Lisa Cook sues Trump over firing attempt, emergency hearing set

Introduction & Market Context

Baldwin Insurance Group Inc. (NYSE:BWIN) released its second quarter 2025 earnings presentation on August 5, 2025, highlighting 11% organic revenue growth despite continued stock price pressure. The company’s shares closed at $36.46, showing a modest 1.25% gain on the day, but remain significantly below their 52-week high of $55.82.

The Q2 results come after a challenging first quarter where Baldwin missed revenue forecasts despite slightly beating earnings expectations. The company’s stock has continued to decline since the end of Q2, when it was trading at $42.81, reflecting ongoing investor concerns despite solid operational performance.

Quarterly Performance Highlights

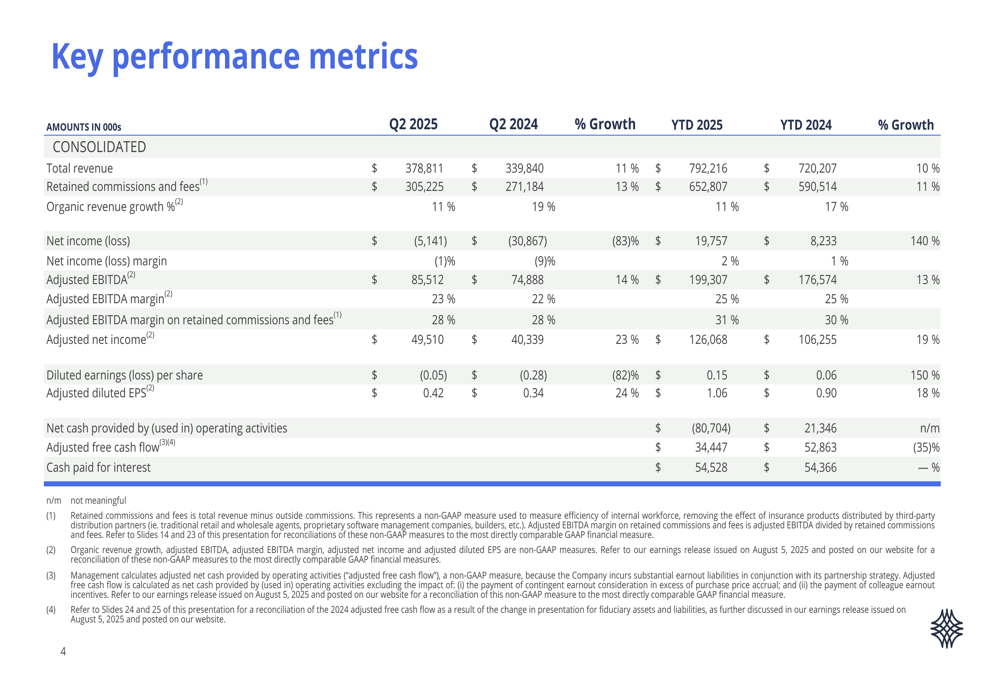

Baldwin reported total revenue of $378,811 thousand for Q2 2025, representing an 11% increase compared to the same period last year. Retained commissions and fees grew by 13% to $305,225 thousand, while organic revenue growth remained strong at 11%.

The company posted a net loss of $5,141 thousand for the quarter, a significant improvement from the $30,867 thousand loss reported in Q2 2024. Adjusted EBITDA increased by 14% to $85,512 thousand, with adjusted net income rising 23% to $49,510 thousand. Adjusted diluted earnings per share grew 24% year-over-year to $0.42.

As shown in the following comprehensive performance metrics table:

Despite the strong top-line and adjusted earnings growth, Baldwin’s adjusted free cash flow declined by 35% year-over-year to $34,447 thousand. This decrease may put pressure on the company’s previously stated goal of generating $150-175 million in free cash flow for the full year, as mentioned in their Q1 earnings call.

Strategic Initiatives

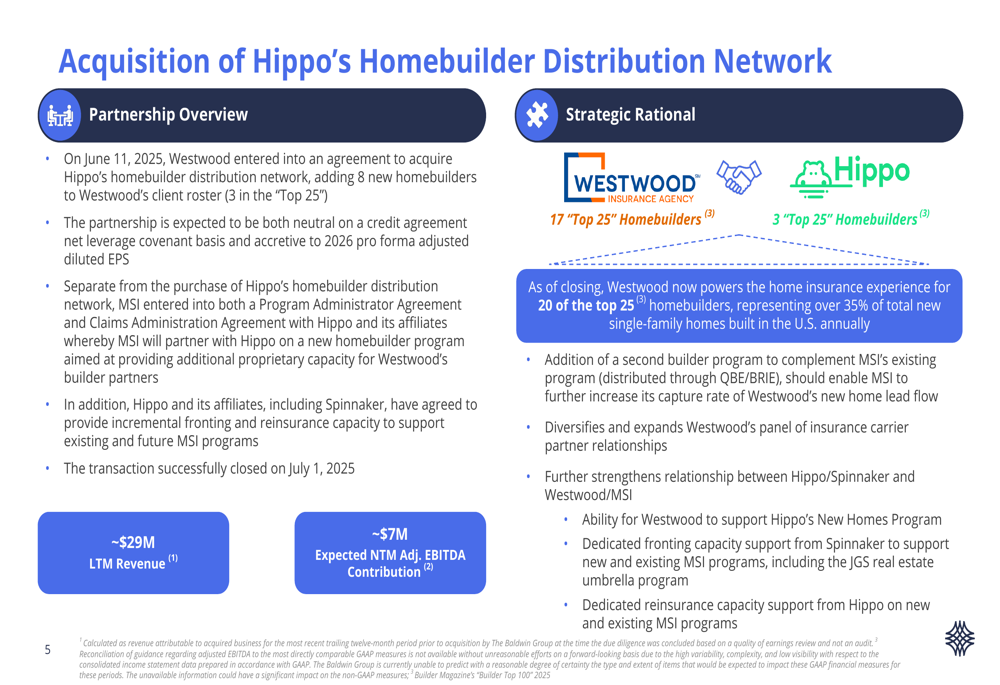

The most significant strategic development in Q2 was Baldwin’s acquisition of Hippo’s Homebuilder Distribution Network, completed on June 11, 2025. This acquisition strengthens Baldwin’s position in the homebuilder insurance market, adding 8 new homebuilders, including 3 in the "Top 25."

The transaction, which closed on July 1, 2025, is expected to be neutral on Baldwin’s credit agreement net leverage covenant basis and accretive to 2026 pro forma adjusted diluted EPS. The acquired business generated approximately $29 million in revenue over the last twelve months and is expected to contribute around $7 million in adjusted EBITDA over the next twelve months.

The strategic rationale and partnership details are illustrated in the following slide:

With this acquisition, Baldwin now powers home insurance for 20 of the top 25 homebuilders, representing over 35% of new single-family homes built in the U.S. annually. The deal also diversifies Baldwin’s carrier relationships and strengthens its partnership with Hippo/Spinnaker.

Detailed Financial Analysis

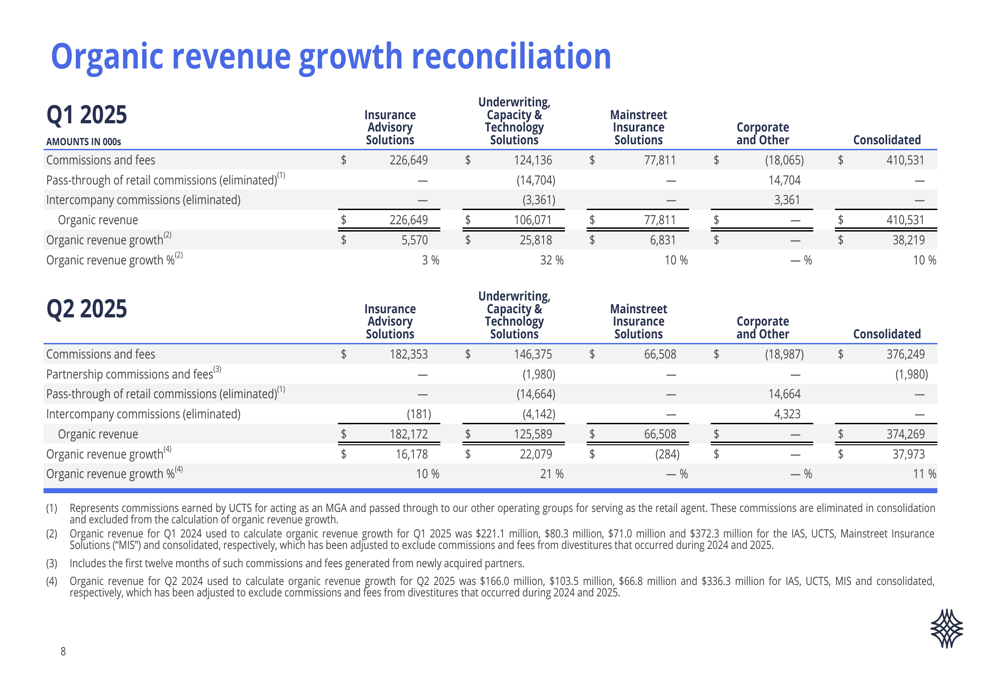

Baldwin’s performance varied across its business segments. The Underwriting, Capacity & Technology Solutions segment showed the strongest organic growth at 21% for Q2 2025, while Insurance Advisory Solutions grew by 10%. However, Mainstreet Insurance Solutions experienced a 2% decline in organic revenue for the quarter.

The following reconciliation shows the components of Baldwin’s organic revenue growth:

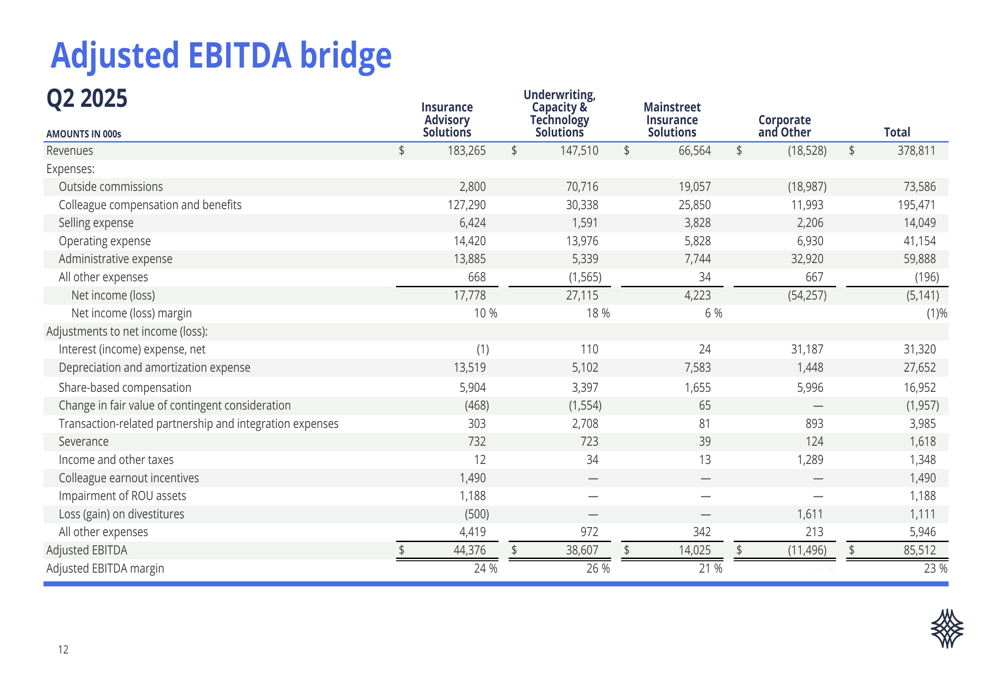

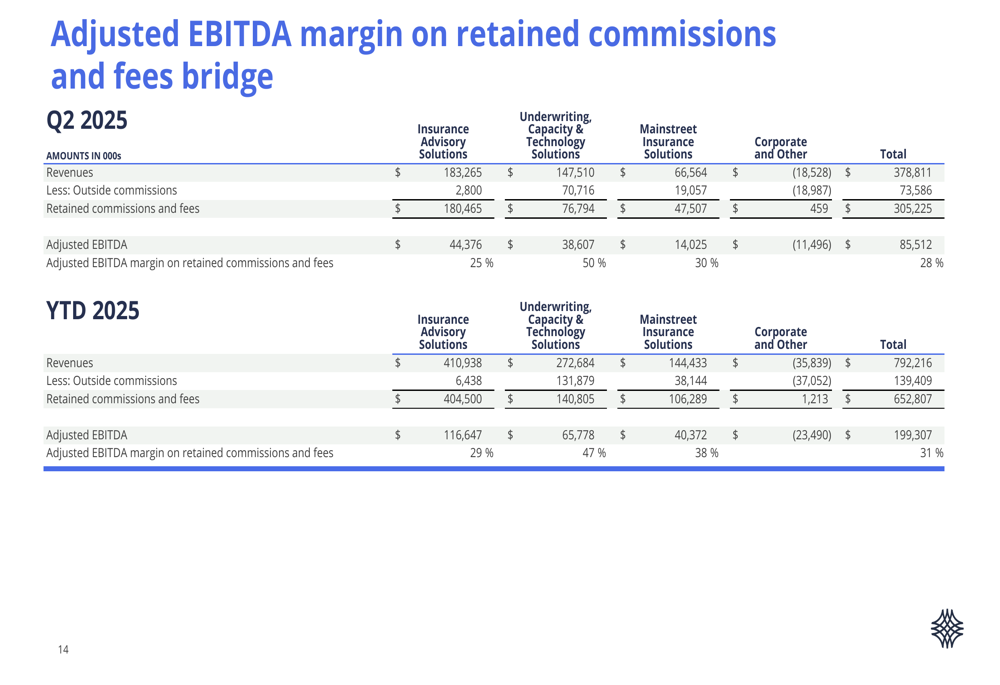

The company’s adjusted EBITDA for Q2 2025 was $85,512 thousand, representing a 23% margin on total revenue. When calculated on retained commissions and fees, the adjusted EBITDA margin was 28%, consistent with the same period last year.

The components contributing to adjusted EBITDA are detailed in the following bridge:

For the first half of 2025, Baldwin’s adjusted EBITDA reached $199,307 thousand, a 13% increase from the first half of 2024. The year-to-date adjusted EBITDA margin on retained commissions and fees was 31%, up from 30% in the comparable period last year.

The following slide illustrates the adjusted EBITDA margin calculation:

Financial Position

As of June 30, 2025, Baldwin maintained a substantial debt position, with $600,000 thousand in Senior Secured Notes at a 7.125% interest rate maturing in May 2031, and $931,121 thousand in Term Loan debt at a 7.31% interest rate also maturing in May 2031. The company had drawn $112,000 thousand from its Revolving Facility, with $474,000 thousand still available.

The weighted average Class A & B shares outstanding increased slightly from 118,373 thousand in Q1 2025 to 119,163 thousand in Q2 2025. The company’s stock price declined from $44.69 at the end of Q1 to $42.81 at the end of Q2, and has since fallen further to $36.46 as of August 5, 2025.

Forward-Looking Statements

While Baldwin did not provide specific updated guidance in the presentation, the company’s acquisition of Hippo’s Homebuilder Distribution Network is expected to contribute positively to future performance. The acquisition is projected to be accretive to 2026 pro forma adjusted diluted EPS and add approximately $7 million in adjusted EBITDA over the next twelve months.

The decline in adjusted free cash flow compared to the previous year may present challenges for Baldwin in meeting its previously stated full-year target of $150-175 million. Additionally, the continued decline in stock price despite solid operational performance suggests ongoing investor concerns about the company’s long-term growth prospects and debt levels.

Baldwin’s year-to-date performance, with 11% organic revenue growth and 13% adjusted EBITDA growth, positions the company to potentially meet or exceed the mid-to-high single-digit organic growth guidance for its Insurance Advisory Solutions segment and double-digit overall growth that was maintained during the Q1 earnings call.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.