Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

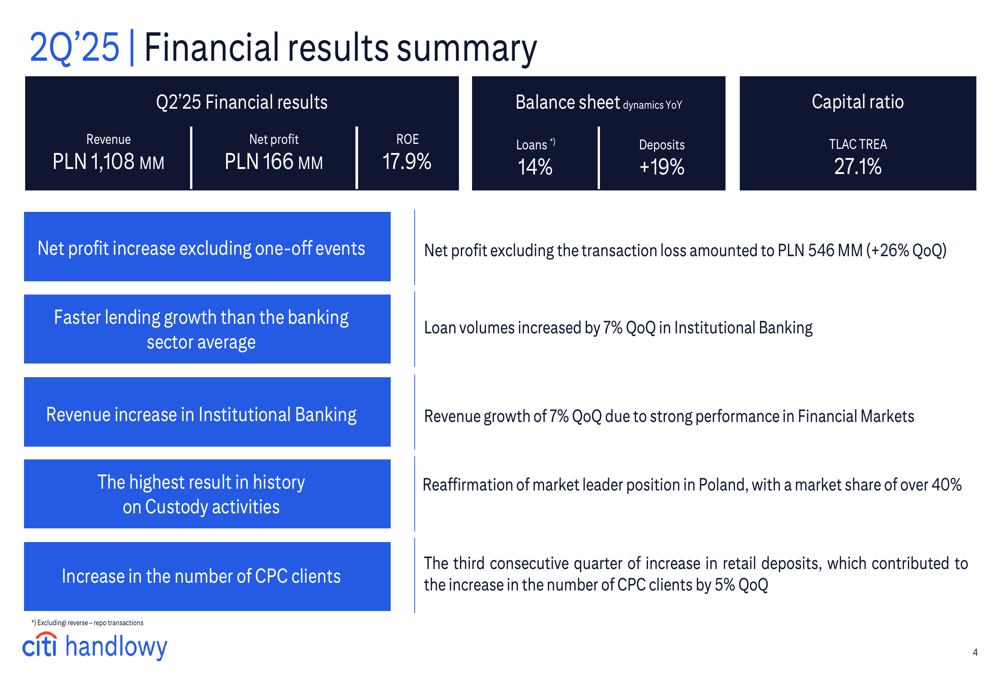

Bank Handlowy w Warszawie S.A. (BHW) presented its second quarter 2025 earnings results on August 28, revealing a strategic transformation toward becoming a "Bank for Global Business" while exiting its Consumer Banking operations. The bank reported a net profit of PLN 166 million with a return on equity of 17.9%, despite absorbing costs related to the Consumer Banking exit.

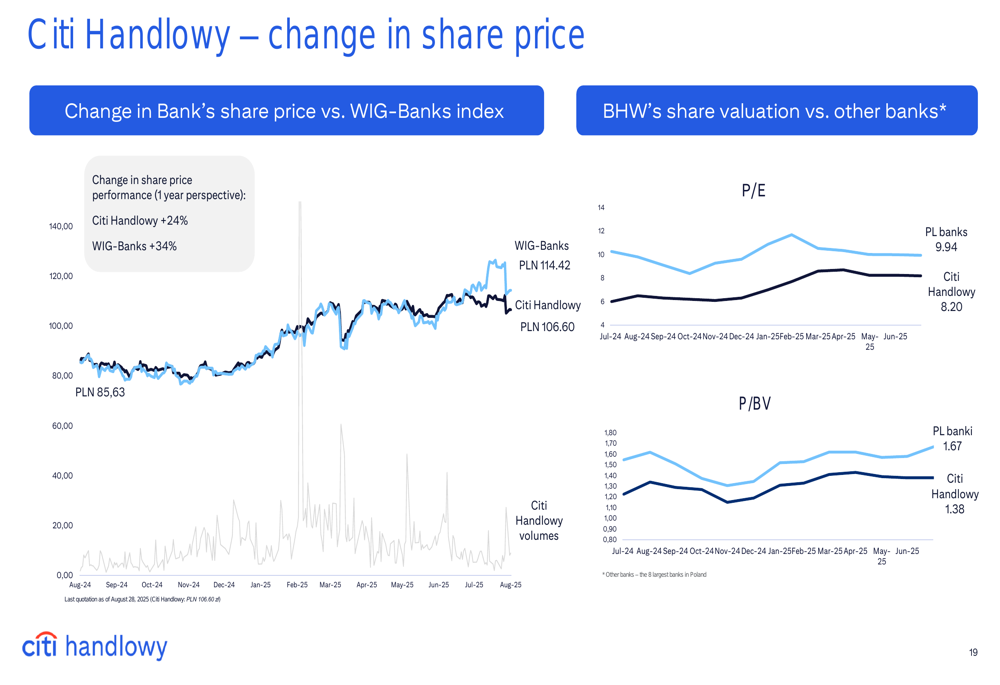

The bank’s shares have risen 24% year-to-date, underperforming the broader WIG-Banks index which gained 34% during the same period. Trading at a P/E ratio of 8.20 and P/BV of 1.38, Bank Handlowy remains valued below the Polish banking sector averages of 9.94 and 1.67 respectively.

Strategic Initiatives

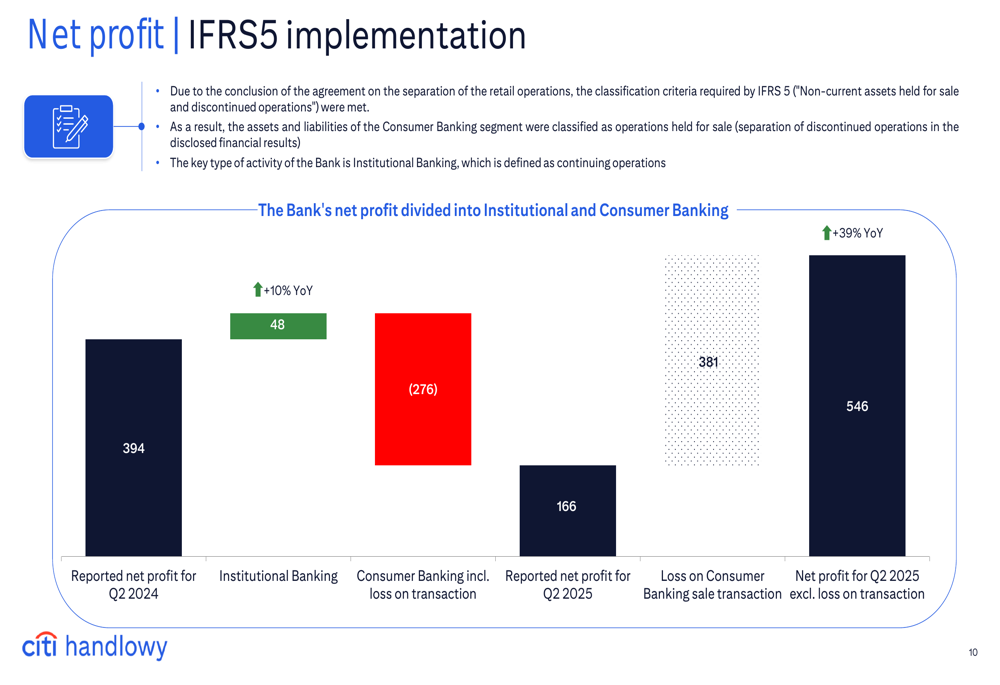

Bank Handlowy’s most significant strategic development is its planned exit from Consumer Banking, with operations scheduled to transfer to a buyer in the first half of 2026, pending regulatory approvals. The bank has implemented IFRS 5 accounting standards for the first time, classifying Consumer Banking as discontinued operations.

As shown in the following strategic overview, the bank is repositioning itself as a specialized institution focused on global business clients:

The new strategy centers on three core growth segments within Institutional Banking:

1. Financial Markets - focusing on client FX and brokerage activities, as well as interbank operations

2. Transaction and Custody activities - providing liquidity management, payments, trade finance, and custody services

3. Relationship Banking - offering comprehensive financing and investment banking services

This strategic pivot leverages the bank’s institutional strengths, with the presentation highlighting that Institutional Banking provides "a solid foundation for growth."

Quarterly Performance Highlights

Despite the transition costs, Bank Handlowy delivered solid financial results in Q2 2025. The bank’s net profit excluding the Consumer Banking transaction loss amounted to PLN 546 million, representing a 26% increase quarter-over-quarter.

The comprehensive financial summary reveals strong growth metrics across key areas:

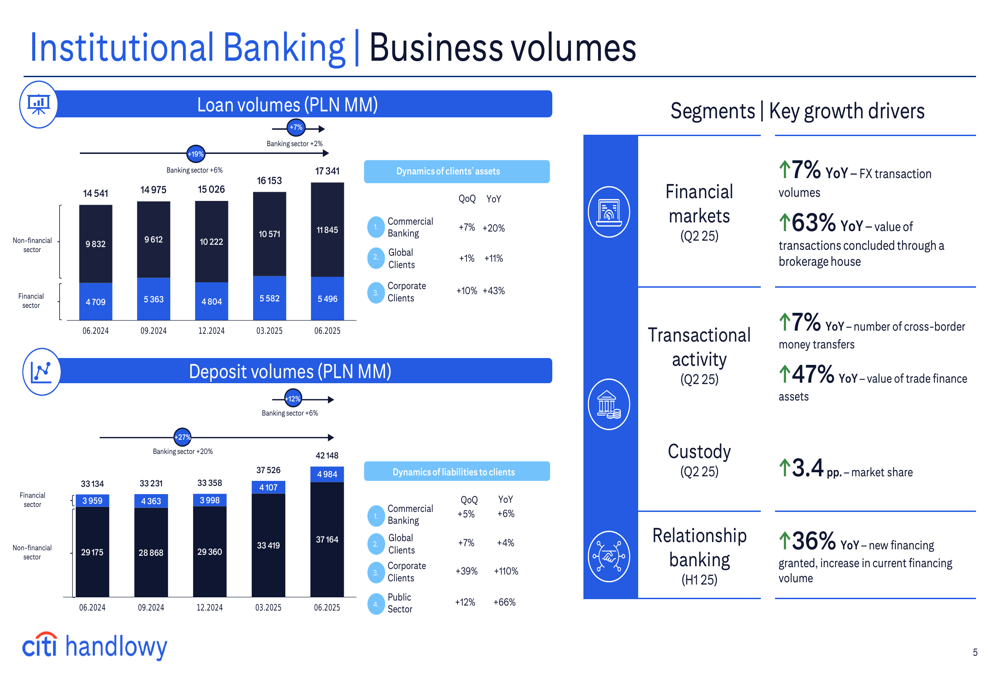

Institutional Banking emerged as the primary growth driver, with loan volumes increasing by 7% quarter-over-quarter and 19% year-over-year, outpacing the banking sector average. Total revenues reached PLN 1,108 million, with Institutional Banking revenues growing 7% quarter-over-quarter due to particularly strong performance in Financial Markets.

The bank’s business volumes show consistent growth trends in both loans and deposits:

Detailed Financial Analysis

The bank’s implementation of IFRS 5 accounting standards has significantly impacted financial reporting, with Consumer Banking now classified as discontinued operations. This accounting change provides greater transparency into the performance of continuing operations while isolating the impact of the Consumer Banking exit.

The following chart illustrates how the bank’s net profit breaks down between continuing operations and the transaction loss:

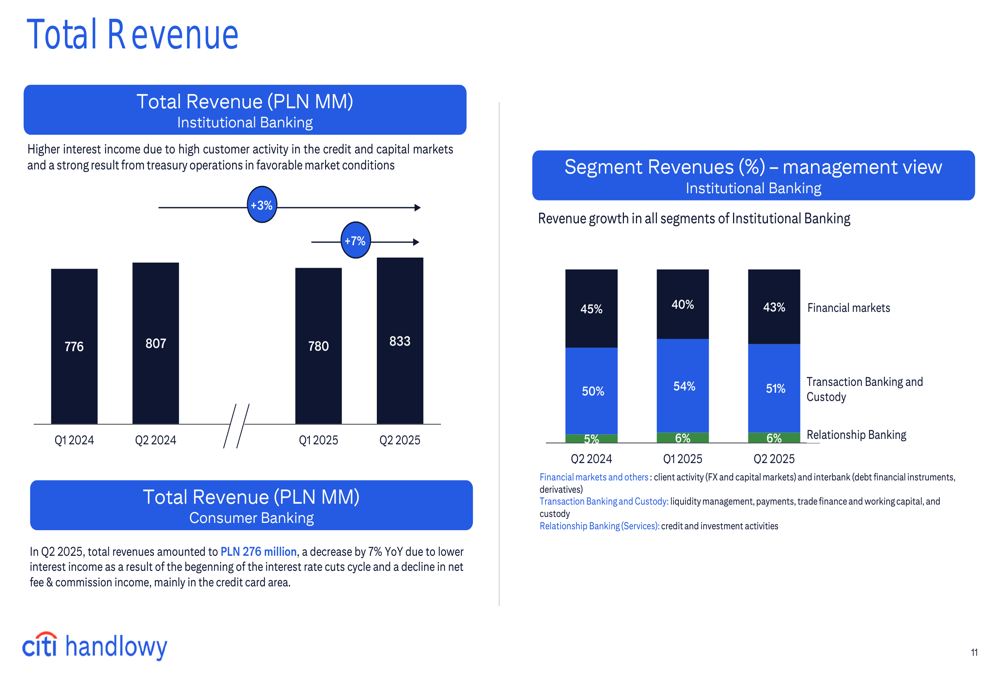

Revenue analysis shows that Institutional Banking continues to strengthen, with total revenue reaching PLN 833 million in Q2 2025. The segment revenue breakdown reveals that Transaction Banking and Custody activities contribute 50% of institutional revenues, followed by Financial Markets at 45%, and Relationship Banking at 5%.

The bank maintains a strong capital position with a TLAC TREA ratio of 27.1%, providing substantial flexibility for future growth and shareholder returns.

Competitive Industry Position

Bank Handlowy has reinforced its market leadership in several key areas. Most notably, the bank achieved its highest historical result in Custody activities, reaffirming its dominant market position with over 40% market share in Poland.

The bank also highlighted several significant institutional banking transactions during the quarter, including accelerated equity offerings worth PLN 1.2 billion and PLN 1.8 billion, as well as a PLN 1 billion syndicated loan. These transactions demonstrate the bank’s capacity to execute large-scale financial deals for institutional clients.

Forward-Looking Statements

Bank Handlowy’s presentation included economic forecasts for Poland, projecting GDP growth to accelerate from 2.9% in 2024 to 3.7% by 2026. The National Bank of Poland reference rate is expected to decline from 5.75% in 2024 to 3.75% by 2026, potentially creating a more favorable environment for lending growth.

The bank’s share price performance relative to the sector suggests potential for valuation improvement as the strategic transformation progresses:

Executive Summary

Bank Handlowy’s Q2 2025 results reflect a company in strategic transition, pivoting decisively toward institutional banking while managing a controlled exit from consumer operations. The bank’s financial performance demonstrates the strength of its institutional franchise, with robust growth in loans, deposits, and fee income.

Shareholders are being rewarded during this transition, with the bank paying out the second-highest dividend in its history from 2024 profits (PLN 1.3 billion, representing an 8.3% yield) and securing regulatory approval to distribute an additional PLN 449 million from 2019 profits.

As the bank completes its transformation into a specialized "Bank for Global Business" over the coming year, investors will be watching closely to see if the streamlined focus translates into sustained profitability and enhanced shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.