Asia tech stocks slide tracking Wall St losses amid AI doubts, govt. uncertainty

Introduction & Market Context

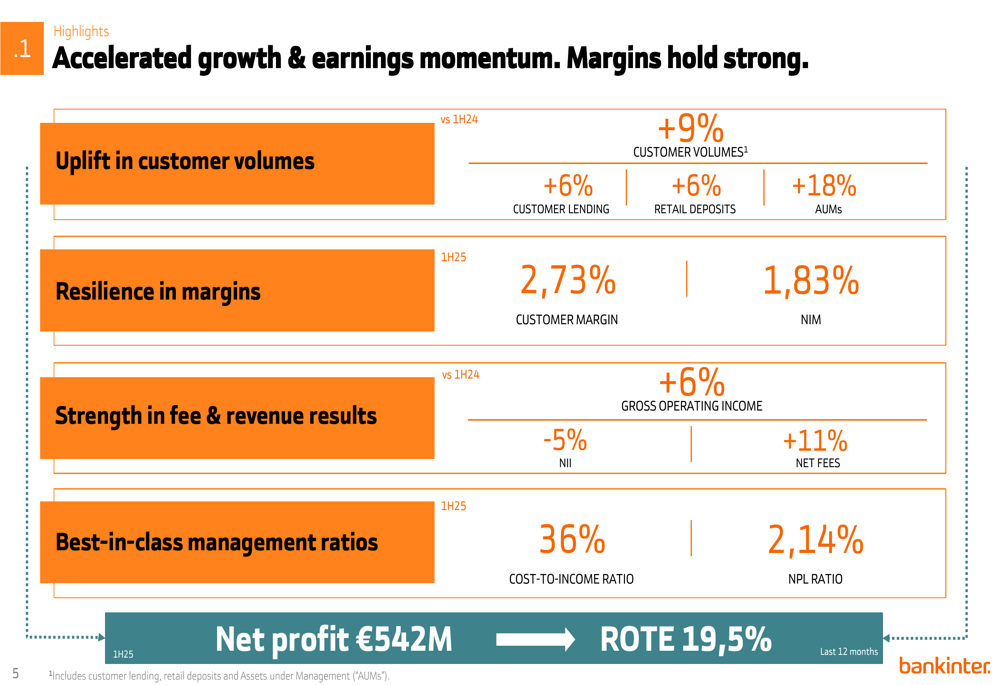

Bankinter (MCE:BME:BKT) presented its first half 2025 earnings results on July 24, 2025, reporting a net profit of €542 million and a Return on Tangible Equity (ROTE) of 19.5%. The Spanish banking group’s stock responded positively to the results, rising 2.07% to €11.60 on the presentation day, continuing its strong performance that has seen the share price reach near its 52-week high of €11.87.

The presentation comes after a strong first quarter where Bankinter reported a 35% year-over-year increase in net income to €270 million, suggesting continued momentum in the second quarter. The bank is now celebrating its 60th anniversary, having evolved from its incorporation as an industrial bank in 1965 to a diversified financial institution with operations across Spain, Portugal, and most recently, Ireland.

Executive Summary

Bankinter’s first half 2025 results demonstrate resilience in a challenging interest rate environment, with the bank successfully offsetting pressure on net interest income through strong fee growth and operational efficiency. Customer volumes increased by 9% year-over-year, reaching €231 billion, driven by 18% growth in Assets Under Management (AUMs).

As shown in the following comprehensive overview of key financial metrics:

While Net Interest Income (NII) decreased by 5% year-over-year, the bank’s gross operating income increased by 6%, supported by an 11% rise in net fees. The bank maintained strong profitability with a ROTE of 19.5% and continued to improve its cost-to-income ratio to 36%, positioning it among the most efficient banks in Europe.

Quarterly Performance Highlights

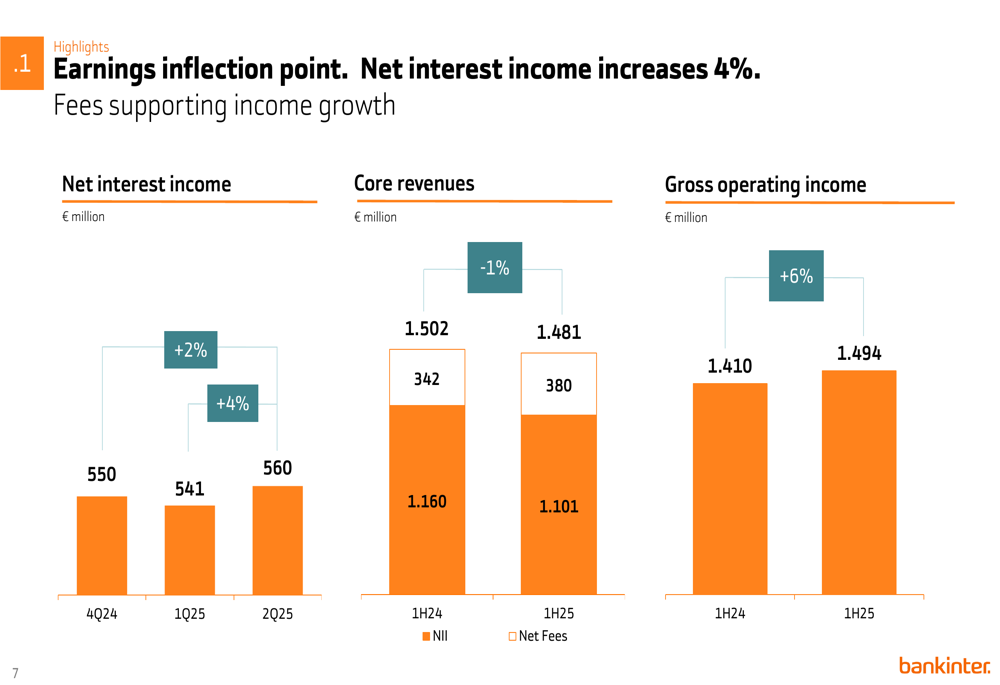

Bankinter’s earnings show signs of an inflection point in Net Interest Income, which has begun to recover after previous pressure. NII increased by 2% from Q4 2024 to Q1 2025, and further accelerated with 4% growth from Q1 to Q2 2025, reaching €560 million in the second quarter.

The quarterly trend in net interest income and core revenues is illustrated in this chart:

Despite the 5% year-over-year decline in NII for the first half (€1.101 billion in 1H25 vs €1.160 billion in 1H24), strong fee income growth of 11% (€380 million in 1H25 vs €342 million in 1H24) helped stabilize core revenues. Overall, gross operating income increased by 6% to €1.494 billion, demonstrating the bank’s ability to grow revenues despite interest rate challenges.

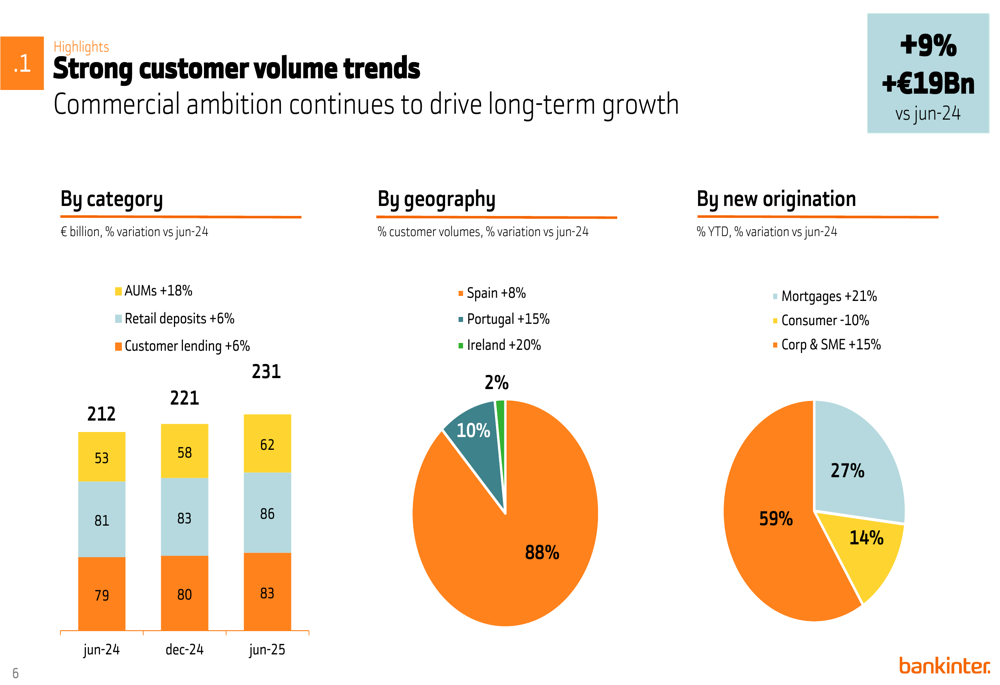

Customer volumes showed robust growth across all categories, with particularly strong performance in Assets Under Management:

The geographic distribution of customer volumes reveals Bankinter’s successful diversification strategy, with Spain representing 88% of volumes (+8% growth), Portugal 10% (+15% growth), and Ireland 2% (+20% growth). This expansion strategy appears to be paying dividends, with international operations growing at a faster pace than the domestic business.

Strategic Initiatives & Geographic Expansion

Bankinter’s digital transformation initiatives are driving significant efficiency improvements. Productivity per employee increased from €33 million in December 2024 to €35 million by June 2025, while costs relative to customer volumes decreased from €4.8 million to €4.6 million over the same period.

The bank has successfully completed the technological and customer migration from EVO to Bankinter, realizing economies of scale. Additionally, Bankinter has deployed a new cloud platform for AI models, which has multiplied the commercial productivity of these models, and implemented over 20 new AI GEN cases this year.

These digital transformation efforts have contributed to Bankinter’s industry-leading efficiency metrics, as the bank continues to invest in technology while maintaining tight cost control.

Competitive Industry Position

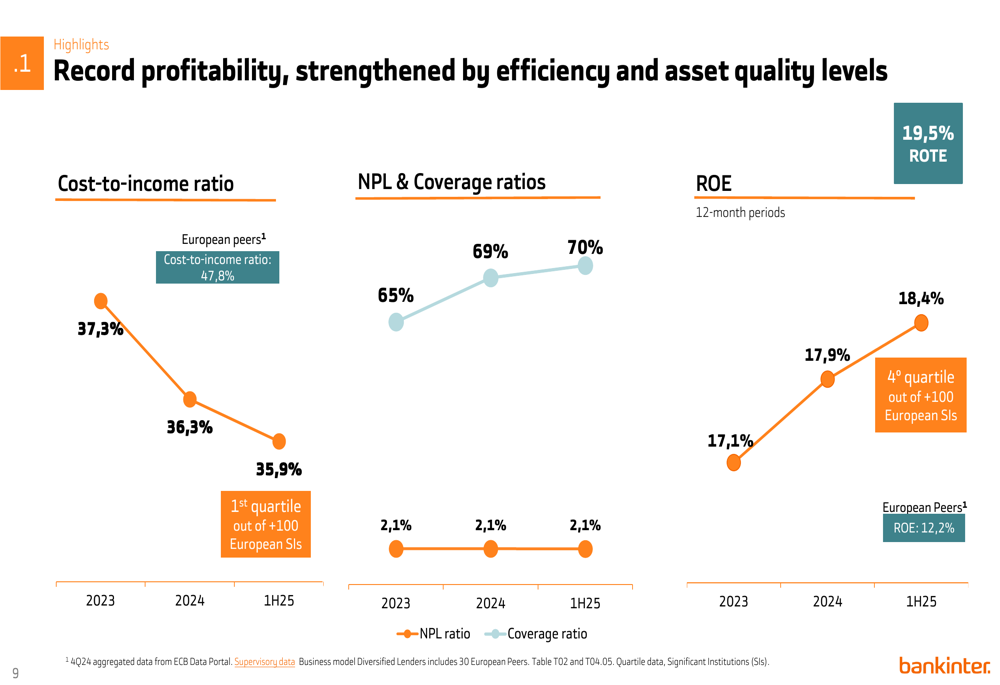

Bankinter’s performance metrics place it among the top-performing banks in Europe. The bank’s efficiency and profitability compared to European peers is illustrated in this chart:

With a cost-to-income ratio of 35.9% in 1H25 (improved from 36.3% in 2024 and 37.3% in 2023), Bankinter ranks in the first quartile among more than 100 European Significant Institutions, significantly outperforming the European peer average of 47.8%.

Similarly, Bankinter’s Return on Equity (ROE) of 18.4% in 1H25 (up from 17.9% in 2024 and 17.1% in 2023) places it in the fourth quartile among European peers, whose average ROE stands at 12.2%. The bank’s ROTE is even more impressive at 19.5%.

Asset quality remains strong, with the Non-Performing Loan (NPL) ratio at 2.1% and the coverage ratio improving to 70% in 1H25 from 69% in 2024 and 65% in 2023. These metrics reflect Bankinter’s prudent risk management approach and the quality of its loan book.

Forward-Looking Statements

While the presentation did not explicitly provide forward guidance, Bankinter’s performance trajectory suggests continued momentum in the second half of 2025. The bank’s previous goal, mentioned in the Q1 earnings call, of achieving over €1 billion in net income for 2025 appears to be on track given the €542 million earned in the first half.

The bank’s focus on fee-generating businesses, particularly wealth management, should continue to provide a counterbalance to any potential pressure on interest margins. Geographic diversification, especially the high-growth operations in Portugal and Ireland, represents another avenue for sustained growth.

The completed integration of EVO Bank and the continued investment in digital transformation initiatives position Bankinter to further improve its industry-leading efficiency metrics. With a cost-to-income ratio target of 35-36% (as mentioned in the Q1 earnings call) and the current ratio at 35.9%, the bank appears well-positioned to achieve its efficiency goals.

As Bankinter celebrates its 60th anniversary, the presentation demonstrates that the bank continues to "think outside the box" with its diversified business model and strategic focus on high-growth segments and geographies.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.