One & One Green Technologies stock soars 100% after IPO debut

Introduction & Market Context

Banco de Chile (NYSE:CHILE) presented its second quarter 2025 earnings results on August 6, 2025, showcasing the bank’s performance in a gradually improving Chilean economic environment. Despite slightly missing analyst expectations with EPS of $3.02 (below the forecast of $3.08) and revenue of $762.56 billion (versus expected $770.74 billion), the bank maintained its position as one of the most profitable financial institutions in Chile.

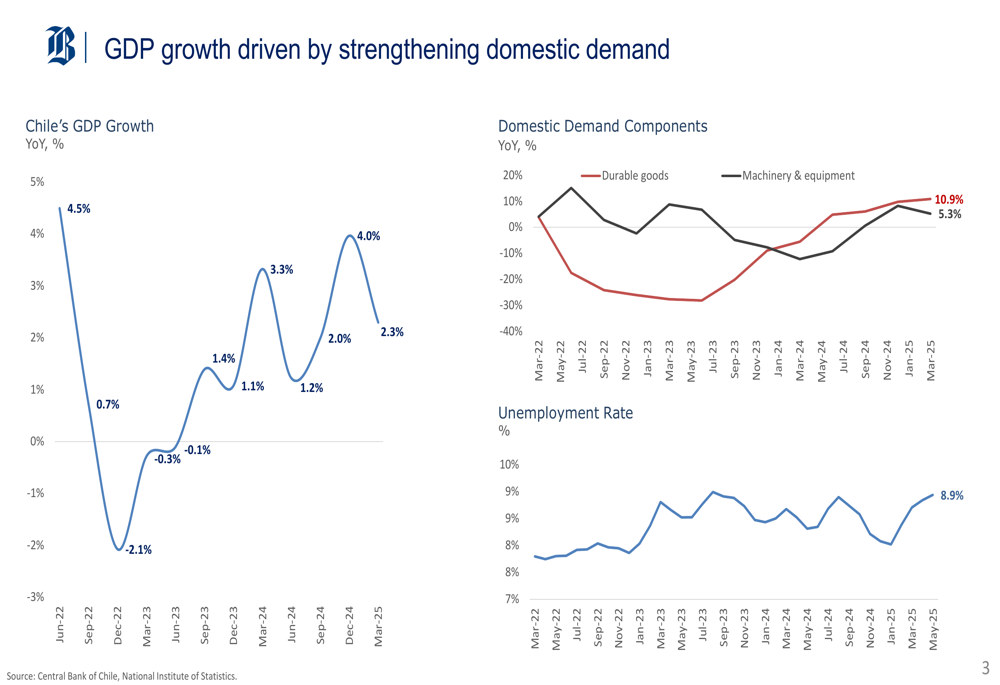

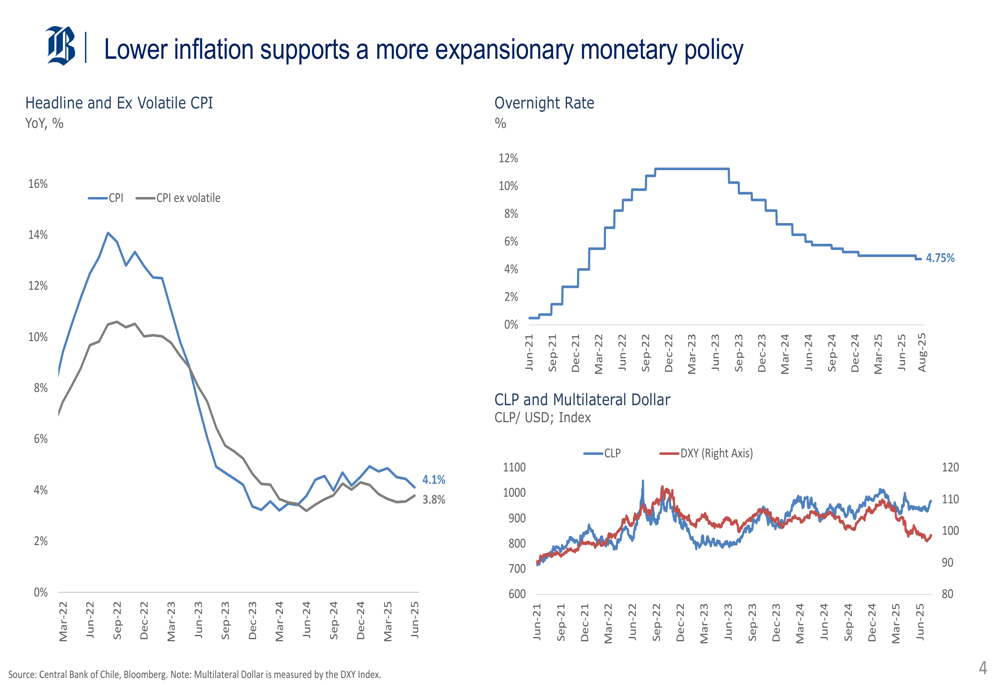

The presentation highlighted Chile’s economic recovery, with GDP growth reaching 2.3% in March 2025, supported by strengthening domestic demand. Inflation has continued its downward trend, with the Consumer Price Index decreasing to 4.1% from previous highs of 14%.

As shown in the following chart of Chile’s GDP growth and unemployment rate, the economy has been gradually recovering despite ongoing challenges:

The monetary policy environment has become more favorable for banking operations, with the overnight rate decreasing to 4.75% by August 2025 from a peak of 11%. This trend, coupled with moderating inflation, creates a more stable operating environment for financial institutions.

The following chart illustrates the inflation trends and monetary policy shifts in Chile:

Quarterly Performance Highlights

Banco de Chile reported a net income of 1,430 billion CLP for Q2 2025, maintaining a Return on Average Equity (ROAE) of 16.3%. While these figures represent solid performance, they fell slightly short of analyst expectations, leading to a 1.84% decline in the bank’s stock price following the announcement.

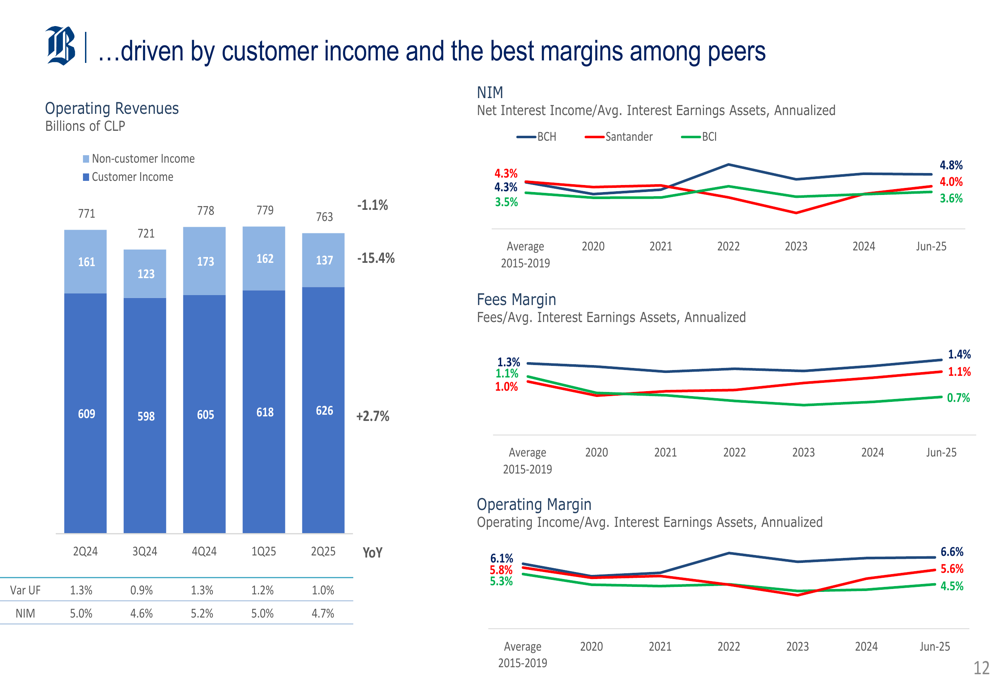

The bank’s customer income showed positive momentum, increasing over time and contributing to stable operating revenues. This performance is particularly noteworthy given the challenging economic conditions Chile has faced in recent years.

The following chart demonstrates Banco de Chile’s customer income and margin analysis compared to competitors:

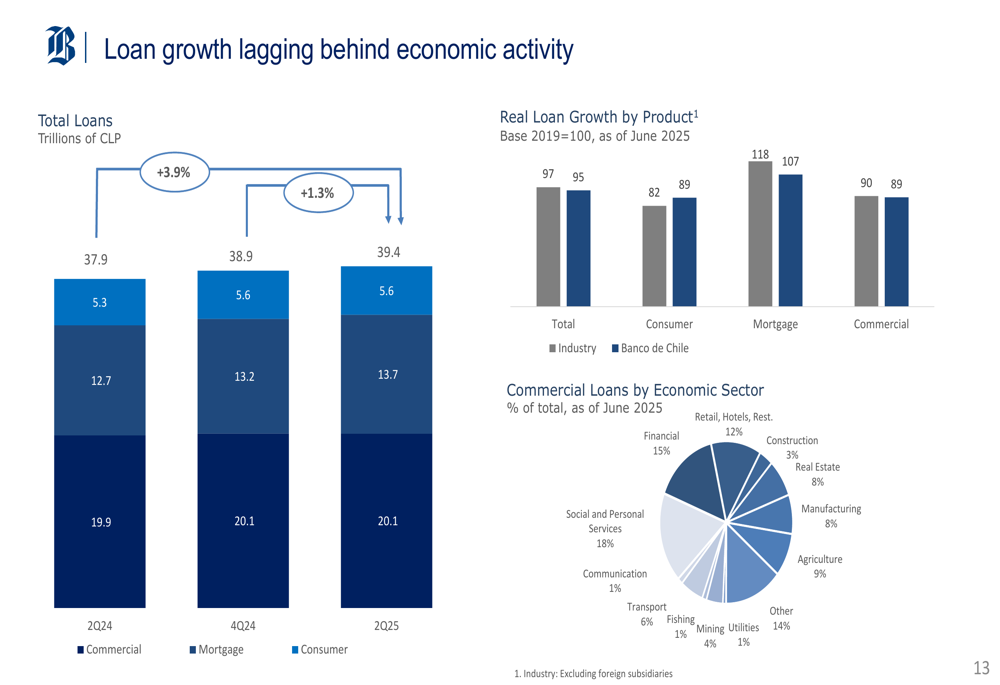

Banco de Chile’s loan portfolio reached 39.4 trillion CLP in Q2 2025, with commercial loans accounting for approximately 50% of the total. The bank’s commercial loan portfolio remains well-diversified across economic sectors, with significant exposure to social and personal services (18%), financial services (15%), and retail, hotels, and restaurants (12%).

The following chart shows the bank’s loan growth and portfolio composition:

Competitive Industry Position

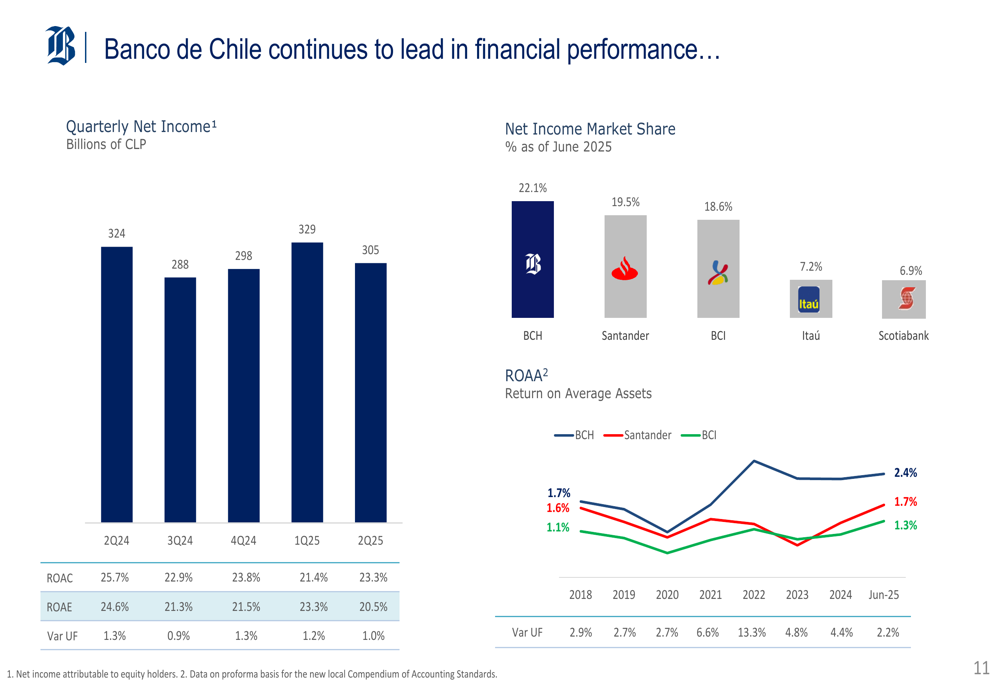

Despite the slight earnings miss, Banco de Chile maintained its leadership position in the Chilean banking sector. The bank holds a 22.1% market share of net income as of June 2025, ahead of competitors Santander (BME:SAN) (19.5%) and BCI (18.6%). This dominant position reflects the bank’s strong operational efficiency and robust business model.

The following chart illustrates Banco de Chile’s financial performance leadership in the industry:

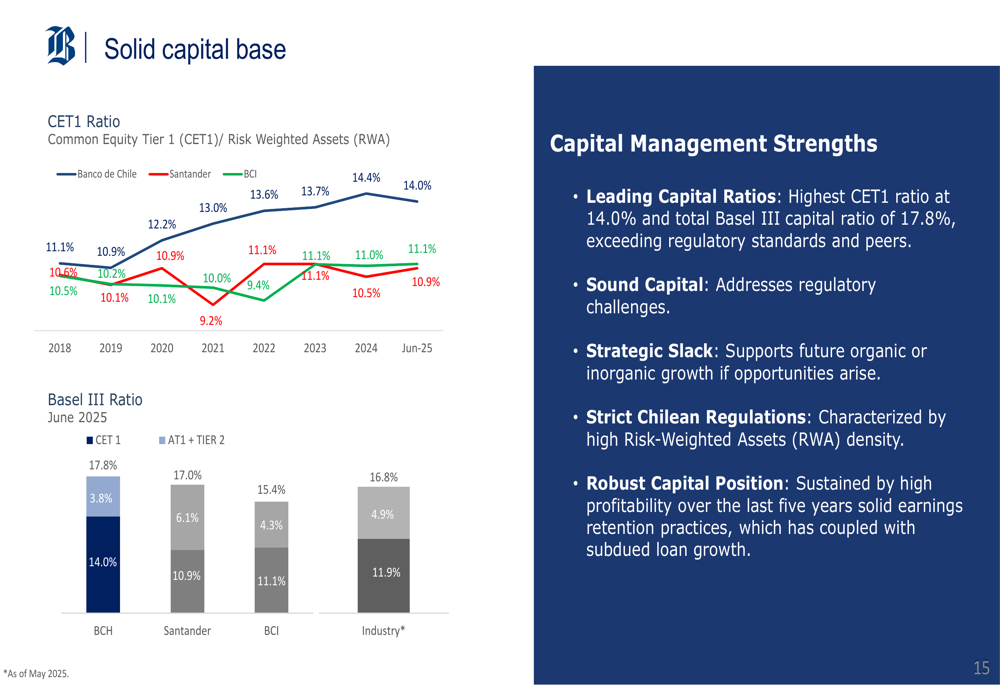

Banco de Chile’s capital position remains exceptionally strong, with the highest Common Equity Tier 1 (CET1) ratio among peers at 14.0% and a total Basel III capital ratio of 17.8%. This robust capital base exceeds regulatory requirements and provides strategic flexibility for future growth opportunities.

As shown in the following capital base analysis, Banco de Chile maintains a significant advantage over competitors:

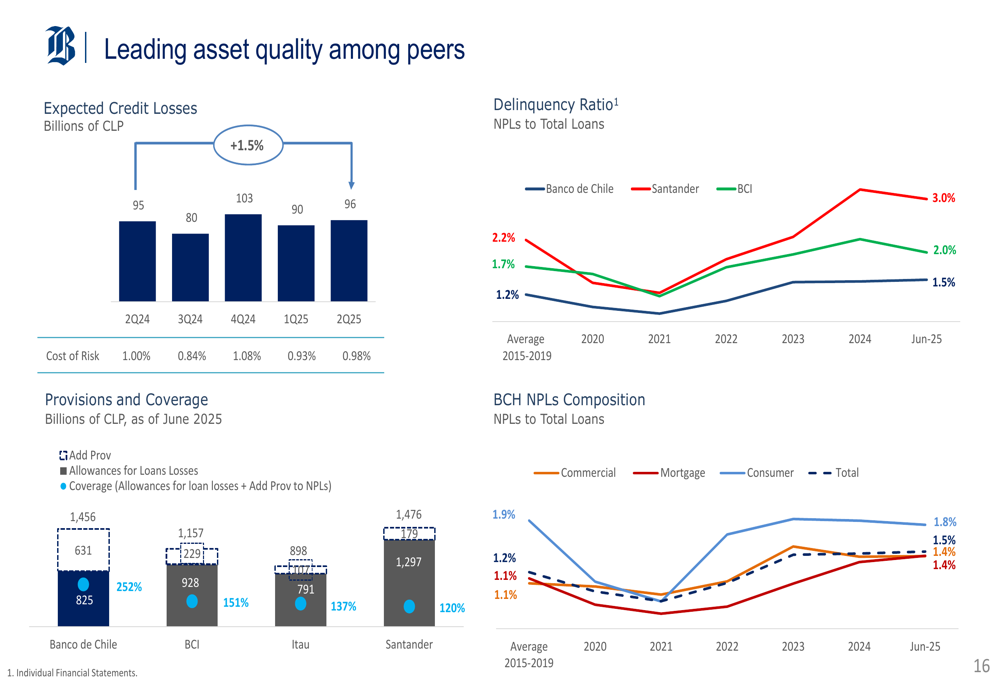

The bank also demonstrated superior asset quality compared to peers, with a non-performing loan (NPL) ratio of 2.4% and a coverage ratio of 148% as of Q2 2025. This strong asset quality position reflects the bank’s prudent risk management practices and selective lending approach.

The following chart shows Banco de Chile’s asset quality metrics compared to competitors:

Strategic Initiatives

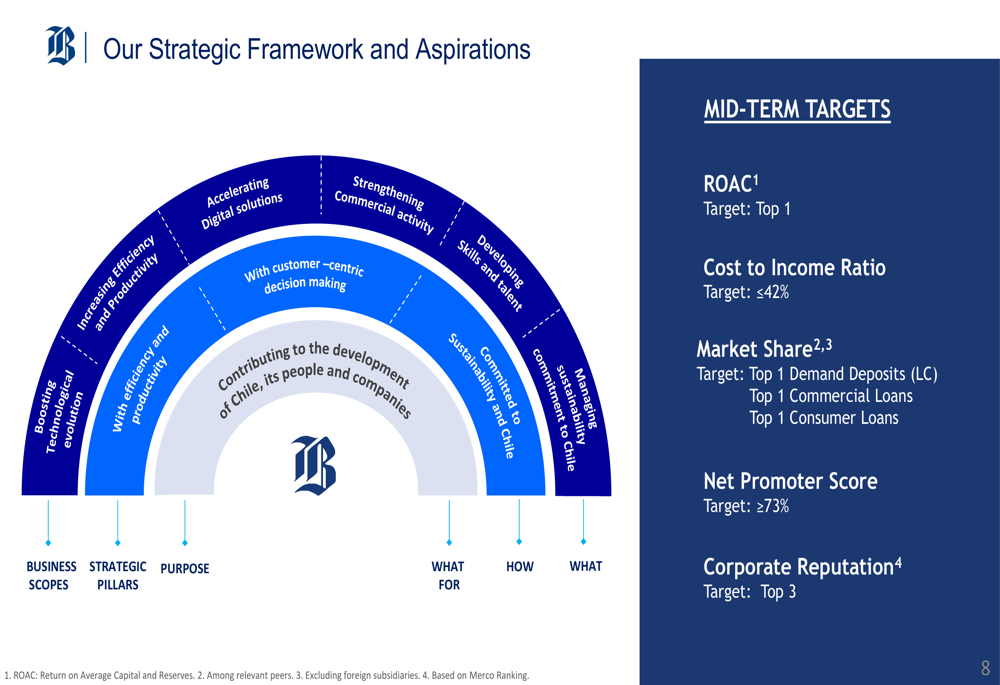

Banco de Chile outlined its strategic framework and aspirations, focusing on technological evolution, efficiency and productivity improvements, digital solutions, commercial activity strengthening, talent development, and sustainability initiatives. The bank has set ambitious mid-term targets, including maintaining top positions in demand deposits, commercial loans, and consumer loans.

The strategic framework is illustrated in the following diagram:

Key business advances highlighted in the presentation include the implementation of new digital functionalities, the placement of a social bond in Switzerland for US$122 million, participation in the FOGAES state-guaranteed credit program, integration of debt collections, productivity improvements, expansion of FAN digital accounts, deployment of AI virtual assistants, and technology cost savings initiatives.

The bank reported a 30% increase in cross-selling to current accounts, credit cards, and microloans for FAN customers, demonstrating the success of its digital strategy. These initiatives align with the bank’s focus on enhancing customer experience while improving operational efficiency.

Economic Outlook

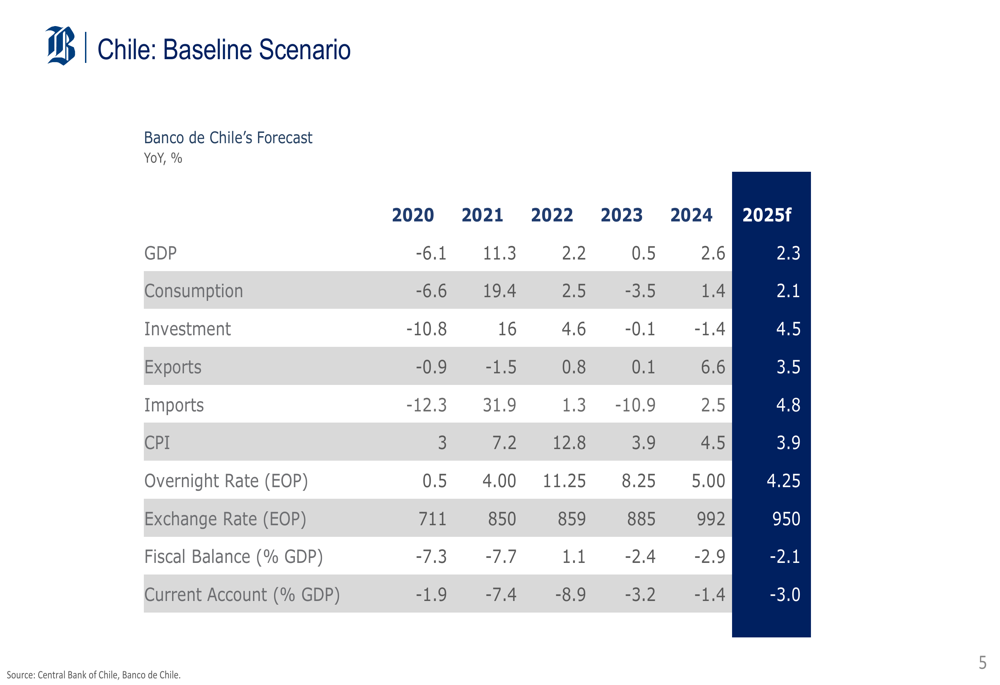

Banco de Chile has revised its GDP growth forecast for 2025 upward to 2.3% from the previous estimate of 2.0%. The bank’s baseline economic scenario presents a cautiously optimistic outlook for Chile, with projected improvements in consumption, investment, and exports.

The following table details Banco de Chile’s baseline economic scenario forecast:

The bank expects inflation to moderate to 3.9% in 2025, with the overnight rate projected to decrease to 4.25% by the end of the year. These projections suggest a more favorable operating environment for the banking sector, potentially supporting loan growth and asset quality.

Forward-Looking Statements

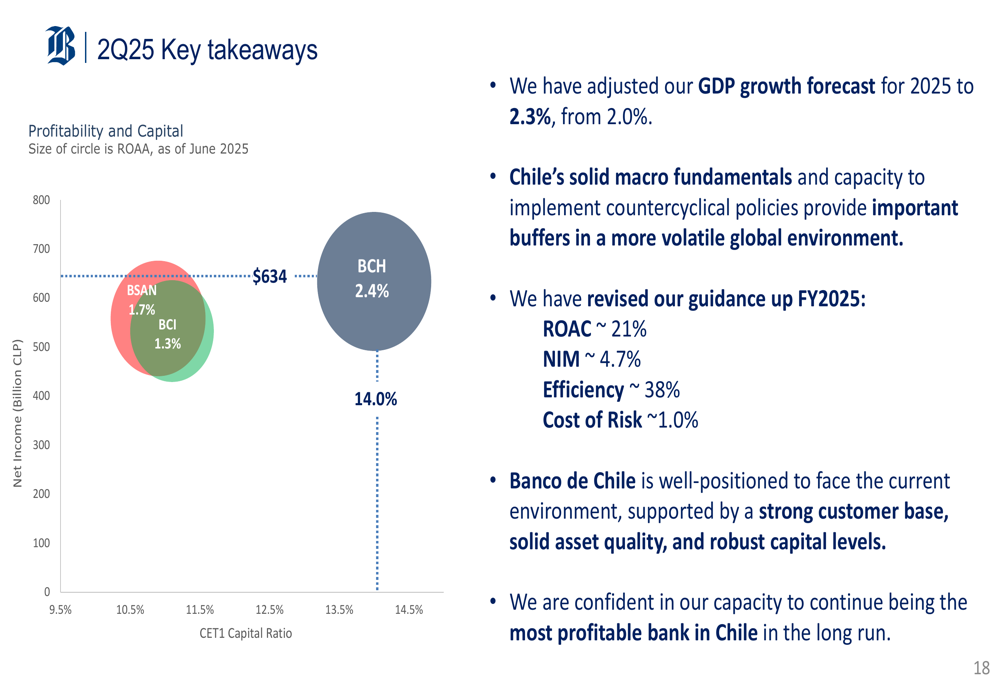

Banco de Chile has updated its guidance for FY2025, projecting a Return on Average Capital (ROAC) of approximately 21%, a Net Interest Margin (NIM) of around 4.7%, an efficiency ratio of approximately 38%, and a cost of risk of about 1.0%. These projections reflect the bank’s confidence in its ability to maintain strong profitability despite economic challenges.

The following slide summarizes the key takeaways and forward-looking statements from the presentation:

The bank emphasized its strong positioning to face the current environment, supported by a solid customer base, robust asset quality, and strong capital levels. Management expressed confidence in Banco de Chile’s capacity to continue being the most profitable bank in Chile over the long term.

Despite the slight earnings miss in Q2 2025, Banco de Chile’s presentation highlighted the bank’s resilience and strategic focus on digital transformation, operational efficiency, and customer-centric initiatives. These factors, combined with the bank’s strong capital position and market leadership, position Banco de Chile favorably for continued success in an evolving economic landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.