5 big analyst AI moves: Nvidia guidance warning; Snowflake, Palo Alto upgraded

Introduction & Market Context

Axos Financial Inc (NYSE:AX) released its fourth quarter fiscal 2025 earnings presentation on July 30, 2025, showcasing continued growth in its loan portfolio and improved credit quality metrics. The digital financial services company, which closed at $85.60 on the presentation date, has maintained its strategic focus on diversified lending and deposit gathering while strengthening its balance sheet.

The presentation follows Axos’s third-quarter performance, which had already demonstrated solid results with an EPS of $1.81 that exceeded analyst expectations. The fourth-quarter slides reveal further momentum in the company’s core business segments.

Quarterly Performance Highlights

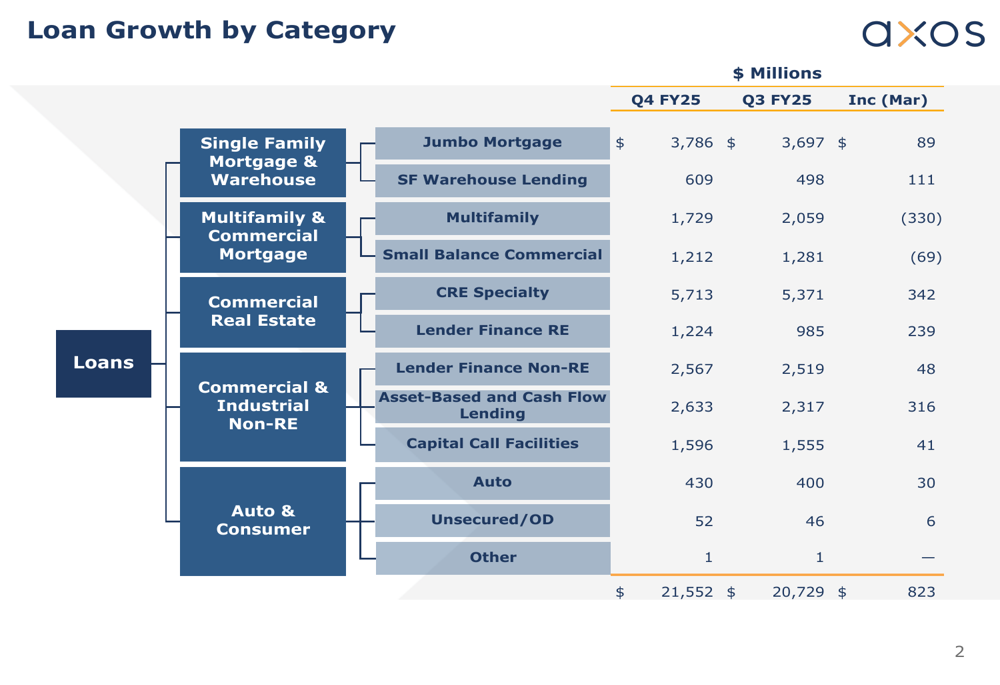

Axos Financial reported continued growth in its loan portfolio, with total loans increasing from $20.73 billion in Q3 FY25 to $21.55 billion in Q4 FY25, representing an $823 million increase quarter-over-quarter. This growth aligns with management’s previous guidance of "high single digits to low teens" loan growth.

The company’s credit quality showed improvement, with non-accrual loans decreasing from 0.89% in Q3 FY25 to 0.79% in Q4 FY25. This positive trend indicates strengthening asset quality despite the expanded loan portfolio.

As shown in the following loan growth breakdown by category:

Commercial Real Estate (CRE) Specialty loans showed the strongest growth, increasing by $342 million quarter-over-quarter to reach $5.71 billion. Asset-Based and Cash Flow Lending also demonstrated significant expansion, growing by $316 million to $2.63 billion. Meanwhile, Multifamily loans decreased by $330 million to $1.73 billion, suggesting a strategic reallocation within the portfolio.

Loan Portfolio Growth and Credit Quality

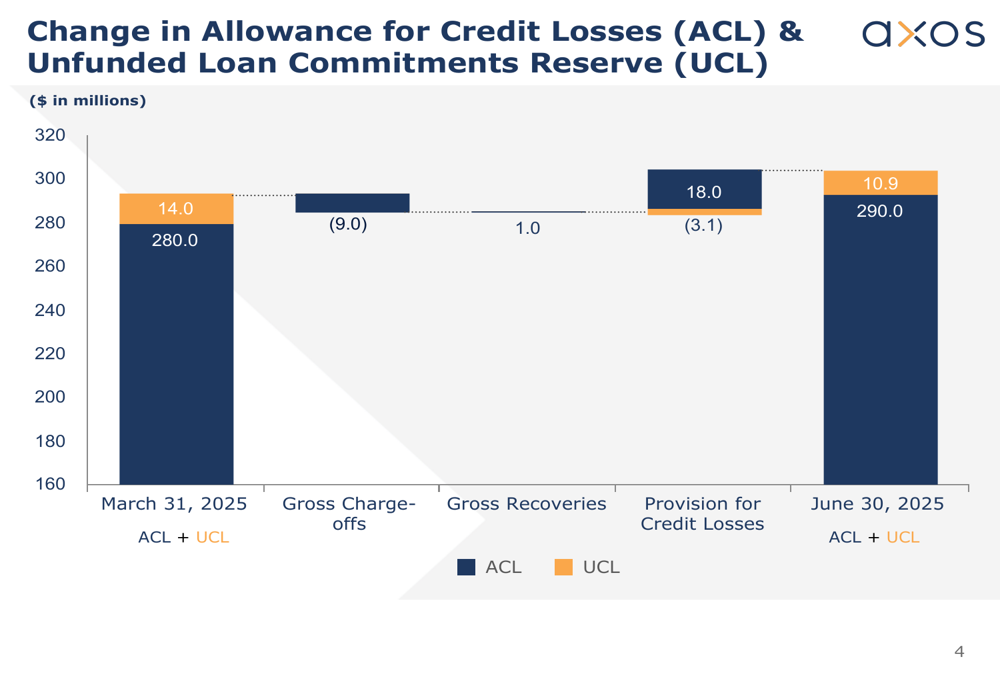

Axos maintained a prudent approach to credit risk management, increasing its Allowance for Credit Losses (ACL) from $280 million to $290 million during the quarter. This conservative stance reflects the company’s commitment to maintaining adequate reserves despite improving credit metrics.

The following chart illustrates the changes in ACL and Unfunded Loan Commitments Reserve (UCL):

The company recorded $9 million in gross charge-offs during the quarter, partially offset by $1 million in recoveries. The provision for credit losses was $18 million, resulting in the net increase to the combined ACL and UCL.

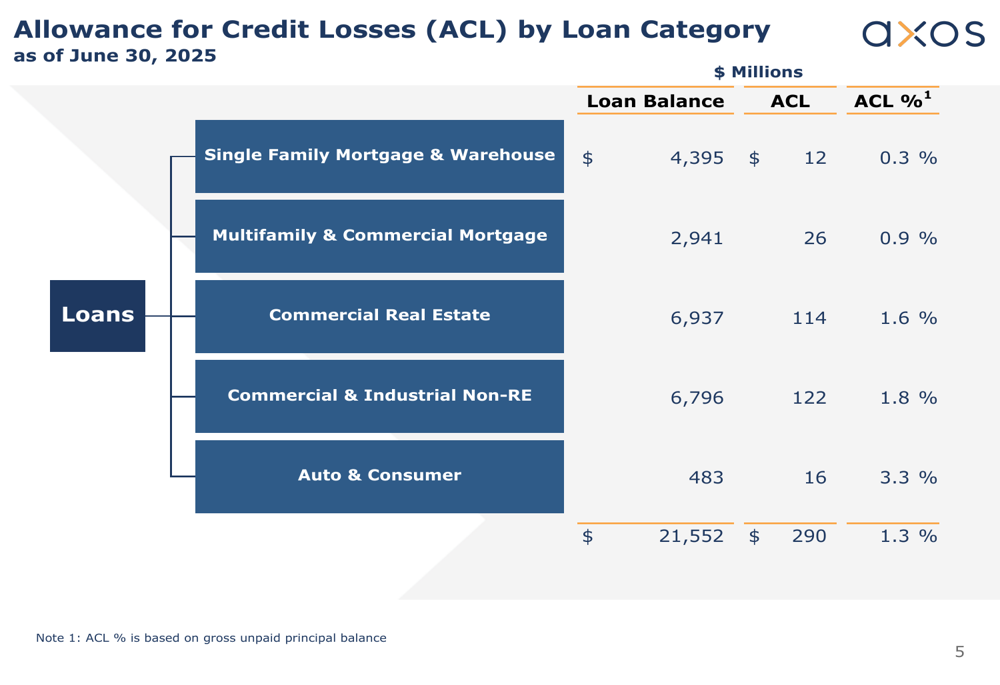

Axos’s allowance allocation varies significantly by loan category, reflecting different risk profiles across its portfolio. The breakdown of ACL by loan category shows:

Commercial & Industrial Non-RE loans carry the highest allowance percentage at 1.8%, followed by Commercial Real Estate at 1.6%. Single Family Mortgage & Warehouse loans have the lowest allowance at 0.3%, reflecting their relatively lower risk profile. The overall ACL percentage stands at 1.3% of the total loan portfolio.

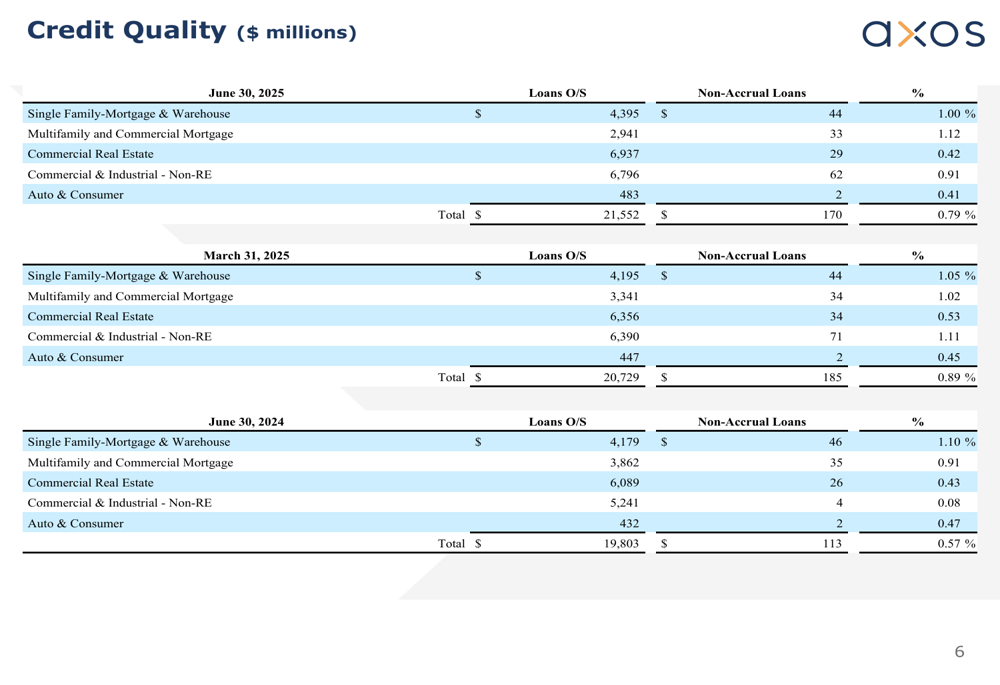

Credit quality metrics show improvement across most loan categories when compared to previous quarters:

Total (EPA:TTEF) non-accrual loans decreased from $185 million (0.89% of total loans) in March 2025 to $170 million (0.79%) in June 2025. This represents a significant improvement in credit quality, though still elevated compared to June 2024 when non-accrual loans were $113 million (0.57%).

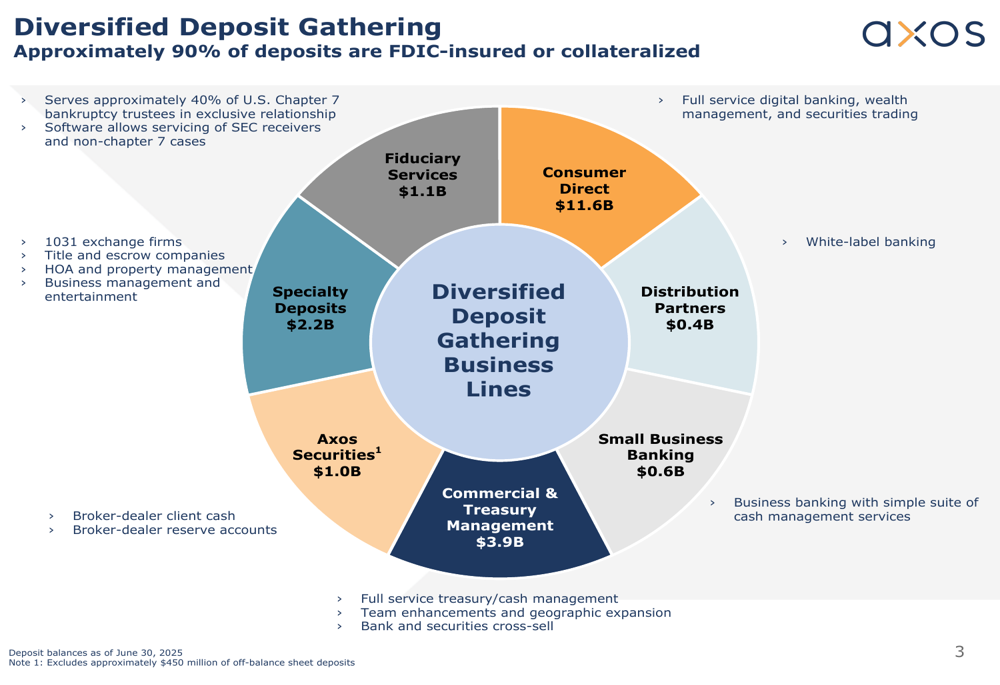

Deposit Strategy and Diversification

A key strength highlighted in Axos’s presentation is its diversified deposit gathering strategy. Approximately 90% of the company’s deposits are either FDIC-insured or collateralized, providing stability to its funding base.

The following chart illustrates the company’s deposit diversification:

Consumer Direct deposits form the largest segment at $11.6 billion, followed by Commercial & Treasury Management at $3.9 billion. The company also maintains specialized deposit channels, including Specialty Deposits ($2.2 billion), Fiduciary Services ($1.1 billion), and Axos Securities ($1.0 billion, excluding approximately $450 million of off-balance sheet deposits).

This multi-channel approach has enabled Axos to build a stable funding base while serving niche markets, including approximately 40% of U.S. Chapter 7 bankruptcy trustees. The diversification strategy helps mitigate concentration risk and supports the company’s continued growth.

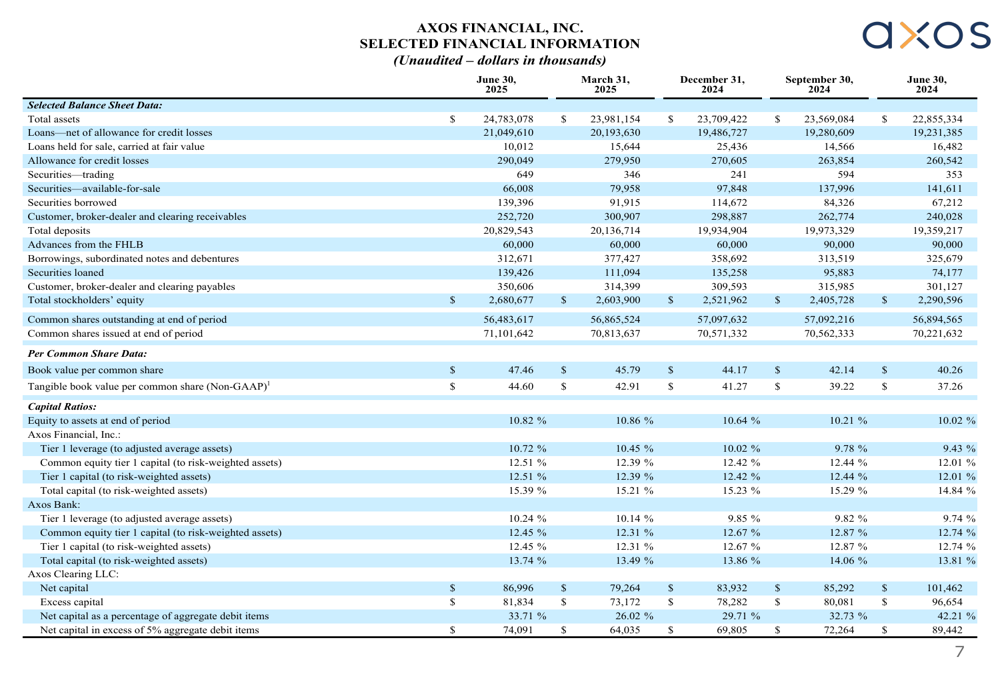

Financial Performance and Outlook

Axos Financial maintained strong financial performance across key metrics during the quarter. The company’s selected financial information shows solid capital ratios and growth in stockholders’ equity:

Total assets reached $24.78 billion as of June 30, 2025, while total stockholders’ equity increased to $2.68 billion. Book value per common share rose to $47.46, and tangible book value per common share reached $44.60, demonstrating continued value creation for shareholders.

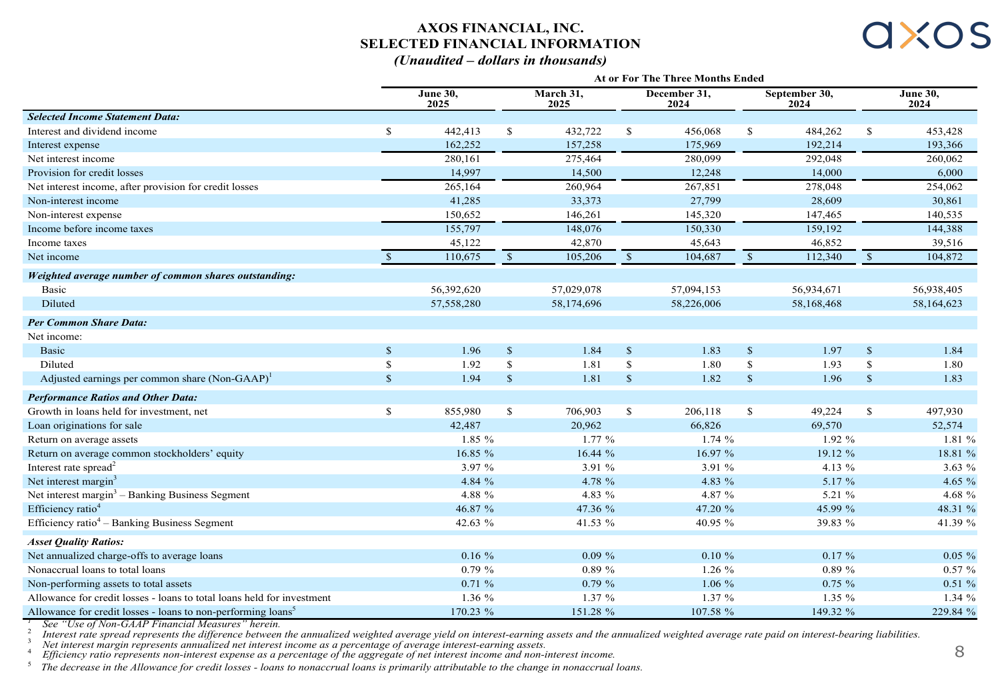

The company’s income statement metrics also remained robust:

Net income for the three months ended June 30, 2025, was $112.3 million, up from $104.9 million in the previous quarter. Return on average assets stood at 1.92%, while return on average common stockholders’ equity was 19.12%. The net interest margin was 5.17%, showing improvement from previous quarters.

These results indicate that Axos continues to execute effectively on its business strategy, maintaining profitability while growing its loan portfolio and improving credit quality. The company’s diversified business model and focus on digital financial services position it well for continued growth in an increasingly competitive banking environment.

With strong capital ratios, improving credit metrics, and a diversified deposit base, Axos Financial appears well-positioned to navigate potential economic challenges while pursuing strategic growth opportunities in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.