Street Calls of the Week

Introduction & Market Context

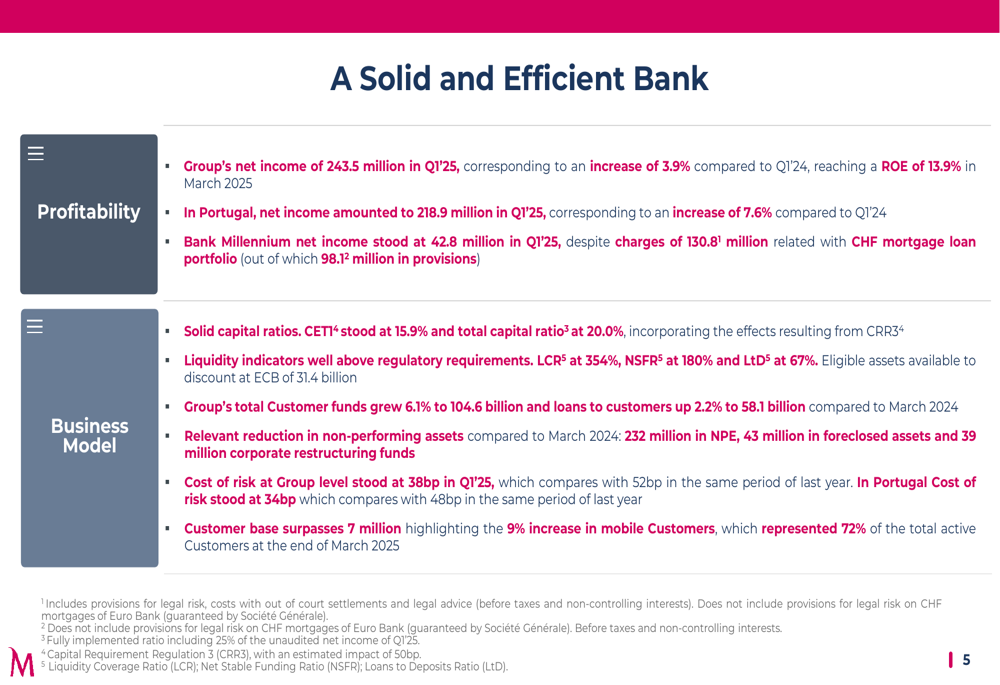

Banco Comercial Português (BCP) has released its Q1 2025 earnings presentation, reporting a 3.9% year-over-year increase in net income to €243.5 million. The results show recovery from the revenue miss experienced in Q4 2024, with the bank’s stock currently trading at €0.6622, up 1.57% in the most recent session.

The bank’s performance demonstrates resilience following last quarter’s challenges, when BCP missed revenue forecasts despite meeting EPS expectations. The Q1 results align with the bank’s previous guidance that 2025 net profit would remain consistent with 2024 levels.

Quarterly Performance Highlights

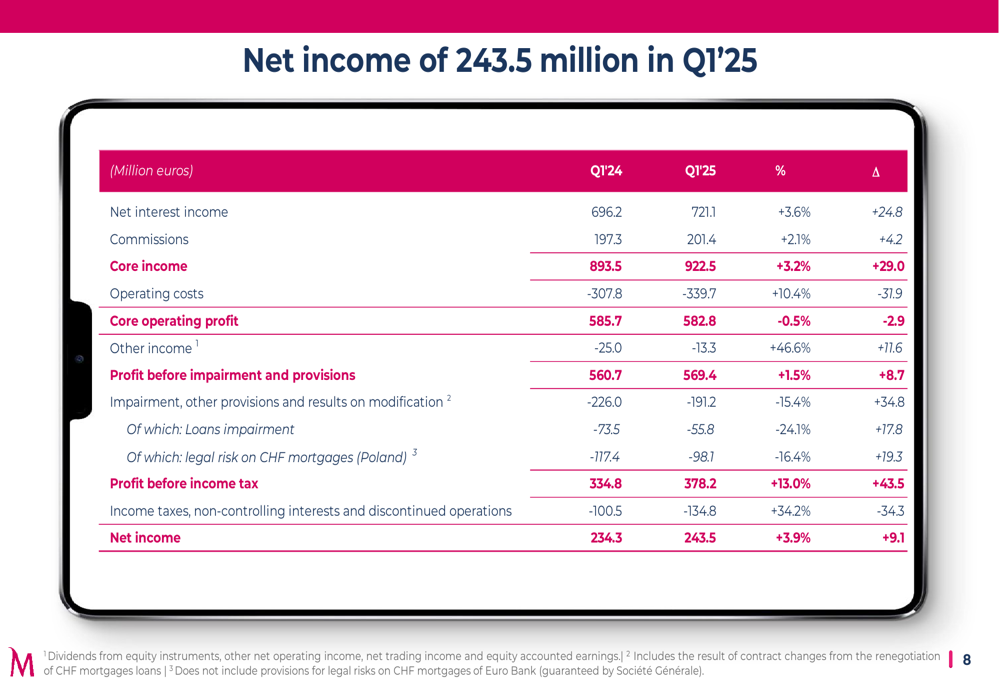

BCP reported core income of €922.5 million for Q1 2025, representing a 3.2% increase compared to the same period last year. This growth was driven by a 3.6% rise in net interest income to €721.1 million and a 2.1% increase in commissions to €201.4 million.

As shown in the following detailed breakdown of the bank’s financial performance:

Operating costs increased by 10.4% to €339.7 million, resulting in a slight 0.5% decrease in core operating profit to €582.8 million. However, profit before income tax grew by 13.0% to €378.2 million, benefiting from a 15.4% reduction in impairments and provisions.

The bank’s Portuguese operations generated €218.9 million in net income, a 7.6% increase compared to Q1 2024. Meanwhile, Bank Millennium in Poland contributed €42.8 million despite ongoing charges of €130.8 million related to its CHF mortgage loan portfolio, of which €98.1 million were provisions.

Digital Transformation Success

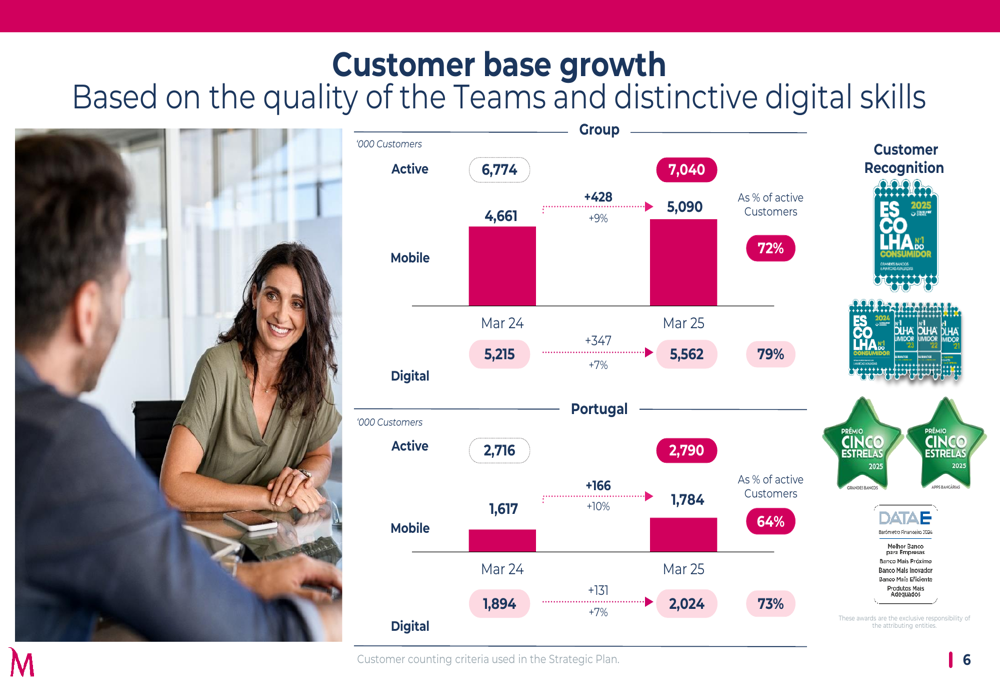

BCP’s digital transformation strategy continues to yield significant results, with the bank’s total customer base surpassing 7 million. Mobile customers increased by 9% year-over-year to 5.09 million, now representing 72% of total active customers.

The following slide illustrates the impressive growth in the bank’s customer base across both its Group operations and specifically in Portugal:

In Portugal, mobile customers grew by 10% to 1.78 million, representing 64% of active customers, while digital customers increased by 7% to 2.02 million, accounting for 73% of active customers. These gains have helped BCP earn recognition as "Consumer’s Choice 2025" and "Five Stars 2025."

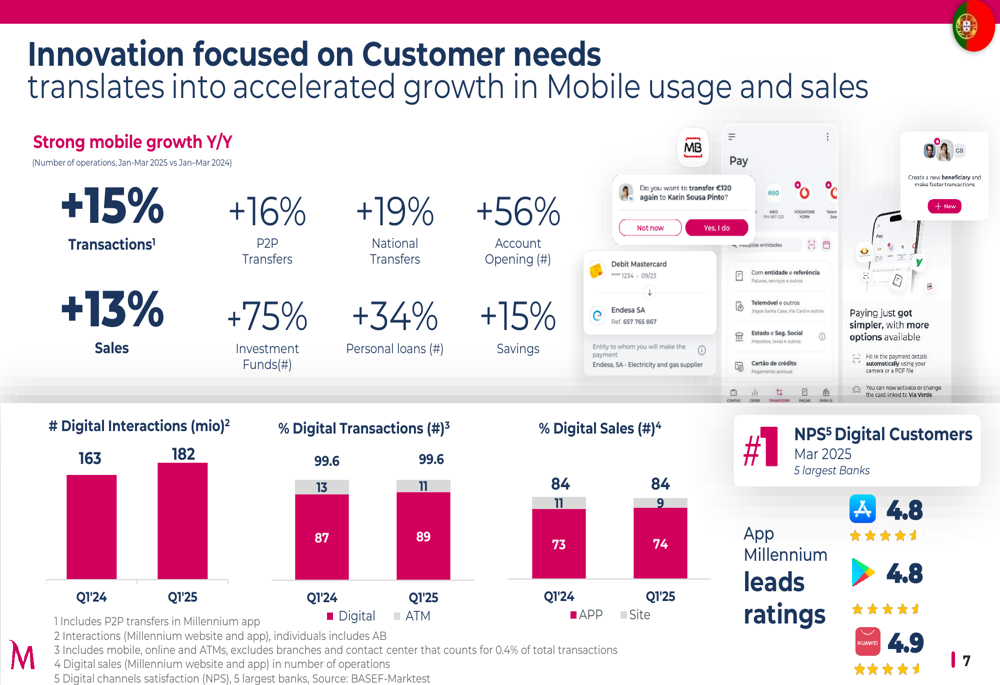

The bank’s digital initiatives have translated into accelerated transaction growth and increased digital sales, as demonstrated in this comprehensive overview:

Digital transactions increased by 15%, P2P transfers by 16%, and national transfers by 19%. Account openings through digital channels surged by 56%, while investment fund transactions increased by 75% and personal loans by 34%. The bank’s mobile app maintains high ratings of 4.8-4.9 across platforms, supporting its digital growth strategy.

Regional Performance Analysis

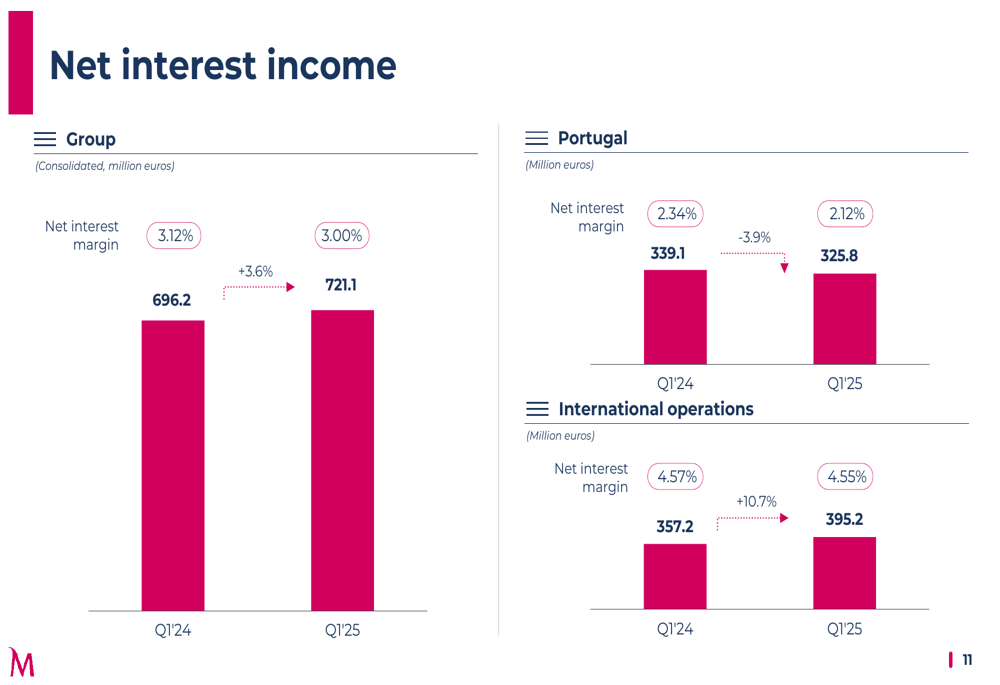

BCP’s international operations outperformed its domestic business in terms of net interest income growth. While the Group’s net interest income increased by 3.6% to €721.1 million, this growth was driven primarily by international operations, which saw a 10.7% increase to €395.2 million.

The following regional breakdown highlights this divergence in performance:

Portugal experienced a 3.9% decrease in net interest income to €325.8 million, with the net interest margin declining from 2.34% to 2.12%. In contrast, international operations maintained a strong net interest margin of 4.55%, only slightly below the 4.57% recorded in Q1 2024.

This regional disparity aligns with the challenges mentioned in the bank’s Q4 2024 earnings report, which noted economic difficulties in some international markets, particularly Mozambique. However, the strong overall international performance suggests improvements in other markets, particularly Poland.

Capital Position and Shareholder Value

BCP maintained strong capital and liquidity positions, with a CET1 ratio of 15.9% and a total capital ratio of 20.0%. These figures incorporate the effects of CRR3 regulations and remain robust despite being slightly below the 16.3% CET1 ratio reported at the end of 2024.

The bank’s liquidity indicators significantly exceed regulatory requirements, with a Liquidity Coverage Ratio (LCR) of 354%, a Net Stable Funding Ratio (NSFR) of 180%, and a Loan-to-Deposit ratio (LtD) of 67%. Eligible assets available for discount at the ECB amount to €31.4 billion.

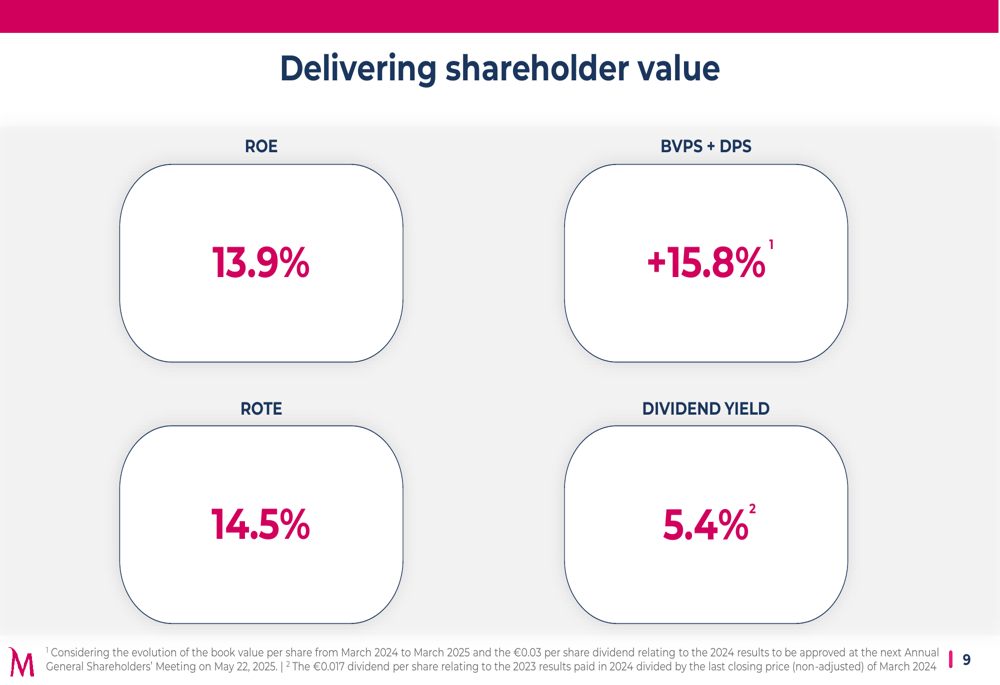

As illustrated in this key performance indicator summary:

BCP continues to deliver strong shareholder value, achieving a Return on Equity (ROE) of 13.9% and a Return on Tangible Equity (ROTE) of 14.5%. The bank’s book value per share plus dividends per share increased by 15.8%, while offering a dividend yield of 5.4%.

Asset quality improved significantly, with reductions in non-performing exposures (NPEs), foreclosed assets, and corporate restructuring funds compared to March 2024. The cost of risk at the Group level improved to 38 basis points in Q1 2025, down from 52 basis points in the same period last year.

Forward Outlook

Based on the Q1 2025 results, BCP appears on track to meet its previous guidance of maintaining profit levels similar to 2024. The continued growth in digital adoption and customer base expansion supports the bank’s strategic focus on digital transformation.

The bank’s solid capital position and improved asset quality provide a strong foundation for sustainable growth, while the dividend yield of 5.4% offers attractive returns for shareholders. However, the divergence between domestic and international performance suggests that regional economic conditions will continue to influence overall results.

The 10.4% increase in operating costs bears monitoring, as it could pressure margins if revenue growth doesn’t keep pace. Additionally, while provisions for CHF mortgage loans in Poland have decreased, they continue to represent a significant drag on the bank’s Polish operations.

Overall, BCP’s Q1 2025 presentation depicts a bank successfully balancing growth initiatives with prudent risk management, while delivering value to shareholders despite challenging economic conditions in some of its markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.