Street Calls of the Week

Executive Summary

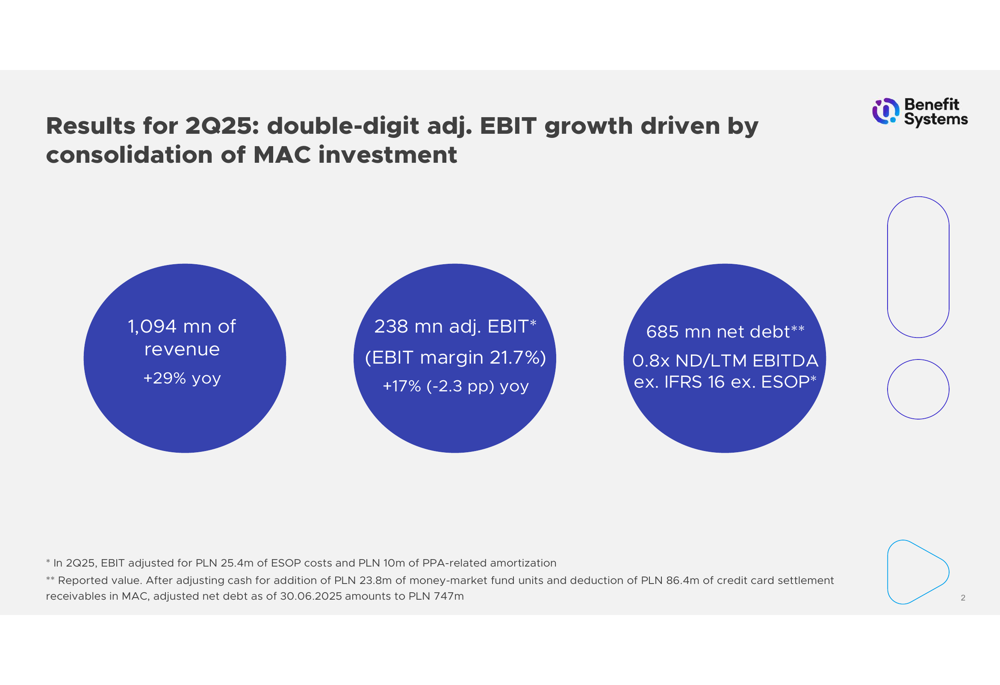

Benefit Systems SA (WSE:WA:BFT) reported strong financial results for the second quarter of 2025, with revenue reaching 1,094 million PLN, a 29% increase year-over-year. The growth was primarily driven by the consolidation of the MAC investment and continued strength in the company’s core Polish market. Adjusted EBIT rose 17% to 238 million PLN, with a margin of 21.7%.

As shown in the following financial highlights chart, the company maintained solid profitability despite significant investments in international expansion:

The company reported net debt of 685 million PLN at the end of Q2, representing a 0.8x net debt to EBITDA ratio (excluding IFRS 16 and ESOP costs). This debt position reflects the company’s recent acquisition activities, particularly the MAC investment that has contributed significantly to growth.

Quarterly Performance Highlights

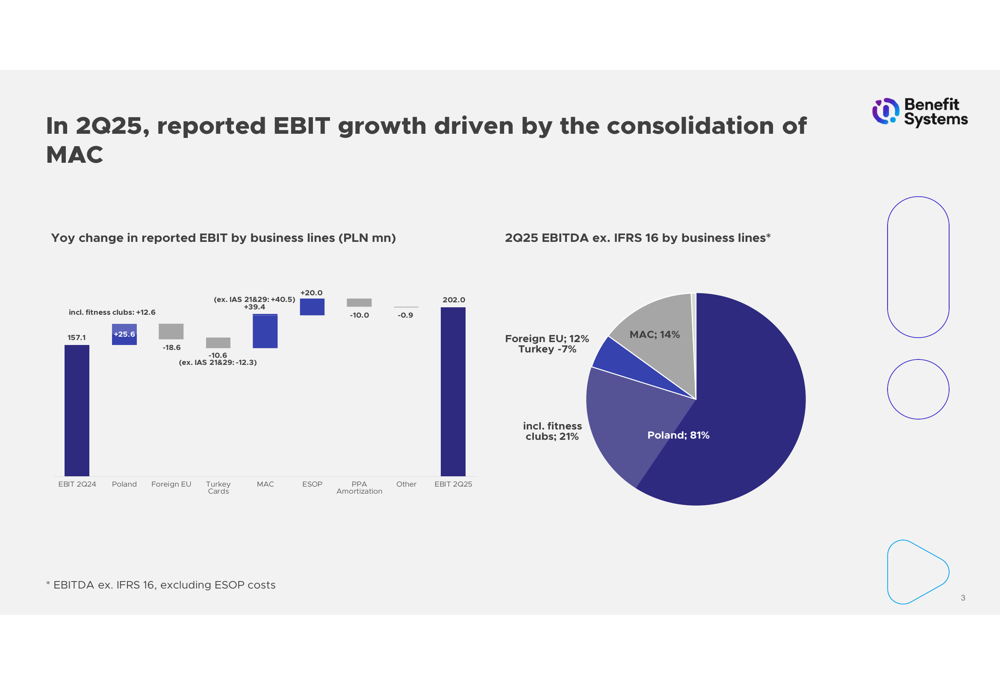

Benefit Systems’ EBIT growth was driven primarily by strong performance in Poland and the contribution from the MAC acquisition, which offset challenges in the Foreign EU segment. The following chart breaks down the reported EBIT growth by business line:

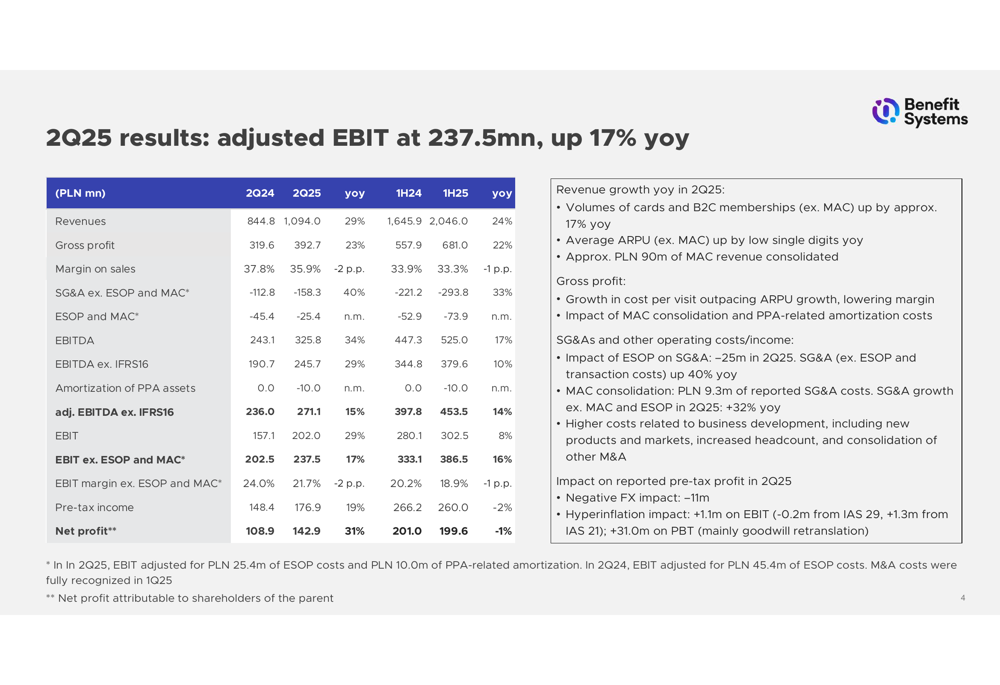

The detailed financial results show a 29% increase in revenue to 1,094 million PLN and a 23% increase in gross profit to 392.7 million PLN. While the gross margin decreased slightly by 2 percentage points to 35.9%, the company maintained strong profitability with adjusted EBIT growing 17% to 237.5 million PLN.

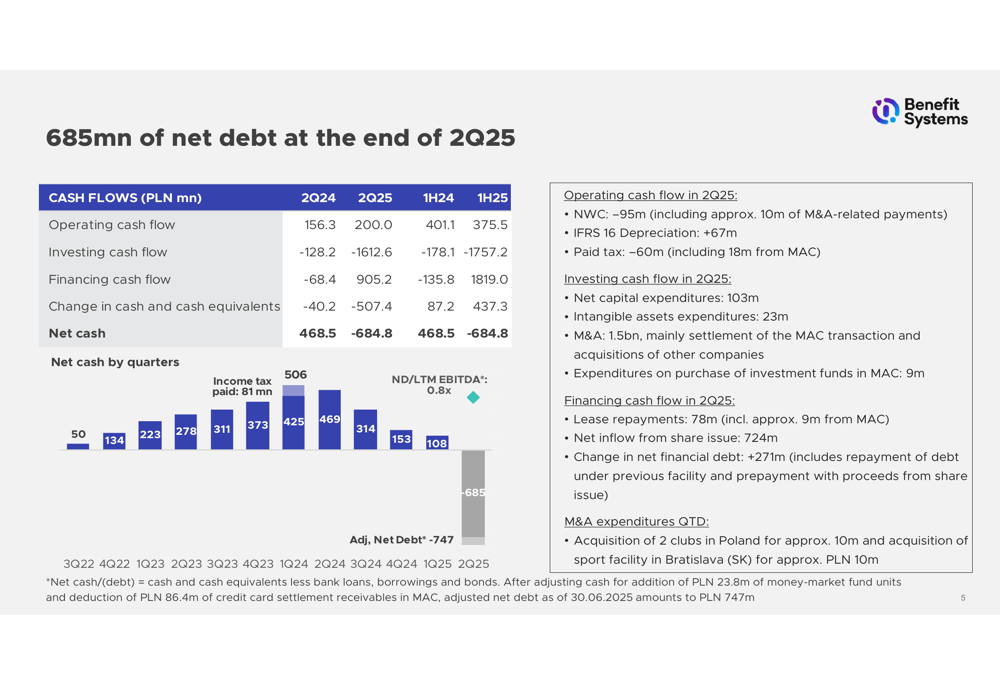

The company’s net debt position changed significantly, moving from a net cash position of 108 million PLN in Q1 2025 to a net debt of 685 million PLN at the end of Q2 2025. This shift was primarily due to investing activities related to acquisitions, as illustrated in the following chart:

Poland Segment: Core Market Strength

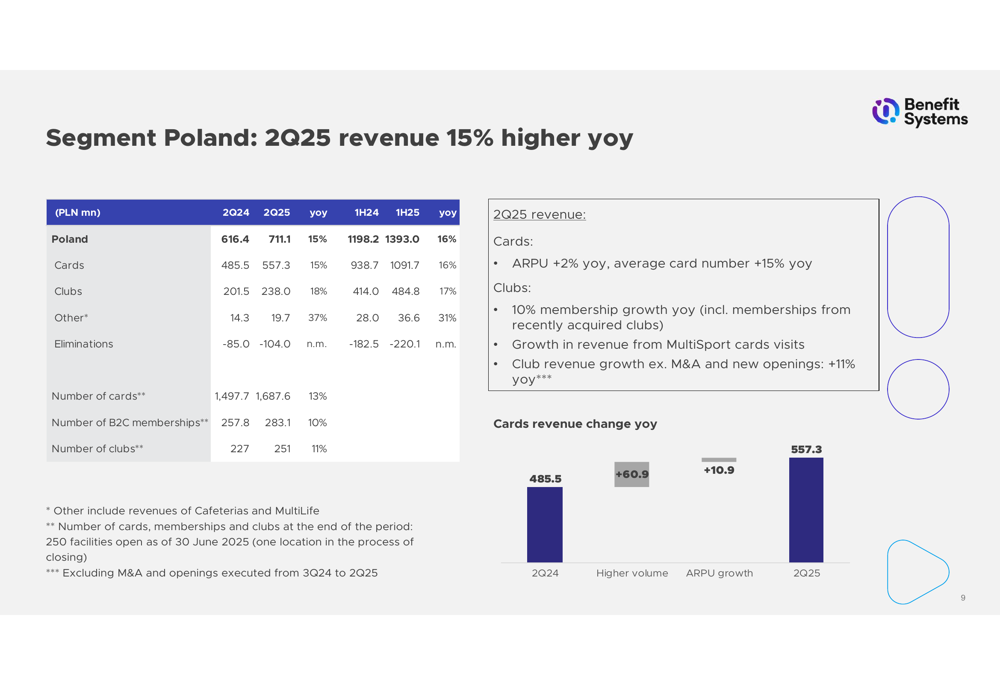

The Poland segment remains the cornerstone of Benefit Systems’ business, accounting for 81% of the group’s EBITDA. The segment showed strong performance with a 15% revenue increase to 711.1 million PLN and a 16% EBIT growth to 190.7 million PLN.

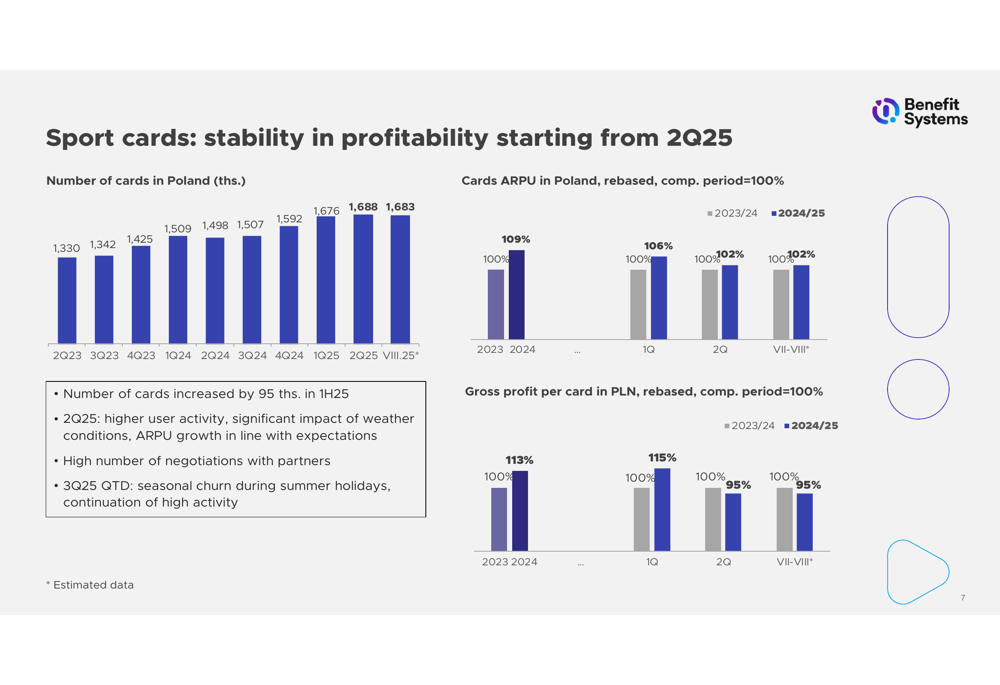

Sport cards in Poland continued to show robust growth, with the number of cards increasing to 1,687,600 by the end of Q2 2025, representing a 13% year-over-year increase. The following chart illustrates the steady growth in card numbers:

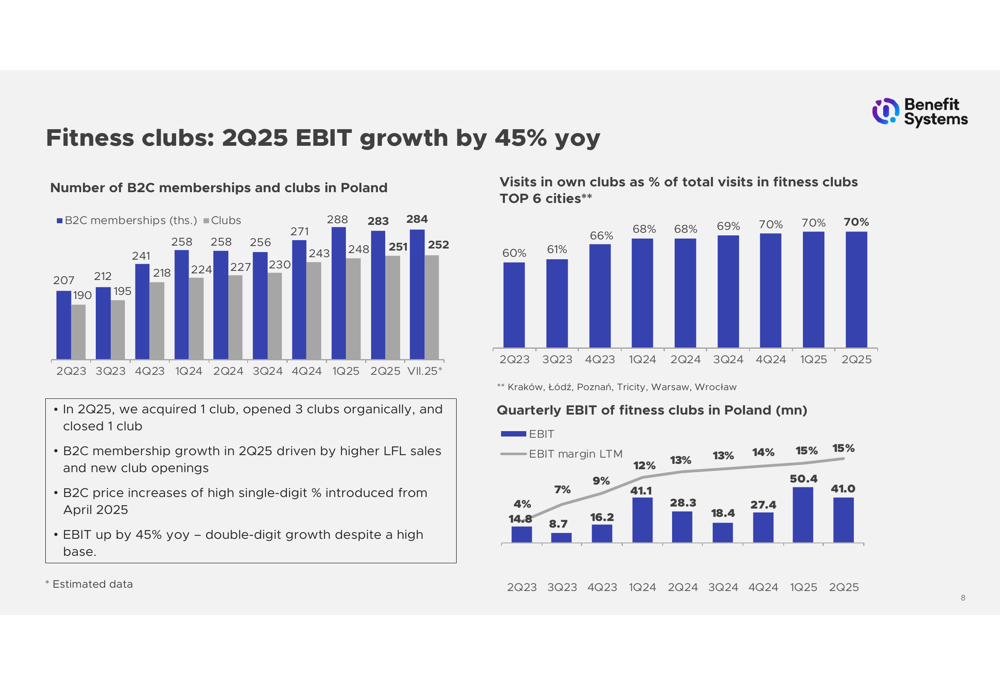

The fitness club business in Poland also demonstrated significant improvement, with EBIT margin reaching 15% in Q2 2025 compared to just 4% in Q2 2023. The number of B2C memberships grew to 283,100, a 10% increase year-over-year, while the company expanded its club network to 251 locations.

Revenue in the Poland segment was driven by both higher card volume and increased ARPU, as shown in the following breakdown:

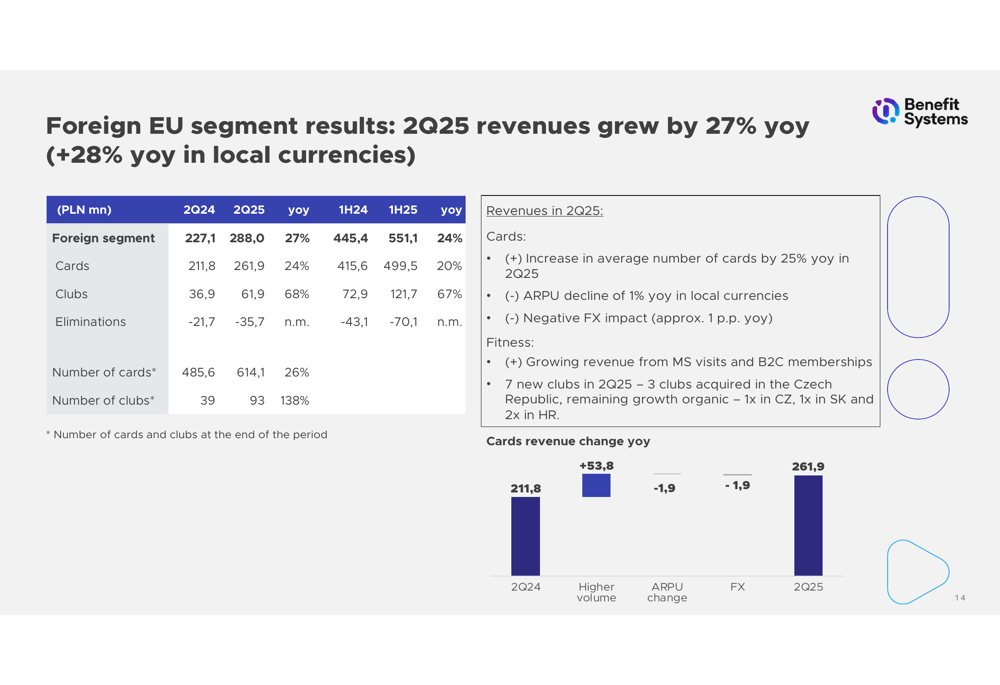

Foreign Markets: Growth and Challenges

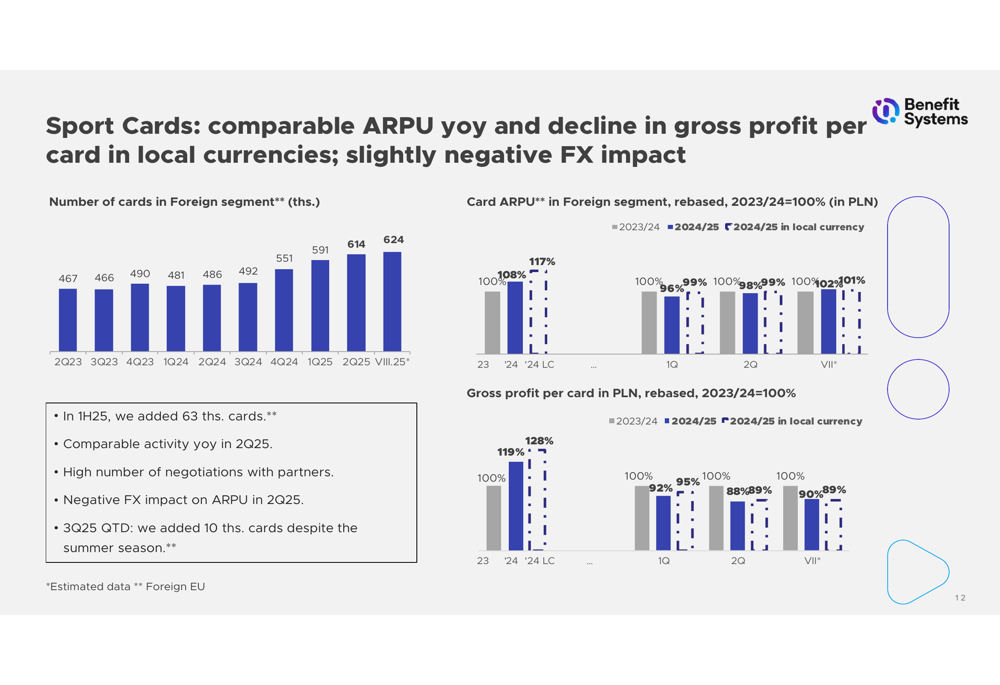

The Foreign EU segment showed strong revenue growth of 27% to 288 million PLN, driven by a 26% increase in card numbers to 614,100. However, profitability declined significantly, with EBIT falling 42% to 25.4 million PLN due to higher costs associated with rapid expansion.

The following chart illustrates the growth in sport cards in the Foreign EU segment:

Despite the revenue growth, the Foreign EU segment faced margin pressure, with gross margin declining by 6 percentage points to 27.8% and SG&A expenses increasing by 61%. The company attributed this to the costs of expanding the fitness club network, which grew from 39 to 93 clubs year-over-year.

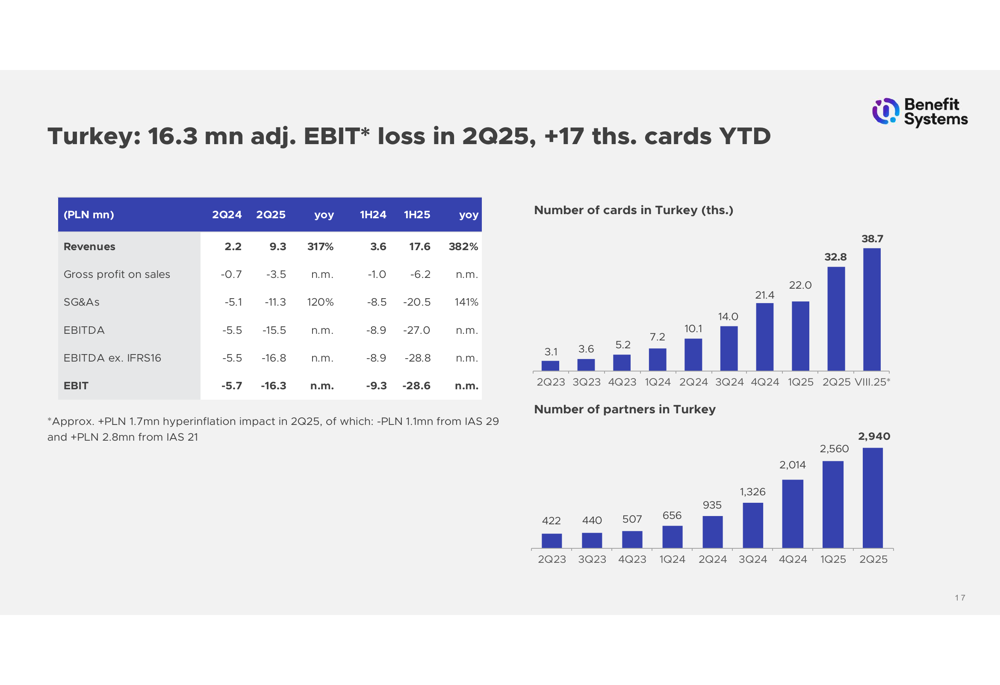

The Turkey segment showed explosive growth with revenue increasing 317% to 9.3 million PLN, driven by rapid card adoption. The number of cards in Turkey grew from just 3,100 in Q2 2023 to 38,700 by August 2025. However, the segment remains unprofitable with an EBIT loss of 16.3 million PLN in Q2 2025.

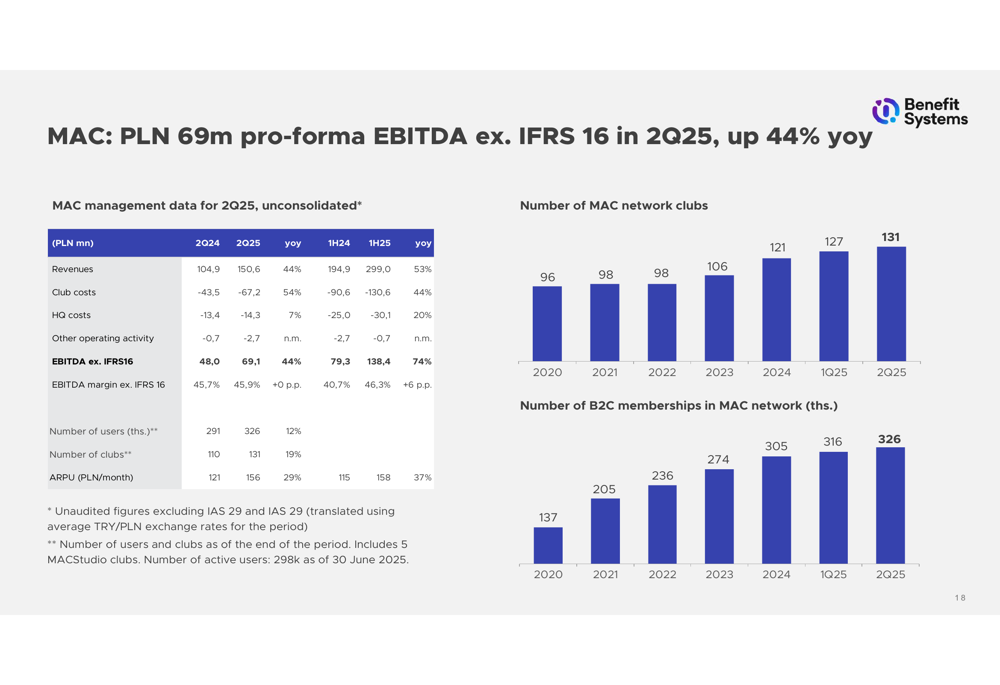

MAC Acquisition Impact

The acquisition of MAC has been a significant driver of growth for Benefit Systems. The MAC network has expanded to 131 clubs with 326,000 B2C memberships as of Q2 2025. The business demonstrated strong profitability with an EBITDA margin (excluding IFRS 16) of 45.9%.

In Q2 2025, MAC contributed 90 million PLN in revenue and 40.5 million PLN in EBIT to the consolidated results, representing a 45% EBIT margin. This acquisition has significantly strengthened Benefit Systems’ position in the fitness club market.

Forward-Looking Statements

For the remainder of 2025, Benefit Systems expects continued improvement in results and increased capital expenditure. The company plans approximately 20 new club openings in Poland and over 45 openings in foreign markets, indicating an ongoing commitment to its expansion strategy.

The stock closed at 3,385 PLN on August 22, 2025, down 1.48% or 50 PLN from the previous close. Despite the strong quarterly results, investors may be concerned about the increased debt position and profitability challenges in international markets.

Benefit Systems continues to execute its strategy of expanding both its sport card business and fitness club network across multiple markets, with Poland remaining the core profit driver while international markets represent significant growth opportunities despite near-term profitability challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.