Street Calls of the Week

Introduction & Market Context

Banco Comercial Português (BCP) released its H1 2025 earnings presentation on July 31, 2025, reporting a 3.5% increase in net income to €502.3 million, continuing the growth momentum seen in Q1 2025. The bank’s stock has performed strongly this year, currently trading at €0.6888, near its 52-week high of €0.705, reflecting investor confidence in the bank’s strategy and performance.

The results demonstrate BCP’s continued focus on digital transformation and international expansion, while maintaining solid capital and liquidity positions. The bank faces some headwinds from rising operating costs and declining net interest margins in Portugal, but these are partially offset by strong growth in international operations and fee income.

Executive Summary

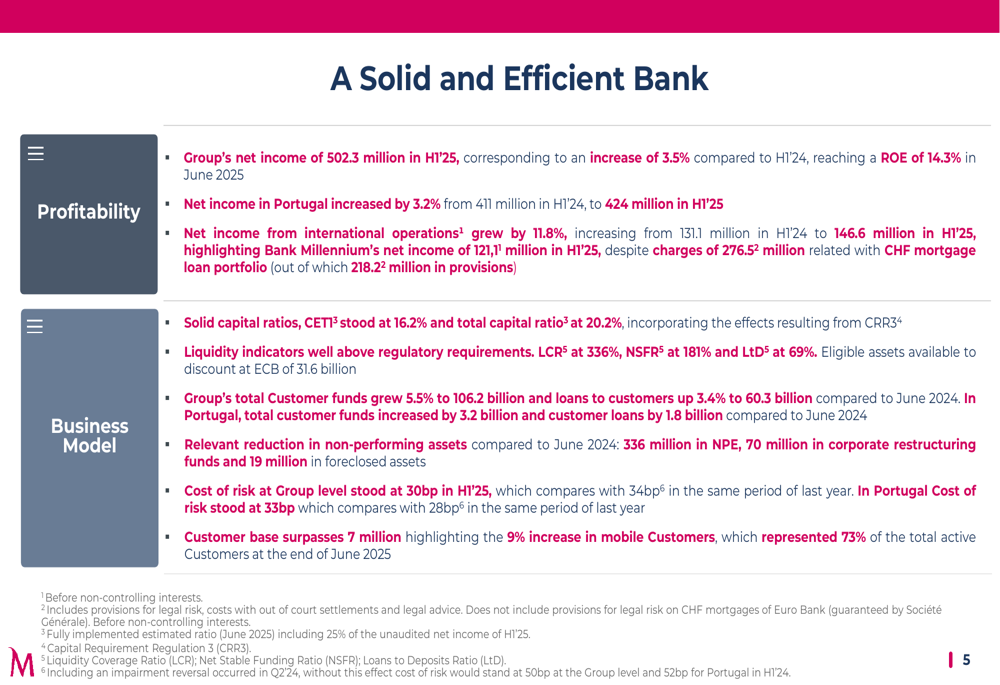

Millennium bcp delivered a solid performance in the first half of 2025, with group net income reaching €502.3 million, up 3.5% year-over-year. The bank achieved a return on equity (ROE) of 14.3% and return on tangible equity (ROTE) of 14.9%, showing improvement from the 13.9% ROE reported in Q1 2025.

Net income in Portugal increased by 3.2% to €424 million, while international operations showed stronger growth of 11.8% to €146.6 million. The bank maintained strong capital ratios, with CET1 at 16.2% and total capital ratio at 20.2%, well above regulatory requirements.

As shown in the following comprehensive performance overview:

Customer funds grew 5.5% to €106.2 billion, and customer loans increased 3.4% to €60.3 billion. The bank also reported significant reductions in non-performing assets, with NPE down by €336 million compared to June 2024.

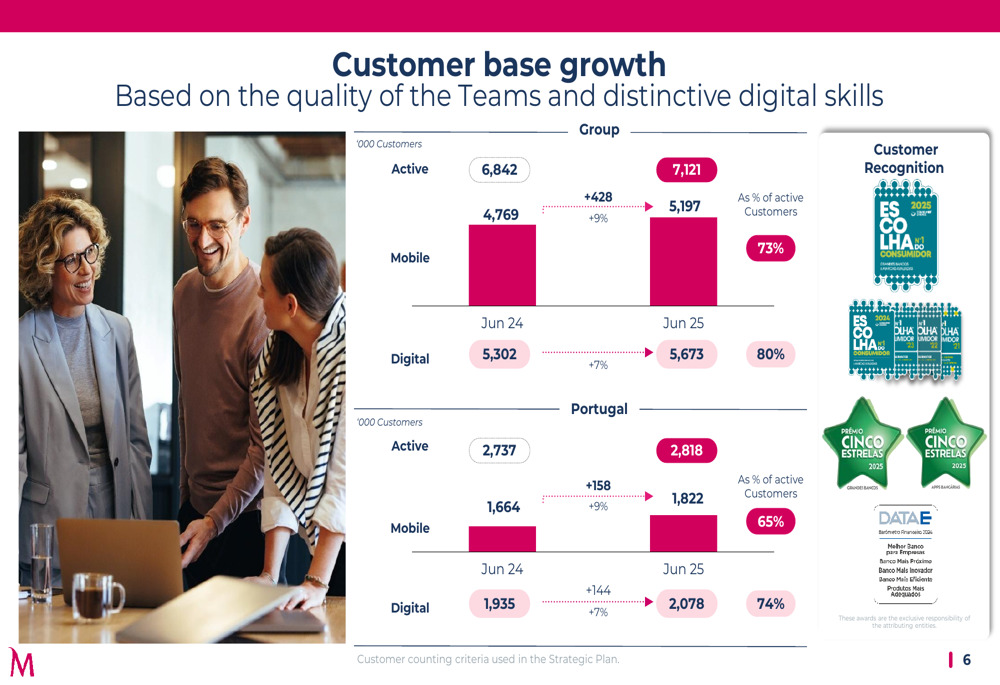

BCP’s customer base surpassed 7 million, with particularly strong growth in mobile customers, which increased 9% year-over-year and now represent 73% of total active customers. This digital transformation is driving significant improvements in customer engagement and operational efficiency.

The bank’s customer base growth across different segments is illustrated here:

Detailed Financial Analysis

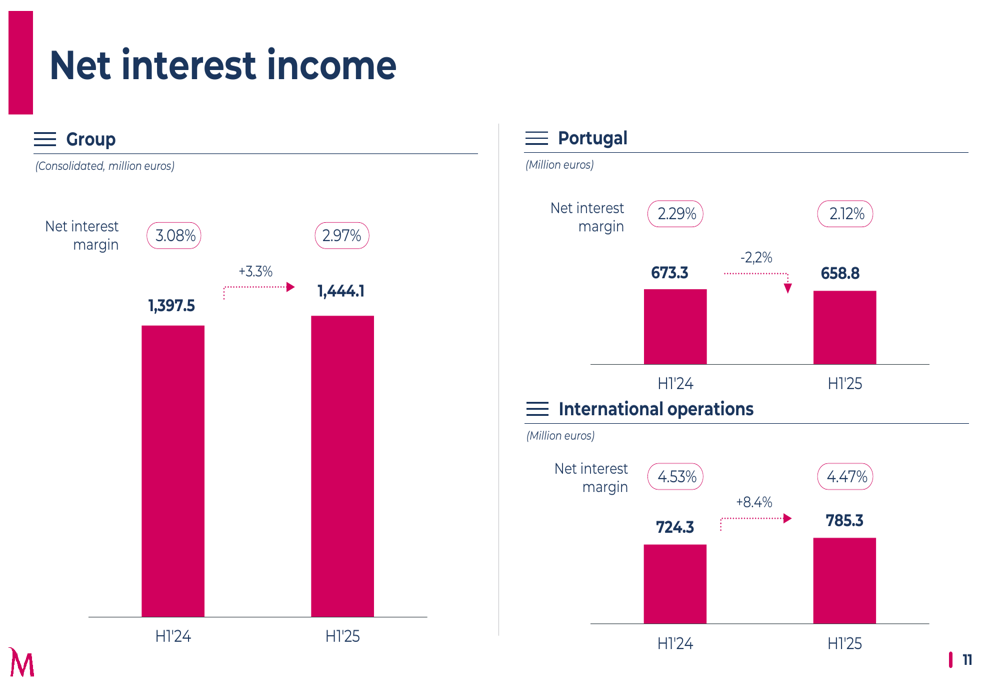

Net interest income, the bank’s main revenue source, increased 3.3% year-over-year to €1,444.1 million. However, this growth was uneven across regions, with Portugal experiencing a 2.2% decline to €658.8 million, while international operations saw an 8.4% increase to €785.3 million. Net interest margin declined from 3.08% to 2.97% at the group level, and from 2.29% to 2.12% in Portugal.

The following chart details the net interest income performance across regions:

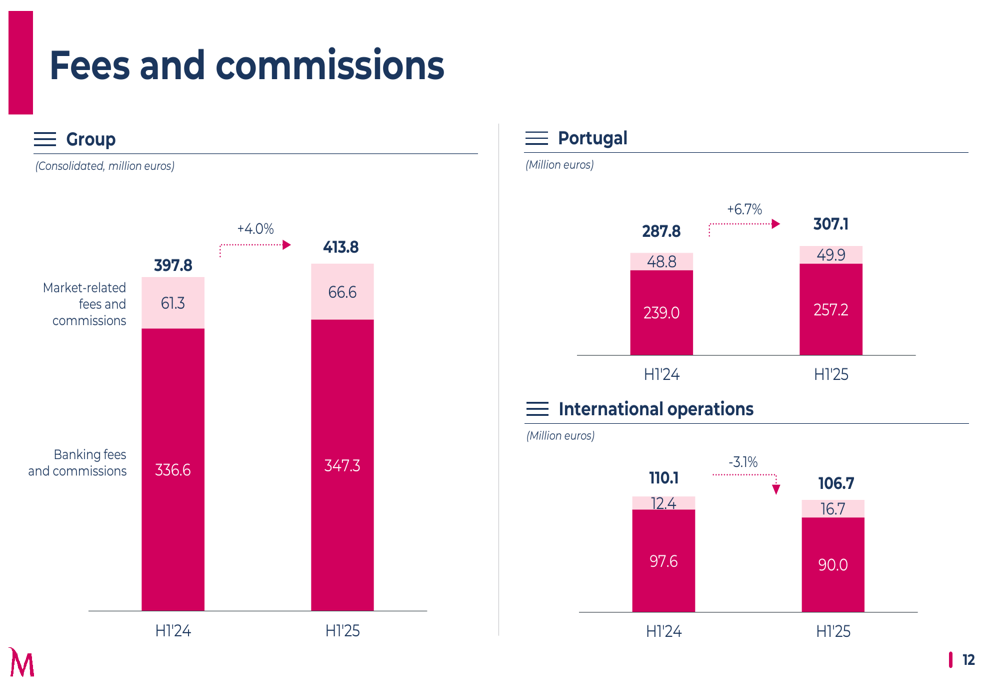

Fee and commission income showed solid growth of 4.0% to €413.8 million, driven by a 6.7% increase in Portugal to €307.1 million, which offset a 3.1% decline in international operations to €106.7 million. Banking fees and commissions rose from €336.6 million to €347.3 million, while market-related fees and commissions increased from €61.3 million to €66.6 million.

The breakdown of fee and commission income is shown here:

Other net operating income improved from -€45.9 million to -€9.9 million, benefiting from higher equity earnings and dividends (€55.8 million, up from €32.3 million) and improved net trading income (€31.8 million, up from €4 million). However, these gains were partially offset by higher other operating expenses (-€97.6 million compared to -€72.9 million).

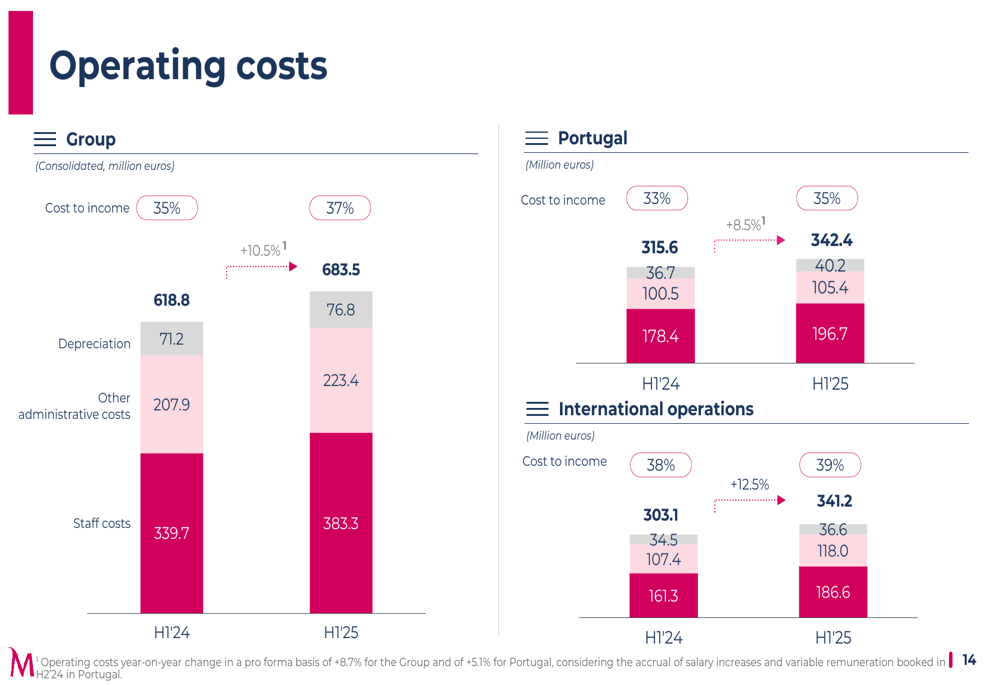

Operating costs increased 10.5% to €683.5 million, with staff costs rising from €339.7 million to €383.3 million, other administrative costs growing from €207.9 million to €223.4 million, and depreciation increasing from €71.2 million to €76.8 million. As a result, the cost-to-income ratio deteriorated from 35% to 37% at the group level.

The operating cost breakdown across regions is illustrated here:

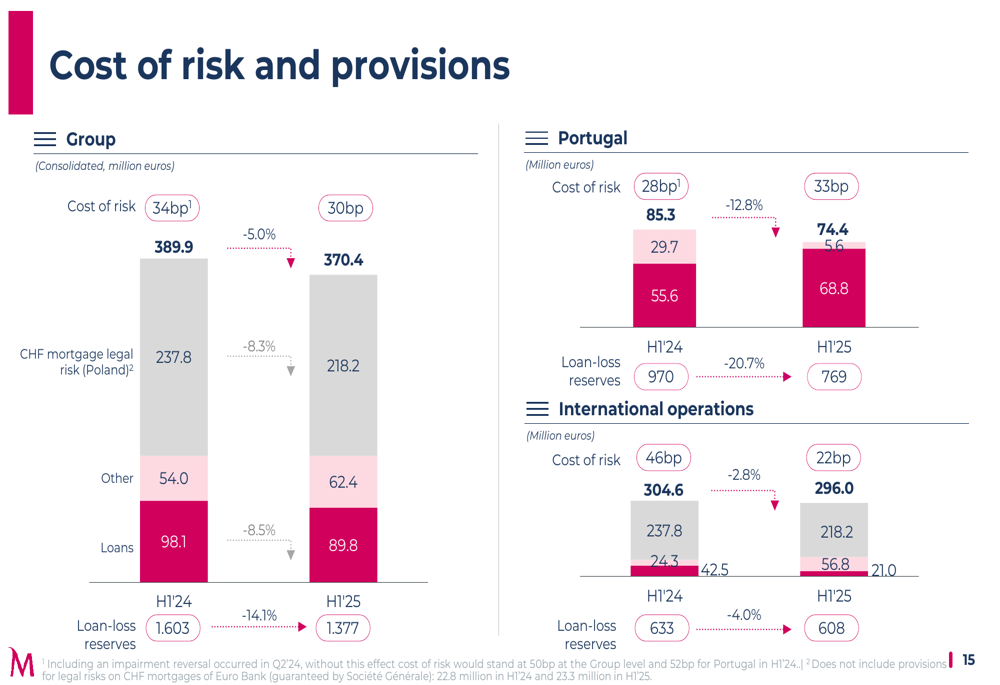

Cost of risk improved from 34bp to 30bp at the group level, with loan impairments decreasing from €98.1 million to €89.8 million. Provisions for CHF mortgage legal risk in Poland also declined from €237.8 million to €218.2 million. Loan-loss reserves decreased from €1,603 million to €1,377 million, reflecting the bank’s improved asset quality.

The following chart shows the cost of risk and provisions across regions:

Strategic Initiatives

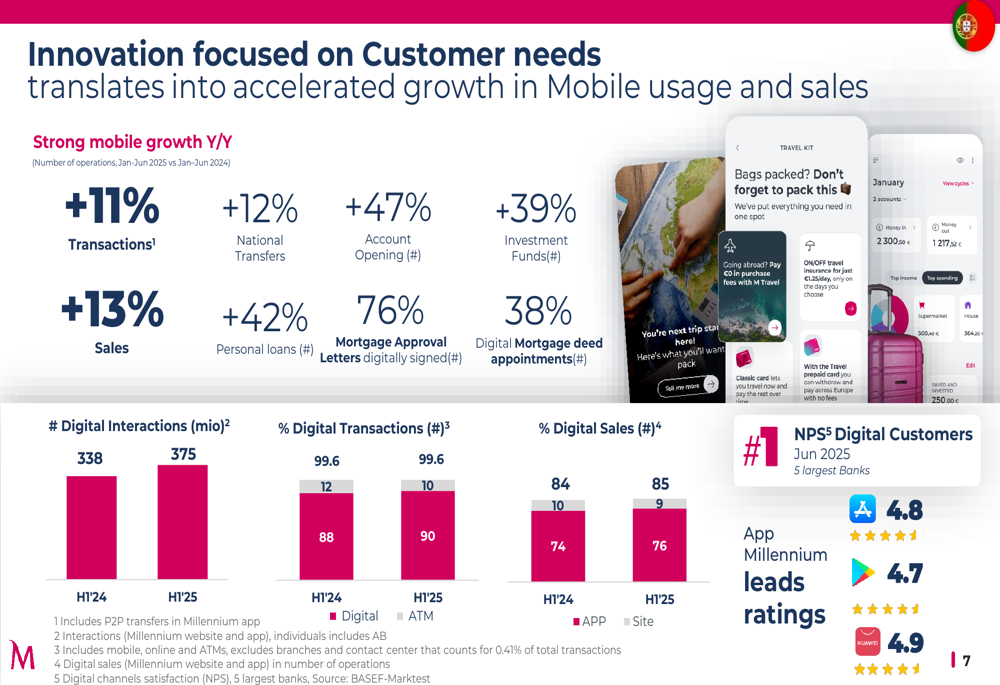

BCP continues to focus on digital transformation as a key strategic priority. The bank reported impressive growth in mobile banking usage, with transactions up 11%, sales up 13%, and national transfers up 12% year-over-year. Digital mortgage processes showed particularly strong growth, with digitally signed mortgage approval letters up 76% and digital mortgage deed appointments up 38%.

Total (EPA:TTEF) digital interactions increased from 338 million in H1 2024 to 375 million in H1 2025, with digital transactions now accounting for 99.6% of total transactions. The bank’s mobile apps maintain high customer satisfaction ratings, with the Millennium app scoring 4.7 on Android and 4.9 on HUAWEI.

The digital transformation metrics are illustrated in the following slide:

This focus on digital innovation is yielding tangible results in customer acquisition and engagement. Mobile customers now represent 73% of active customers at the group level and 65% in Portugal, up from 70% and 61% respectively in June 2024.

Forward-Looking Statements

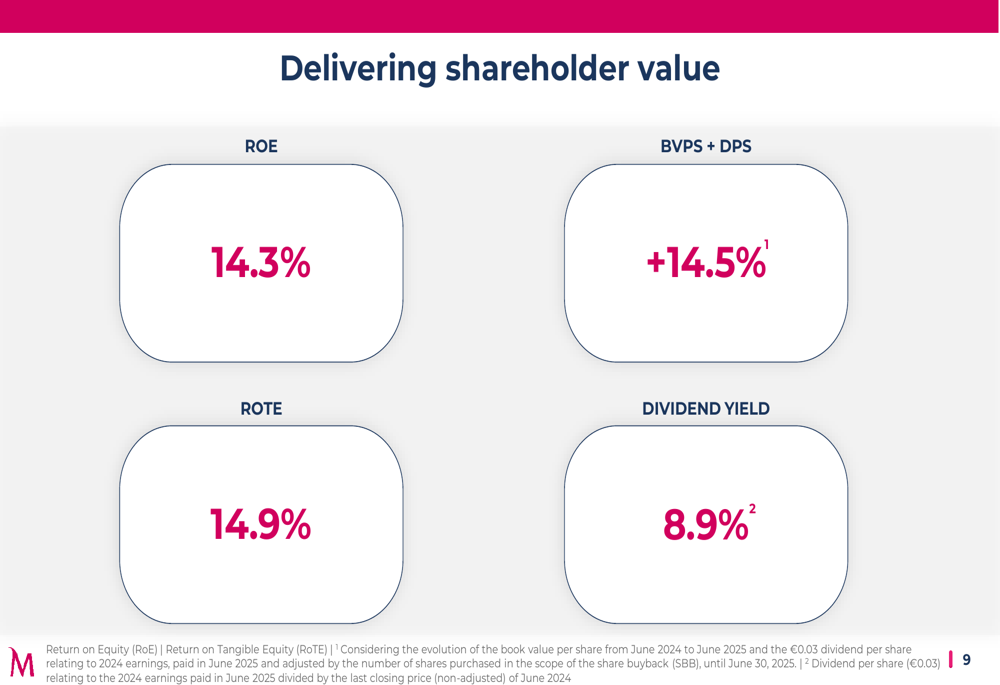

BCP is focused on delivering shareholder value, with a dividend yield of 8.9% and book value per share plus dividend per share growth of 14.5%. This aligns with statements made during the Q1 2025 earnings call, where executives emphasized their commitment to "delivering on shareholder distribution" and plans to distribute up to 75% of cumulative net income.

The bank’s shareholder value metrics are highlighted here:

Looking ahead, BCP faces both opportunities and challenges. The continued growth in digital banking and strong performance in international operations provide avenues for sustained growth. However, rising operating costs and declining net interest margins in Portugal could pressure profitability if not managed effectively.

The bank’s strong capital and liquidity positions (LCR at 336%, NSFR at 181%, and LtD at 69%) provide a solid foundation for navigating potential economic uncertainties. The reduction in non-performing assets and improved cost of risk also enhance the bank’s resilience to potential economic downturns.

BCP’s H1 2025 results demonstrate that the bank is successfully executing its strategy of digital transformation and international diversification, while maintaining a strong focus on shareholder returns. The 3.5% growth in net income, despite challenging conditions in some markets, reflects the resilience of the bank’s business model and its ability to adapt to changing market dynamics.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.