Trump announces 100% chip tariff as Apple ups U.S. investment

Introduction & Market Context

Berry Petroleum Corporation (NASDAQ:BRY) presented its Q1 2025 investor deck highlighting stable production, consistent cash flow generation, and strategic expansion plans in the Uinta Basin. Despite reporting strong operational metrics, the company’s stock has struggled to gain traction, trading at $2.40 as of May 7, 2025, well below its 52-week high of $7.805.

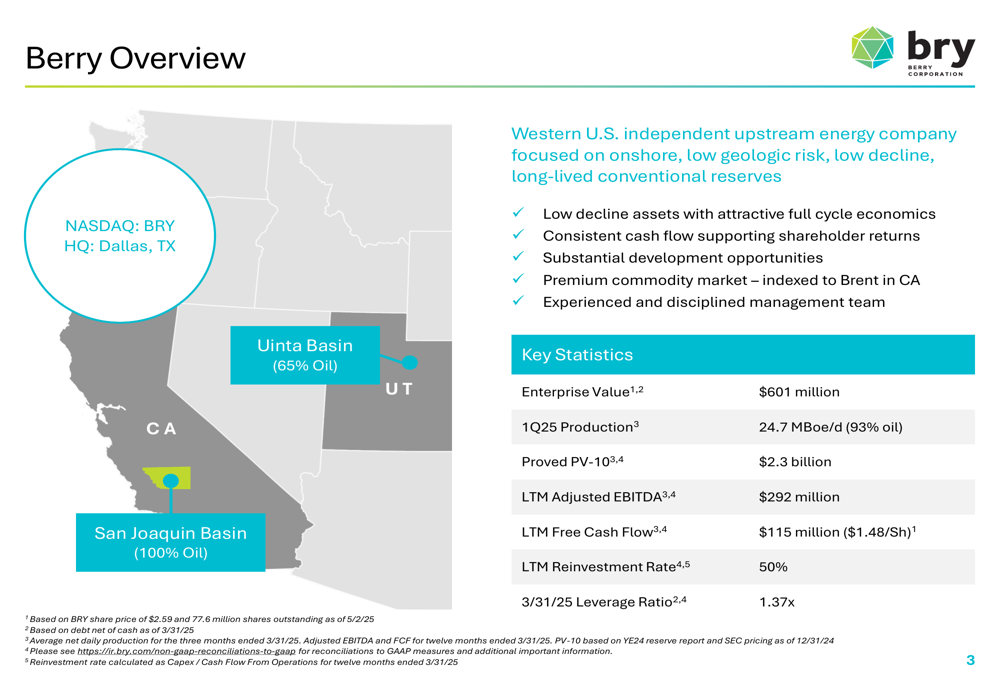

The company positions itself as a Western U.S. independent upstream energy company focused on low-risk, long-lived conventional reserves, with operations primarily in California’s San Joaquin Basin and Utah’s Uinta Basin. Berry’s presentation emphasizes its low-decline assets, consistent cash flow, and premium commodity market exposure through Brent-indexed pricing in California.

As shown in the following overview of Berry’s key metrics and asset locations:

Quarterly Performance Highlights

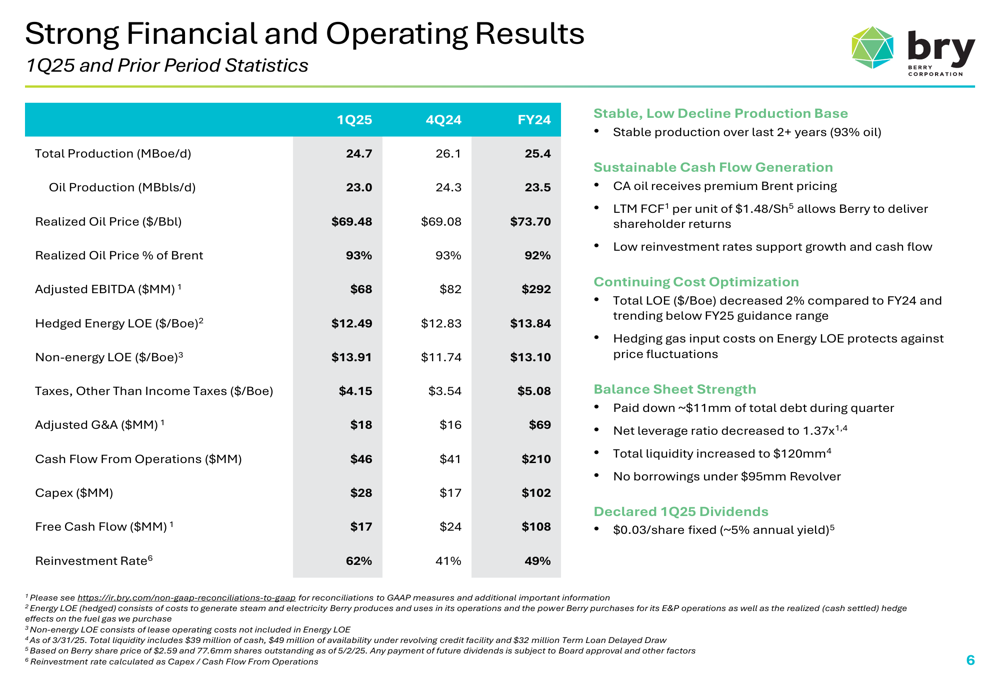

Berry reported solid Q1 2025 results with production of 24.7 MBoe/d (93% oil), generating $68 million in Adjusted EBITDA and $17 million in free cash flow. The company maintained a reinvestment rate of 62% while achieving a realized oil price of $69.48/Bbl. Operating expenses remained controlled with hedged energy LOE at $12.49/Boe and adjusted G&A at $18 million for the quarter.

The company’s financial and operating results demonstrate its ability to generate consistent cash flow even in a challenging price environment:

Berry’s low-decline production profile has been a key strength, with base production accounting for approximately 95% of total production over the past three years. This stability provides a solid foundation for the company’s cash flow generation and capital allocation strategy.

Strategic Initiatives

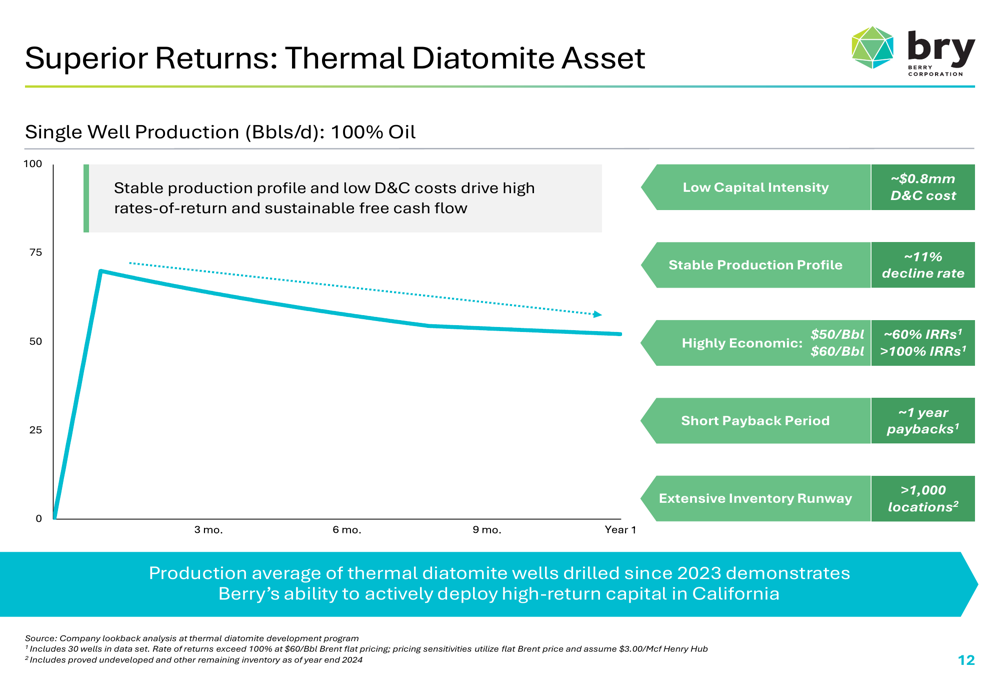

Berry’s strategy centers around three pillars: driving operational excellence in California, unlocking upside value in Utah, and maintaining financial discipline. The company’s thermal diatomite asset in California continues to deliver superior returns with low capital intensity (~$0.8 million D&C cost) and stable production profiles (~11% decline rate).

The economics of these wells are particularly compelling, as illustrated in the following chart showing the production profile and returns of thermal diatomite wells:

These wells deliver approximately 60% IRRs at $50/Bbl oil prices and over 100% IRRs at $60/Bbl, with payback periods of around one year. The company has identified more than 1,000 potential drilling locations in this play, providing a substantial inventory runway.

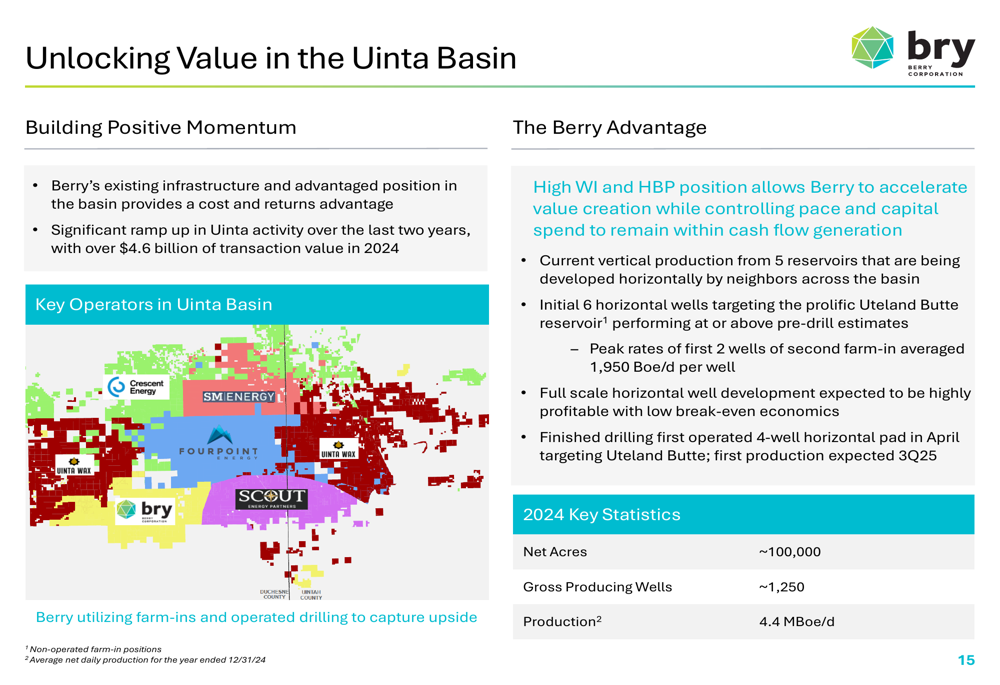

Simultaneously, Berry is strategically expanding its presence in the Uinta Basin, where it holds approximately 100,000 net acres and operates around 1,250 gross producing wells. The company is leveraging its existing infrastructure and high working interest position to accelerate value creation while controlling pace and capital spend.

The following map illustrates Berry’s advantaged position in the emerging Uinta play:

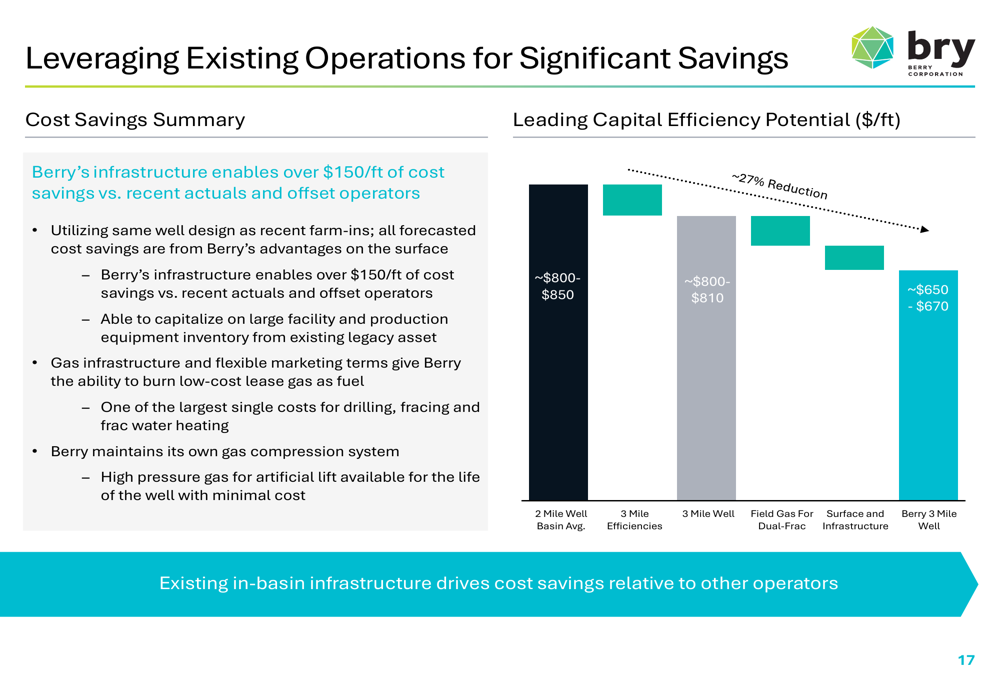

Berry’s infrastructure advantages in the Uinta Basin enable significant cost savings compared to offset operators. The company estimates over $150/ft of cost savings by utilizing existing facilities, production equipment, and gas infrastructure.

As shown in the following chart detailing the company’s capital efficiency potential:

Competitive Industry Position

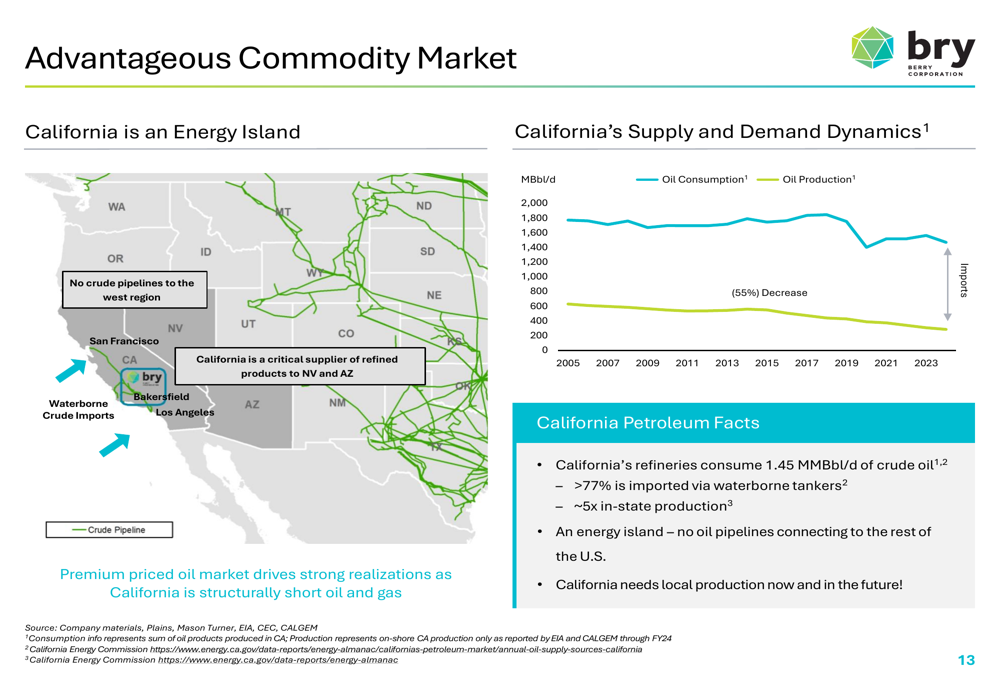

A key competitive advantage for Berry is its operations in California, which the company describes as an "Energy Island" with limited pipeline infrastructure. California’s refineries consume approximately 1.45 MMBbl/d of crude oil, with over 77% imported via waterborne tankers, creating a premium market for local production.

The following map and chart illustrate California’s unique supply-demand dynamics:

This market positioning allows Berry to receive Brent-indexed pricing for its California production, providing a premium over WTI pricing that many U.S. producers receive.

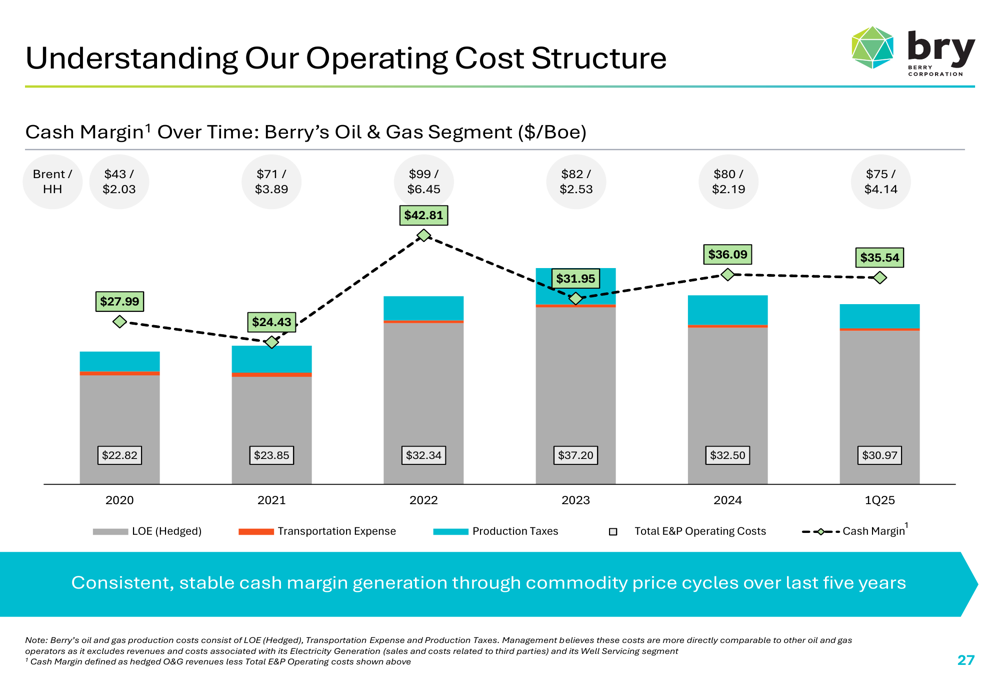

The company’s operating cost structure has remained relatively stable over time, allowing for consistent cash margin generation despite fluctuations in commodity prices:

Environmental Initiatives

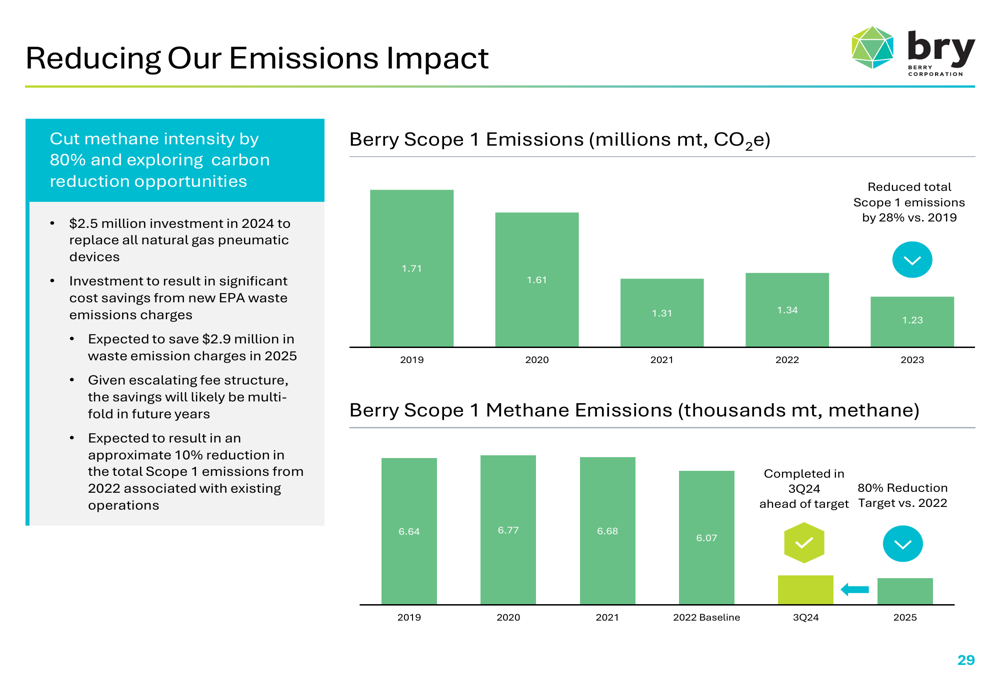

Berry has made significant progress in reducing its environmental footprint, cutting methane intensity by 80% ahead of target. The company invested $2.5 million in 2024 to replace all natural gas pneumatic devices, which is expected to save approximately $2.9 million in waste emission charges.

The following chart shows Berry’s progress in reducing Scope 1 emissions:

Forward-Looking Statements

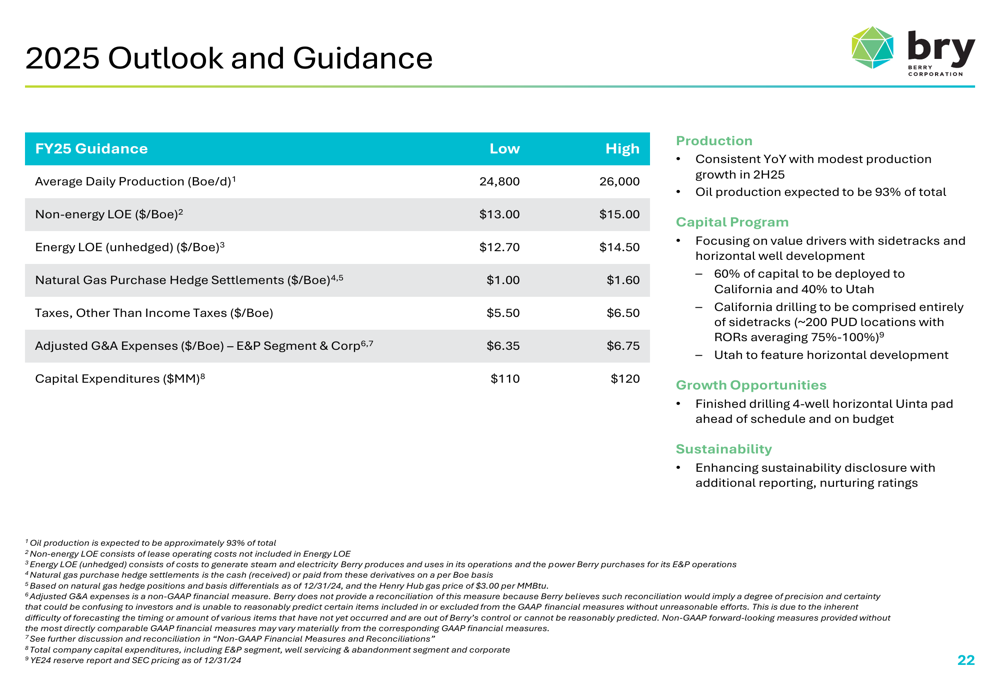

For 2025, Berry provided guidance for average daily production of 24,800-26,000 Boe/d, with capital expenditures of $110-$120 million. The company plans to focus 60% of its capital program on California assets while continuing to develop its opportunities in Utah, including a 4-well pad that is ahead of schedule.

The detailed 2025 guidance metrics are presented in the following table:

Financial Analysis

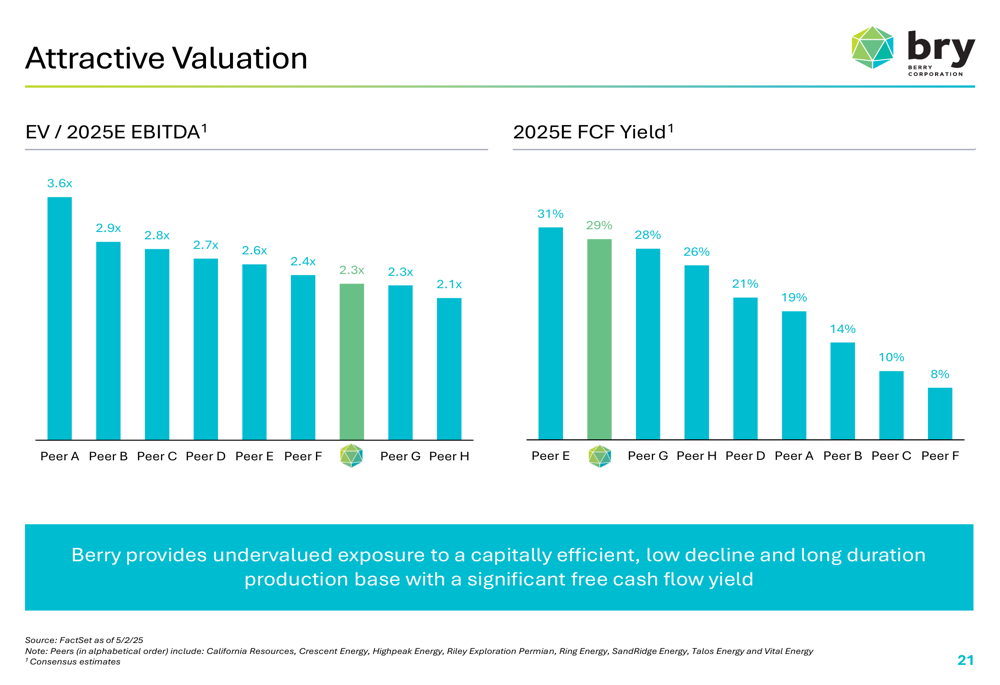

Berry highlights its attractive valuation compared to peers, with a lower EV/EBITDA multiple and higher free cash flow yield. This suggests potential undervaluation in the market despite the company’s stable production and consistent cash flow generation.

The following comparative charts illustrate Berry’s valuation metrics relative to peers:

The company has also maintained balance sheet strength, with a net leverage ratio of 1.37x as of March 31, 2025. Berry’s debt structure includes a $95 million revolving credit facility with a $63 million elected commitment amount and a $439 million term loan.

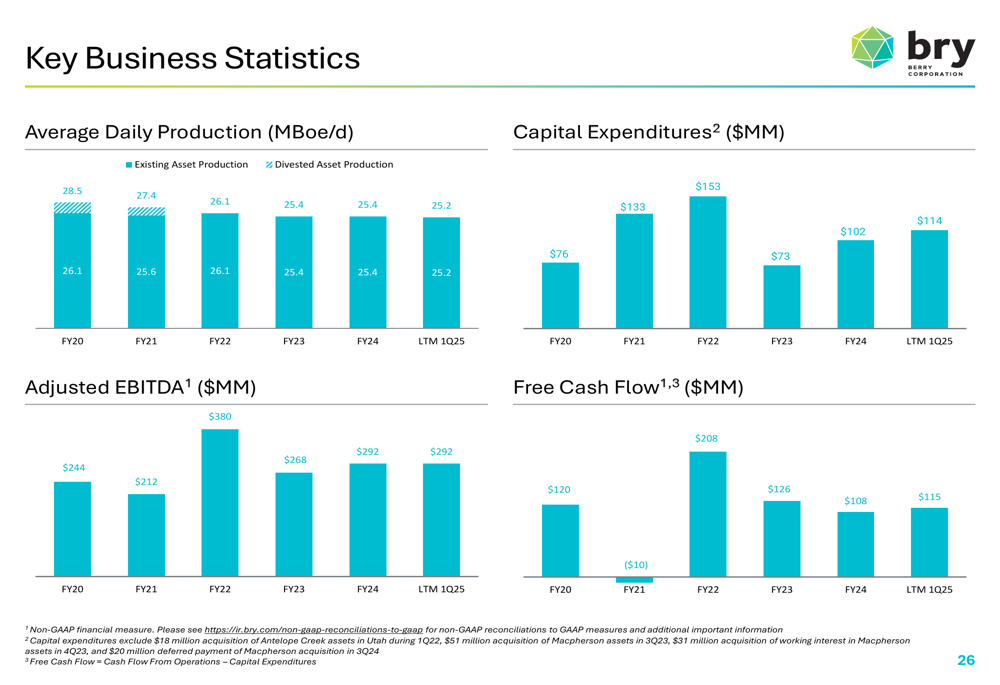

Berry’s key business statistics over time demonstrate the company’s ability to generate consistent results:

Conclusion

Berry Petroleum’s Q1 2025 presentation portrays a company with stable production, strong cash flow generation, and strategic growth opportunities, particularly in the Uinta Basin. The company’s low-decline California assets provide a solid foundation, while its expansion into Utah offers potential upside.

Despite these positive operational metrics and an attractive valuation compared to peers, Berry’s stock continues to trade at a significant discount to its 52-week high. The company’s focus on financial discipline, balance sheet strength, and returning capital to shareholders through dividends ($0.03/share fixed in Q1 2025) may eventually help bridge this valuation gap as it executes on its strategic initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.