Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

Bank of Ireland Group PLC (BIRG) presented its H1 2025 interim results on July 29, 2025, showcasing solid performance in a resilient Irish economy. The bank’s shares closed at 12.80 on July 28, with a 2.07% increase ahead of the results announcement. Trading near its 52-week high of 12.94, the stock has shown strong momentum, reflecting investor confidence in the bank’s strategic direction.

The presentation, delivered by Group CEO Myles O’Grady and Group CFO Mark Spain, highlighted the bank’s continued progress toward its medium-term targets while operating in an Irish economy that continues to outperform the broader Eurozone.

Executive Summary

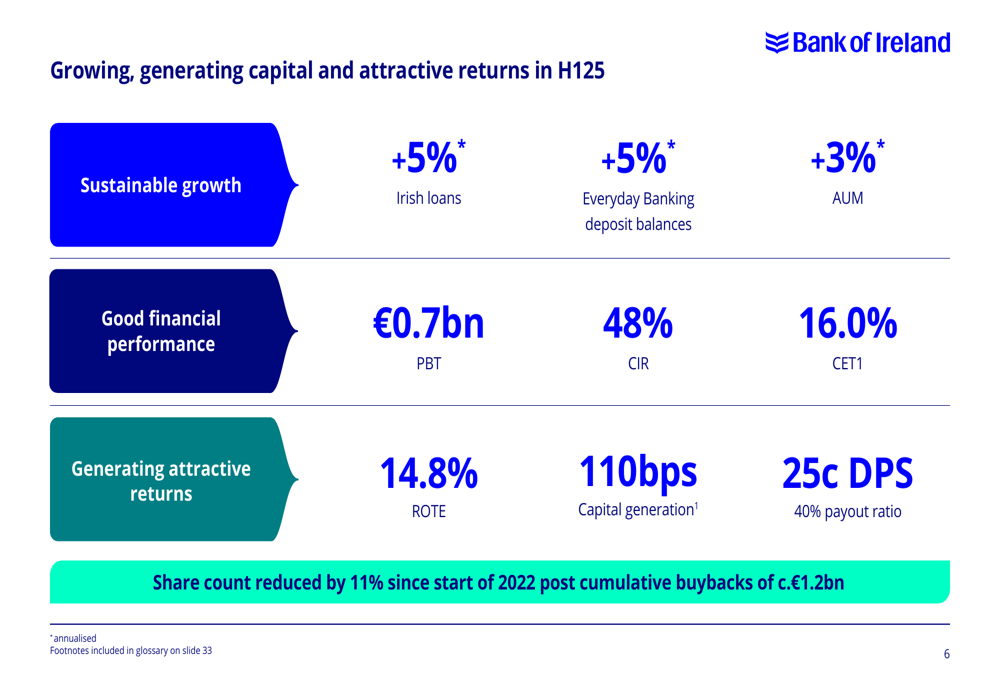

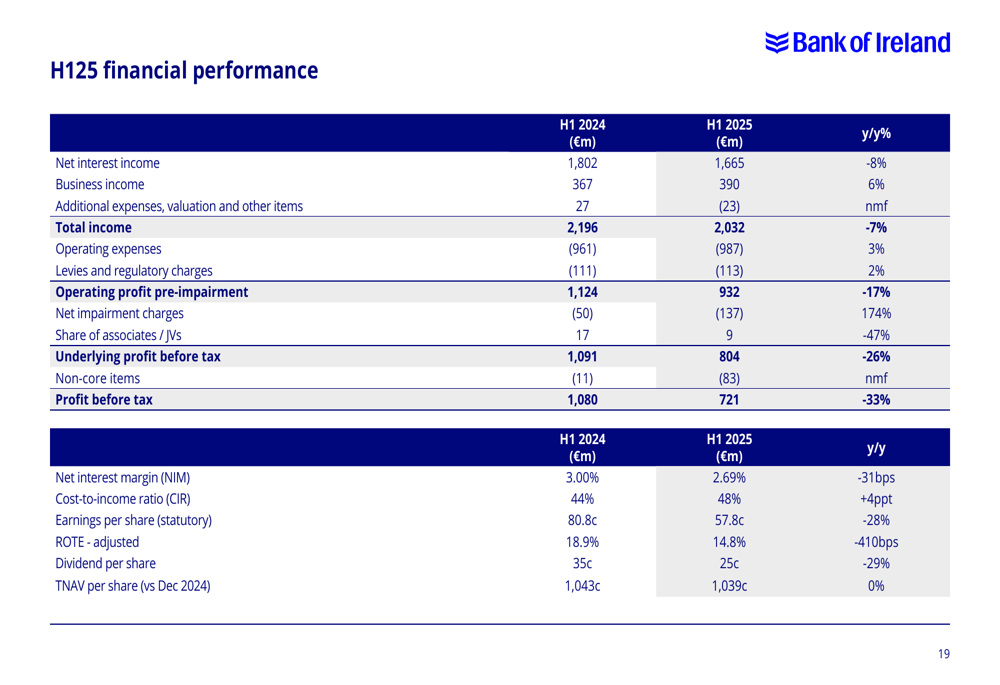

Bank of Ireland reported profit before tax of €0.7 billion for H1 2025, maintaining a strong return on tangible equity (ROTE) of 14.8% while generating 110 basis points of capital. The bank’s cost-to-income ratio remained disciplined at 48%, below its target of 50%.

The bank’s growth trajectory remained solid with 5% annualized growth in Irish loans, 5% growth in Everyday Banking deposit balances, and 3% growth in Assets Under Management (AUM). This performance supported a dividend of 25 cents per share, representing a 40% payout ratio.

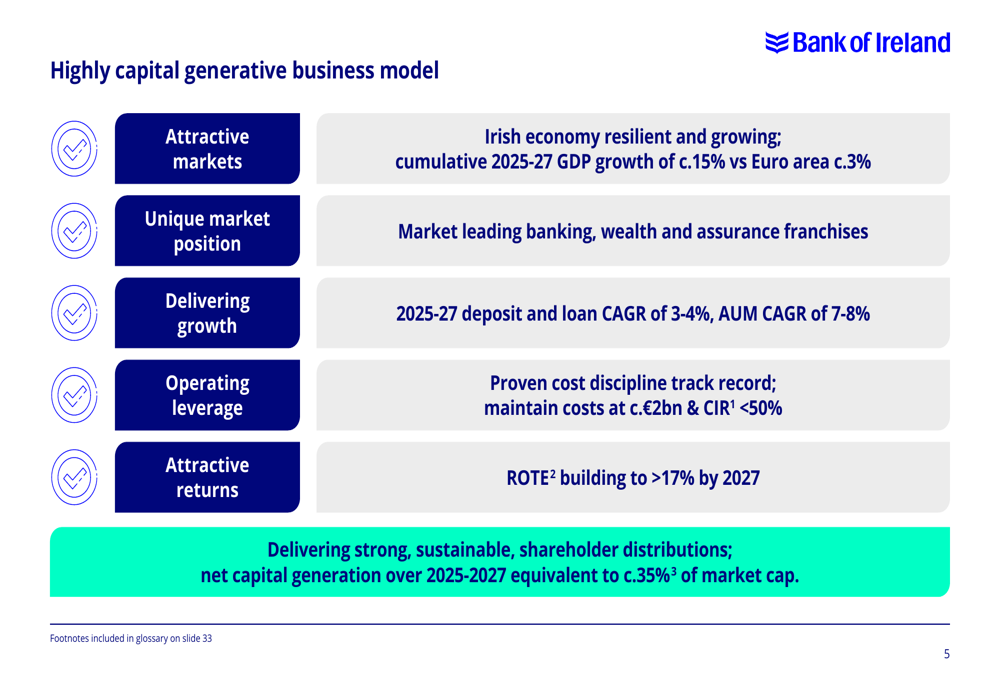

As shown in the following comprehensive overview of the bank’s business model and market position:

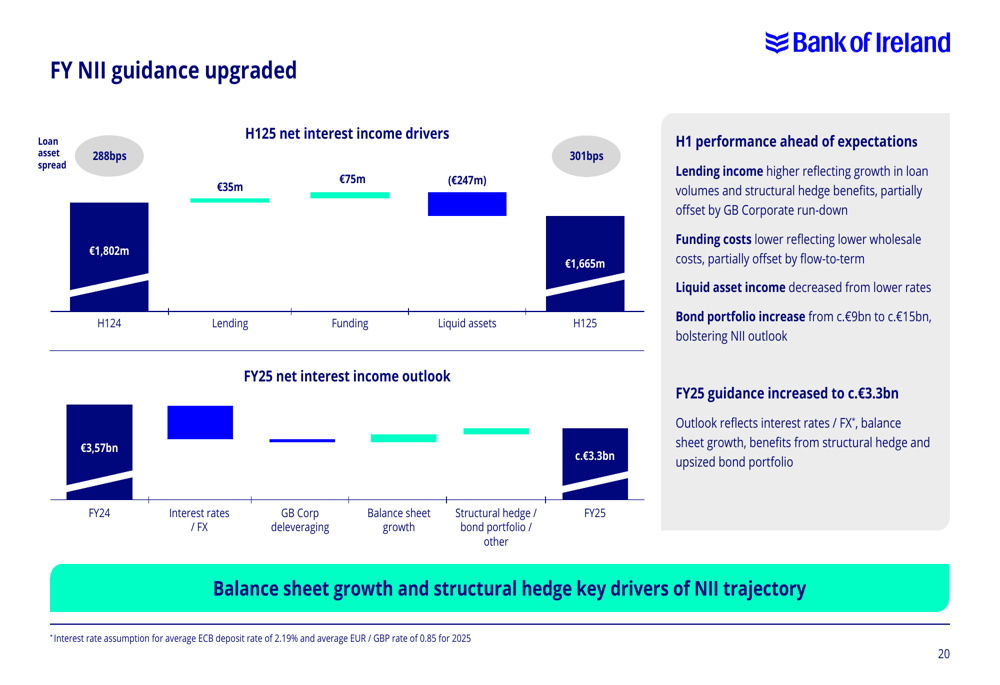

A notable highlight was the upgrade of full-year Net Interest Income (NII) guidance to approximately €3.3 billion, reflecting stronger lending income from volume growth despite higher funding costs. This represents a positive shift from the "over €3.25 billion" guidance provided in the Q1 2025 earnings call.

The bank’s key financial metrics for H1 2025 demonstrate its continued momentum:

Detailed Financial Analysis

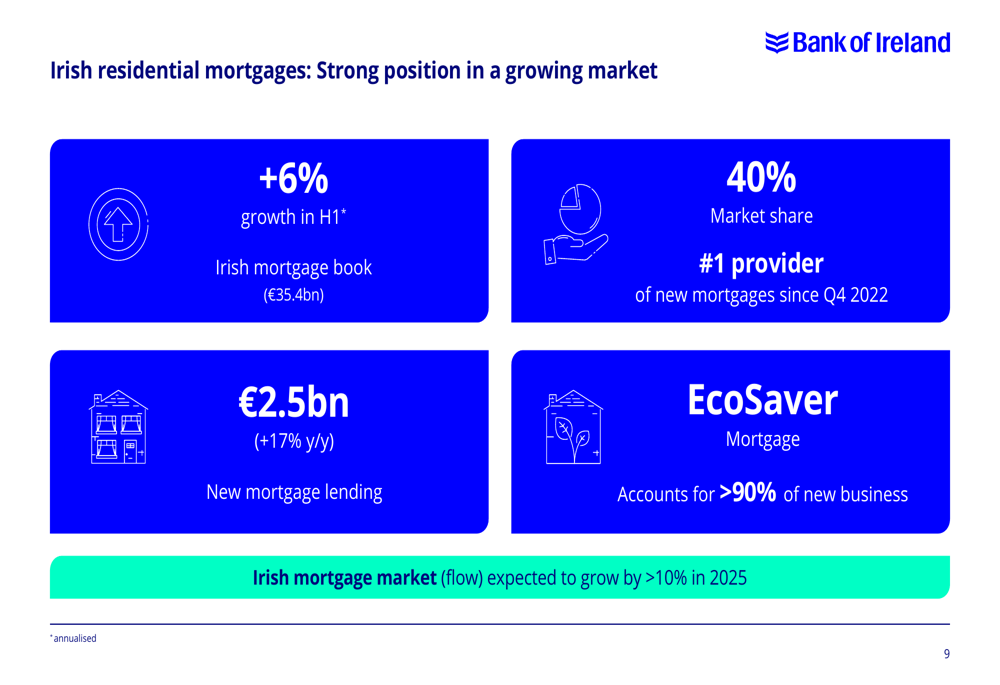

Bank of Ireland’s financial performance in H1 2025 was driven by growth across multiple segments. The Irish residential mortgage business showed particular strength, with new mortgage lending of €2.5 billion, up 17% year-over-year. The bank maintained its position as the number one provider of new mortgages since Q4 2022, with a 40% market share.

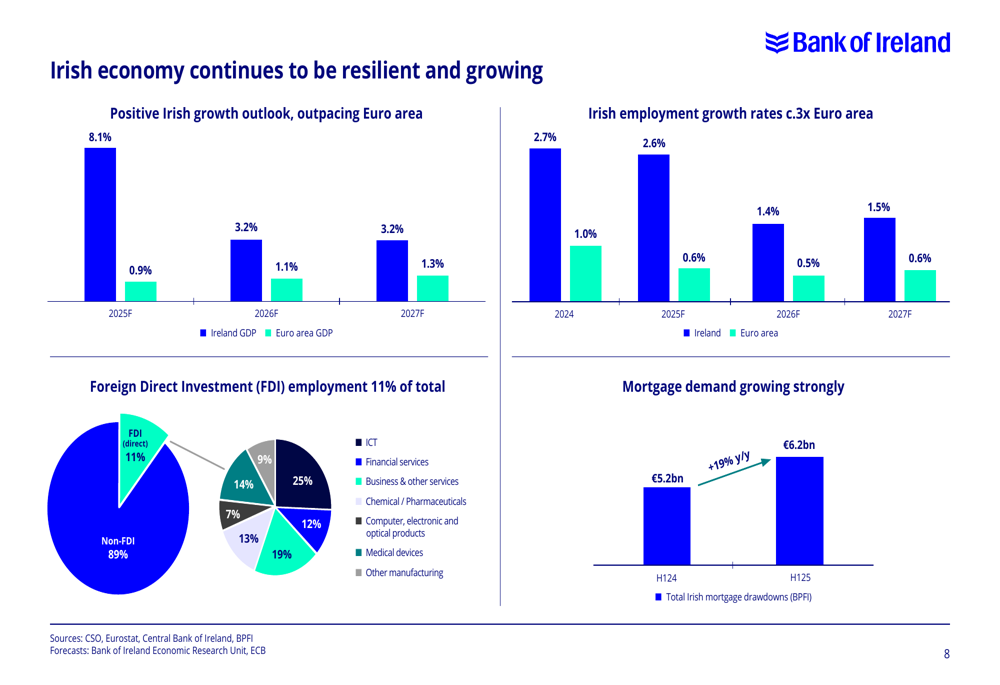

The bank’s performance is underpinned by Ireland’s economic resilience, with GDP growth forecasts significantly outpacing the Euro area. As illustrated in the following economic overview:

In the mortgage segment, the bank’s EcoSaver mortgage product now accounts for over 90% of new business, aligning with the bank’s sustainability goals while capturing growth in a market expected to expand by more than 10% in 2025.

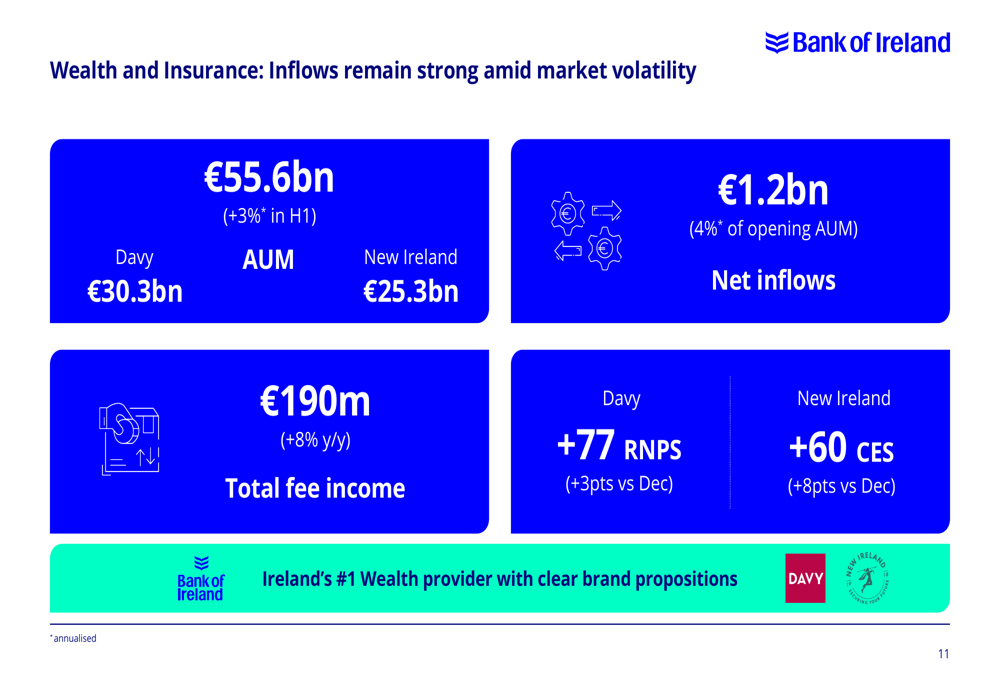

The Wealth and Insurance division also demonstrated strong performance, with Assets Under Management reaching €55.6 billion (up 3% in H1) and net inflows of €1.2 billion, representing 4% of opening AUM. Total (EPA:TTEF) fee income from this segment grew 8% year-over-year to €190 million.

Corporate & Commercial banking showed solid growth with Irish net lending up 3% in H1 to €15.8 billion, while fee income increased 11% year-over-year to €83 million. The bank continued its disciplined approach to capital allocation, with a €1.0 billion run-down of exiting portfolios.

The detailed financial performance across key metrics shows improvement in most areas:

A significant development was the upgrade to the bank’s Net Interest Income guidance for the full year 2025, now expected to reach approximately €3.3 billion. This upgrade was driven by higher lending income reflecting growth in loan volumes, partially offset by higher funding costs.

Strategic Initiatives

Bank of Ireland continues to execute on its strategic priorities of building stronger relationships, creating a simpler business, and developing a sustainable company. Customer metrics showed improvement with a Customer Effort Score of +61 and Personal RNPS of +30.

Digital adoption continues to increase, with 80% of personal current account customers now digitally active, while customer complaints decreased by 22% year-over-year. The bank’s focus on sustainability is evident in its €15.5 billion of sustainable-related lending, up 24% year-over-year.

In Everyday Banking, balances grew to €83.6 billion, up 5% in H1. The bank is planning a mobile app upgrade in H2, building on its already strong app Customer Effort Score of +66. Term and saver balances reached €9.5 billion, representing 11% of total volumes.

The UK business performed in line with expectations, with the loan book growing 4% in H1 to £17.3 billion and an NPE ratio of 2.2%. The UK operation generated £112 million in underlying profit before tax, delivering sustainable returns.

Forward-Looking Statements

Bank of Ireland reiterated its guidance for full-year 2025 ROTE and capital generation, maintaining confidence in its ability to deliver on medium-term targets. The bank continues to project ROTE building to greater than 17% by 2027, supported by disciplined cost management and growth in key segments.

The bank’s capital generation over 2025-2027 is expected to be equivalent to approximately 35% of its current market capitalization, supporting continued strong shareholder distributions. Since the start of 2022, the bank has reduced its share count by 11% through cumulative buybacks of approximately €1.2 billion.

CEO Myles O’Grady emphasized the bank’s strong strategic execution in H1 2025 and expressed confidence in the positive outlook to FY27. This outlook aligns with his comments from the Q1 earnings call, where he highlighted the bank’s strategic positioning amid global trade discussions and the supportive domestic economy.

The bank continues to progress toward its 2023-25 medium-term targets, with H1 2025 performance showing ROTE at 14.8%, CIR at 48%, and a 40% dividend payout ratio. The FY24 share buyback program is approximately 80% complete, further demonstrating the bank’s commitment to returning capital to shareholders.

Overall, Bank of Ireland’s H1 2025 results demonstrate continued momentum in a resilient Irish economy, with upgraded guidance for Net Interest Income reflecting confidence in the bank’s growth trajectory and ability to deliver attractive returns to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.