Gold prices tick higher on fresh US tariff threats, Fed rate cut hopes

Introduction & Market Context

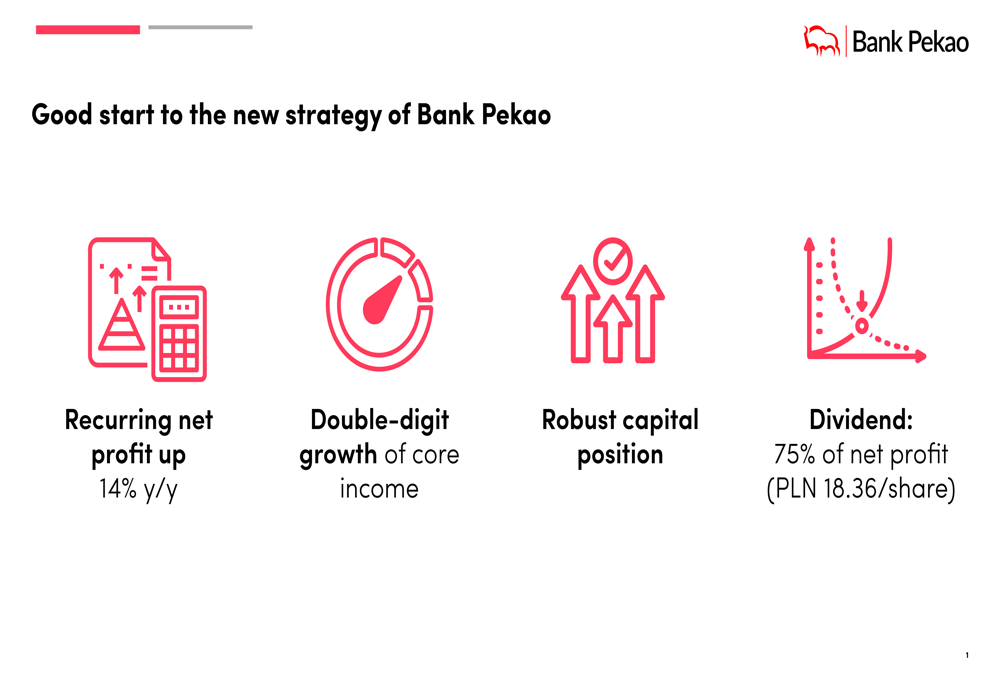

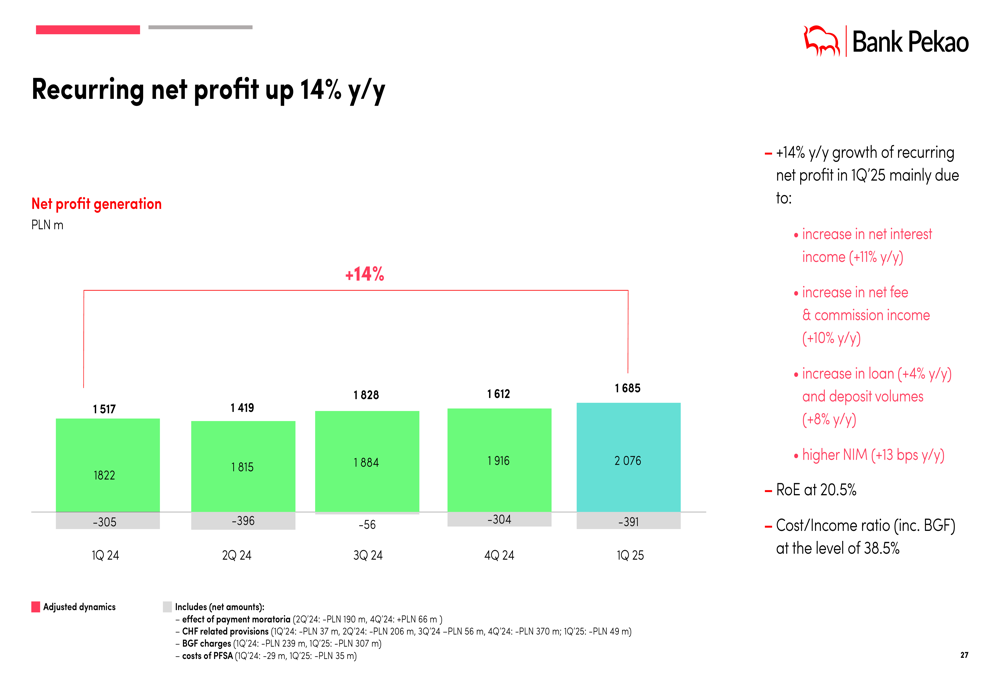

Bank Polska Kasa Opieki SA (WSE:PEO), one of Poland’s leading financial institutions, presented its Q1 2025 financial results on April 30, 2025, showcasing strong performance across key metrics. The bank reported a 14% year-over-year increase in recurring net profit, supported by growth in its loan portfolio and deposit base amid a favorable Polish economic environment expected to grow by 4% in 2025.

The presentation highlighted the bank’s successful implementation of its 2025-2027 strategy, with the tagline "Good start to the new strategy of Bank Pekao" setting a positive tone for the quarter’s achievements.

As shown in the following key achievements slide, Bank Pekao delivered strong results across multiple financial metrics:

Quarterly Performance Highlights

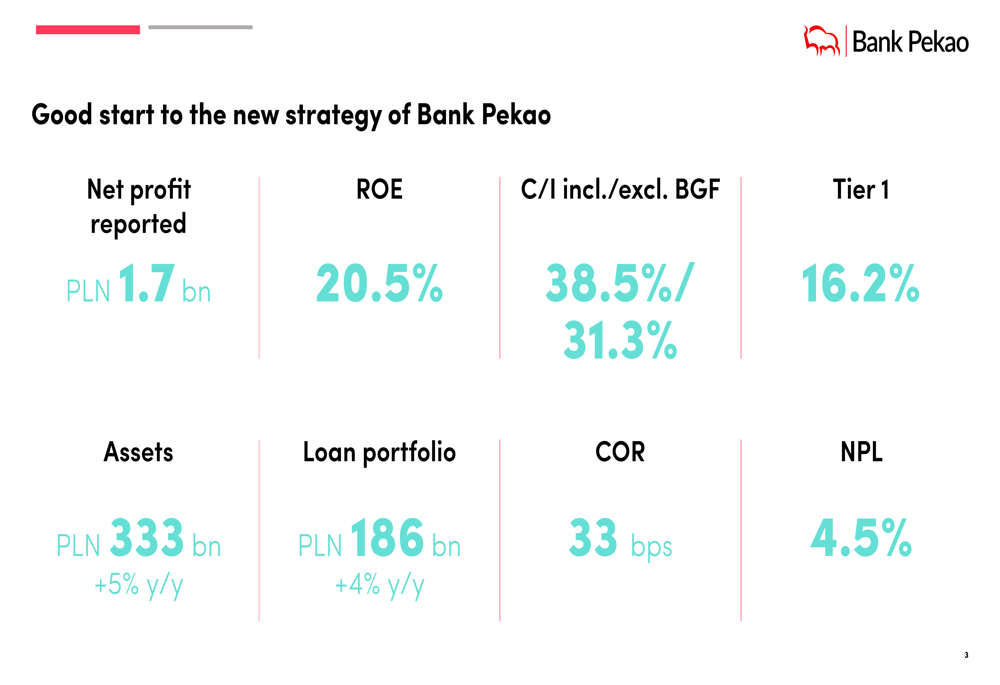

Bank Pekao reported a net profit of PLN 1.7 billion for Q1 2025, with return on equity (ROE) reaching an impressive 20.5%. The bank maintained efficiency with a cost-to-income ratio of 38.5% including BGF (Bank Guarantee Fund) contributions, or 31.3% excluding these regulatory costs. Total (EPA:TTEF) assets grew to PLN 333 billion, representing a 5% increase year-over-year.

The following slide details these key financial metrics, showing the bank’s strong capital position with a Tier 1 ratio of 16.2%:

The bank’s loan portfolio expanded to PLN 186 billion, up 4% year-over-year, while maintaining strong asset quality with a non-performing loan (NPL) ratio of 4.5% and a cost of risk at just 33 basis points.

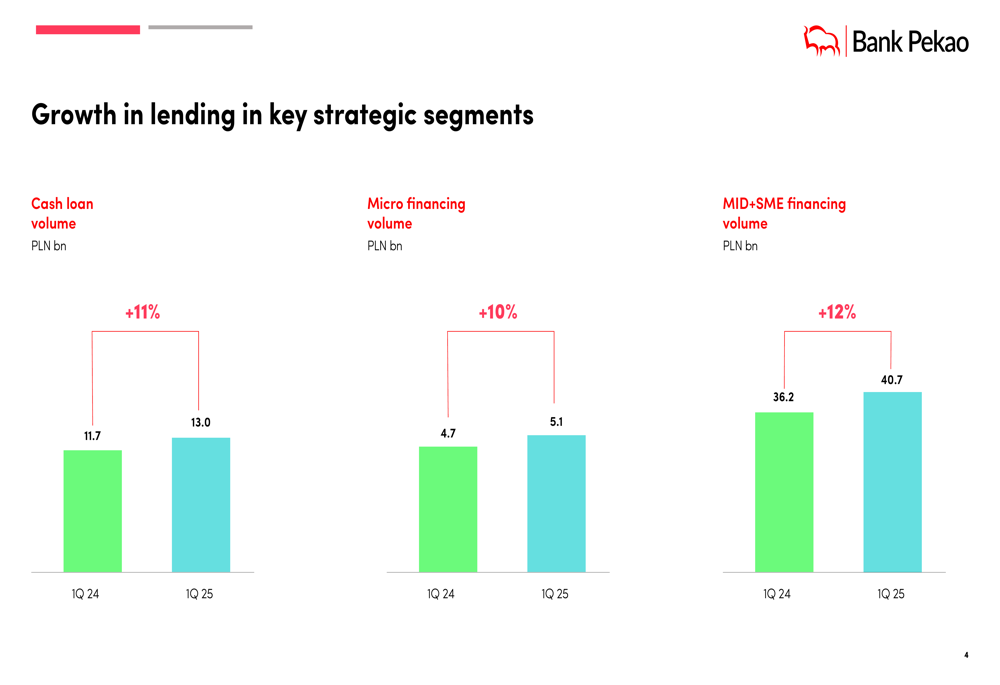

Bank Pekao’s performance was particularly strong in strategic lending segments. As illustrated in the following chart, cash loan volumes increased by 11% year-over-year to PLN 13.0 billion, micro financing grew by 10% to PLN 5.1 billion, and MID+SME financing volume expanded by 12% to PLN 40.7 billion:

Detailed Financial Analysis

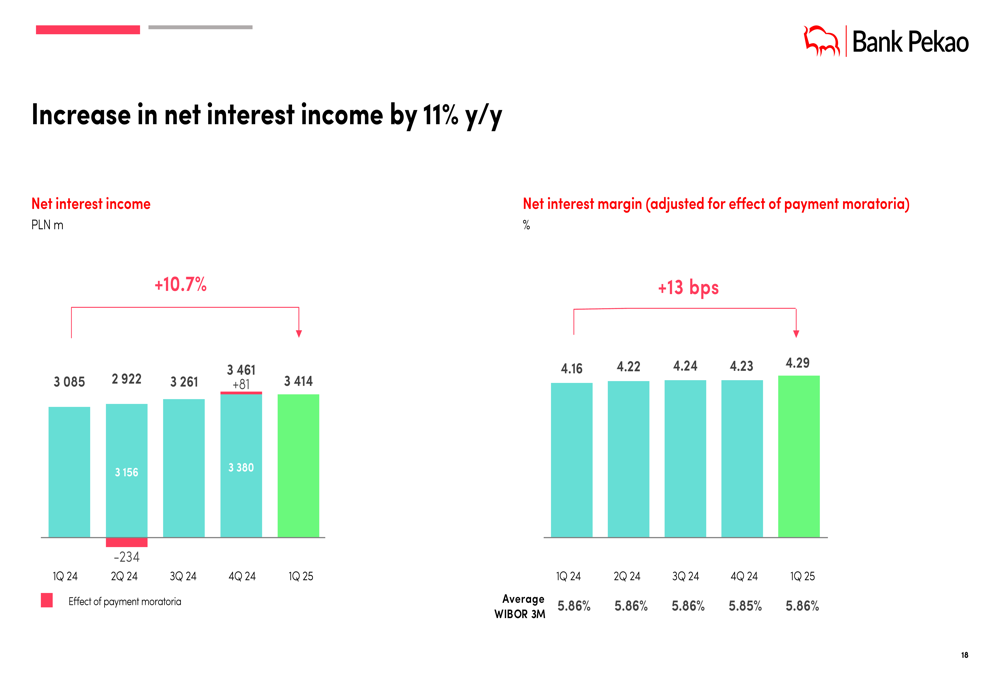

The bank’s core income showed double-digit growth, with net interest income increasing by 11% year-over-year to PLN 3,414 million in Q1 2025. The net interest margin improved to 4.29%, up 13 basis points compared to Q1 2024.

The following chart illustrates the consistent growth in net interest income over the past five quarters:

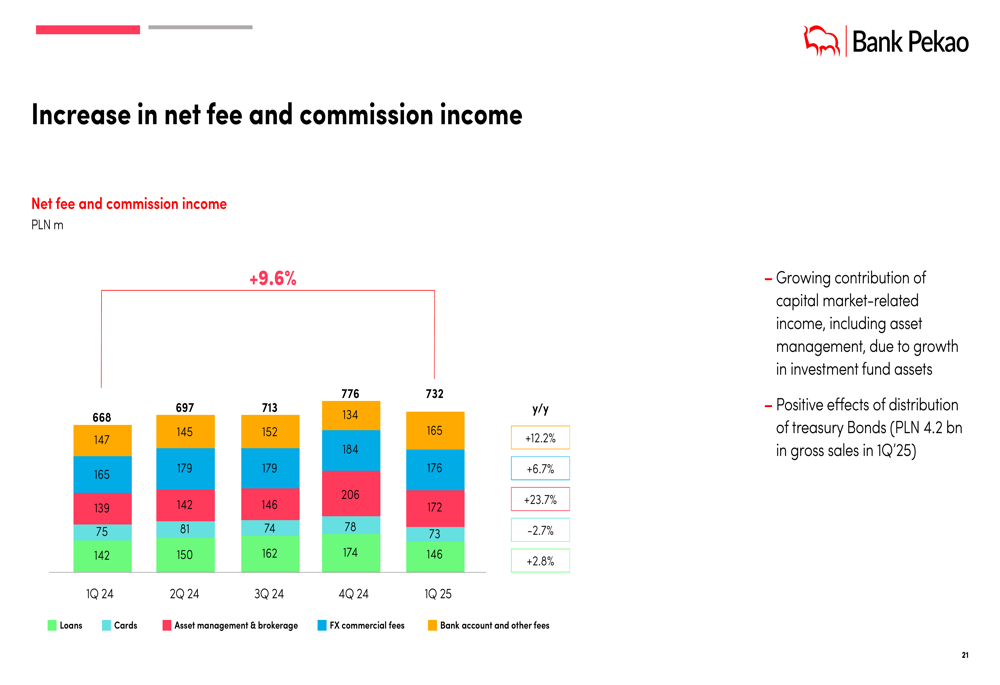

Net fee and commission income also performed strongly, increasing by 9.6% year-over-year to PLN 732 million. This growth was primarily driven by asset management and brokerage fees, which grew from PLN 139 million in Q1 2024 to PLN 172 million in Q1 2025, reflecting the bank’s success in wealth management services and the positive effects of treasury bond distribution.

As shown in the following breakdown of fee and commission income:

Cost management remained effective, with the cost-to-income ratio at 38.5% including BGF contributions. Operating costs increased by 27.3% year-over-year, primarily due to personnel costs rising to PLN 1,286 million in Q1 2025 from PLN 1,202 million in Q1 2024.

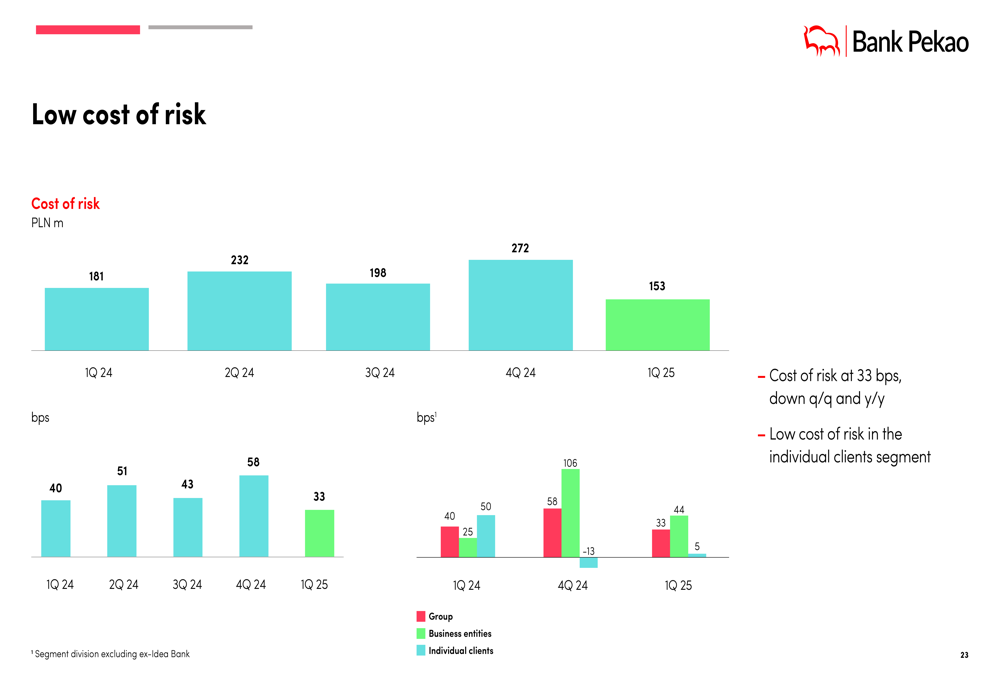

The bank maintained excellent asset quality with a low cost of risk at 33 basis points, down both quarter-over-quarter and year-over-year. This reflects the bank’s prudent risk management approach and the overall health of its loan portfolio.

The following chart shows the trend in cost of risk over the past five quarters:

Strategic Initiatives

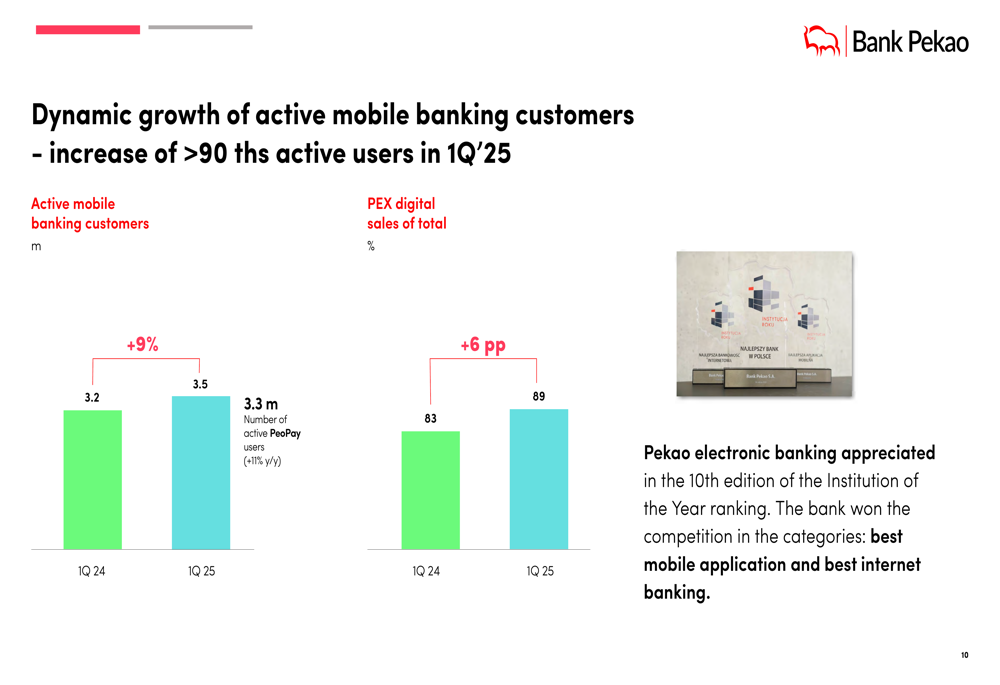

Bank Pekao continued to make significant progress in its digital transformation efforts. The number of active mobile banking customers increased by 9% year-over-year to 3.5 million, with digital sales accounting for 89% of total sales, up 6 percentage points from Q1 2024.

As illustrated in the following mobile banking growth chart:

The bank’s client acquisition strategy also showed strong results, with net customer acquisition continuing to grow. Current accounts for individual clients increased from 4.37 million in December 2020 to 5.69 million by March 2025. The bank was also recognized in the Golden Banker competition, particularly for its mortgage loan offerings.

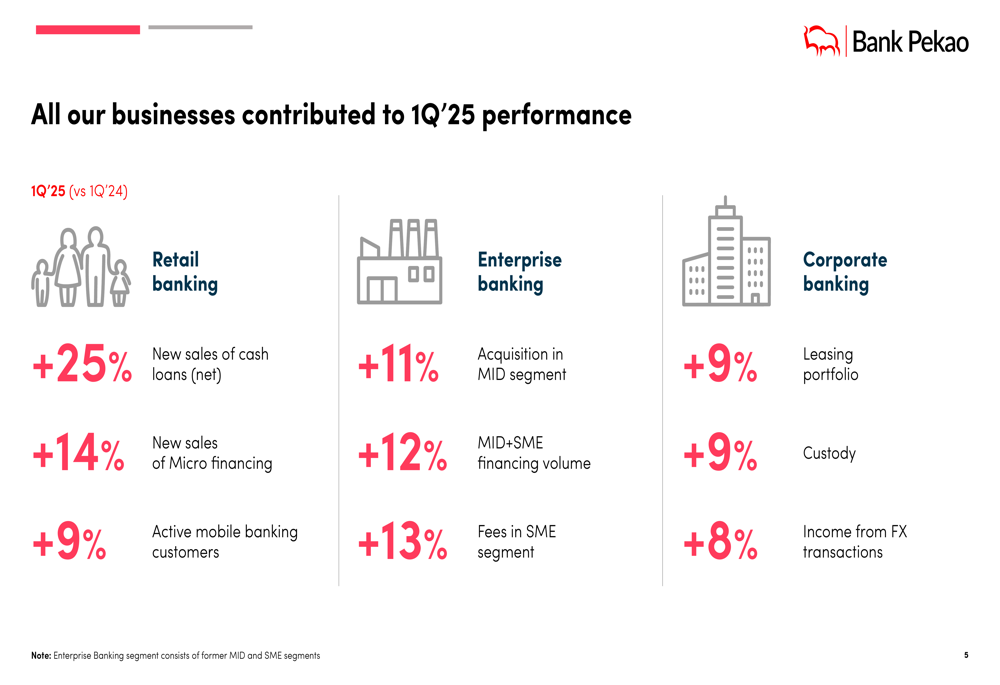

Bank Pekao’s business performance showed improvements across all segments. In retail banking, new sales of cash loans increased by 25% year-over-year, while new sales of micro financing grew by 14%. In enterprise banking, acquisition in the MID segment rose by 11%, and fees in the SME segment increased by 13%. Corporate banking saw growth in leasing portfolio (9%), custody services (9%), and income from FX transactions (8%).

The following slide details the performance across these business segments:

Forward-Looking Statements

Bank Pekao outlined its strategic goals for 2027, targeting an ROE above 18%, a cost-to-income ratio below 35%, a cost of risk between 65-75 basis points, and a dividend payout ratio of 50-75% of net profit.

The bank noted its limited sensitivity to interest rate changes, with a natural sensitivity resulting in approximately 20-25 basis points decline in net interest margin for every 100 basis points decrease in interest rates. However, the bank has implemented hedging strategies through derivatives (approximately PLN 20 billion) to mitigate this risk.

Looking ahead, Bank Pekao expects the Polish economy to grow by 4% in 2025, with conditions for inflation to fall below the central bank’s target being favorable. The bank anticipates interest rates to fall by 100 basis points by June.

The following slide shows the recurring net profit growth of 14% year-over-year, highlighting the bank’s strong financial performance:

Competitive Industry Position

Bank Pekao maintains a strong competitive position in the Polish banking sector, particularly in mortgage loans where it ranks in the top three for sales. The bank’s robust capital position, with a capital surplus over 5 percentage points, provides a solid foundation for future growth and dividend payments.

The bank declared a dividend of PLN 18.36 per share, representing 75% of net profit, in line with its strategic goal of maintaining a dividend payout ratio between 50-75%.

Bank Pekao’s asset quality remains strong compared to the market, with one of the smallest CHF mortgage loan portfolios and high reserve coverage, limiting its risk exposure in this area.

The bank’s growth in mutual funds was particularly impressive, with a 32.4% year-over-year increase in assets under management at Pekao TFI, reflecting strong customer trust and effective wealth management services.

In conclusion, Bank Pekao’s Q1 2025 financial results demonstrate strong performance across all key metrics, with double-digit growth in core income, expanding digital banking capabilities, and robust capital position, positioning the bank well for continued success in implementing its 2025-2027 strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.