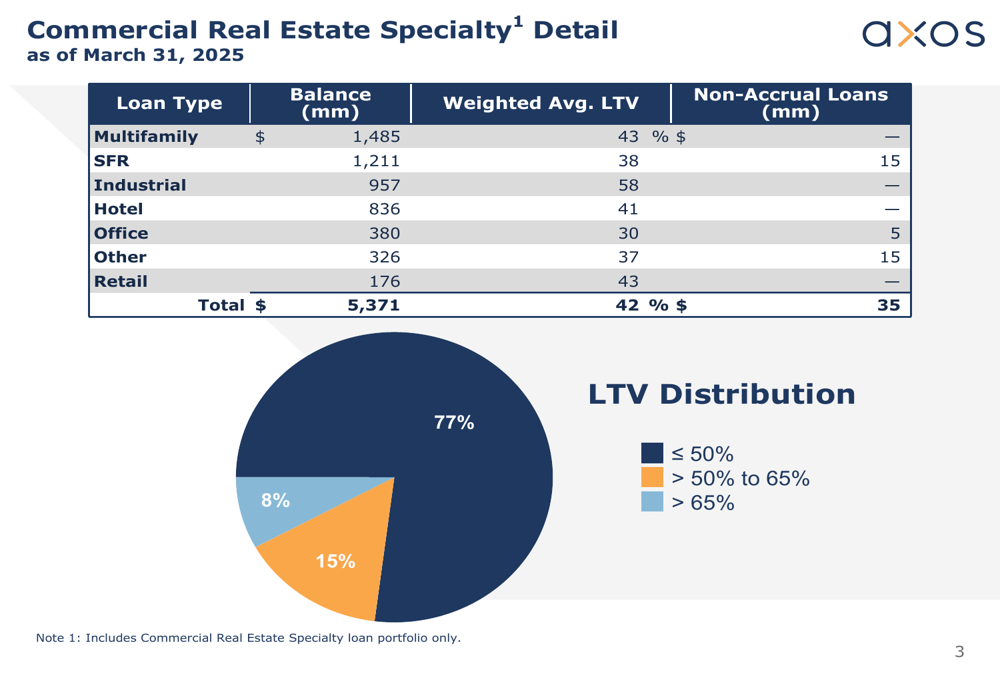

The company’s Commercial Real Estate portfolio maintains conservative loan-to-value ratios, with a weighted average LTV of 42% and 77% of the portfolio having an LTV of 50% or less. This conservative approach provides significant protection against potential market downturns.

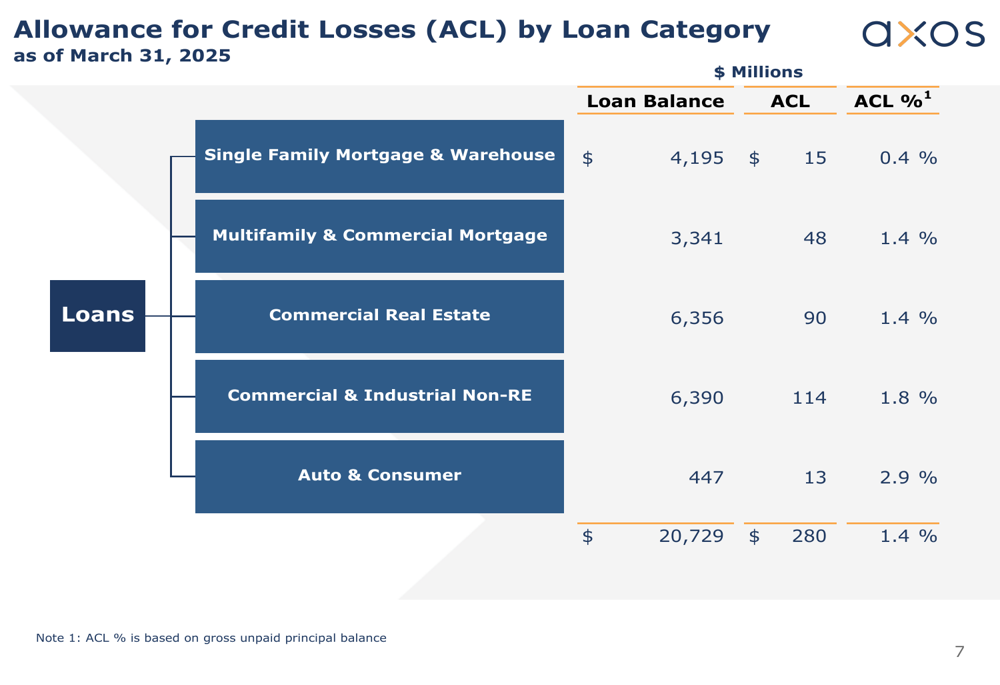

Credit Quality Improvements

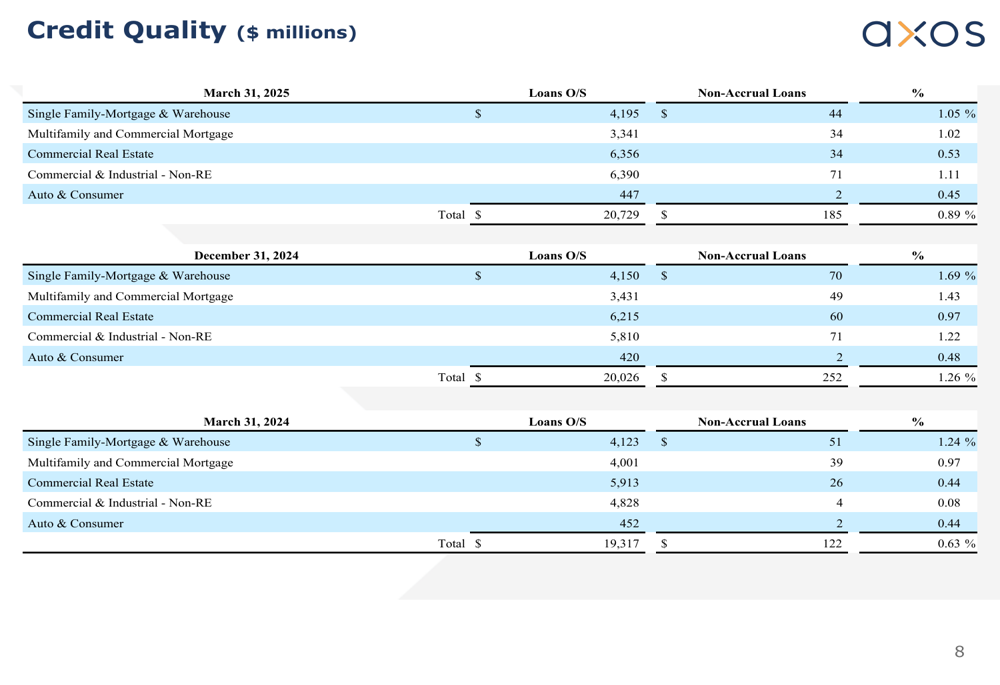

A notable highlight from the presentation is the significant improvement in credit quality metrics. Non-accrual loans decreased to $185 million (0.89% of total loans) as of March 31, 2025, down from $252 million (1.26%) in December 2024 and up from $122 million (0.63%) in March 2024.

The following chart illustrates the credit quality metrics across different loan categories:

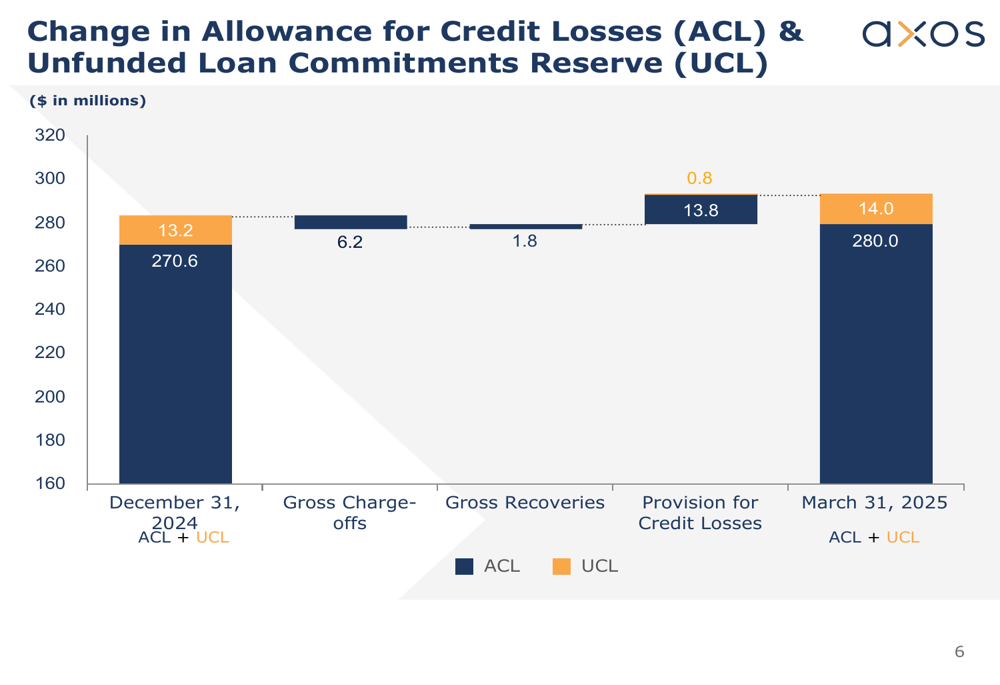

The company maintained an Allowance for Credit Losses (ACL) of $280 million, representing 1.4% of the total loan portfolio. The provision for credit losses was $14.6 million for the quarter, reflecting the company’s prudent approach to potential credit risks.

The ACL varies by loan category, with higher reserves allocated to riskier segments such as Commercial & Industrial Non-RE (1.8%) and Auto & Consumer (2.9%), while maintaining lower reserves for well-secured categories like Single Family Mortgage (0.4%).

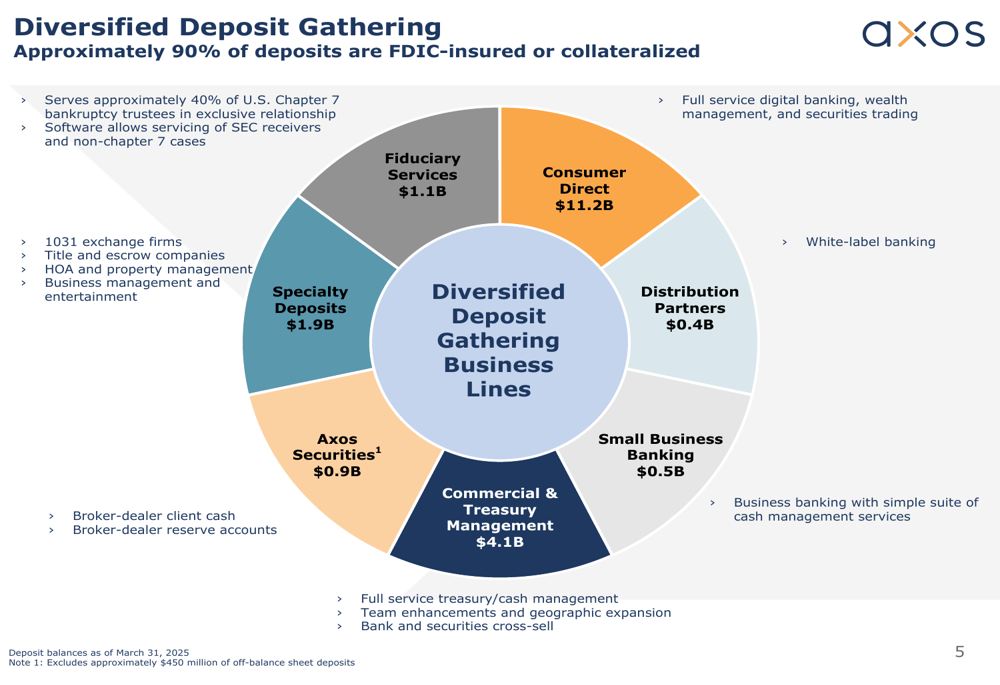

Deposit Strategy and Interest Rate Positioning

Axos continues to emphasize its diversified deposit gathering strategy, with approximately 90% of its $20.14 billion deposit base being either FDIC-insured or collateralized. The company’s deposit sources span multiple channels, with Consumer Direct representing the largest segment at $11.2 billion.

The deposit diversification strategy is illustrated in the following diagram:

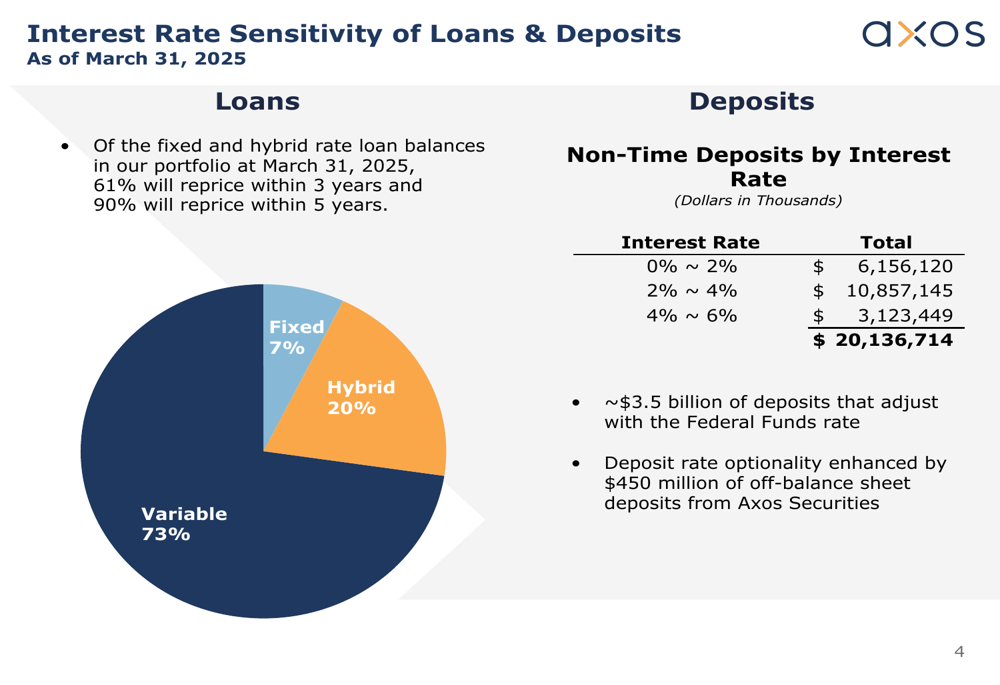

The company’s interest rate sensitivity positioning appears favorable in the current environment, with 73% of loans at variable rates and another 20% in hybrid structures. Of the fixed and hybrid rate loans, 61% will reprice within three years and 90% within five years, providing flexibility as interest rates evolve.

Forward Outlook

While the presentation doesn’t provide explicit forward guidance, Axos’s strategic positioning suggests continued focus on specialized lending categories and maintaining strong credit quality. The company’s conservative loan-to-value ratios in commercial real estate and diversified deposit base appear designed to weather potential economic uncertainties.

The improvement in non-accrual loans and continued loan growth indicate positive momentum, though the stock’s performance suggests investors may be taking a cautious approach. At $63.48 in after-hours trading, Axos shares remain well below their 52-week high of $88.46, potentially reflecting broader market concerns about the financial sector despite the company’s improving fundamentals.

Axos’s emphasis on variable-rate loans and diversified deposit sources positions it to potentially benefit from any future interest rate cuts while maintaining flexibility in a changing rate environment. The company’s continued focus on specialized lending categories with strong credit metrics suggests a disciplined approach to growth in challenging market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.