Street Calls of the Week

Introduction & Market Context

Banca IFIS (BIT:IF) presented its first quarter 2025 results on May 8, 2025, showing resilience in a challenging interest rate environment. The Italian specialized lender reported a net income of €47 million, driven by its Commercial Banking and NPL businesses. The stock closed at €22.78 on the day of the presentation, up 0.35%, reflecting investor confidence in the bank’s performance and strategic direction.

Quarterly Performance Highlights

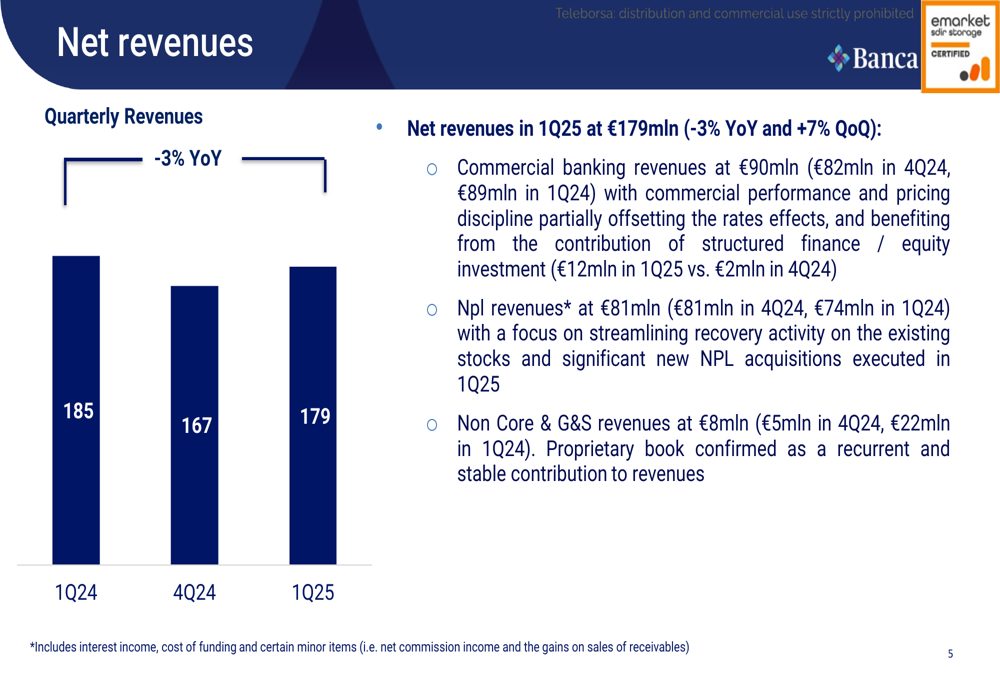

Banca IFIS reported net revenues of €179 million for Q1 2025, representing a 7% increase quarter-over-quarter, though a 3% decrease year-over-year. The bank maintained solid profitability while focusing on reducing its cost of funding following TLTRO repayment.

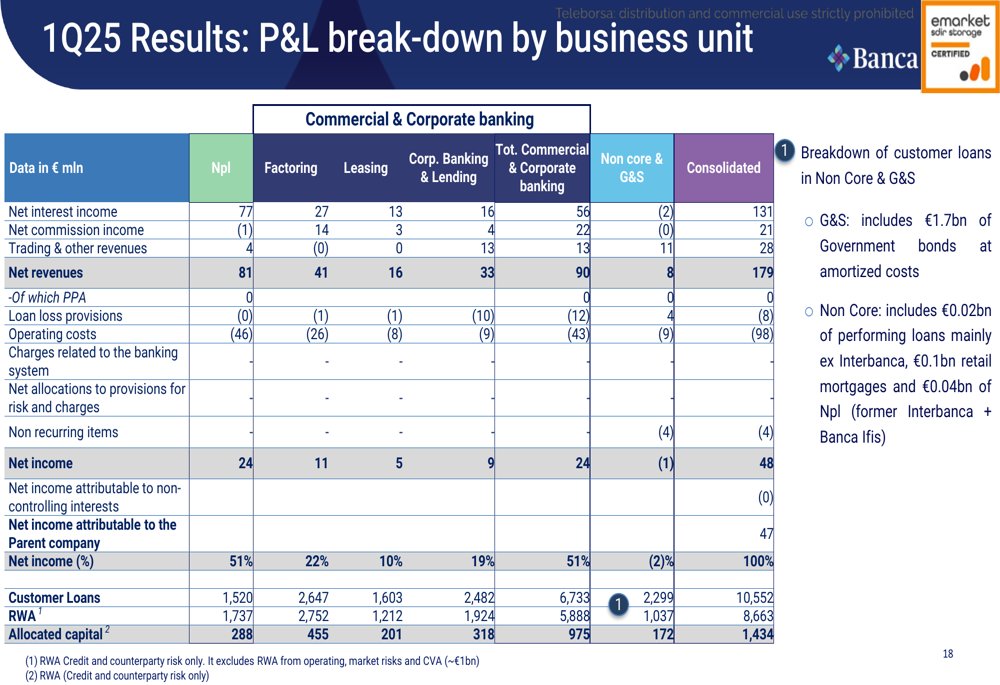

As shown in the following revenue breakdown chart, Commercial Banking contributed €90 million, NPL activities generated €81 million, and Non-Core & G&S added €8 million to the total revenue:

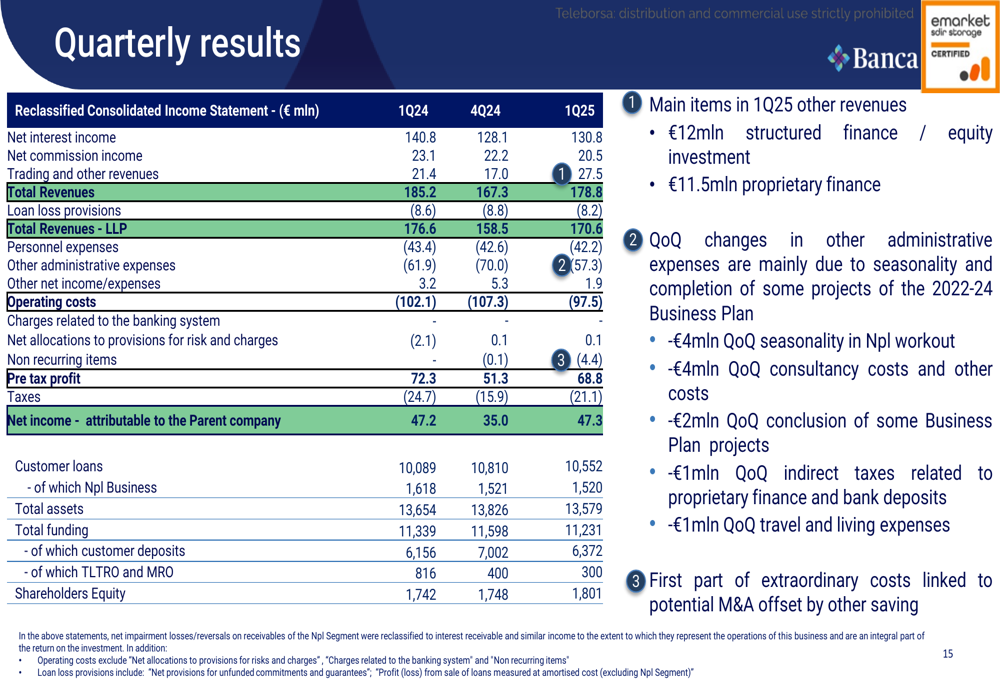

Operating costs decreased significantly to €98 million, down 9% from the previous quarter, demonstrating the bank’s commitment to operational efficiency. The bank also reported that loan loss provisions remained substantially flat, reflecting stable asset quality.

The quarterly consolidated income statement provides a comprehensive view of the bank’s performance:

Segment Performance Analysis

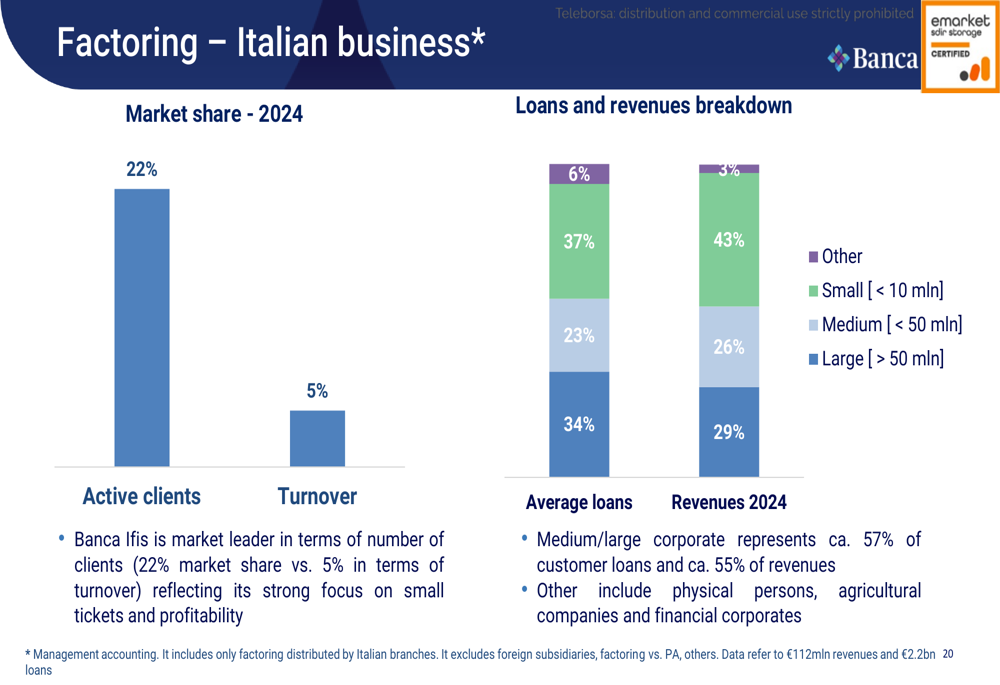

The bank’s factoring business maintained stable performance with a turnover of €3.0 billion in Q1 2025, in line with Q1 2024 but slightly down from €3.4 billion in Q4 2024. This segment continues to be a cornerstone of Banca IFIS’s business model, with the bank holding a 22% market share in active clients and 5% in turnover within the Italian market.

The following chart illustrates the factoring segment’s market position and revenue distribution by client size:

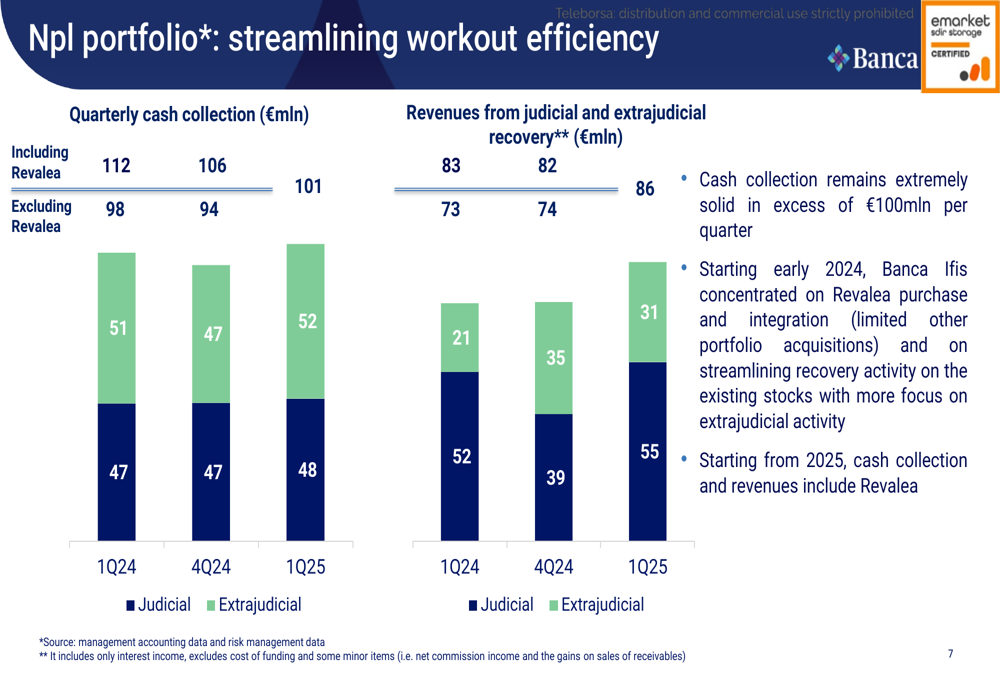

In the NPL business, cash collection reached €101 million in Q1 2025, with revenues from judicial and extrajudicial recovery totaling €86 million. The bank has strategically shifted focus to streamlining recovery activities.

The NPL portfolio performance metrics demonstrate the effectiveness of the bank’s recovery strategies:

Capital Position and Risk Management

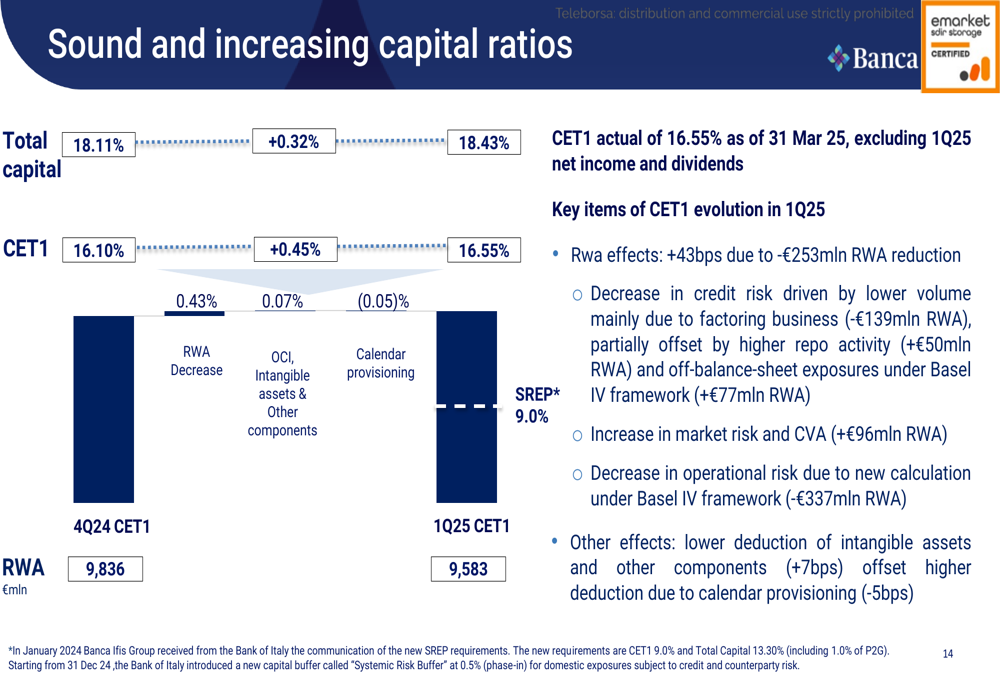

Banca IFIS maintained a strong capital position with a CET1 ratio exceeding 16.55% (excluding Q1 2025 net income), well above the 9.0% SREP requirement. This solid capital base supports the board’s proposal of €111.5 million in total dividends for 2024, equivalent to €2.12 per share.

The following chart illustrates the bank’s capital ratio evolution:

The bank has been actively managing its interest rate sensitivity, reducing potential impact from a 0.50% decrease in reference rates from €11-13 million in March 2024 to €6-8 million in March 2025. This has been achieved through increasing the duration of the proprietary bond portfolio and boosting origination of fixed-rate leasing.

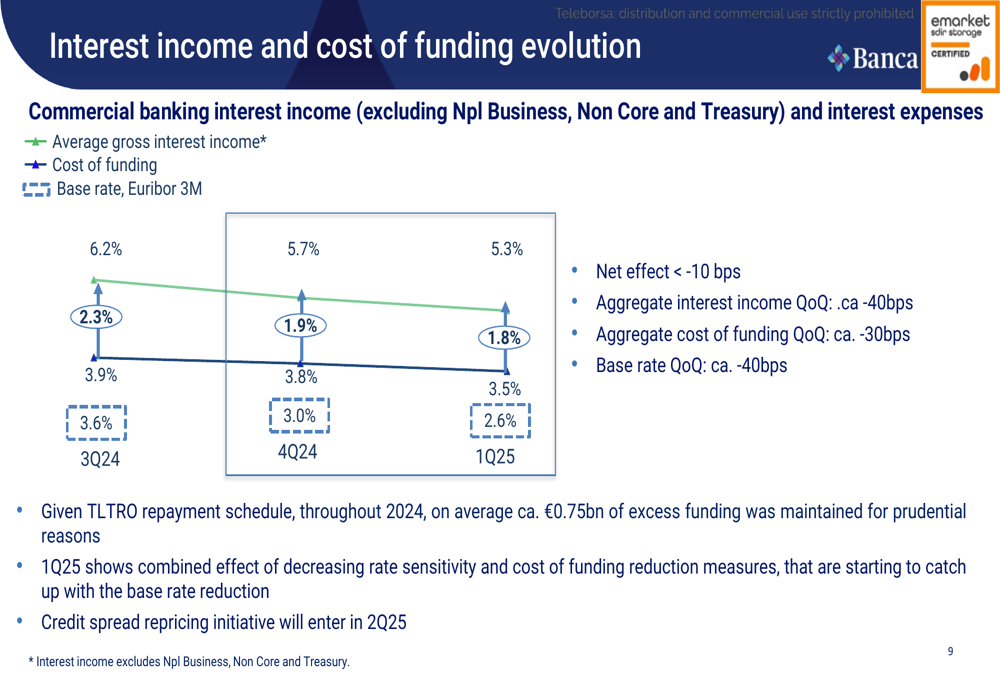

Interest income and funding costs have evolved favorably, with the cost of funding decreasing to 1.8% in Q1 2025 from 1.9% in Q4 2024, despite the TLTRO repayment:

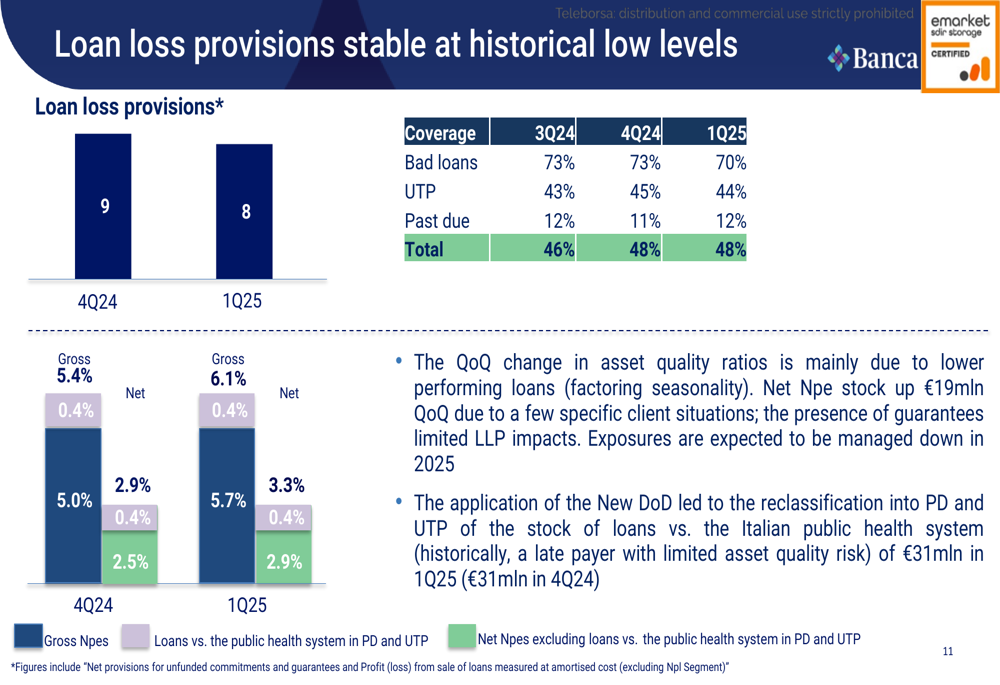

Asset quality remains strong, with coverage ratios for non-performing exposures maintained at healthy levels. The total coverage ratio stood at 48% in Q1 2025, unchanged from Q4 2024:

ESG Achievements

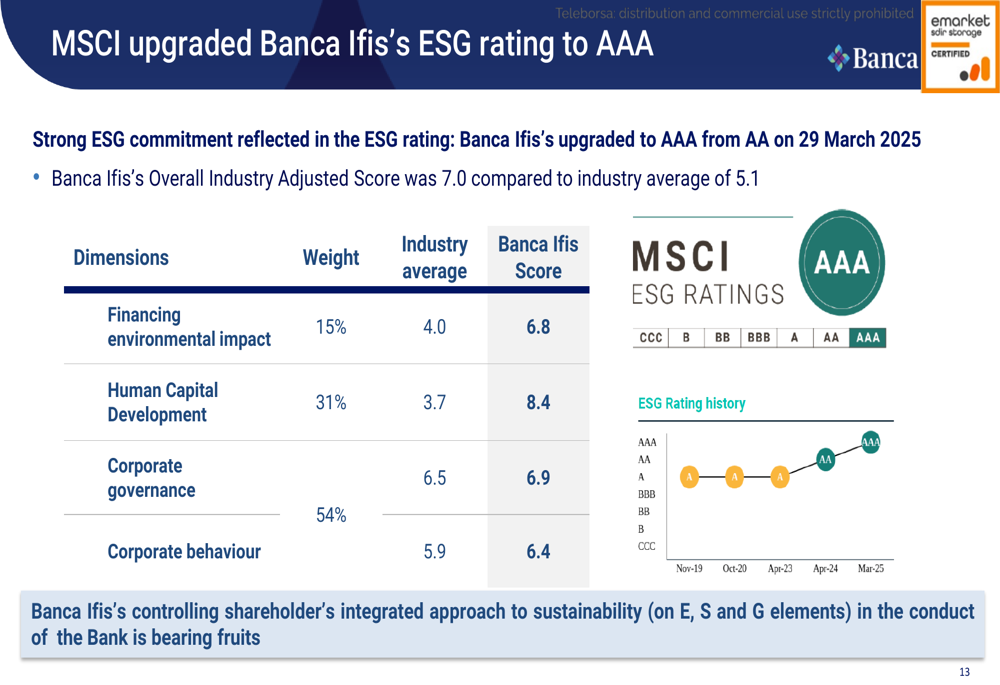

A significant milestone for Banca IFIS was the upgrade of its MSCI ESG rating to AAA on March 29, 2025, from the previous AA rating. The bank achieved an Overall Industry Adjusted Score of 7.0, compared to an industry average of 5.1, demonstrating its commitment to environmental, social, and governance best practices.

The ESG rating breakdown highlights the bank’s particularly strong performance in human capital development:

Forward-Looking Statements

Banca IFIS has outlined its focus on several strategic initiatives for the remainder of 2025, including:

1. Continuing to reduce interest rate sensitivity through portfolio duration management and fixed-rate origination

2. Maintaining strict cost control while investing in strategic growth areas

3. Further streamlining NPL recovery activities to optimize returns

4. Advancing ESG initiatives, with expected dividend flow increase of around 30% in 2025 versus 2024

The bank’s business unit breakdown provides insight into how each segment contributes to the overall performance and will likely drive future growth:

Banca IFIS appears well-positioned to navigate the evolving interest rate environment while maintaining its leadership in specialized financing segments. With its strong capital position, operational efficiency improvements, and top-tier ESG rating, the bank has established a solid foundation for sustainable growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.