Powell’s speech, Nvidia’s chips, Meta deal - what’s moving markets

BE Semiconductor Industries NV ( AMS (VIE:AMS2):AS:BESI) reported mixed first-quarter 2025 results in its April 23 investor presentation, showing declining revenue but increasing orders as the company positions itself for an anticipated market recovery in advanced packaging for AI applications.

Quarterly Performance Highlights

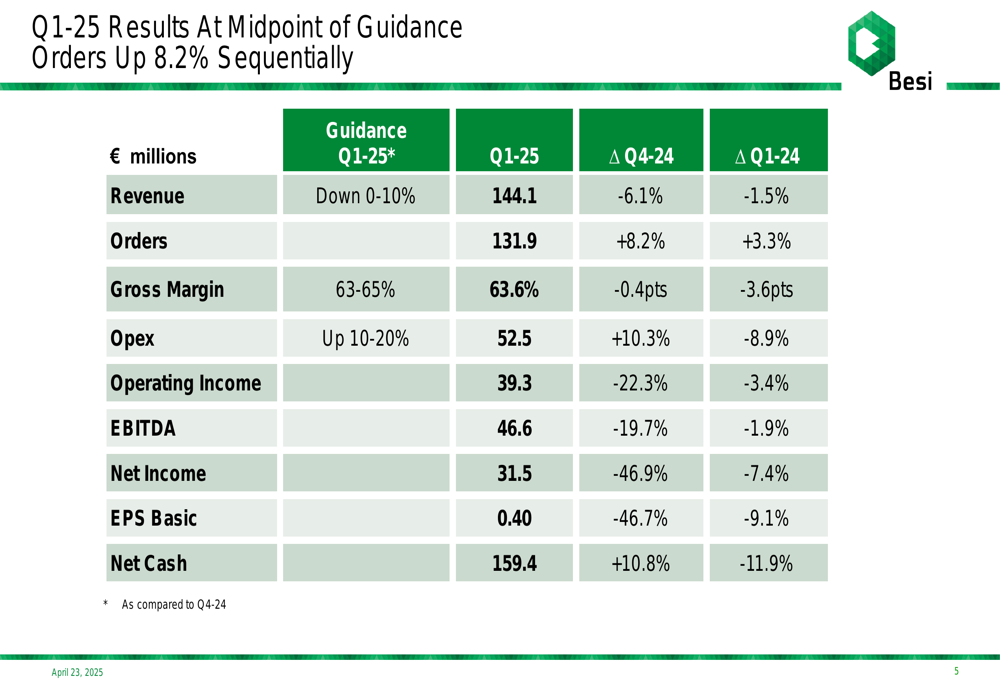

BESI reported Q1 2025 revenue of €144.1 million, representing a 1.5% year-over-year decline and a 6.1% sequential decrease from Q4 2024. Despite the revenue dip, orders increased to €131.9 million, up 3.3% year-over-year and 8.2% quarter-over-quarter, driven primarily by increased demand for AI-related datacenter applications from Asian subcontractors.

As shown in the following chart of quarterly financial results:

The company’s gross margin stood at 63.6% in Q1 2025, down 3.6 percentage points from Q1 2024 and slightly below the 64.0% reported in Q4 2024. Net income fell to €31.5 million, down 7.4% year-over-year and 46.9% quarter-over-quarter, with the sequential decline partly attributed to a one-time tax benefit in Q4 2024.

These results fell short of analyst expectations, with EPS of €0.40 missing the forecast of €0.4916 and revenue coming in below the anticipated €159.94 million. Nevertheless, BESI’s stock rose 1.85% in pre-market trading following the announcement, suggesting investors focused more on the company’s strategic positioning and order growth than on the quarterly miss.

Financial Position and Capital Allocation

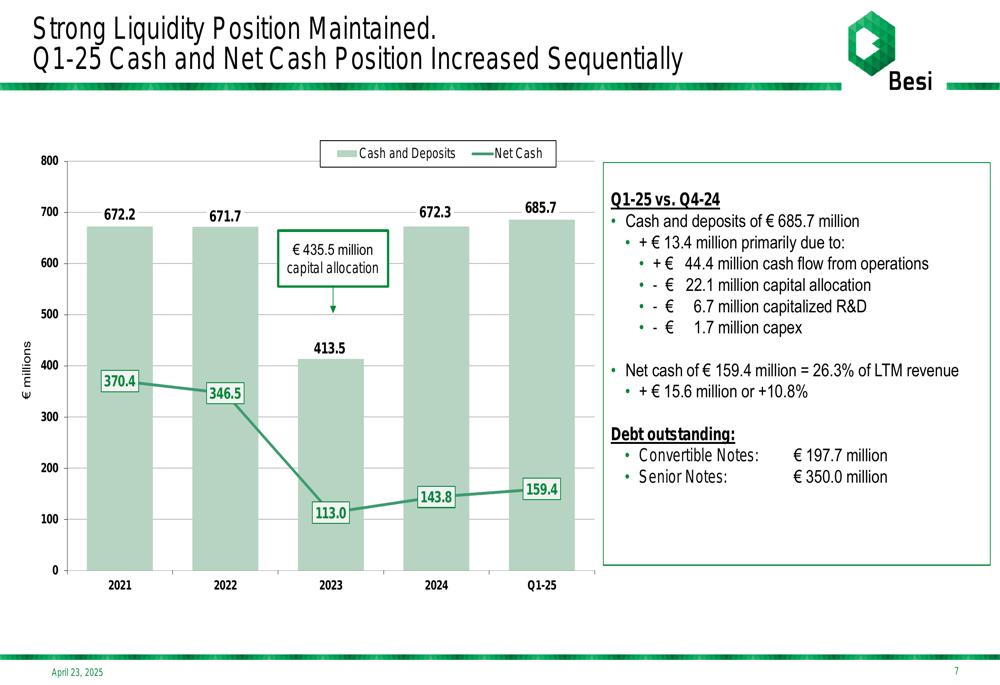

BESI maintained a strong financial position with cash and deposits of €685.7 million and net cash of €159.4 million as of March 31, 2025. The net cash position increased by 10.8% from the previous quarter, primarily due to €44.4 million in cash flow from operations, partially offset by capital allocation and investments.

The company’s liquidity position is illustrated in the following chart:

BESI has maintained a consistent capital return policy, with cumulative dividends of €1.5 billion since 2011, representing €19.96 per share. The company held approximately 2.0 million treasury shares at the end of Q1 2025, representing 2.5% of shares outstanding.

Strategic Initiatives

The presentation highlighted BESI’s strategic focus on wafer-level assembly and advanced packaging technologies, particularly for AI applications. Key developments in Q1 2025 included:

- Expansion of wafer-level assembly adoption into the memory space

- Important announcements for future hybrid bonding use cases in ASICs and co-packaged optics

- Volume production using BESI’s hybrid bonders in integrated production lines by a leading US logic manufacturer

- Expansion of cleanroom capacity and Asian support capabilities in anticipation of advanced packaging growth in H2-25

As shown in the strategic agenda highlights:

A significant development was Applied Materials (NASDAQ:AMAT)’ announcement of a 9% stake in BESI as a strategic investment, potentially validating the company’s technology and market position in advanced packaging.

Market Outlook and Guidance

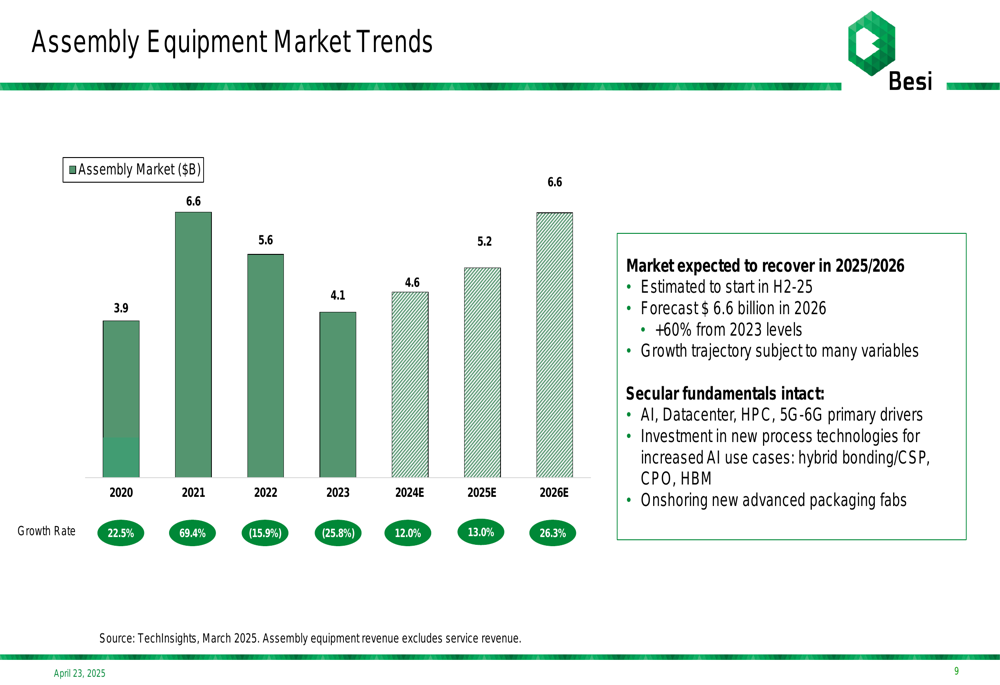

BESI expects the assembly equipment market to recover in 2025/2026, with growth anticipated to begin in the second half of 2025. The company forecasts the market to reach $6.6 billion in 2026, representing a 60% increase from 2023 levels.

The following chart illustrates the expected market recovery trajectory:

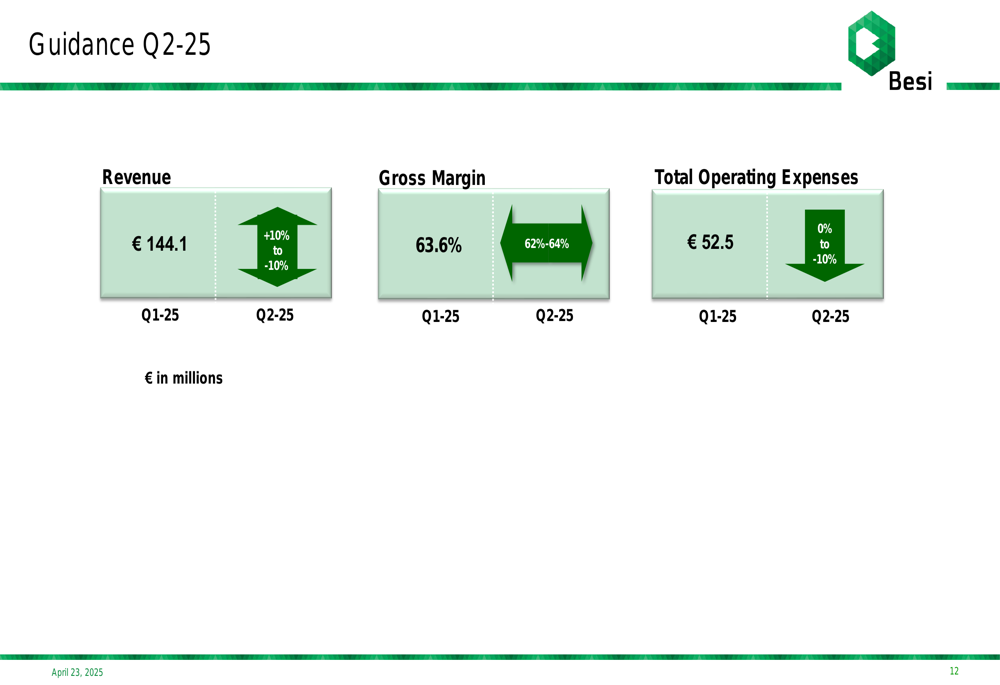

For Q2 2025, BESI provided guidance for:

- Revenue in the range of +10% to -10% compared to Q1 2025

- Gross margin between 62% and 64%

- Operating expenses to decrease by 0% to 10%

The Q2 guidance is visualized in the following slide:

Investment Considerations

BESI highlighted several key investment considerations in its presentation, emphasizing the growing importance of assembly in the semiconductor value chain and the long-term secular trends driving advanced packaging growth.

The company’s investment case centers on its disciplined strategic focus, leadership in wafer-level assembly for AI applications, and growing market presence through key IDMs, supply chains, and partners:

CEO Richard Blakeman emphasized BESI’s leading position in hybrid bonding technology during the earnings call, stating, "We are currently with the hundred nanometer well advanced in comparison to everyone else." He also noted Tech Insights’ forecast of a 13% assembly market upturn in 2025, followed by a 26% increase in 2026.

Despite the mixed quarterly results, BESI’s strategic positioning in high-growth segments of the semiconductor assembly market, particularly for AI applications, appears to have resonated with investors as the company prepares for an anticipated market recovery in late 2025 and 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.