JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

BankUnited (NYSE:BKU) released its Q1 2025 supplemental presentation on April 28, showing mixed results with a sequential decline in earnings but year-over-year improvement. The bank’s stock jumped 4.94% in premarket trading to $35.29, suggesting investors were encouraged by the underlying trends despite the quarterly earnings dip.

The presentation highlighted BankUnited’s continued progress on strategic priorities, particularly in improving its deposit mix and funding profile, while maintaining a conservative approach to commercial real estate exposure in a challenging market environment.

Quarterly Performance Highlights

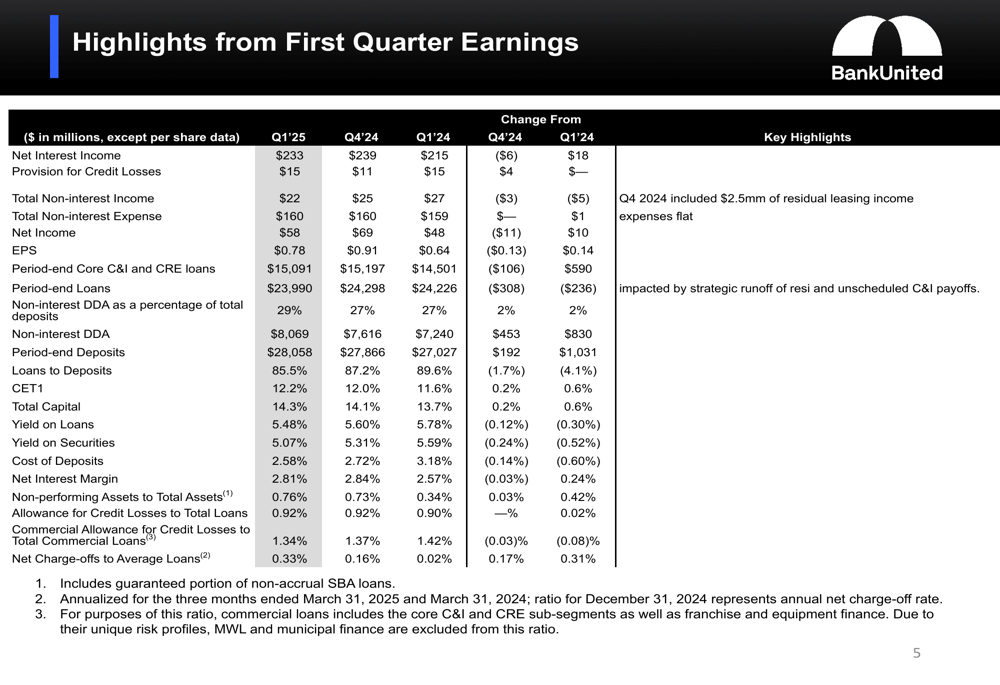

BankUnited reported net income of $58 million for Q1 2025, down from $69 million in Q4 2024 but up from $48 million in Q1 2024. Earnings per share followed a similar pattern, coming in at $0.78 for the quarter, compared to $0.91 in the previous quarter and $0.64 in the same period last year.

As shown in the following comprehensive summary of key financial metrics:

Net interest income totaled $233 million, down from $239 million in Q4 2024 but up from $215 million in Q1 2024. The net interest margin slightly compressed to 2.81% from 2.84% in the previous quarter. Total (EPA:TTEF) non-interest income decreased to $22 million from $25 million in Q4 2024, while non-interest expenses remained flat at $160 million.

The bank’s provision for credit losses increased to $15 million from $11 million in the previous quarter, reflecting ongoing caution in the current economic environment.

Deposit and Funding Strategy

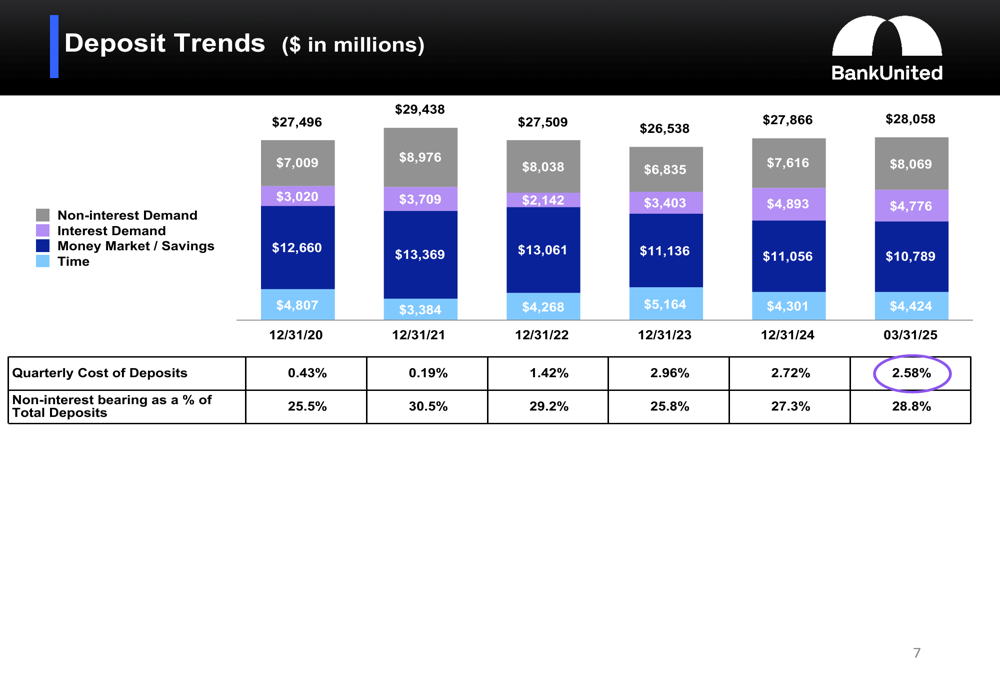

A key bright spot in BankUnited’s Q1 results was the continued improvement in its deposit mix and funding profile. Non-interest demand deposits (NIDDA) grew by $453 million or 6% during the quarter, now representing 29% of total deposits, up from 27% at the end of 2024.

The following chart illustrates the positive trend in deposit composition over time:

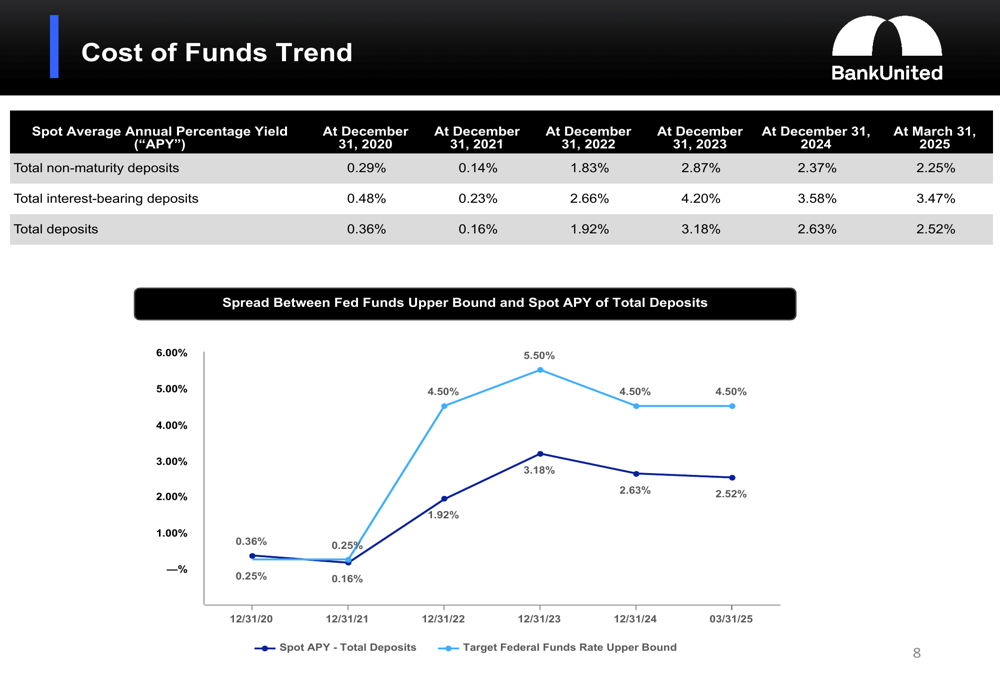

The cost of deposits declined to 2.58% from 2.72% in the previous quarter, representing a meaningful 14 basis point reduction. This improvement in deposit costs is particularly significant given the current interest rate environment, as shown in the cost of funds trend:

BankUnited also reduced its reliance on wholesale funding by $1.1 billion during the quarter, further strengthening its funding profile. Total deposits stood at $28.1 billion as of March 31, 2025, with a loans-to-deposits ratio of 85.5%.

Loan Portfolio Quality and Composition

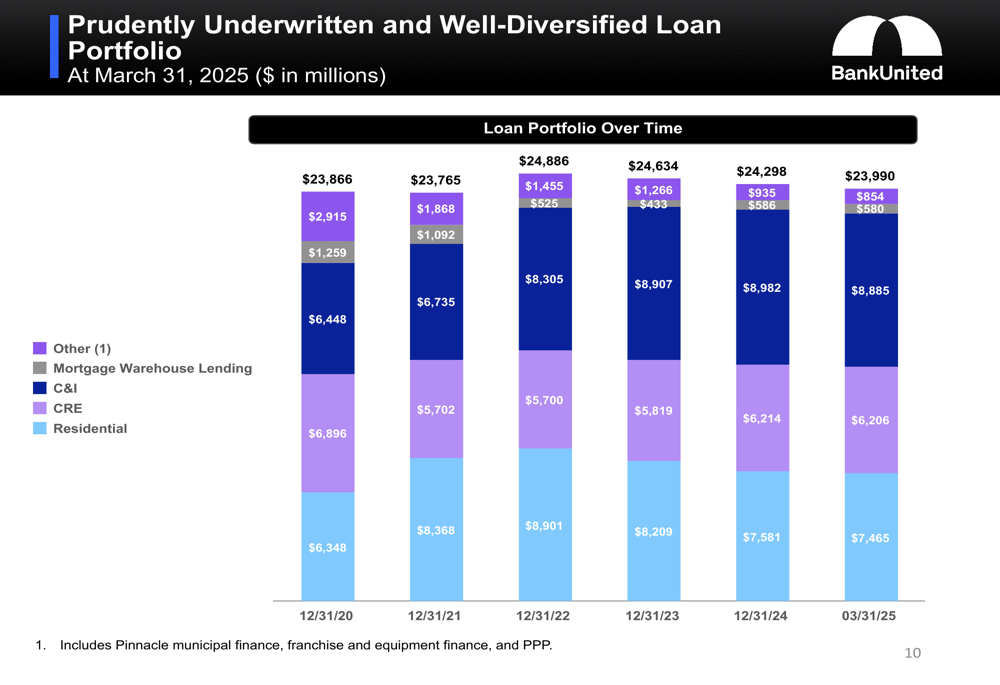

BankUnited’s total loan portfolio decreased to $24.0 billion from $24.3 billion at the end of 2024. Core commercial and industrial (C&I) and commercial real estate (CRE) loans declined by $106 million, which the bank attributed to seasonal factors. Lower-yielding and non-core residential, franchise, equipment, and municipal finance loans decreased by $196 million, reflecting the bank’s strategic shift toward higher-yielding assets.

The following chart shows the evolution of BankUnited’s loan portfolio composition:

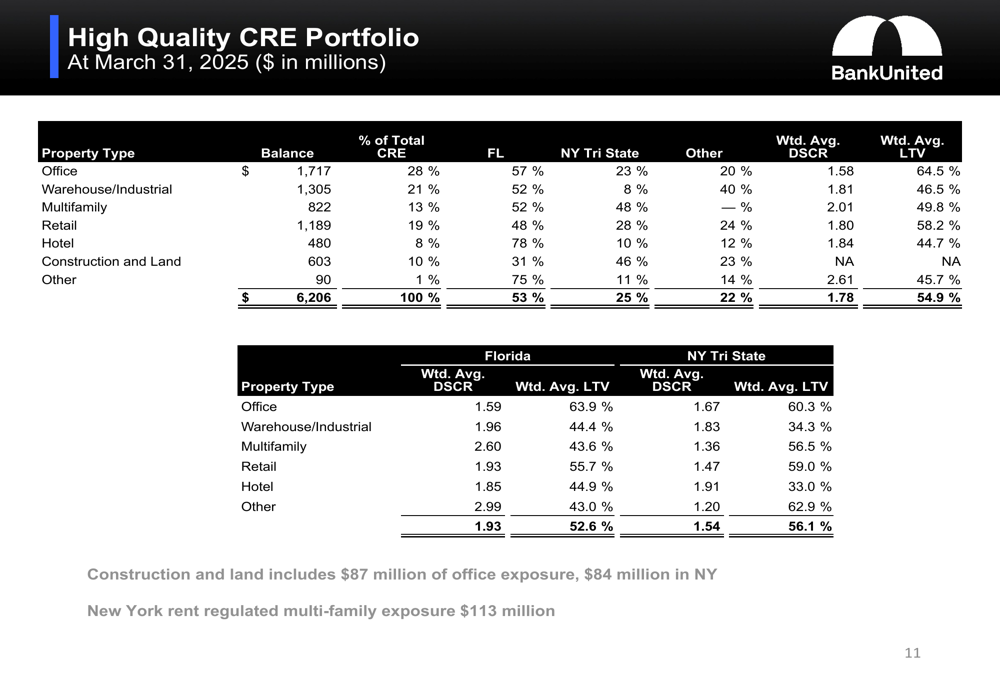

A notable aspect of BankUnited’s presentation was its emphasis on a conservative approach to CRE exposure, particularly in the office segment. The bank’s CRE portfolio details reveal a diversified mix across property types and geographies:

Office properties represent 28% of the CRE portfolio, with 20% of that being medical office space, which typically carries lower risk. The CRE portfolio shows strong weighted average debt service coverage ratios (1.78) and conservative loan-to-value ratios (54.9%), indicating prudent underwriting standards.

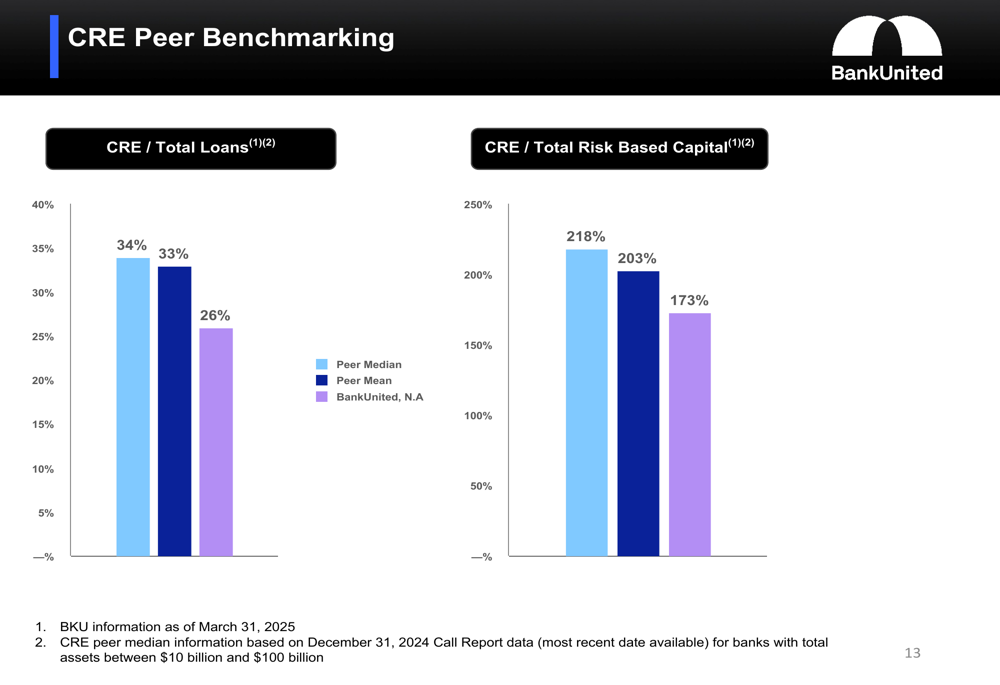

BankUnited’s CRE exposure compares favorably to peers, with CRE loans representing 26% of total loans versus a peer median of 34%:

The bank also highlighted its manageable CRE maturity profile, with only 14% of the total CRE portfolio fixed and maturing in the next 12 months, reducing refinancing risk in the current rate environment.

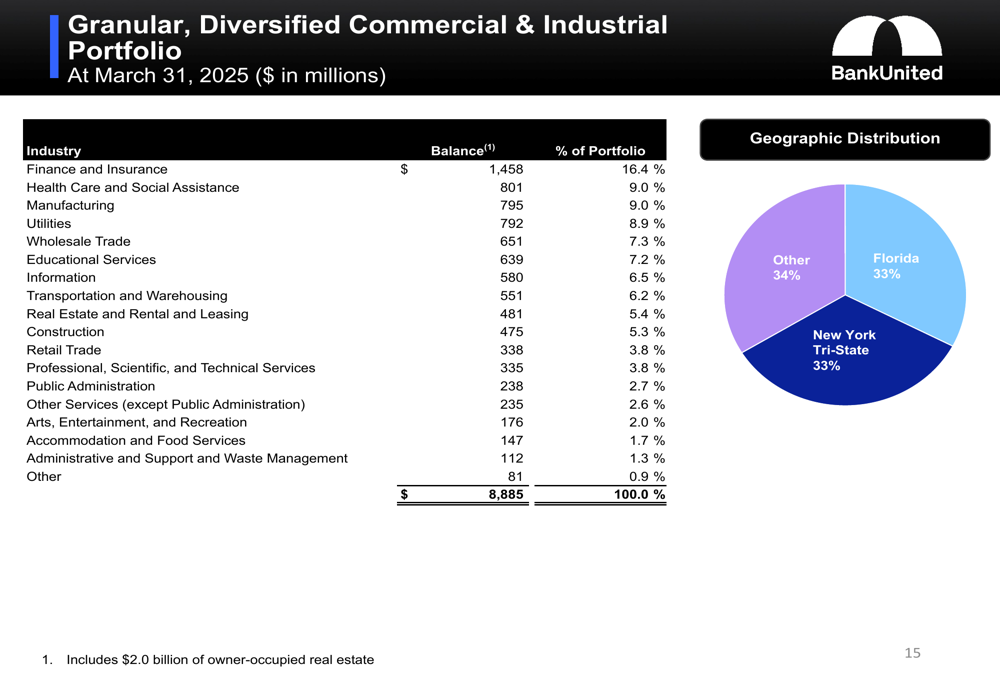

The C&I portfolio shows strong diversification across industries and geographies:

Credit Quality and Risk Management

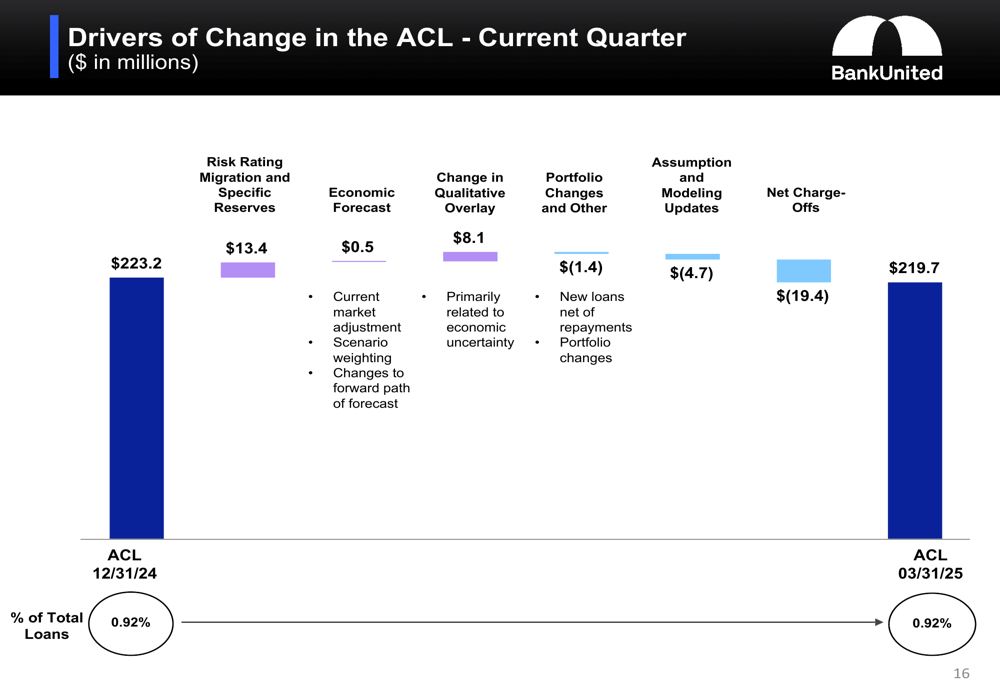

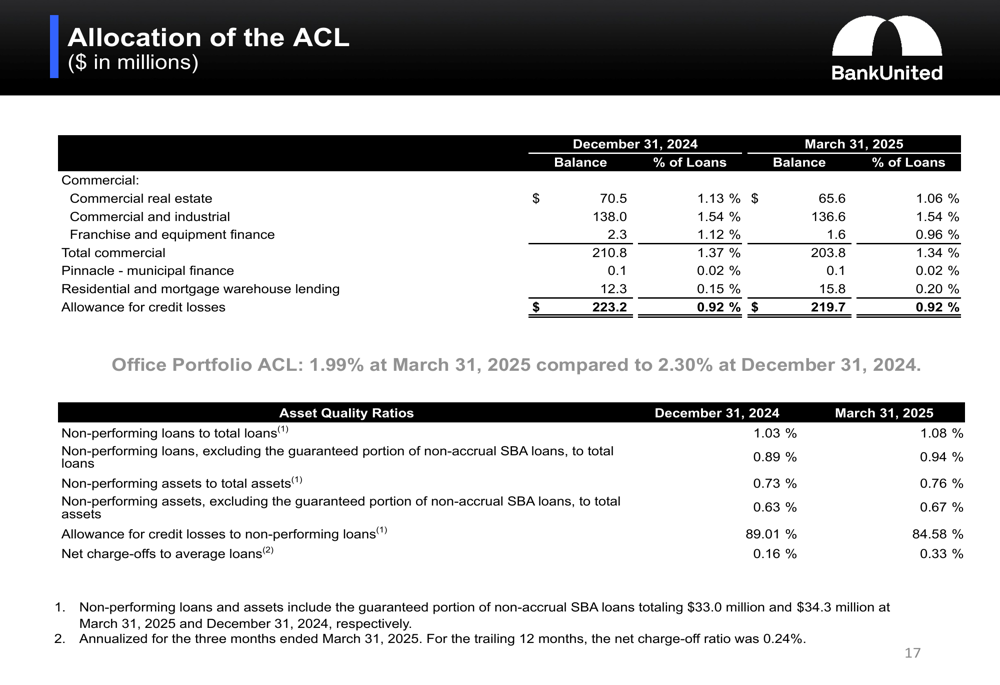

BankUnited maintained its allowance for credit losses (ACL) at 0.92% of total loans, unchanged from the previous quarter. The commercial ACL stood at 1.34%, while the office portfolio ACL was 1.99%, down from 2.30% at the end of 2024.

The following chart illustrates the drivers of change in the ACL during Q1 2025:

Risk rating migration and specific reserves added $13.4 million to the ACL, while net charge-offs of $19.4 million reduced the reserve. The annualized net charge-off rate was 0.33% for the quarter, compared to 0.24% for the trailing 12 months.

The allocation of the ACL across different loan segments shows the bank’s risk assessment by portfolio:

Strategic Initiatives and Outlook

BankUnited’s presentation emphasized its near-term strategic priorities, including improving its funding profile, enhancing asset mix, managing net interest margin, maintaining credit quality, and preserving strong liquidity and capital positions.

The bank’s capital ratios remain robust, with a CET1 ratio of 12.2% and a tangible common equity to tangible assets ratio of 8.11%. Same-day available liquidity stood at $15.6 billion, providing ample flexibility.

While the presentation did not provide specific forward guidance, the Q4 2024 earnings call (the most recent available) had projected mid to high single-digit growth in net interest income for 2025, with the net interest margin expected to reach 3% by the latter half of the year. The bank had also anticipated mid-single-digit deposit growth and low single-digit loan growth.

BankUnited’s Q1 2025 results show progress toward these goals, particularly in deposit growth and mix improvement, though the sequential decline in earnings suggests ongoing challenges in the current operating environment. The bank’s conservative approach to credit risk and strong capital position provide a solid foundation as it continues to execute its strategic priorities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.