Lisa Cook sues Trump over firing attempt, emergency hearing set

Introduction & Market Context

Bank of Marin Bancorp (NASDAQ:BMRC) released its second quarter 2025 earnings presentation on July 28, revealing a strategic securities repositioning that resulted in a net loss, despite improvements in core banking metrics. The stock reacted negatively to the results, dropping 1.85% to $23.34 following the announcement, as the company missed analyst expectations on both earnings per share and revenue.

The Novato, California-based bank, with $3.7 billion in total assets, reported a net loss of $8.5 million or ($0.53) per share for the quarter. However, excluding the one-time loss on securities sales, the bank would have posted net income of $4.7 million or $0.29 per share, still below the $0.33 expected by analysts.

Quarterly Performance Highlights

The bank’s second quarter results were significantly impacted by the sale of $185.8 million in available-for-sale (AFS) securities, resulting in a pre-tax loss of $18.7 million. This strategic repositioning overshadowed otherwise positive developments in core banking operations.

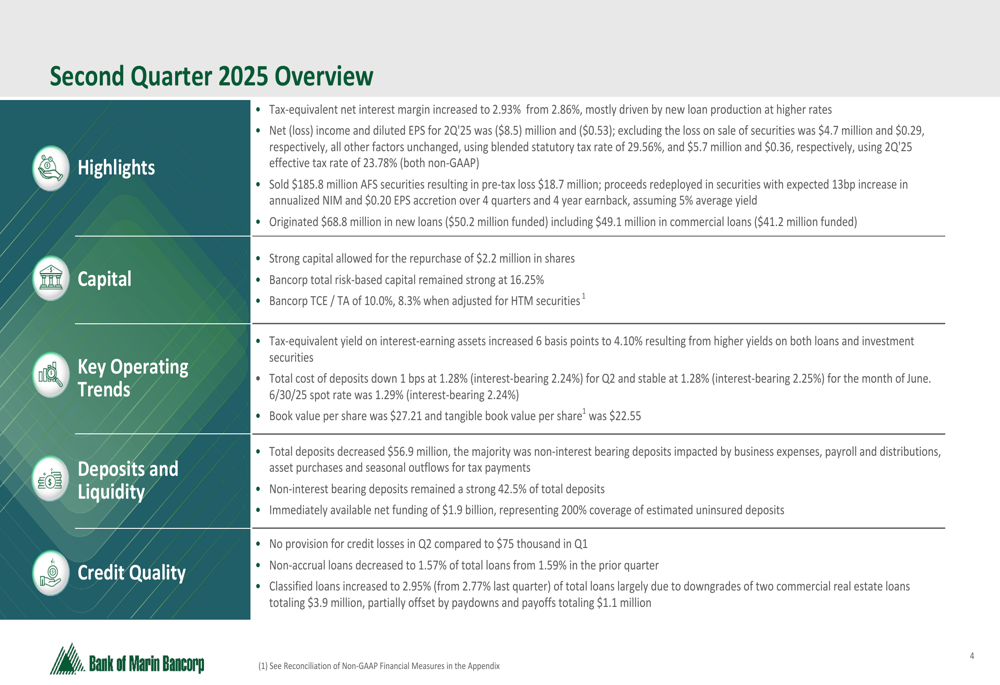

As shown in the following overview of Q2 2025 performance, the bank saw improvements in several key metrics:

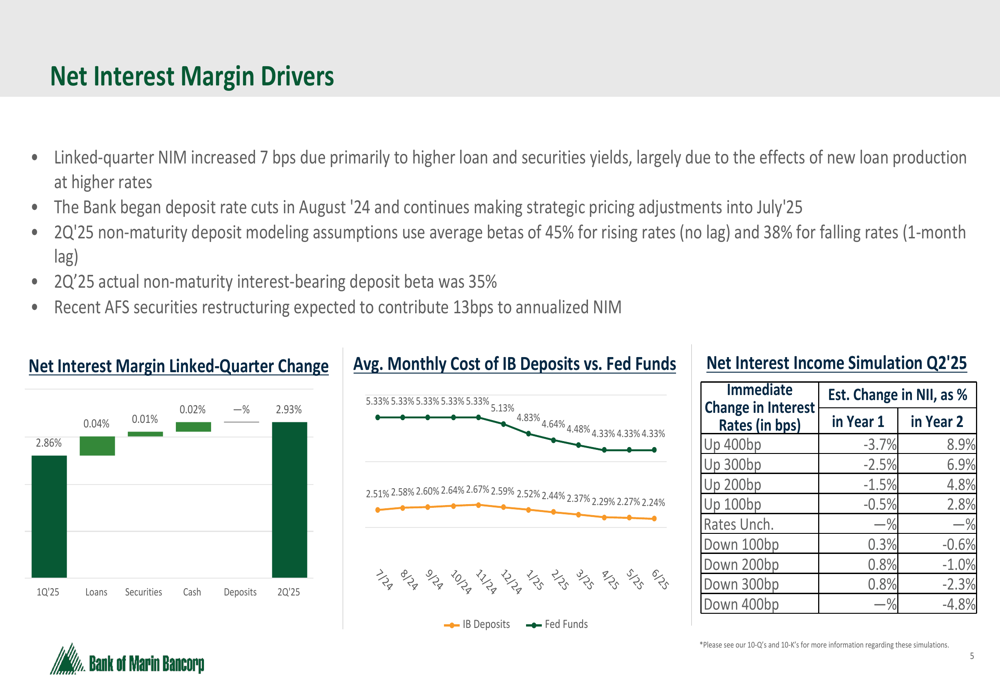

Despite the securities loss, Bank of Marin’s tax-equivalent net interest margin increased to 2.93% from 2.86% in the previous quarter, driven by higher loan and securities yields. The bank’s presentation highlighted that the securities restructuring is expected to add approximately 13 basis points to annualized net interest margin going forward.

The following chart illustrates the drivers behind the net interest margin improvement:

The bank originated $68.8 million in new loans during the quarter, with $50.2 million funded. Credit quality remained strong, with non-accrual loans decreasing slightly to 1.57% of total loans from 1.59% in the prior quarter, and no provision for credit losses was required in Q2 compared to $75,000 in Q1.

Capital and Liquidity Position

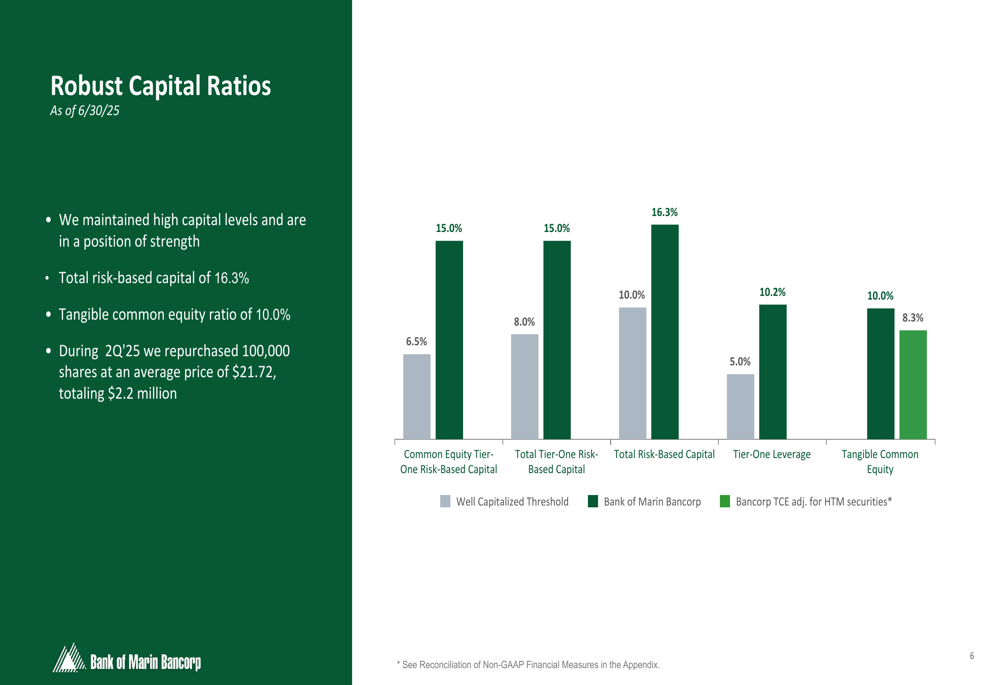

Bank of Marin emphasized its strong capital position, which allowed for the repurchase of $2.2 million in shares during the quarter. The bank’s total risk-based capital ratio remained robust at 16.25%, well above regulatory requirements for a well-capitalized institution.

The following chart details the bank’s capital ratios as of June 30, 2025:

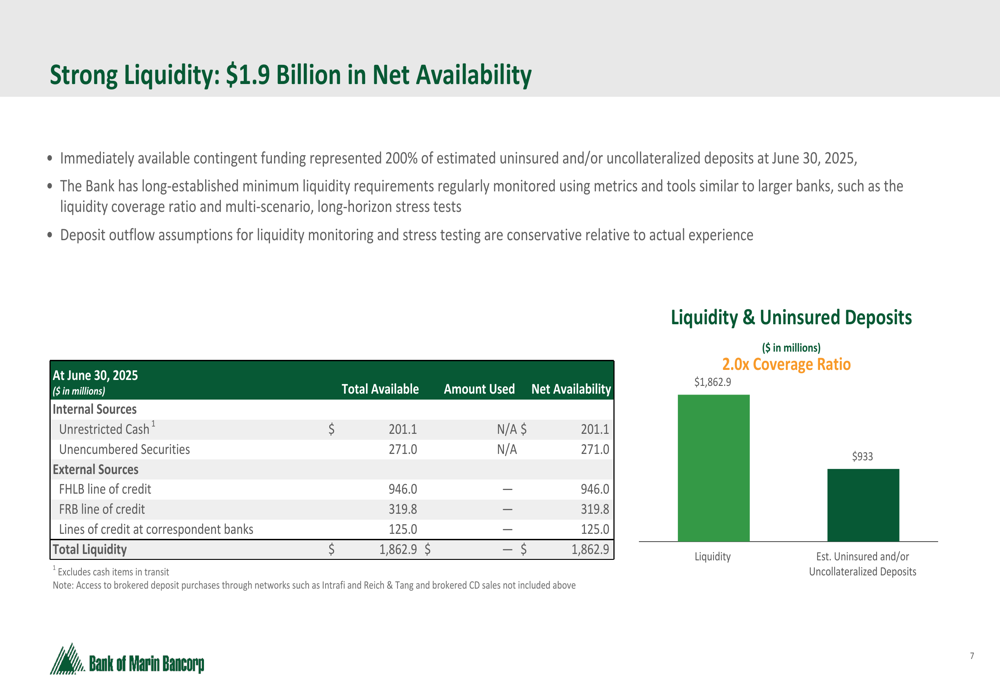

Liquidity also remains a strength for Bank of Marin, with $1.9 billion in net availability, representing 200% of estimated uninsured and/or uncollateralized deposits. This strong liquidity position provides a significant buffer against potential market volatility.

As illustrated in the following breakdown of the bank’s liquidity sources:

Loan and Deposit Trends

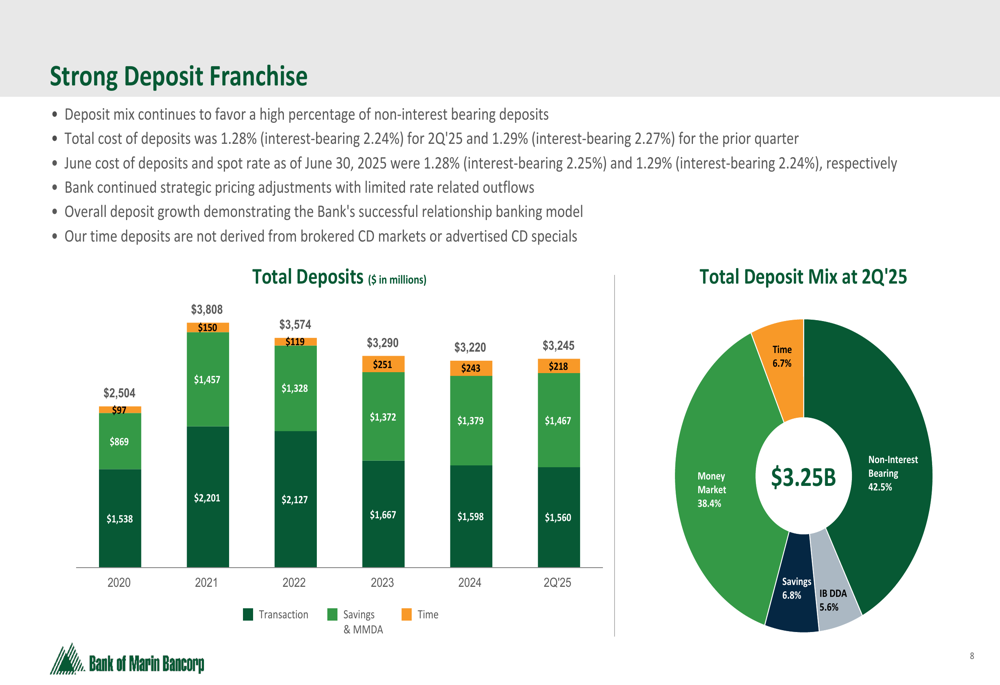

Bank of Marin’s deposit franchise continues to be a competitive advantage, with non-interest bearing deposits accounting for 42.5% of total deposits. This favorable deposit mix helps maintain a relatively low cost of funds, with the total cost of deposits at 1.28% for Q2 2025, down 1 basis point from the previous quarter.

The following chart shows the bank’s deposit composition and trends:

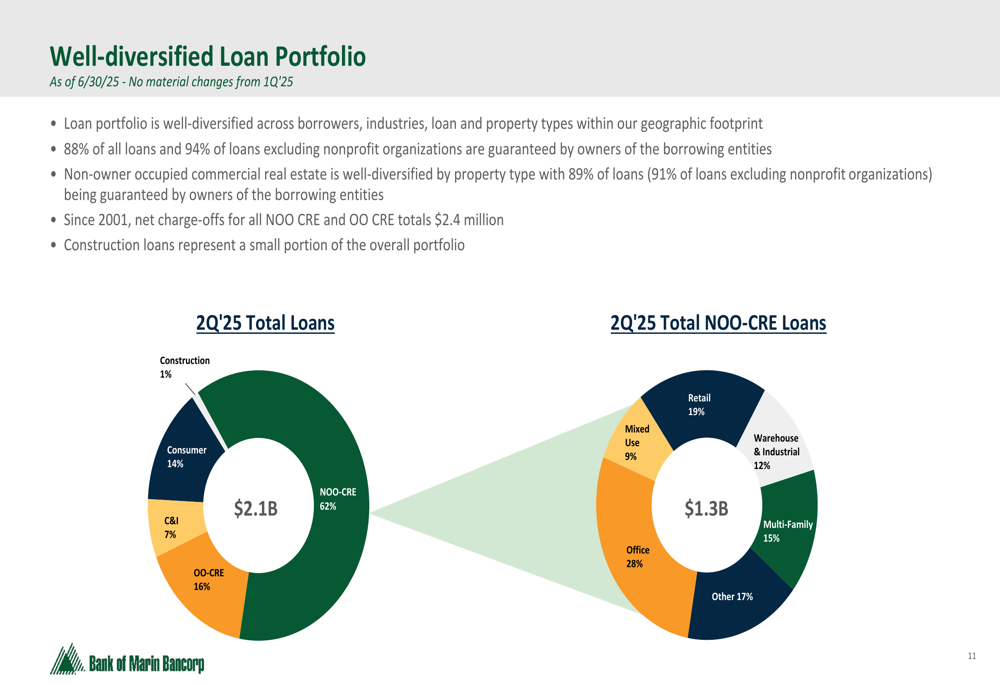

The loan portfolio remains well-diversified across borrowers, industries, and property types. The bank reported that 88% of all loans (94% excluding nonprofit organizations) are guaranteed by owners, which helps mitigate credit risk.

The following chart illustrates the diversification of the loan portfolio:

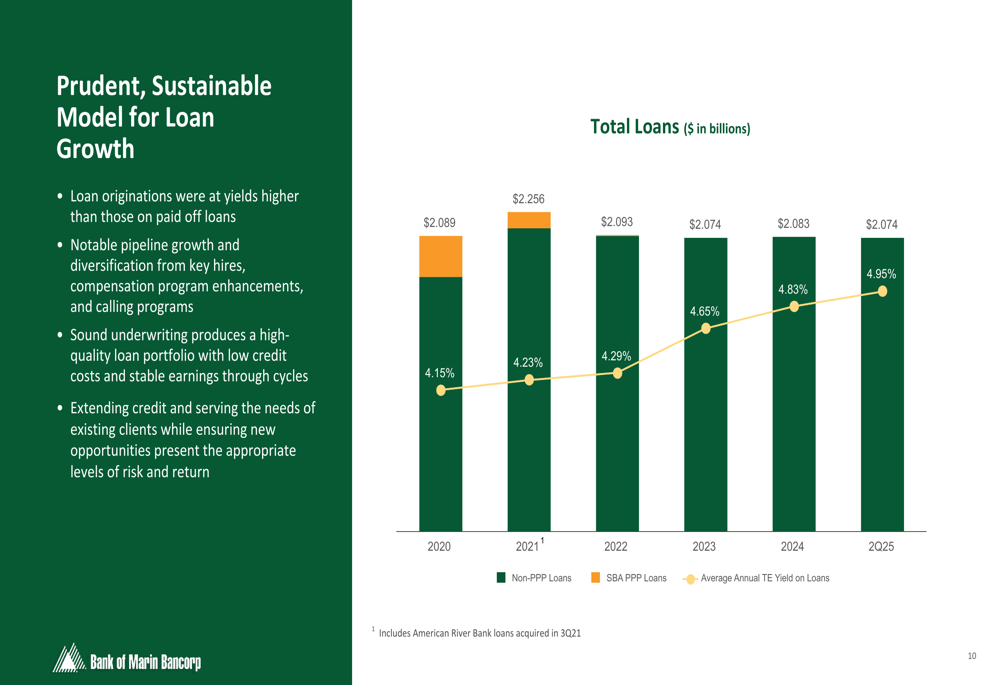

Bank of Marin has maintained a prudent approach to loan growth, focusing on high-quality relationships rather than aggressive expansion. This strategy has contributed to the bank’s historically strong asset quality.

As shown in the following chart of loan growth trends:

Strategic Initiatives and Outlook

Looking ahead, Bank of Marin is targeting mid-single-digit loan growth for 2025, with expectations of continued net interest margin expansion. According to the earnings call, the bank anticipates reaching a net interest margin of 3.5% by the latter half of 2026.

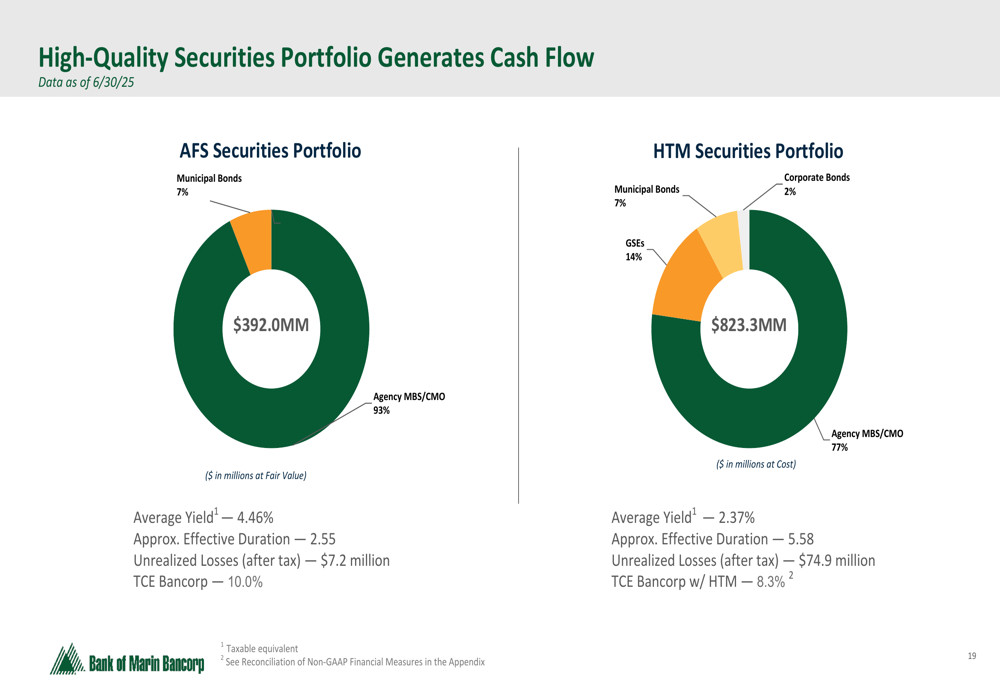

The bank’s securities portfolio is positioned to generate consistent cash flow, with a focus on high-quality investments. The restructuring of the AFS securities portfolio is expected to improve yields and overall profitability.

The composition of the securities portfolio is illustrated below:

CEO Tim Myers emphasized the competitive market environment during the earnings call, stating, "We are maintaining our disciplined underwriting and pricing criteria." This approach reflects the bank’s commitment to sustainable growth rather than pursuing volume at the expense of credit quality.

CFO Dave Bonacorso provided additional context on margin expectations, noting, "Three and a half [margin] is probably more a back half of ’26 number than a front half of ’26 number."

While Bank of Marin’s Q2 2025 results were impacted by the securities repositioning, the underlying fundamentals of the bank remain solid, with improving net interest margin, strong capital and liquidity positions, and stable credit quality. The strategic decision to reposition the securities portfolio, though resulting in a short-term loss, appears aimed at enhancing long-term profitability in the current interest rate environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.