Intel surges more than 8% after chipmaker’s profits top expectations

Introduction & Market Context

Baytex Energy Corp (NYSE:BTE) (TSX:BTE) released its May 2025 investor presentation outlining the company’s strategic priorities, operational outlook, and financial targets. The North American oil and gas producer is navigating a challenging market environment, with its stock currently trading at $1.53, down 6.71% in the most recent session and significantly below its 52-week high of $3.84.

The presentation comes after Baytex reported strong Q3 2024 results, which included CAD 220 million in free cash flow generation and increased production averaging over 154,000 BOE per day. However, the May 2025 outlook suggests a more conservative approach moving forward, with production targets adjusted to reflect current market realities.

Executive Summary

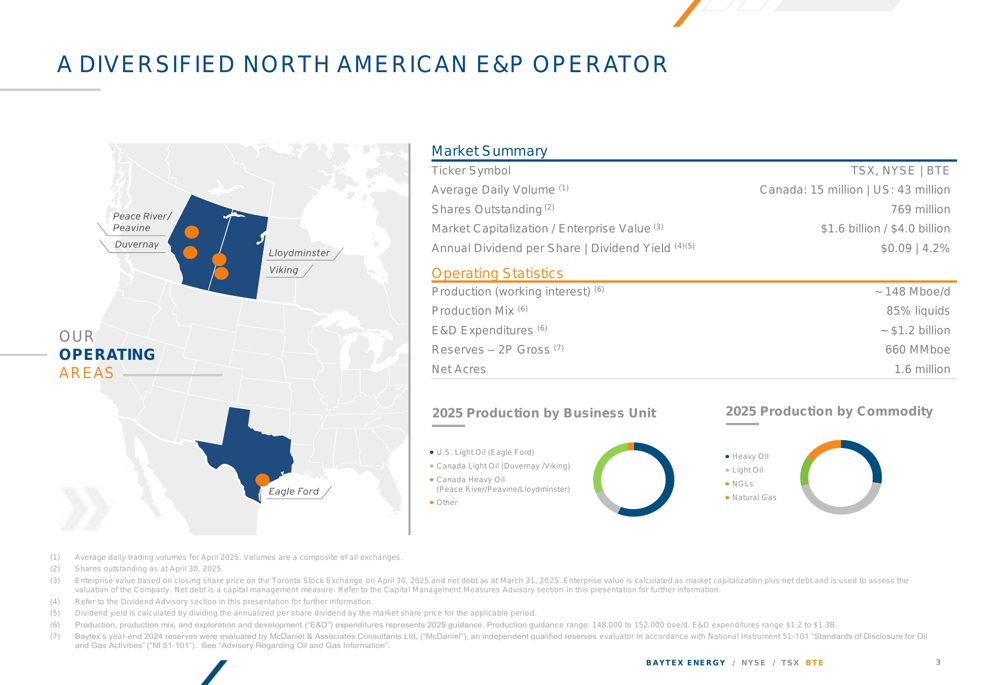

Baytex positions itself as a diversified North American energy producer with approximately 148,000 boe/d of production (85% liquids) and a market capitalization of $1.6 billion. The company’s strategy centers on disciplined capital allocation, prioritizing free cash flow generation, debt reduction, and shareholder returns through dividends and share repurchases.

As shown in the following overview of Baytex’s operational footprint and production mix:

The company maintains a balanced portfolio across U.S. and Canadian assets, with operations in the Eagle Ford (Texas), Duvernay and Viking (Canada Light Oil), and Peace River, Peavine, and Lloydminster (Canada Heavy Oil) regions. This diversification provides operational flexibility and multiple avenues for value creation.

Production and Financial Outlook for 2025

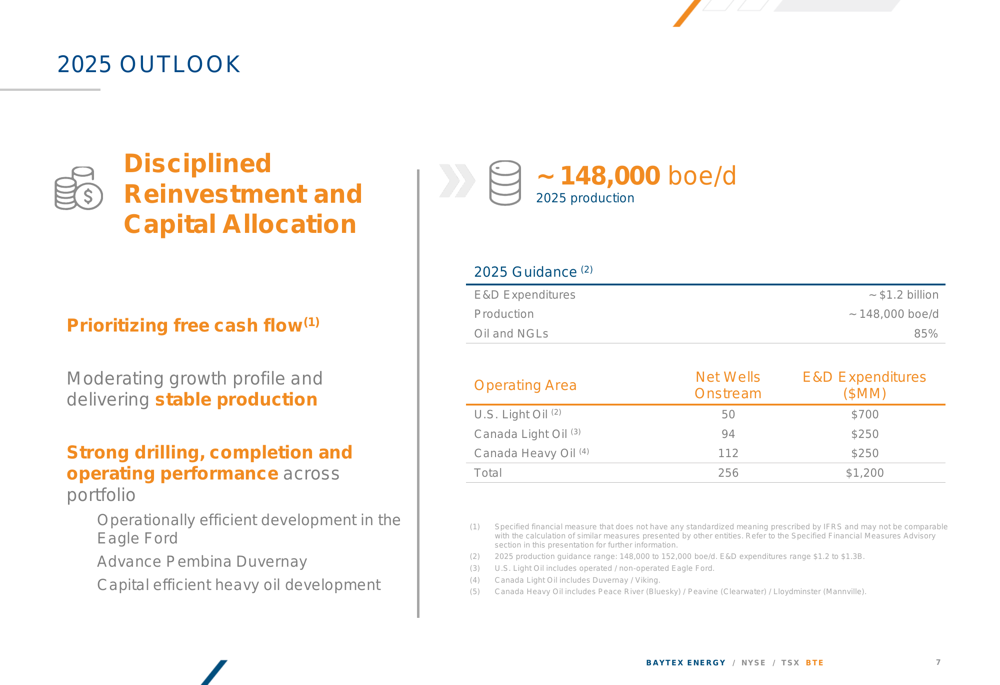

For 2025, Baytex is targeting production of approximately 148,000 boe/d with exploration and development expenditures of $1.2 billion. This represents a slight decrease from the production levels reported in Q3 2024 (over 154,000 BOE/d), suggesting a more conservative outlook amid market volatility.

The company’s 2025 plan emphasizes operational efficiency and free cash flow generation across its portfolio:

Free cash flow projections for 2025 are estimated at $60 million at $60 WTI, $65 million at $65 WTI, and $70 million at $70 WTI. These projections highlight the company’s sensitivity to oil prices and reflect a cautious approach to financial planning.

Baytex’s capital program for 2025 includes bringing 50 wells onstream in U.S. Light Oil operations, 94 wells in Canada Light Oil, and 112 wells in Canada Heavy Oil. The company is targeting a 7% improvement in drilling and completion costs per lateral foot in its Eagle Ford operations compared to 2024.

Strategic Initiatives

Baytex has outlined three key investment pillars in its presentation: disciplined reinvestment and capital allocation, shareholder returns, and financial strength.

The company’s investment highlights emphasize these strategic priorities:

In terms of capital allocation, Baytex is prioritizing free cash flow generation from its high-quality, oil-weighted portfolio. The company has demonstrated a track record of new discoveries and efficient development, particularly in its Canadian heavy oil assets.

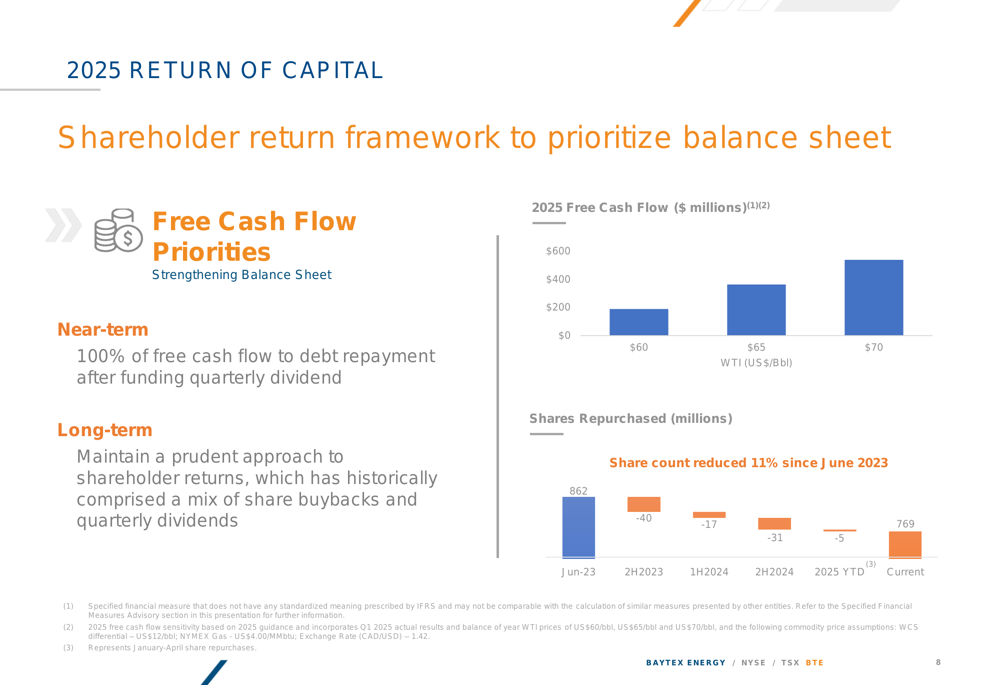

For shareholder returns, Baytex maintains an annual dividend of $0.09 per share (yielding 4.2% at current prices) and has repurchased 11% of its shares since June 2023. The company’s return of capital framework prioritizes balance sheet strength while providing sustainable returns to shareholders:

Five-Year Strategic Plan (2024-2028)

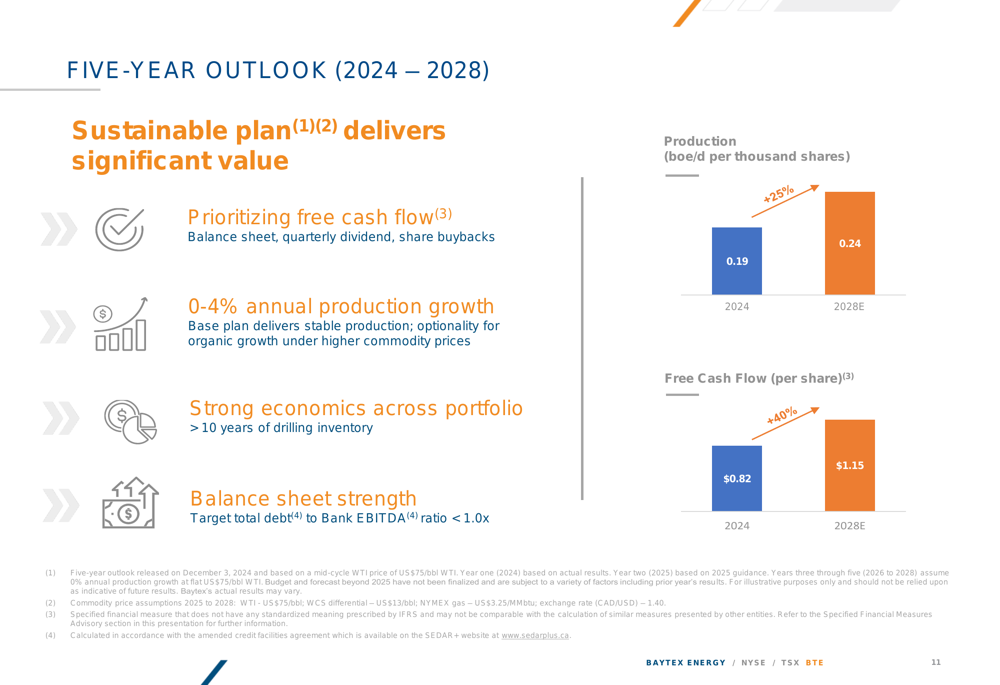

Looking beyond 2025, Baytex has outlined an ambitious five-year plan targeting production growth of 0-4% annually while prioritizing free cash flow generation and debt reduction.

The company projects significant improvements in key metrics through 2028:

Production per share is expected to increase by 25% from 2024 to 2028, while free cash flow per share is projected to grow by 40% over the same period. These targets are based on maintaining a disciplined capital allocation strategy and leveraging operational efficiencies across the portfolio.

Asset Portfolio and Business Unit Performance

Baytex’s diversified asset base provides multiple avenues for value creation, with each business unit contributing to the company’s overall strategy:

The Eagle Ford assets in the U.S. represent the largest component of production (82,000 boe/d in 2025E) and generate 55% of asset-level free cash flow. These assets feature approximately 800 drilling locations with IRRs ranging from 45-90%.

In Canada Light Oil, the Viking and Duvernay assets contribute 18,000 boe/d (2025E) with approximately 1,200 drilling locations. While these assets generate only 5% of asset-level free cash flow currently, the company sees significant growth potential in the Pembina Duvernay, where it plans to bring 9 net wells onstream in 2025.

The Canada Heavy Oil assets, including Peace River, Peavine (Clearwater), and Lloydminster, contribute 44,000 boe/d (2025E) with 96% liquids content. These assets generate 40% of asset-level free cash flow and feature approximately 900 drilling locations with exceptional IRRs (95% to over 250%) and rapid payouts (8-13 months).

Financial Position and Risk Management

Baytex is focused on maintaining financial strength and flexibility through prudent balance sheet management and risk mitigation strategies.

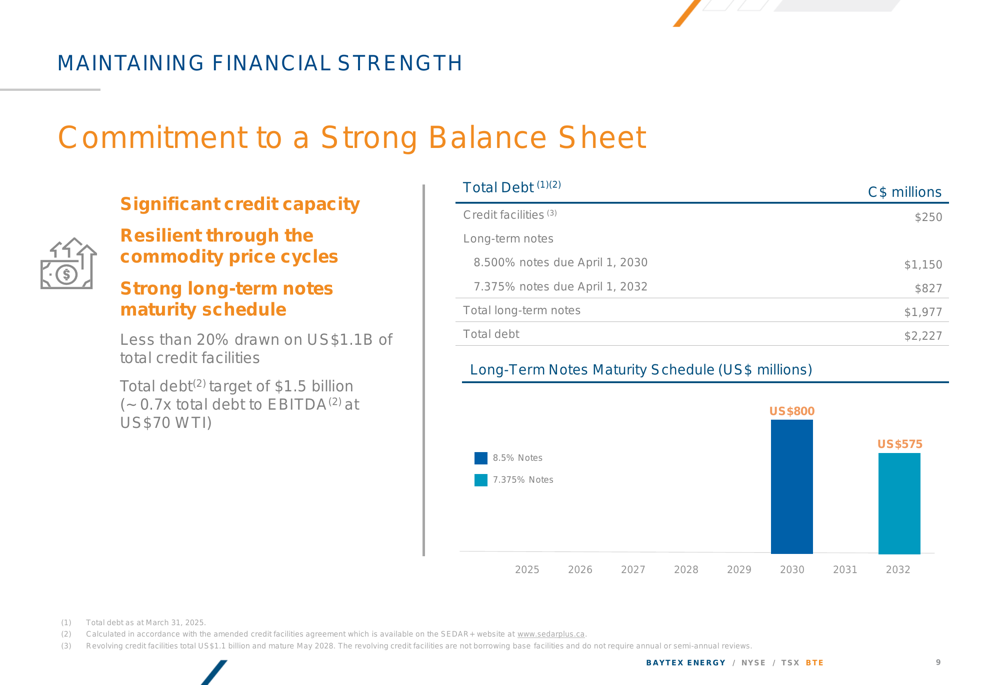

The company’s financial position includes significant credit capacity and a well-structured debt maturity profile:

Baytex has set a total debt target of $1.5 billion, representing approximately 0.7x total debt to EBITDA at US$70 WTI. This target represents a significant reduction from the CAD 2.5 billion net debt reported in Q3 2024, highlighting the company’s commitment to deleveraging.

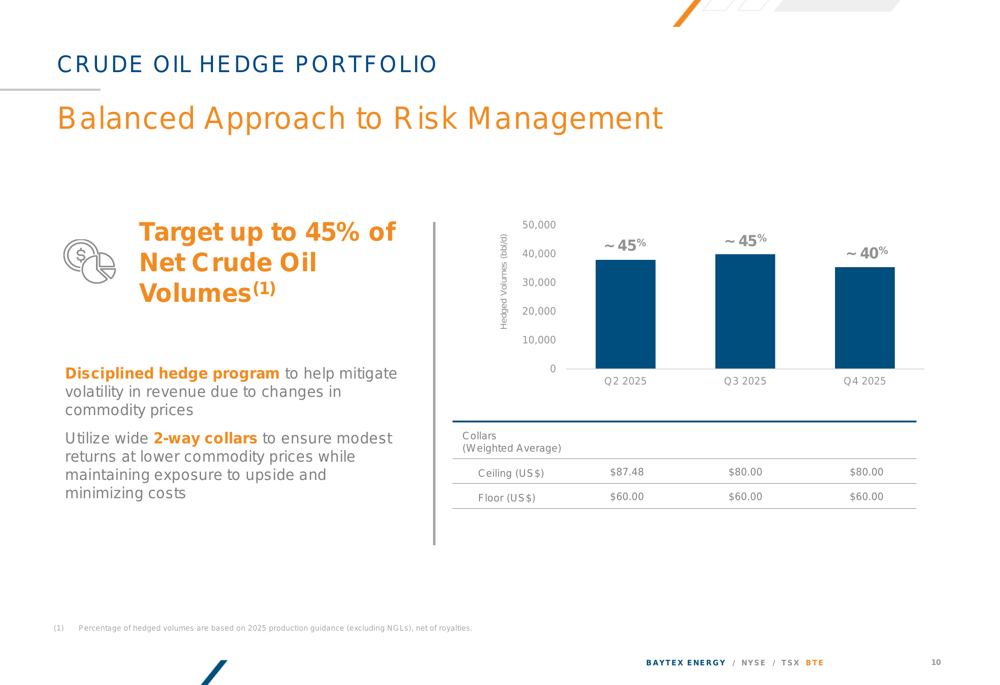

To manage commodity price risk, Baytex employs a balanced hedging strategy targeting up to 45% of net crude oil volumes:

The company utilizes wide 2-way collars to protect downside while maintaining upside exposure. For Q2-Q4 2025, Baytex has secured floor prices of US$60.00 with ceilings ranging from US$80.00 to US$87.48.

Market Context and Stock Performance

Despite the company’s operational achievements and strategic initiatives, Baytex’s stock has faced significant pressure. Trading at $1.53 (as of May 5, 2025), the shares are well below their 52-week high of $3.84 and have declined 6.71% in the most recent session.

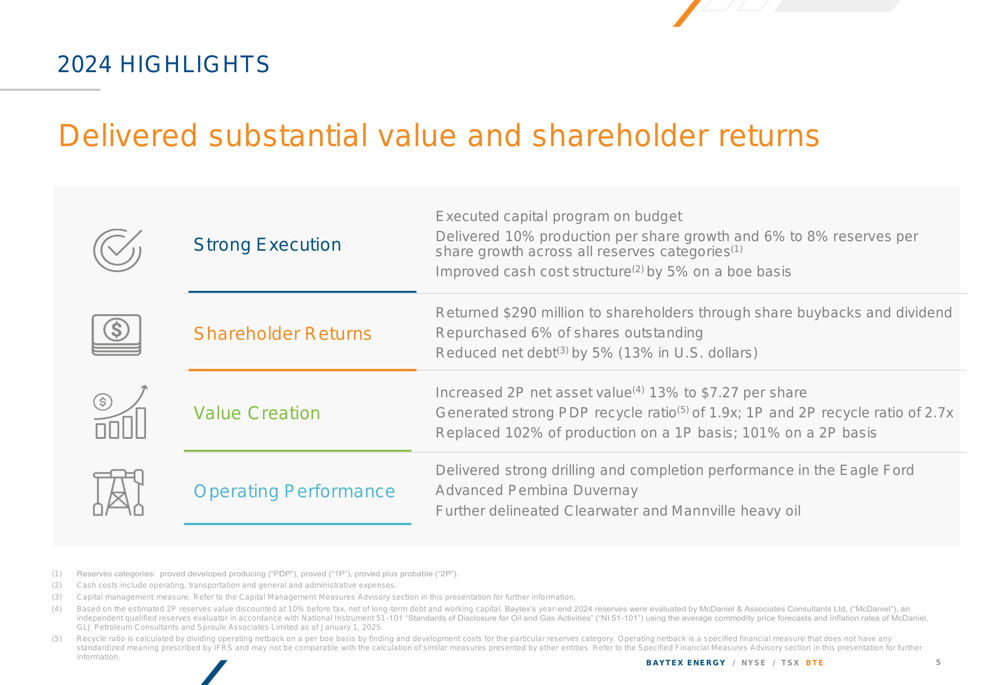

This stock performance contrasts with the company’s reported operational success in 2024, which included:

The disconnect between operational performance and stock price suggests investors may be concerned about broader industry challenges, including commodity price volatility and the long-term outlook for oil and gas producers amid energy transition pressures.

Baytex’s focus on debt reduction, free cash flow generation, and shareholder returns appears designed to address these market concerns and demonstrate the company’s commitment to creating sustainable value in a challenging environment.

In conclusion, Baytex Energy’s May 2025 investor presentation outlines a conservative but focused strategy emphasizing production stability, debt reduction, and shareholder returns. While the company faces market headwinds, its diversified asset base and disciplined capital allocation approach provide a foundation for navigating the current environment and potentially capitalizing on any improvement in commodity prices.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.