How are energy investors positioned?

Banner Corporation (NASDAQ:BANR) reported steady financial performance in its second quarter 2025 presentation, showcasing continued loan growth and stable interest margins despite ongoing economic uncertainties. The regional bank, which operates primarily in the Pacific Northwest and California, maintained its focus on its "super community bank" strategy while leveraging the diverse economic drivers in its operating regions.

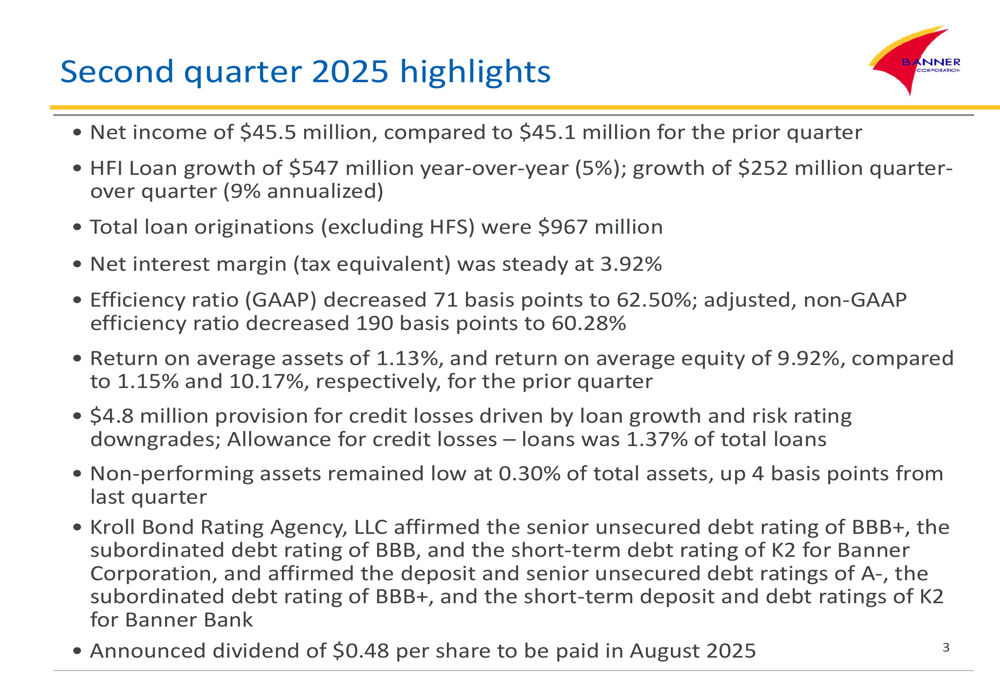

Quarterly Performance Highlights

Banner reported net income of $45.5 million for Q2 2025, a slight improvement from the $45.1 million reported in the previous quarter. The company maintained a steady net interest margin of 3.92% while improving its efficiency ratio, which decreased by 71 basis points to 62.50% on a GAAP basis. The adjusted non-GAAP efficiency ratio showed even greater improvement, decreasing 190 basis points to 60.28%.

As shown in the following quarterly highlights summary:

Return metrics showed a slight decline compared to the previous quarter, with return on average assets at 1.13% (down from 1.15%) and return on average equity at 9.92% (down from 10.17%). The company announced a quarterly dividend of $0.48 per share to be paid in August 2025, continuing its commitment to shareholder returns.

Banner’s stock closed at $66.71 on July 16, 2025, with a slight after-hours increase of 0.06%, reflecting investor confidence following the earnings announcement. The stock has traded between $51.14 and $78.05 over the past 52 weeks.

Strategic Positioning and Growth Drivers

Banner continues to benefit from its strategic positioning in high-growth regions. The company’s presentation highlighted that it operates in areas with strong population growth projections, particularly Idaho, which is expected to grow by 20% by 2030. This geographic advantage supports Banner’s expansion strategy and potential for continued deposit and loan growth.

The company’s operating region features a diverse economic base with major companies across multiple sectors, providing resilience against industry-specific downturns. This diversity is illustrated in the following image showing key economic drivers in Banner’s markets:

Banner’s reputation and service quality continue to be recognized through various awards and certifications, reinforcing its market position and ability to attract and retain customers. These accolades include J.D. Power’s recognition for customer satisfaction in retail banking in the Northwest and being named among America’s Best Regional Banks.

The following image showcases Banner’s awards and certifications:

Financial Performance and Revenue Trends

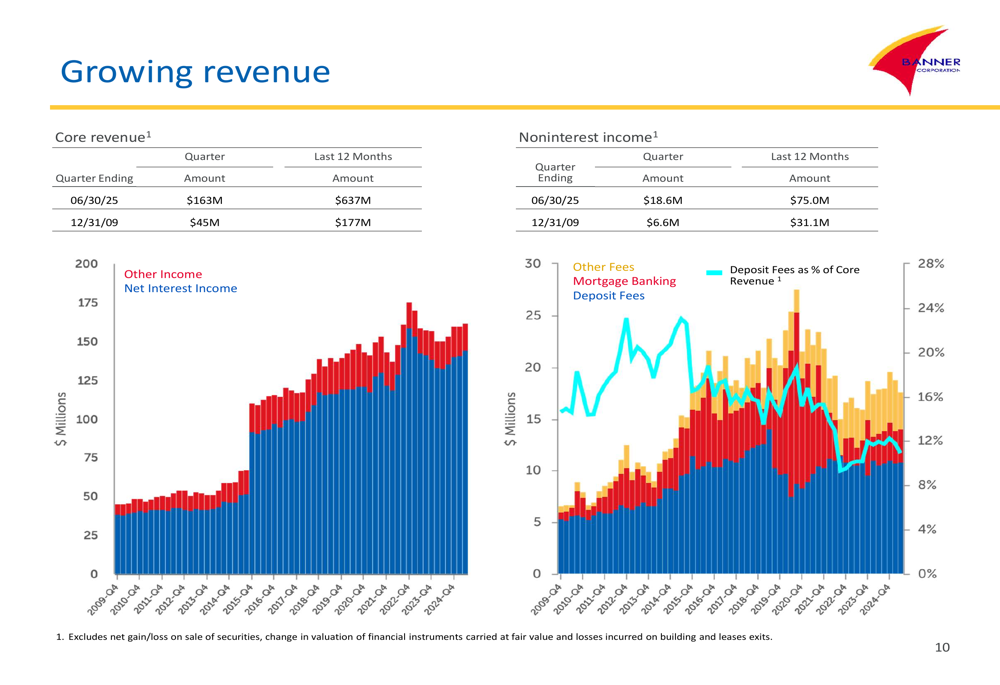

Banner’s core revenue has shown consistent growth over time, with both net interest income and non-interest income contributing to overall performance. The presentation highlighted the evolution of these revenue streams since 2009, demonstrating the bank’s ability to grow its business organically and through strategic acquisitions.

As shown in the following chart of revenue trends:

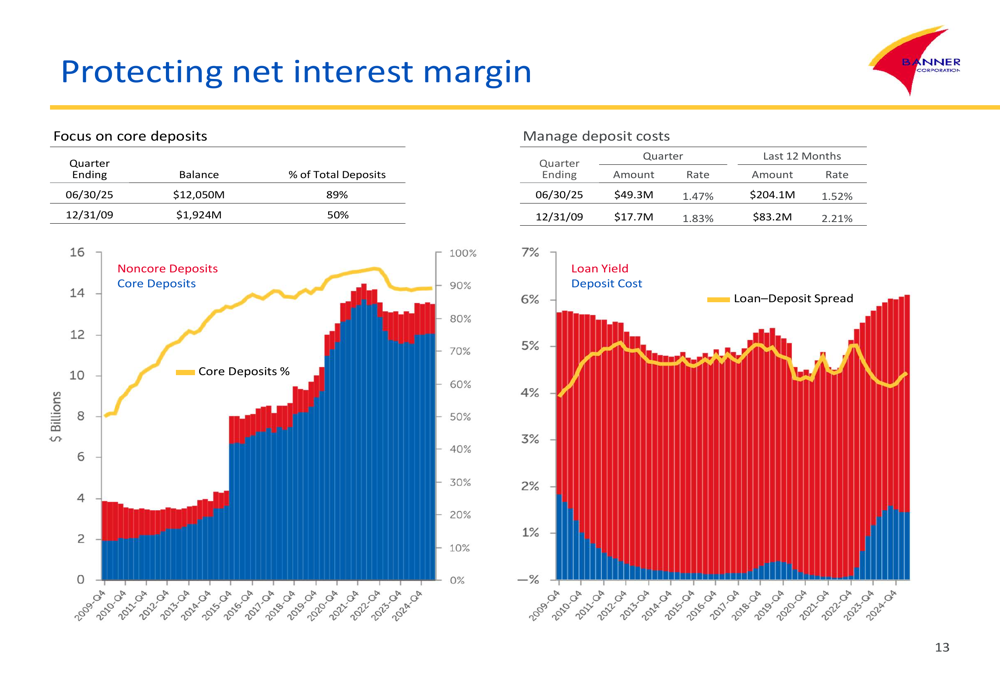

The company’s funding mix remains a strength, with core deposits representing 89% of total deposits ($12,050 million). This favorable deposit composition helps Banner maintain competitive funding costs and supports its net interest margin. The loan-to-deposit ratio is being actively managed to balance growth opportunities with liquidity considerations.

The following chart illustrates Banner’s deposit mix and loan-deposit spread:

Loan Portfolio and Credit Quality

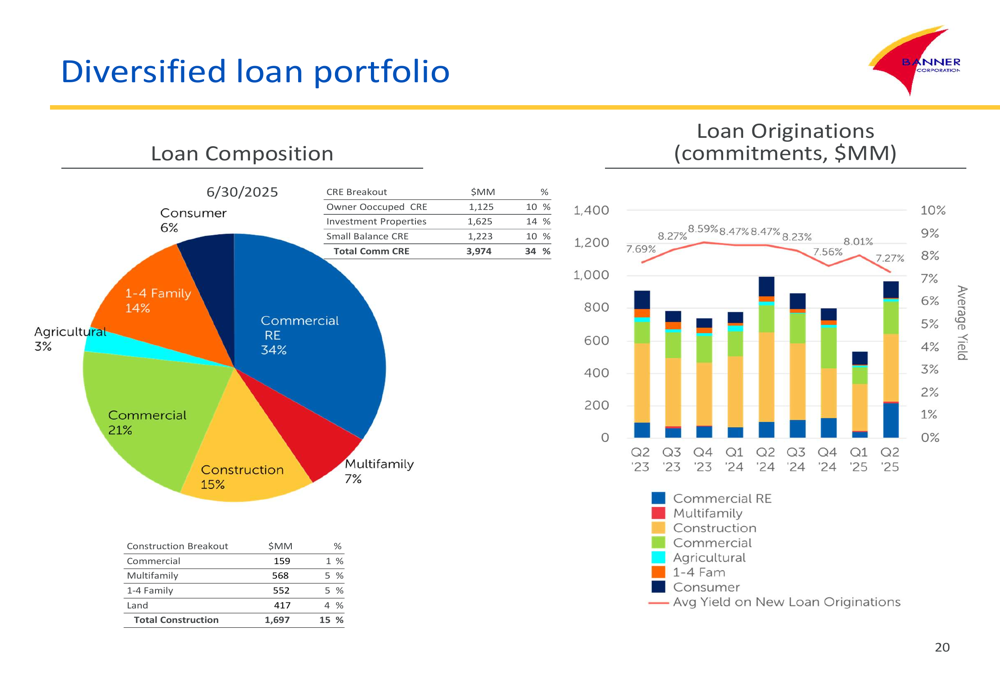

Banner reported healthy loan growth, with held-for-investment loans increasing by $547 million year-over-year (5%) and $252 million quarter-over-quarter (9% annualized). Total (EPA:TTEF) loan originations (excluding held-for-sale) were $967 million for the quarter. The loan portfolio remains diversified across various segments, with commercial real estate representing the largest portion at 34%.

The composition of Banner’s loan portfolio is illustrated in the following chart:

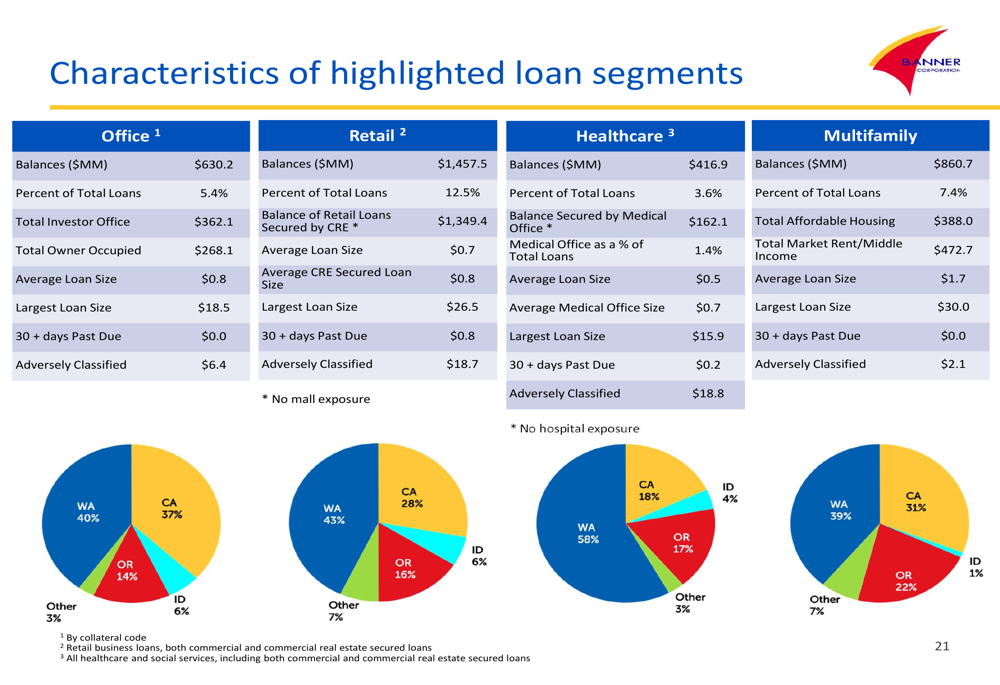

The presentation provided detailed analysis of specific loan segments, including office, retail, healthcare, and multifamily properties. This granular view demonstrates Banner’s thorough understanding of its credit exposures and risk management approach.

The following image details the characteristics of these highlighted loan segments:

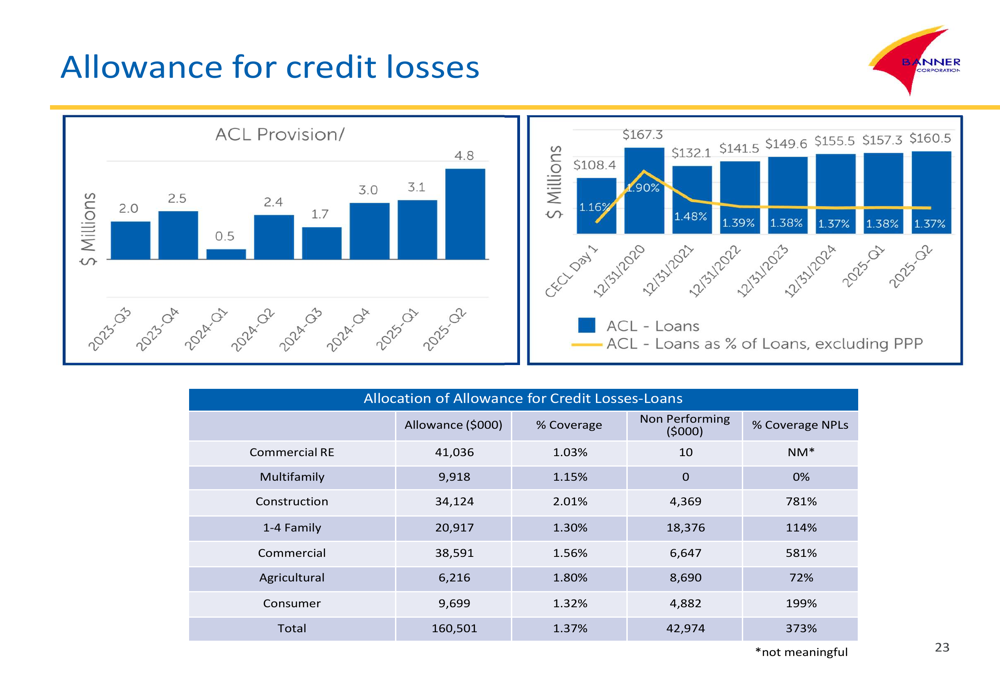

Credit quality metrics remained generally strong, though the company reported a $4.8 million provision for credit losses driven by loan growth and risk rating downgrades. Non-performing assets remained low at 0.30% of total assets, though this represented a 4 basis point increase from the previous quarter. The allowance for credit losses on loans stood at 1.37% of total loans.

The following chart shows the allowance for credit losses:

Investment Portfolio and Interest Rate Sensitivity

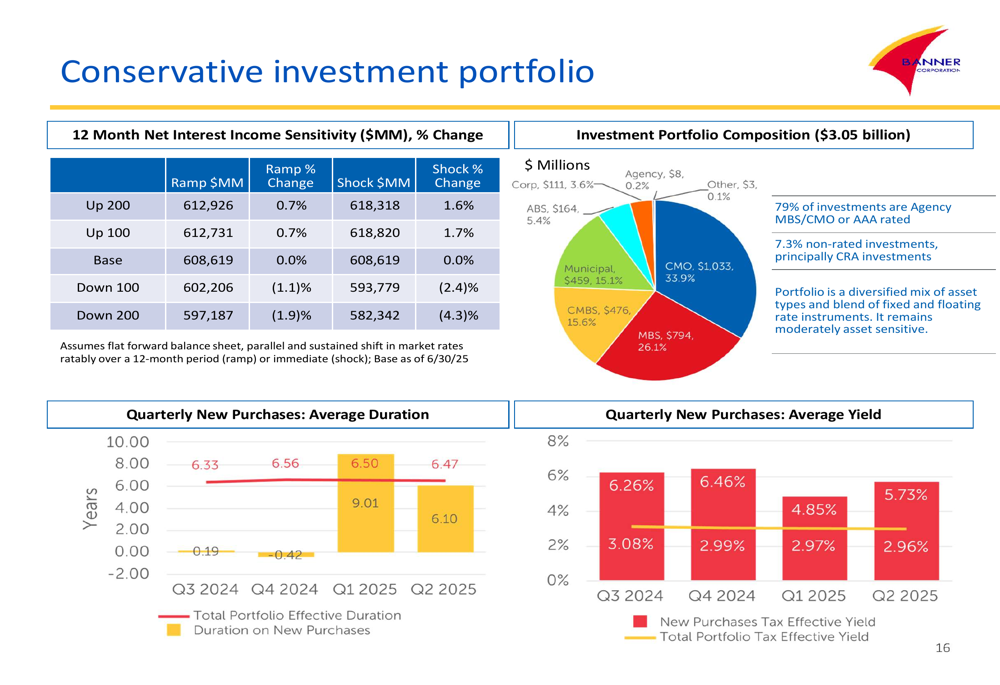

Banner maintains a $3.05 billion investment portfolio, with 79% of investments in Agency MBS/CMO or AAA-rated securities. This conservative approach to investments aligns with the company’s moderate risk profile while providing liquidity and income.

The company’s interest rate sensitivity analysis suggests limited exposure to interest rate changes, with a projected 1.6% increase in net interest income in a +200 basis point scenario and a 4.3% decrease in a -200 basis point scenario.

The following image details Banner’s investment portfolio composition and interest rate sensitivity:

Expense Management and Efficiency

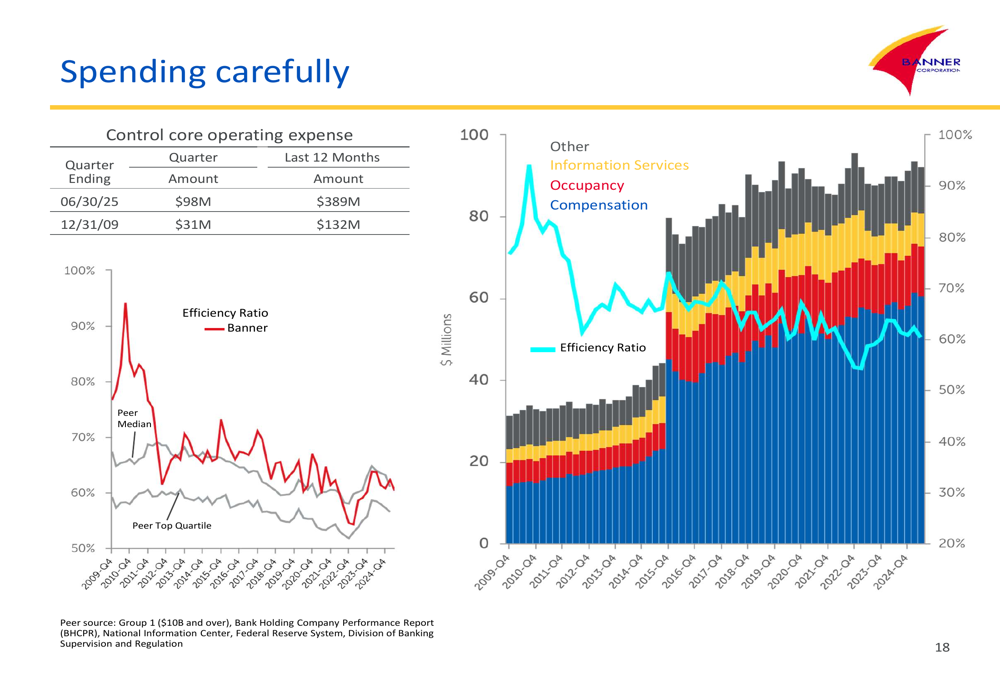

Banner demonstrated improved expense management, as evidenced by the declining efficiency ratio. The presentation highlighted the company’s focus on controlling core operating expenses while achieving benefits from scale. This disciplined approach to expenses supports profitability in a challenging interest rate environment.

As shown in the following chart of operating expense trends:

Outlook and Forward Strategy

Looking ahead, Banner appears well-positioned to continue executing its "super community bank" strategy, focusing on decision-making close to clients, broad product offerings, and community investment. The company’s strong capital position, diversified loan portfolio, and presence in growing markets provide a solid foundation for future growth.

While the presentation did not provide specific forward guidance, the company’s emphasis on maintaining a moderate risk profile, protecting net interest margin, and employing capital wisely suggests a continued conservative approach to growth and risk management in the coming quarters.

Banner’s management continues to focus on building value for shareholders through top-quartile financial performance, for clients through superior service and products, for employees through opportunity and reward, and for communities through capital provision and involvement.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.