How are energy investors positioned?

Introduction & Market Context

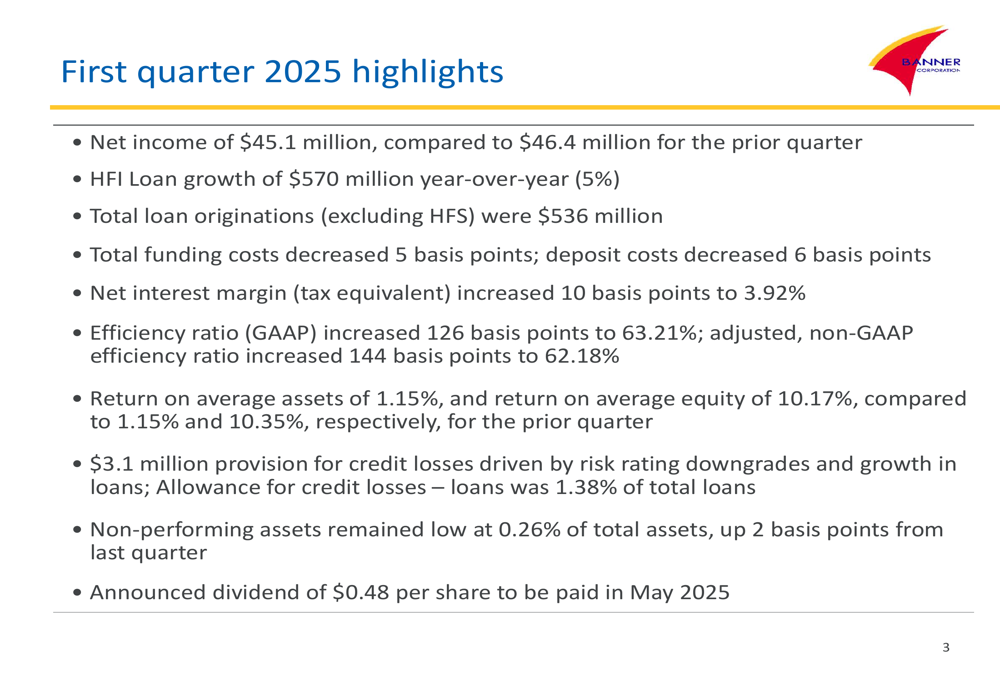

Banner Corporation (NASDAQ:BANR) released its first quarter 2025 presentation on April 17, 2025, highlighting improved net interest margin and continued loan growth despite a challenging banking environment. The company reported net income of $45.1 million for Q1 2025, compared to $46.4 million in the previous quarter. Banner’s stock closed at $59.68 on April 16, 2025, trading well above its 52-week low of $42 but still below its 52-week high of $78.05.

The regional bank, which operates 135 offices across Washington, Oregon, Idaho, and California, continues to leverage its strong market position in regions experiencing above-average population growth, particularly in Idaho where 20% growth is projected between 2020-2030.

Quarterly Performance Highlights

Banner’s Q1 2025 results demonstrated resilience in a competitive banking landscape. The company reported a 10 basis point increase in net interest margin (tax equivalent) to 3.92%, reflecting improved earning asset yields and lower funding costs. This represents a continued improvement from the 3.72% NIM reported in Q3 2024.

As shown in the following chart of quarterly highlights, Banner achieved held-for-investment loan growth of $570 million year-over-year (5%), while maintaining strong credit quality with non-performing assets at just 0.26% of total assets:

Total (EPA:TTEF) loan originations (excluding held-for-sale) reached $536 million for the quarter. The company’s efficiency ratio (GAAP) increased 126 basis points to 63.21%, indicating some pressure on operational efficiency. Return on average assets remained steady at 1.15%, while return on average equity was 10.17%, compared to 10.35% in the previous quarter.

Banner’s provision for credit losses was $3.1 million, driven by risk rating downgrades and loan growth. The allowance for credit losses stood at 1.38% of total loans, providing substantial coverage against potential loan losses.

Strategic Positioning

Banner continues to position itself as a "super community bank" with a focus on middle market, small business, and consumer clients. The company’s strategic approach centers on five core banking competencies: growing revenue, protecting net interest margin, spending carefully, maintaining a moderate risk profile, and employing capital wisely.

The bank operates in regions with diverse economic drivers, including major technology companies, manufacturing, consumer brands, logistics, natural resources, and agriculture. This economic diversity provides resilience against sector-specific downturns.

As illustrated in the following image highlighting the economic diversity in Banner’s footprint, the company benefits from proximity to major corporations and industries:

Banner’s reputation in the marketplace continues to strengthen, as evidenced by numerous awards and recognitions. The company has been named among the Most Trustworthy Companies in America by Newsweek for 2023 and 2024, received the Best in Customer Satisfaction for Retail Banking in the Northwest from J.D. Power, and has been included in Forbes’ 100 Best Banks in America for nine consecutive years (2017-2025).

The following image showcases Banner’s impressive collection of industry recognitions:

Loan Portfolio and Credit Quality

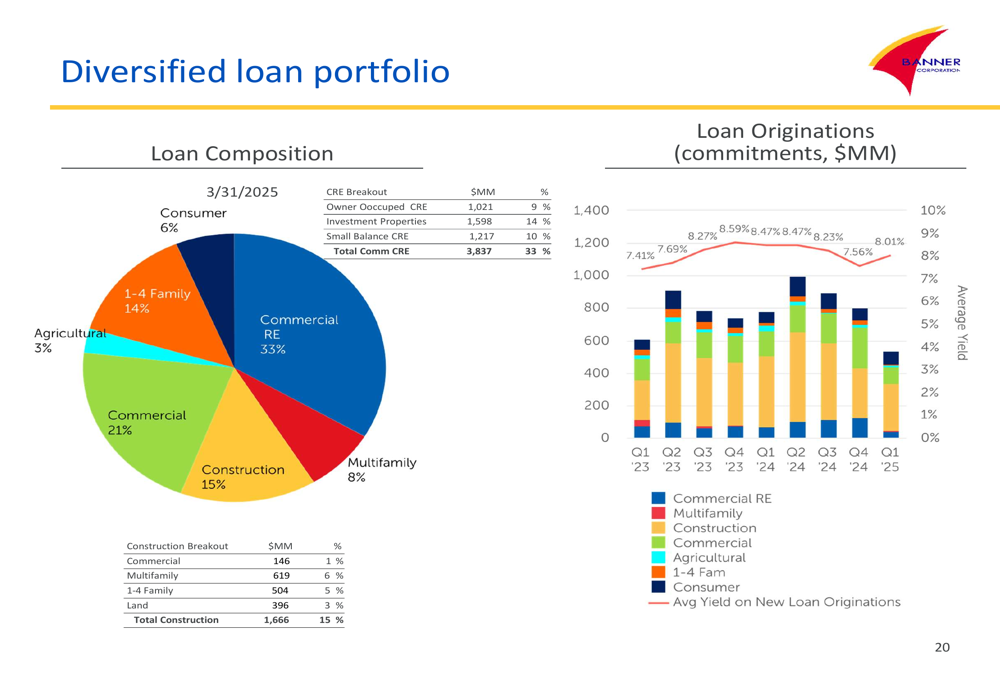

Banner maintains a diversified loan portfolio, which helps mitigate concentration risks. As of March 31, 2025, the portfolio composition was: Commercial Real Estate (33%), Commercial (21%), Construction (15%), 1-4 Family (14%), Multifamily (8%), Consumer (6%), and Agricultural (3%).

The company’s loan portfolio composition and origination trends are illustrated in the following chart:

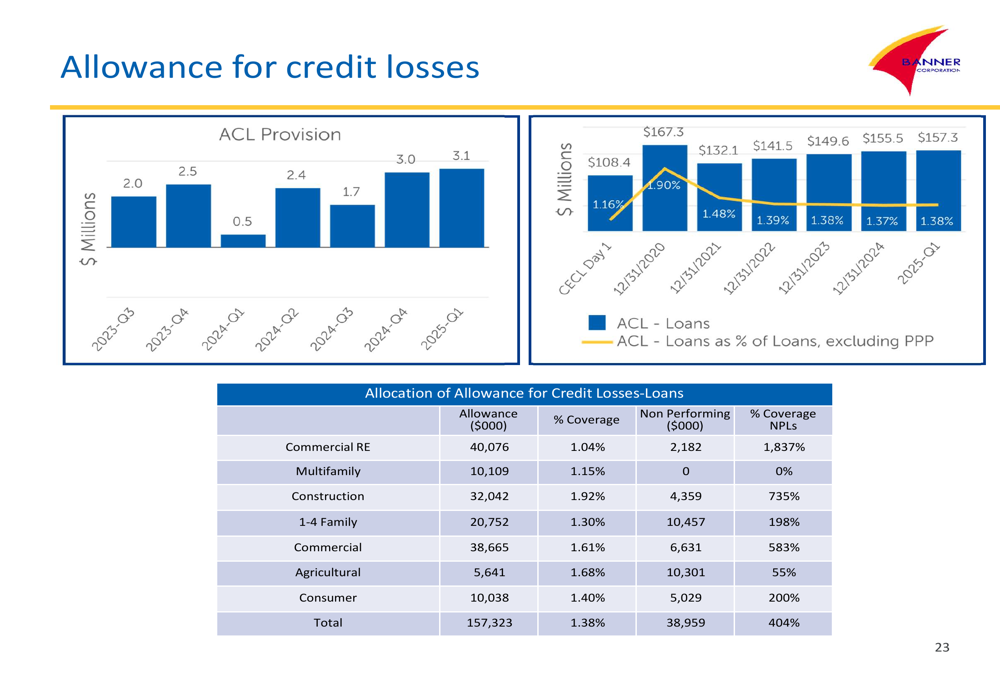

Credit quality remains strong, with non-performing assets at just 0.26% of total assets, up slightly by 2 basis points from the previous quarter. The allowance for credit losses provides 404% coverage of non-performing loans, indicating substantial protection against potential losses.

The following chart details Banner’s allowance for credit losses across different loan categories:

Funding and Liquidity

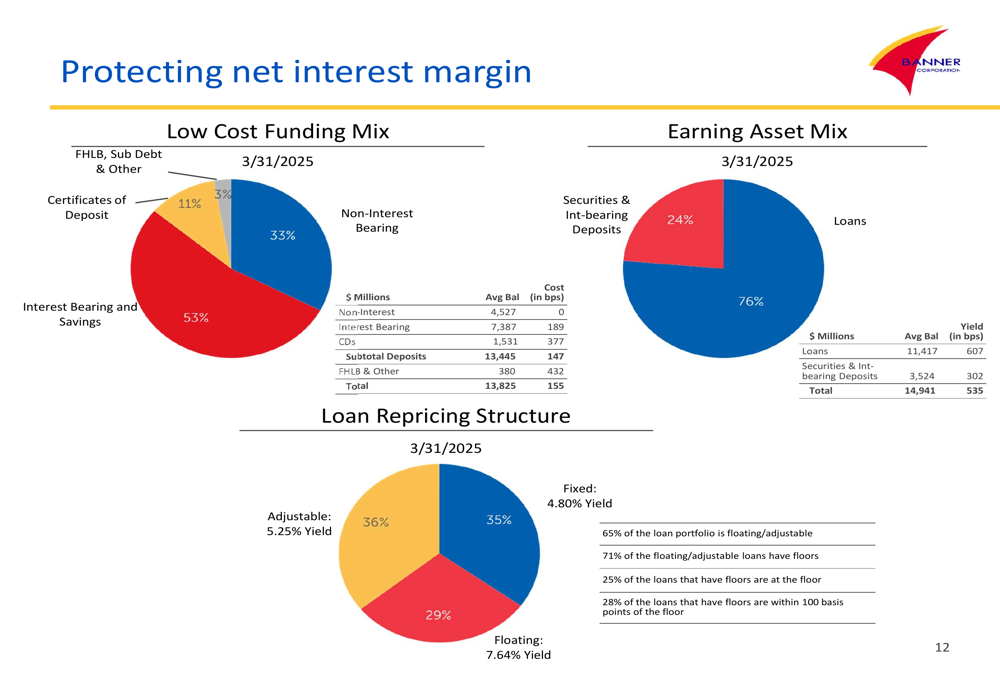

Banner’s funding strategy continues to emphasize core deposits, which represented 89% of total deposits as of Q1 2025. This strong core deposit base provides stable, low-cost funding for the bank’s operations. Total funding costs decreased 5 basis points during the quarter, while deposit costs decreased 6 basis points.

The company’s funding mix and earning asset composition are illustrated below:

Banner’s loan repricing structure is well-balanced, with 35% fixed-rate loans (4.80% yield), 29% floating-rate loans (7.64% yield), and 36% adjustable-rate loans (5.25% yield). This balanced approach helps the bank manage interest rate risk while maintaining strong yields.

The investment portfolio totals $3.10 billion and is conservatively positioned, with 79% of investments in Agency MBS/CMO or AAA-rated securities. This conservative approach helps maintain liquidity while managing interest rate risk.

Forward Outlook

Banner’s presentation emphasized its continued focus on building value for stakeholders through its core banking competencies. The company’s strong presence in growing markets, particularly in the Pacific Northwest and Idaho, positions it well for continued organic growth.

The bank’s focus on relationship banking and its super community bank model should continue to drive deposit growth and client acquisition. Banner’s strong capital position, with tangible common equity per share increasing 24% from the same period last year, provides flexibility for potential acquisitions, dividend payments, and share repurchases.

Banner announced a quarterly dividend of $0.48 per share to be paid in May 2025, demonstrating its commitment to returning capital to shareholders. This consistent dividend policy aligns with the company’s strategy of employing capital wisely while maintaining strong regulatory capital ratios.

Looking ahead, Banner appears well-positioned to navigate the current banking environment with its diversified loan portfolio, strong deposit base, and improved net interest margin. The company’s presence in economically diverse and growing regions should provide opportunities for continued expansion, while its conservative credit approach helps mitigate potential risks in an uncertain economic environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.