Gold rally may be losing steam but no major correction seen: DB

Introduction & Market Context

Bang & Olufsen (CPH:BO) shares fell 7.51% to DKK 12.56 following the release of its Q1 2025/26 results on October 9, 2025, despite the luxury audio manufacturer reporting a record gross margin. The company’s presentation revealed a complex quarter marked by channel inventory adjustments that impacted revenue, even as direct retail channels showed positive growth.

The Danish audio brand maintained its full-year outlook despite the challenging start to the fiscal year, signaling confidence in its strategic direction as it approaches its centenary. This comes against a backdrop of continued macroeconomic uncertainty and shifting inventory strategies among retail partners.

Quarterly Performance Highlights

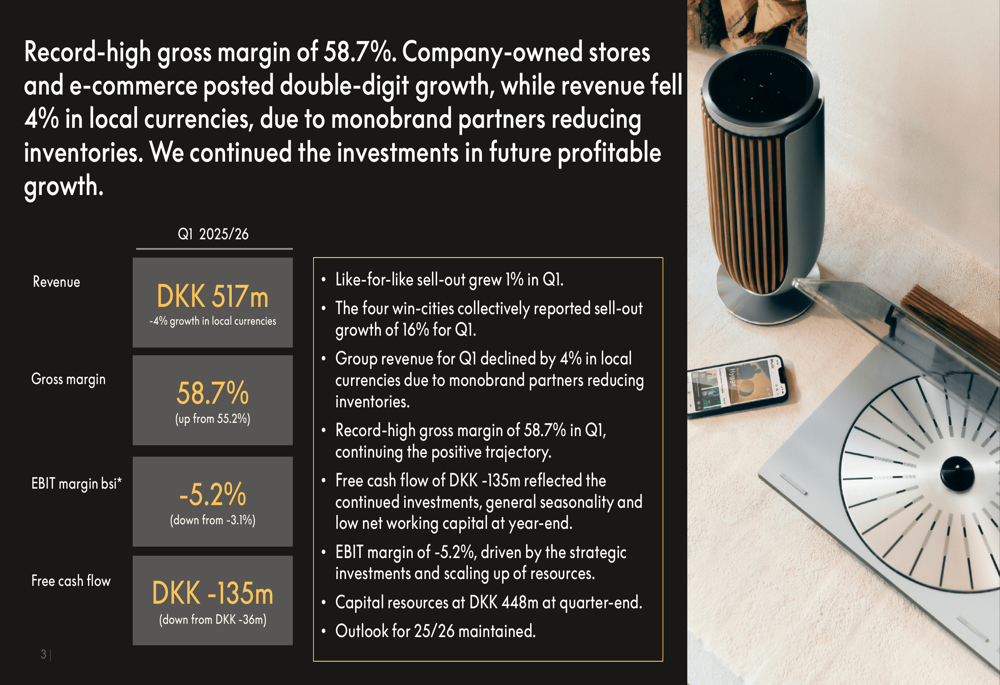

Bang & Olufsen reported Q1 2025/26 revenue of DKK 517 million, representing a 4% decline in local currencies compared to the same period last year. Despite this top-line challenge, the company achieved a record gross margin of 58.7%, up significantly from 55.2% in the prior year. EBIT margin before special items deteriorated to -5.2% from -3.1% a year earlier, while free cash flow declined to DKK -135 million from DKK -36 million.

As shown in the following comprehensive financial overview:

The company noted that like-for-like sell-out grew 1% in Q1, with particularly strong performance in its strategic "win-cities" which collectively reported 16% sell-out growth. This disconnect between sell-out growth and revenue decline highlights the impact of inventory adjustments in the monobrand partner channel.

Regional performance varied significantly, with Americas showing the strongest sell-out growth at 18%, followed by APAC at 5%, while EMEA declined by 5%. The company’s four designated win-cities outperformed the broader market with their collective 16% growth.

The following chart illustrates the regional sell-out performance:

Detailed Financial Analysis

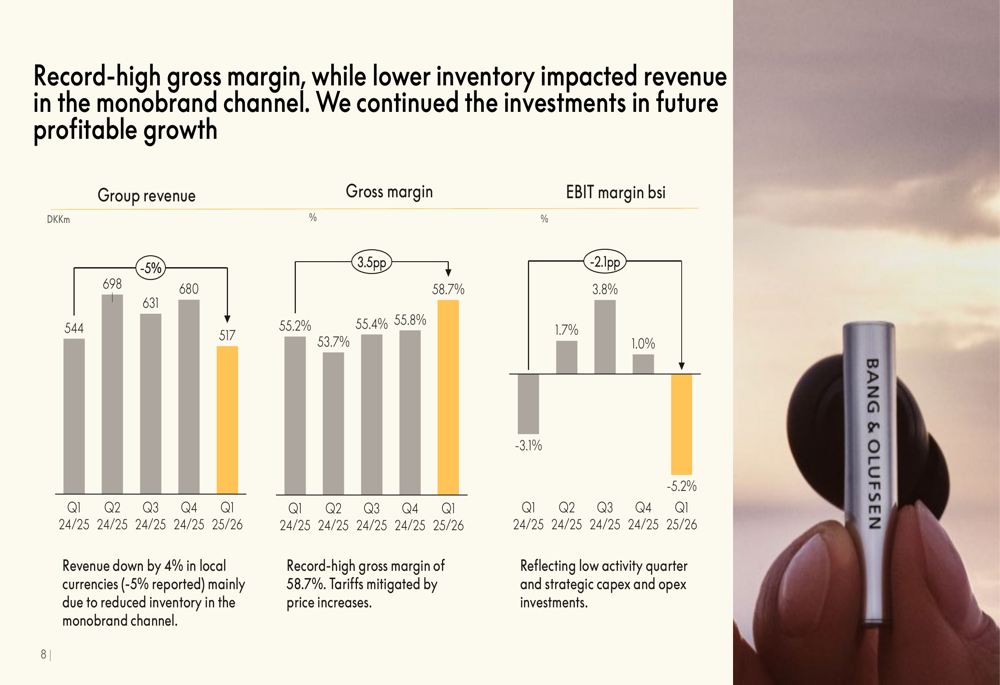

Bang & Olufsen’s financial metrics reveal a company in transition, with investments in future growth temporarily impacting profitability. The revenue decline of 4% in local currencies (-5% reported) was primarily attributed to reduced inventory in the monobrand channel, even as company-owned stores and e-commerce grew.

The following chart shows the quarterly progression of revenue, gross margin, and EBIT margin:

The record-high gross margin of 58.7% represents a continuation of positive trajectory over five consecutive quarters, demonstrating the company’s ability to maintain pricing power and manage costs effectively. The company noted that it has successfully mitigated tariff impacts through price increases.

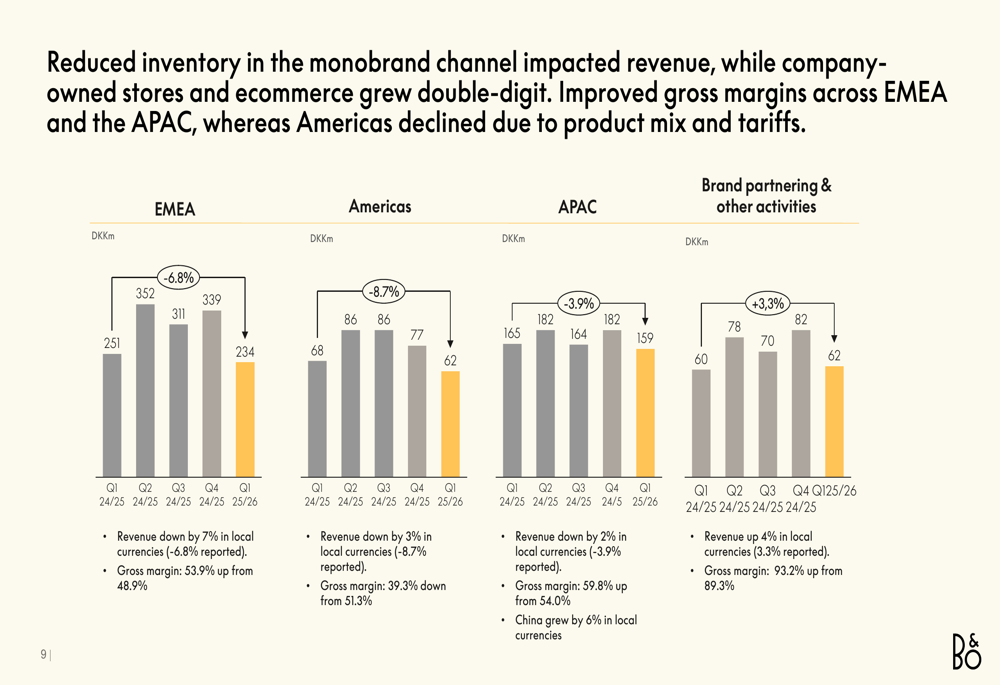

Regional revenue breakdown reveals challenges across all major markets:

EMEA revenue declined by 7% in local currencies, though gross margin improved to 53.9% from 48.9%. Americas saw a 3% revenue decline in local currencies, with gross margin falling to 39.3% from 51.3% due to product mix and tariffs. APAC revenue decreased by 2% in local currencies, though China grew by 6%. Brand partnering activities provided a bright spot with 4% revenue growth and an impressive 93.2% gross margin.

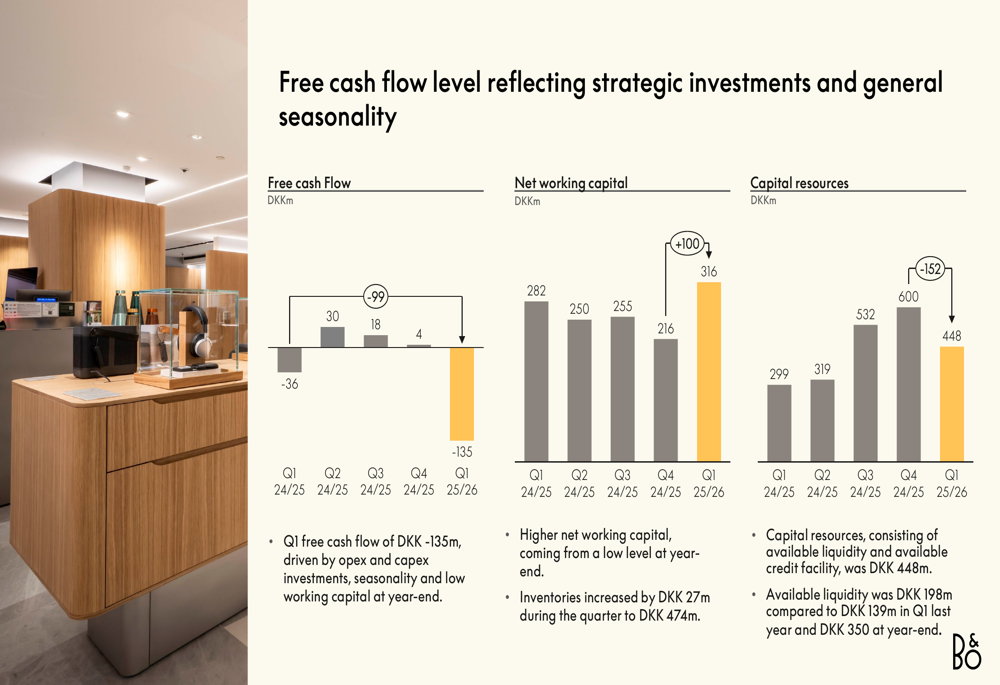

The company’s cash position and working capital also reflected the transitional quarter:

Free cash flow of DKK -135 million reflected continued investments, general seasonality, and low working capital at year-end. Net working capital increased to DKK 316 million from DKK 216 million at year-end, with inventories rising by DKK 27 million during the quarter to DKK 474 million. Capital resources stood at DKK 448 million at quarter-end.

Strategic Initiatives

Bang & Olufsen continues to position itself at the intersection of luxury, timeless design, and technology. The company announced the launch of new earpieces, Beo Grace, in September, and highlighted ongoing store openings, relocations, and upgrades in preparation for this product launch.

The company’s strategic focus on win-cities appears to be yielding results, with 16% sell-out growth across these locations. This targeted approach allows Bang & Olufsen to concentrate resources in high-potential urban markets.

Forward-Looking Statements

Despite the challenging Q1 results, Bang & Olufsen maintained its full-year outlook for 2025/26:

The company continues to project revenue growth of 1% to 8% in local currencies for the full year, with an EBIT margin before special items between -3% and 1%. Free cash flow is expected to range from DKK -100 million to 0 million.

Capital expenditure is anticipated to be around DKK 320-360 million, while capacity costs are projected to increase by approximately DKK 150 million in 2025/26, reflecting the company’s continued investment in growth initiatives.

The maintained guidance suggests management expects improved performance in subsequent quarters to offset the weak start to the fiscal year. This outlook comes as Bang & Olufsen prepares for its 100-year anniversary, a milestone that could provide marketing opportunities and heightened brand visibility in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.