Street Calls of the Week

Introduction & Market Context

BFF Bank SpA (BIT:BFF) presented its first half 2025 results on August 5, 2025, showcasing solid financial performance with particularly strong second-quarter growth. The bank, currently trading at €11.20 per share, near its 52-week high of €11.46, delivered a 6% year-over-year increase in adjusted net profit for the first half, with Q2 results showing an impressive 37% surge compared to the same period last year.

The presentation comes as BFF celebrates its 40th anniversary in July 2025, with the bank continuing to strengthen its position across European markets while maintaining a focus on its core factoring and lending business targeting public administration clients.

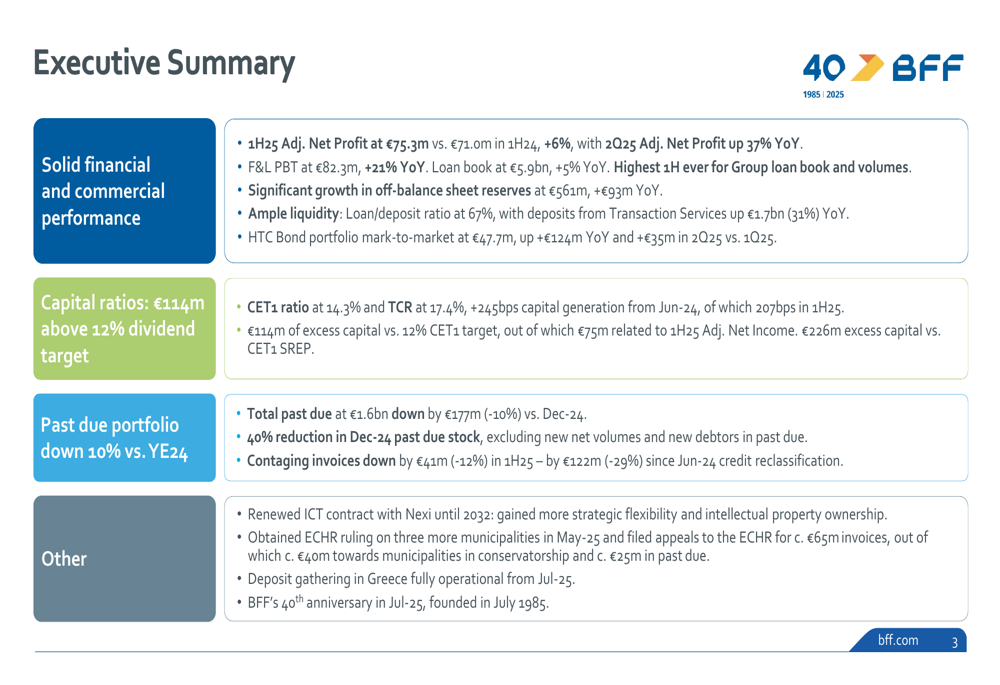

Executive Summary

BFF Bank reported adjusted net profit of €75.3 million for the first half of 2025, up 6% from €71.0 million in the same period last year. The bank’s performance was particularly strong in the second quarter, with adjusted net profit growing 37% year-over-year and 15% quarter-over-quarter.

The bank’s core Factoring & Lending (F&L) segment showed robust growth with profit before tax (PBT) reaching €82.3 million, up 21% year-over-year. The loan book reached €5.9 billion, representing a 5% increase compared to 1H 2024 and marking the highest first-half figure in the bank’s history.

As shown in the following executive summary slide, BFF maintained strong capital ratios with a CET1 ratio of 14.3% and total capital ratio of 17.4%, representing 245 basis points of capital generation since June 2024:

Detailed Financial Analysis

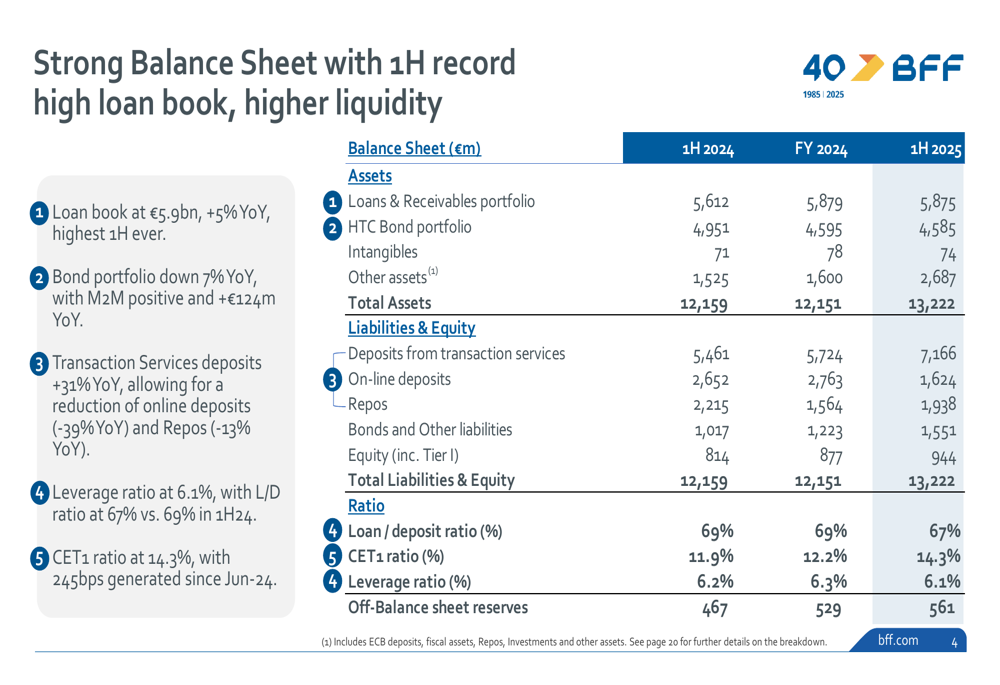

BFF’s balance sheet showed significant strength, with the loan book growing 5% year-over-year to €5.9 billion, while the bank maintained ample liquidity with a loan-to-deposit ratio of 67%, improved from 69% in the first half of 2024. The bank’s HTC bond portfolio mark-to-market value stood at €47.7 million, a substantial improvement of €124 million compared to the previous year.

The following balance sheet breakdown provides a comprehensive view of the bank’s financial position:

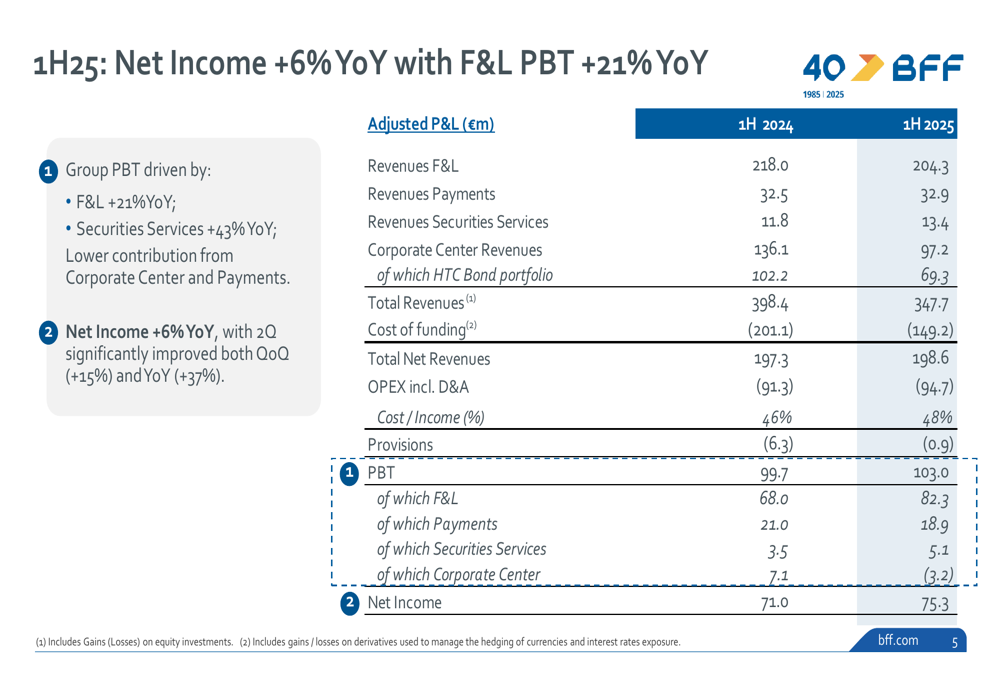

In terms of profitability, BFF’s adjusted profit and loss statement shows total net revenues of €198.6 million, slightly up from €197.3 million in 1H 2024. Operating expenses including depreciation and amortization increased by 3.7% to €94.7 million, resulting in a cost-to-income ratio of 48%, compared to 46% in the same period last year.

The detailed profit and loss breakdown is illustrated in the following slide:

The Factoring & Lending segment, which represents BFF’s core business, showed resilient performance despite the lower interest rate environment. The gross yield on average loans decreased to 6.8% from 7.6% in 1H 2024, but this decline was significantly less than the reduction in the ECB reference rate, indicating an improved spread.

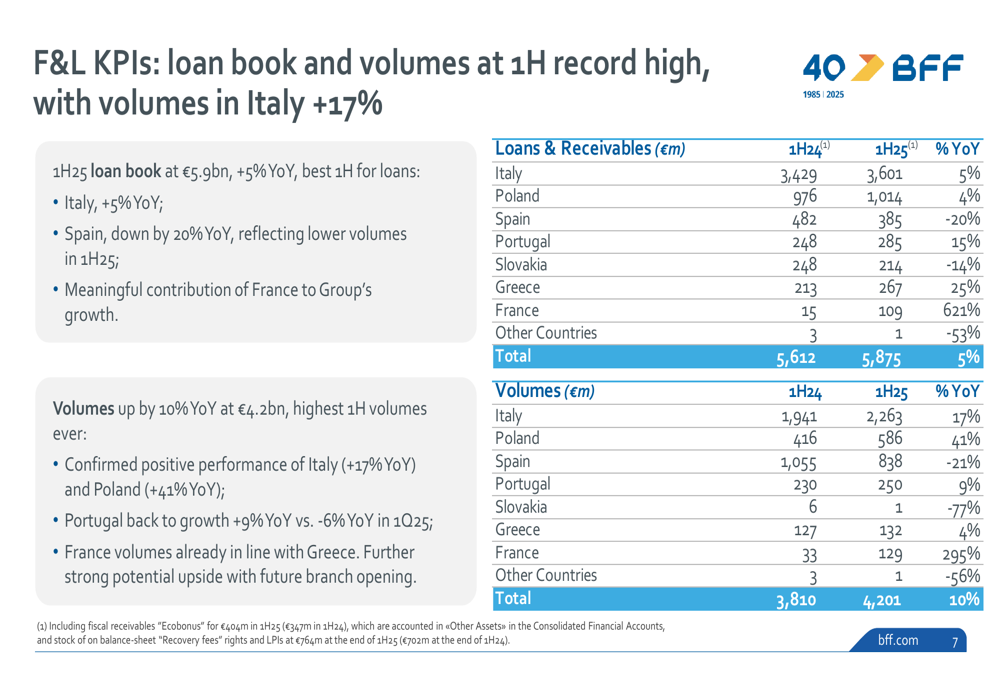

Country-by-country analysis shows strong growth in key markets, with loan volumes in Italy increasing by 17% year-over-year and Poland showing an impressive 41% growth. France also demonstrated substantial expansion with volumes up 295% year-over-year, albeit from a smaller base. Spain, however, showed a 21% decline in volumes.

The following slide provides a detailed breakdown of loan book and volumes by country:

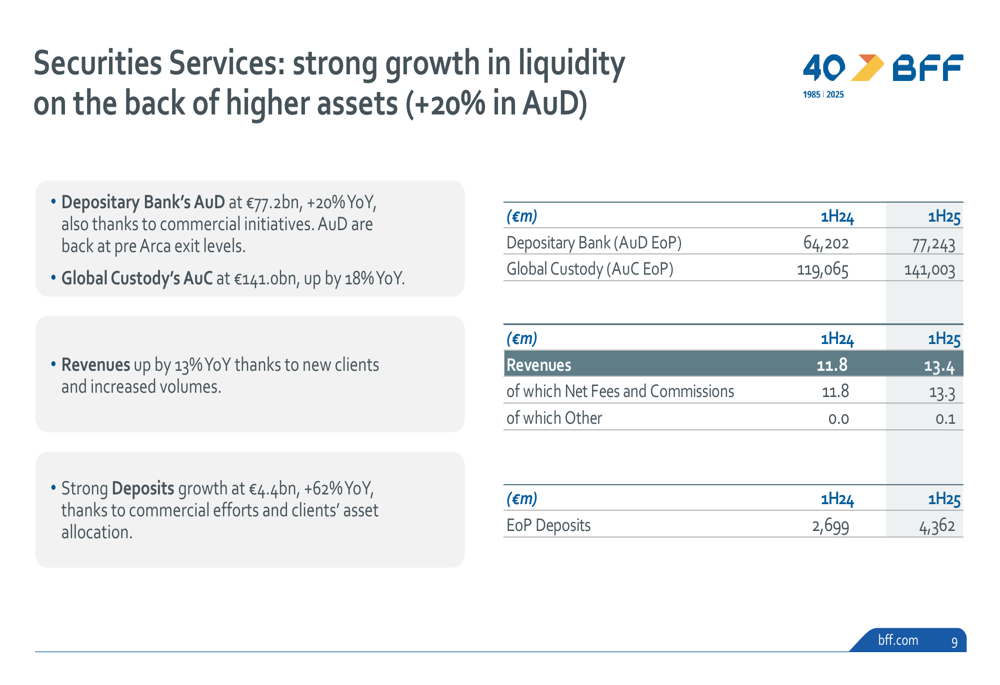

The Securities Services segment demonstrated strong growth, with assets under depositary (AuD) increasing by 20% year-over-year to €77.2 billion and assets under custody (AuC) growing by 18% to €141.0 billion. This translated into a 13% increase in revenues and a 62% surge in deposits to €4.4 billion.

The performance of the Securities Services segment is illustrated in the following slide:

Risk Profile and Capital Position

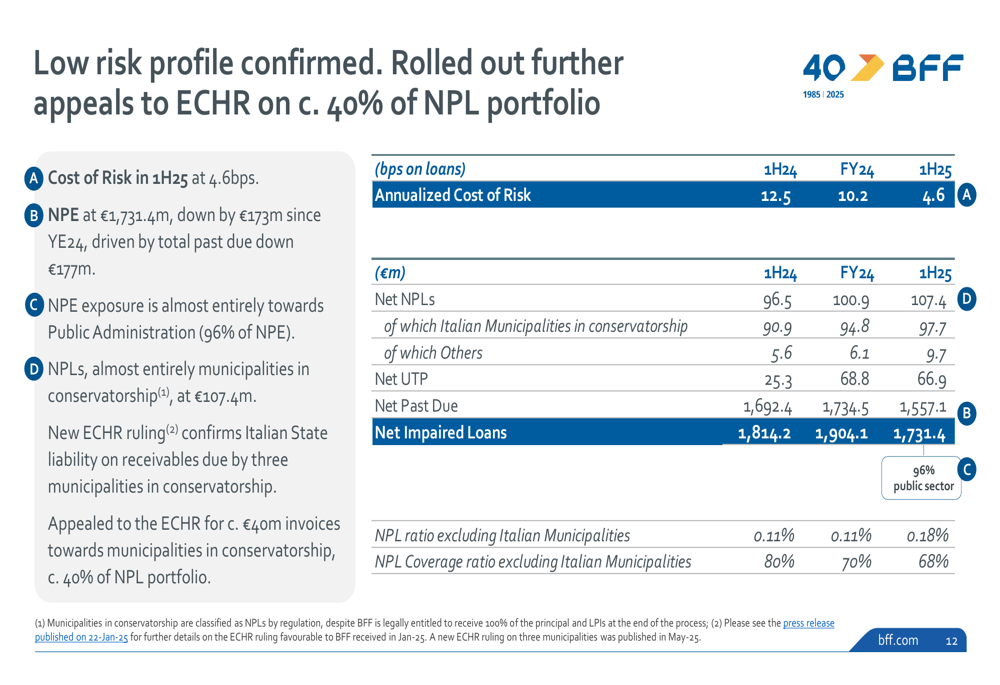

BFF maintained its low risk profile, with annualized cost of risk in 1H 2025 at just 4.6 basis points. Non-performing exposures (NPE) decreased by €173 million since year-end 2024, with 96% of NPE being towards Public Administration entities.

The bank has made significant progress in reducing its past due portfolio, with total past due exposure down by €177 million (-10%) compared to December 2024. The bank achieved a 40% reduction in the December 2024 past due stock and reduced contaging invoices by €41 million (-12%) in the first half of 2025.

The following slide illustrates the bank’s risk profile:

Capital generation remained strong, with the CET1 ratio reaching 14.3%, representing 245 basis points of capital generation since June 2024. The bank has €114 million of excess capital compared to its 12% CET1 target and €226 million excess capital versus CET1 SREP requirements.

Strategic Initiatives

BFF highlighted several strategic developments during the presentation. The bank renewed its ICT contract with Nexi (BIT:NEXII) until 2032, ensuring technological continuity. Deposit gathering operations in Greece became fully operational from July 2025, expanding the bank’s funding sources.

The bank also obtained European Court of Human Rights (ECHR) rulings on three more municipalities in May 2025, which could positively impact its non-performing loan portfolio, approximately 40% of which is subject to ECHR appeals.

Forward-Looking Statements

Looking ahead, BFF expects to maintain its positive momentum, with continued growth in its core Factoring & Lending business and Securities Services segments. The bank will focus on further reducing its past due portfolio and optimizing its collection processes.

As noted by Massimiliano Bingeri, Group CEO (quoted in the earnings article): "We continue to deliver on growth while keeping substantial liquidity." This statement underscores the bank’s balanced approach to growth and risk management.

The bank’s strong capital position, with €114 million of excess capital above its dividend target, suggests potential for enhanced shareholder returns, particularly if the Bank of Italy removes dividend policy restrictions as anticipated.

BFF’s 1H 2025 results demonstrate the bank’s ability to generate sustainable growth while maintaining strong capital ratios and a low risk profile, positioning it well for continued success in its niche market of public administration financing across Europe.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.