Gold prices tick higher on fresh US tariff threats, Fed rate cut hopes

Introduction & Market Context

Balco Group AB (STO:BALCO) shares plunged 13.12% on April 28, 2025, after the Nordic balcony solutions provider presented first-quarter results showing negative margins and announced significant restructuring measures. The company, which specializes in glazed balconies and balcony solutions primarily for the renovation market, reported that market recovery is progressing slower than anticipated despite increased quotation activity.

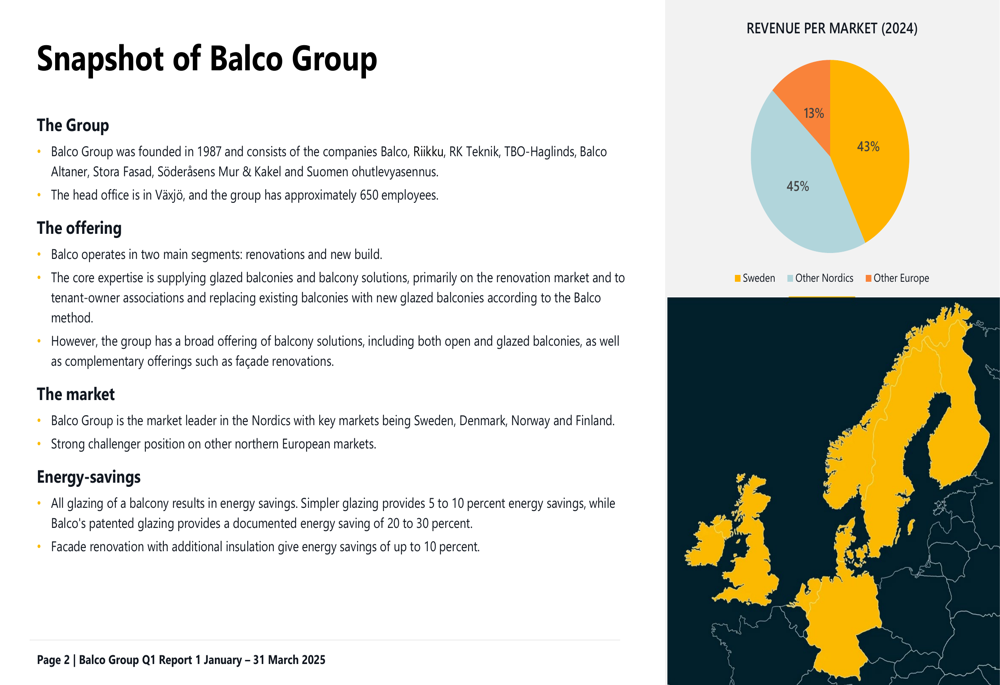

As a market leader in the Nordics with operations across Northern Europe, Balco faces varying regional challenges, with its revenue distribution showing Sweden accounting for 45% of sales, other Nordic countries 43%, and other European markets 13%.

Quarterly Performance Highlights

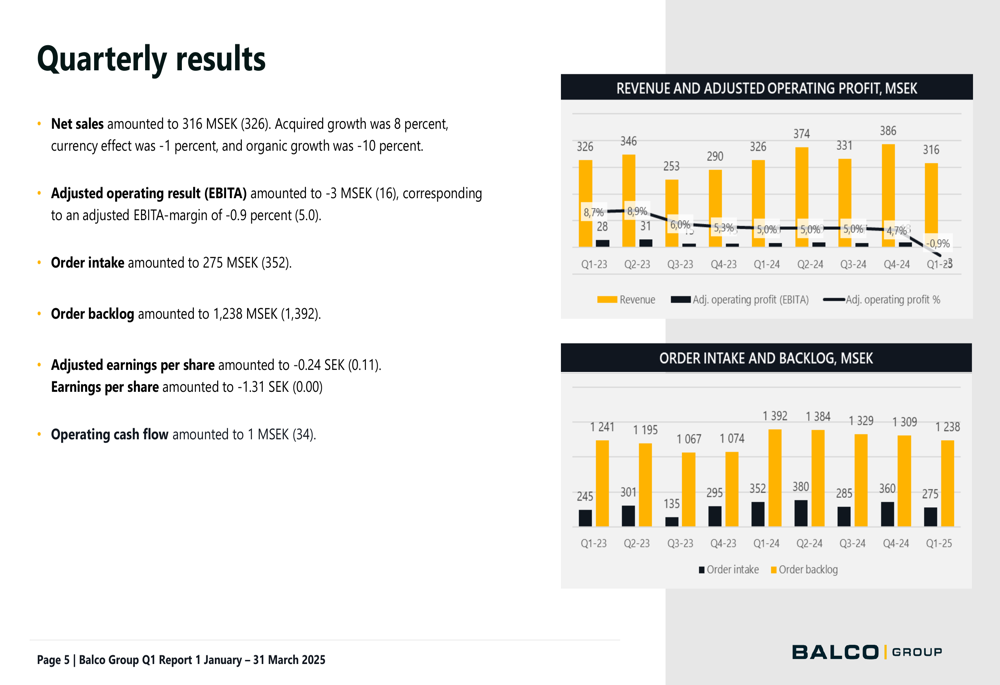

Balco reported net sales of 316 MSEK for Q1 2025, representing a 3% decrease from 326 MSEK in the same period last year. The company’s adjusted EBITA margin turned negative at -0.9%, down significantly from 5.0% in Q1 2024. Order intake declined to 275 MSEK compared to 352 MSEK in the prior-year period, with the order backlog standing at 1,238 MSEK, down from 1,392 MSEK.

The quarterly results show a concerning trend across multiple financial metrics, with adjusted earnings per share falling to -0.24 SEK from 0.11 SEK in Q1 2024, while operating cash flow decreased dramatically to 1 MSEK from 34 MSEK in the comparable period.

As shown in the following chart of quarterly revenue and adjusted operating profit:

Strategic Initiatives

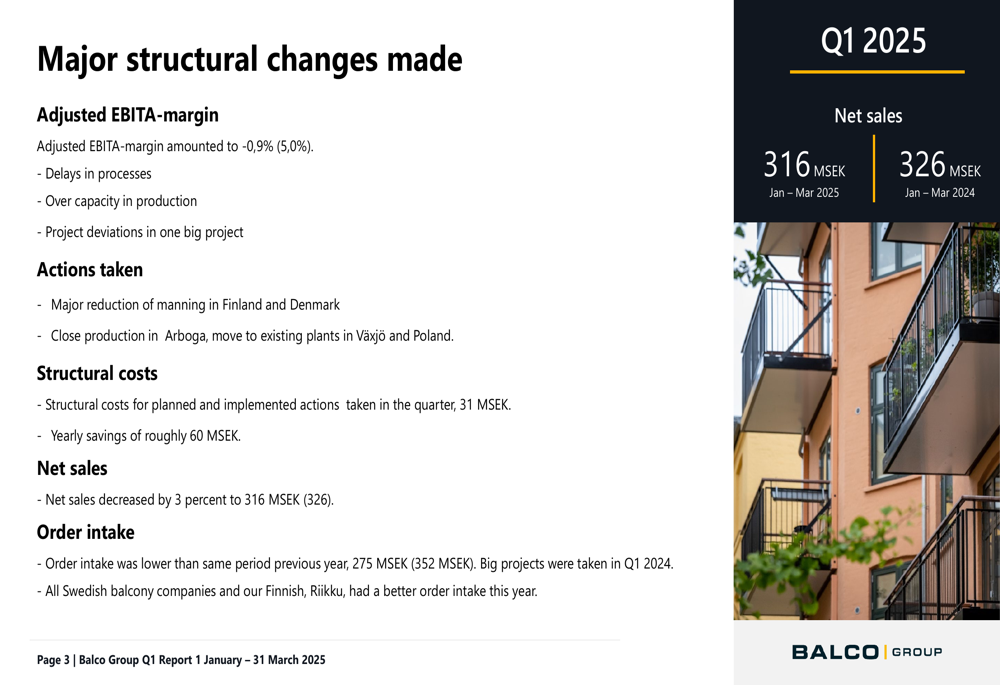

In response to operational challenges, Balco has implemented major structural changes aimed at improving profitability. The company cited delays in processes, overcapacity in production, and project deviations in one large project as key factors behind the poor quarterly performance.

The restructuring includes significant workforce reductions in Finland and Denmark, as well as the closure of production facilities in Arboga, with operations being transferred to existing plants in Växjö, Sweden and Poland. These measures resulted in structural costs of 31 MSEK during the quarter but are expected to generate annual savings of approximately 60 MSEK.

The following slide details the major structural changes implemented:

Segment Analysis

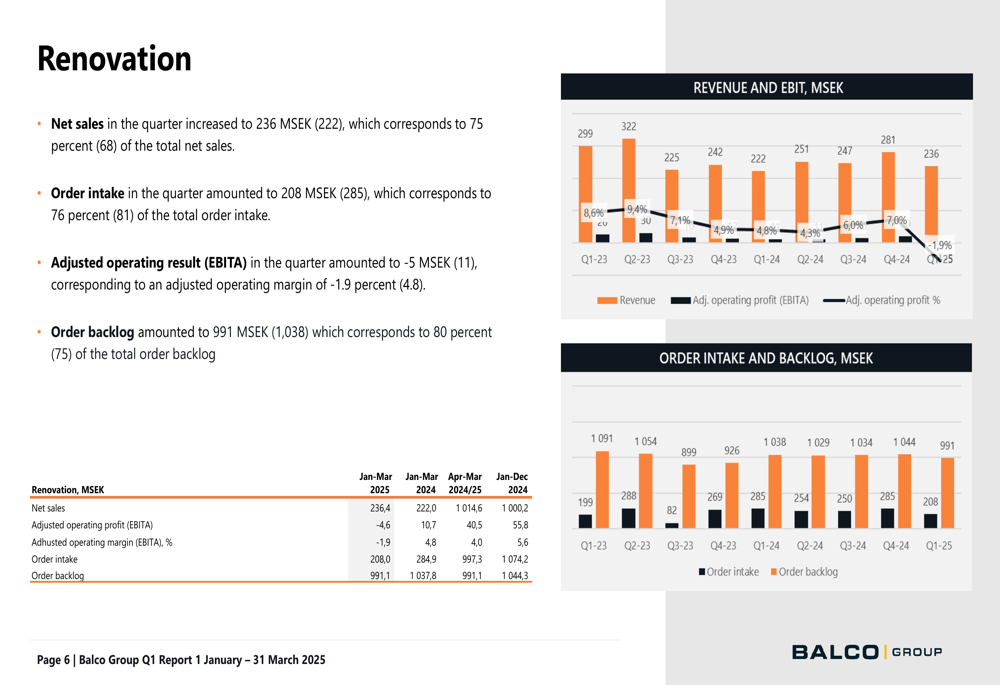

Balco’s business is divided into two main segments: Renovation and New Build. The Renovation segment, which constitutes 75% of total sales, showed resilience with net sales increasing to 236 MSEK from 222 MSEK in Q1 2024. However, the segment’s adjusted EBITA margin turned negative at -1.9%, down from 4.8% in the prior-year period. Order intake for the Renovation segment amounted to 208 MSEK, down from 285 MSEK.

The segment performance is illustrated in the following chart:

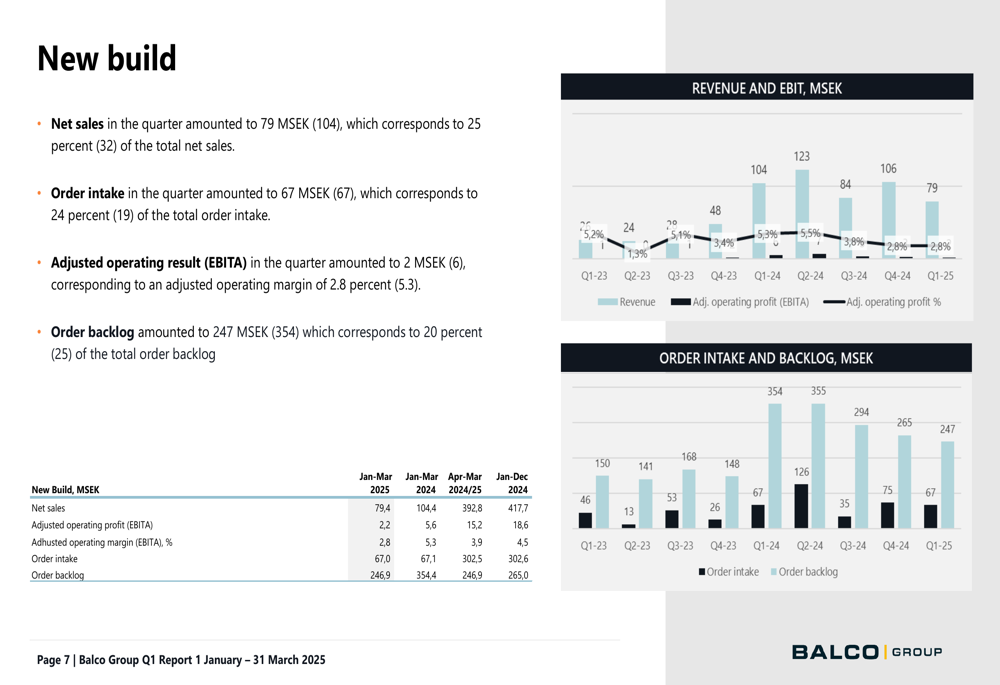

Meanwhile, the New Build segment, representing 25% of total sales, experienced a more significant decline with net sales falling to 79 MSEK from 104 MSEK in Q1 2024. Despite the sales decrease, this segment maintained a positive adjusted EBITA margin of 2.8%, though down from 5.3% in the comparable period. Order intake remained stable at 67 MSEK.

The New Build segment performance is shown below:

Forward-Looking Statements

Balco’s management maintains that the overall market will gradually improve but acknowledges that recovery will take longer than previously anticipated, with setbacks likely to occur. The company expects the coming quarters to be affected in terms of sales and earnings, with an aim to return to earnings levels in line with the previous year.

The company highlighted increased customer activity in the renovation segment in Sweden and Norway, though noted delays in permission processes. The Finnish new build market appears to have bottomed out, but no rapid return is expected. Balco also reported good activity in the new build segment in the UK and Germany, where it has increased investment in local design resources.

The maritime segment, which had been struggling, has started to recover with new orders for ships to shipyards.

Financial Position

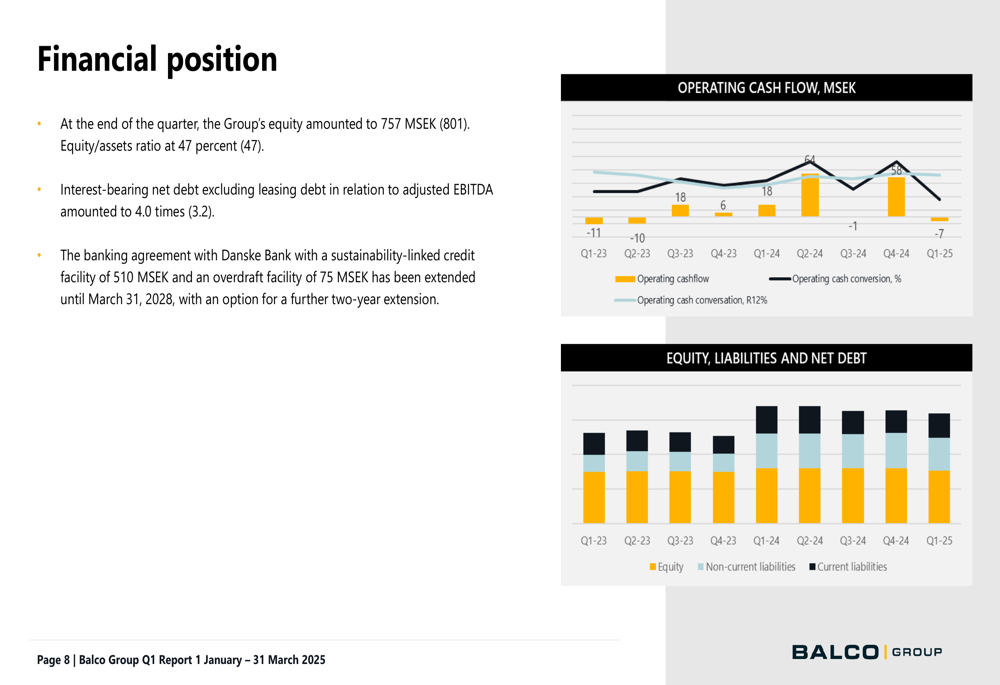

At the end of Q1 2025, Balco’s equity amounted to 757 MSEK, down from 801 MSEK, with an equity/assets ratio holding steady at 47%. The company’s interest-bearing net debt excluding leasing debt in relation to adjusted EBITDA increased to 4.0 times from 3.2 times.

In a positive development for financial stability, Balco extended its banking agreement with Danske Bank (CSE:DANSKE) until March 31, 2028, with an option for a further two-year extension. The agreement includes a sustainability-linked credit facility of 510 MSEK and an overdraft facility of 75 MSEK.

The following chart illustrates the company’s financial position:

Despite the current challenges, Balco emphasized its strong market position, high-quality products, and the long durability of its offerings, with glazed balconies having an estimated lifetime of 90 years and city balconies 70 years. The company continues to invest in sales, market, and product development, highlighting that the fundamental need for its services and products remains strong in the long term.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.