Street Calls of the Week

Introduction & Market Context

BFF Bank (BIT:BFF) presented its first quarter 2025 results on May 8, 2025, showcasing solid performance despite mixed regional results. The bank’s shares closed at €8.40 on the day of the announcement, down 0.54%, as investors digested the results that highlighted growth in key segments while maintaining strong capital ratios.

Executive Summary

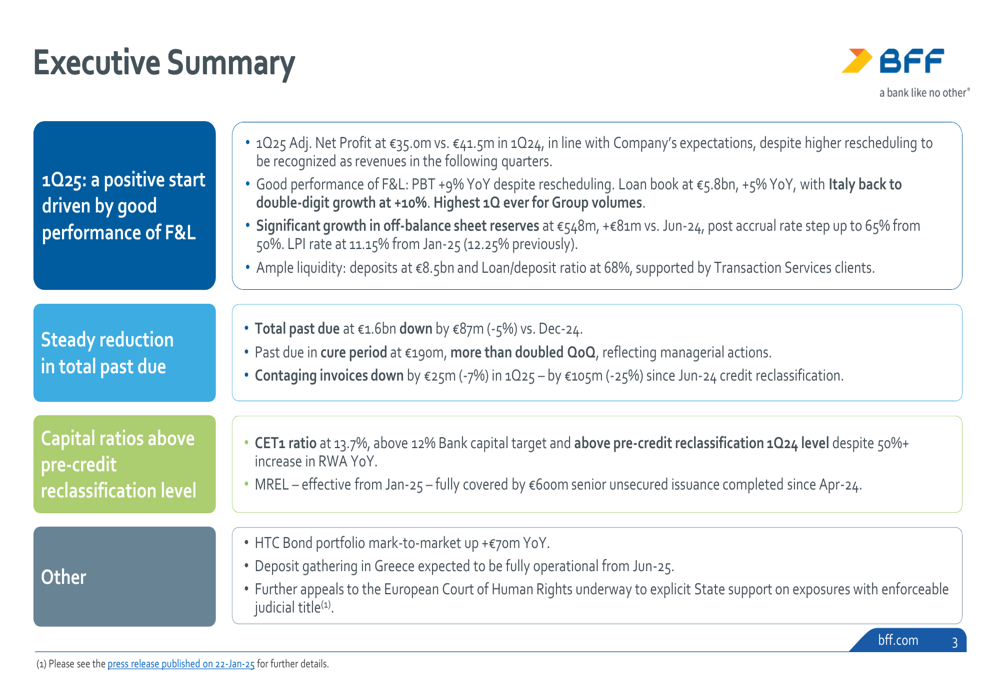

BFF Bank reported an adjusted net profit of €35.0 million for Q1 2025, with particularly strong performance in its Factoring & Lending (F&L) division, where profit before tax increased 9% year-over-year. The bank’s loan book reached €5.8 billion, growing 5% compared to the same period last year, with Italian operations showing robust 10% growth.

As shown in the following summary of key performance indicators:

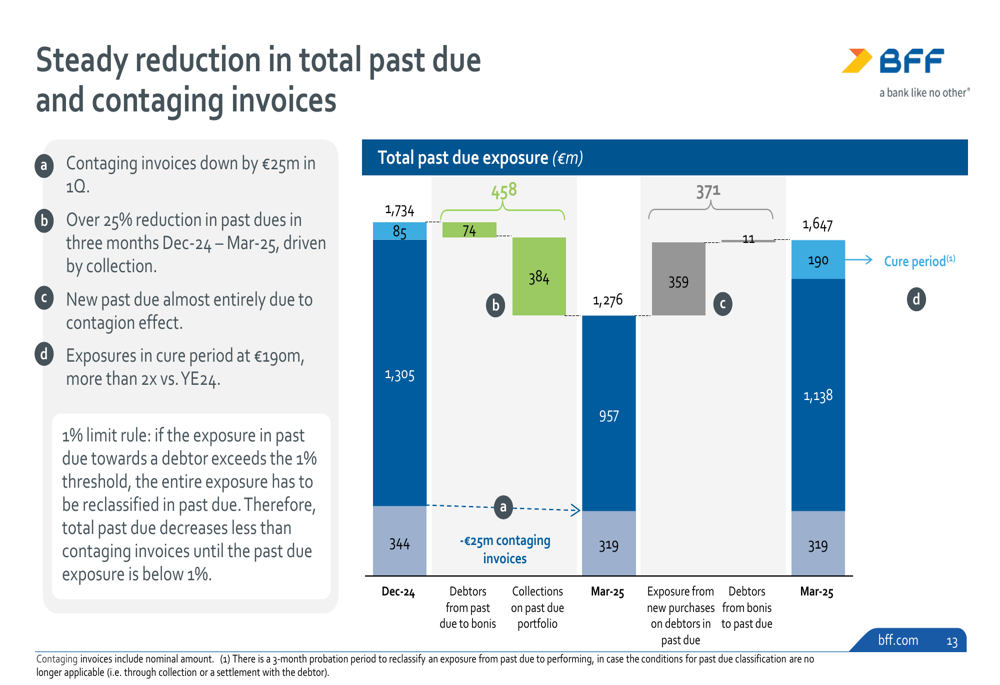

The bank also reported significant growth in off-balance sheet reserves, which reached €548 million, an increase of €81 million compared to June 2024. Total (EPA:TTEF) past due amounts decreased by €87 million (-5%) compared to December 2024, reflecting improved credit quality management.

Quarterly Performance Highlights

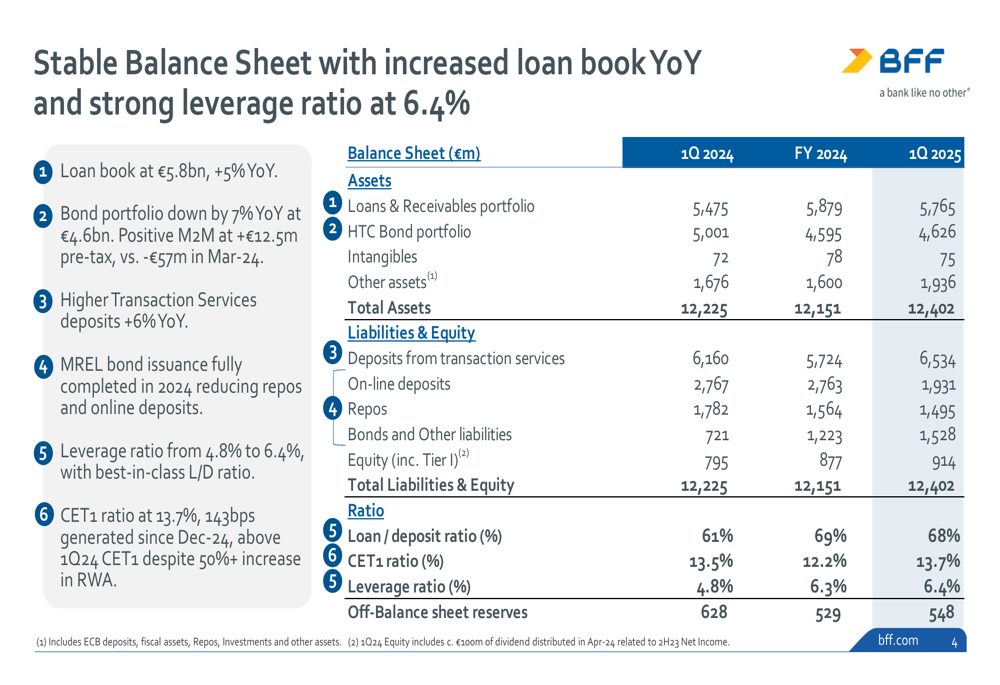

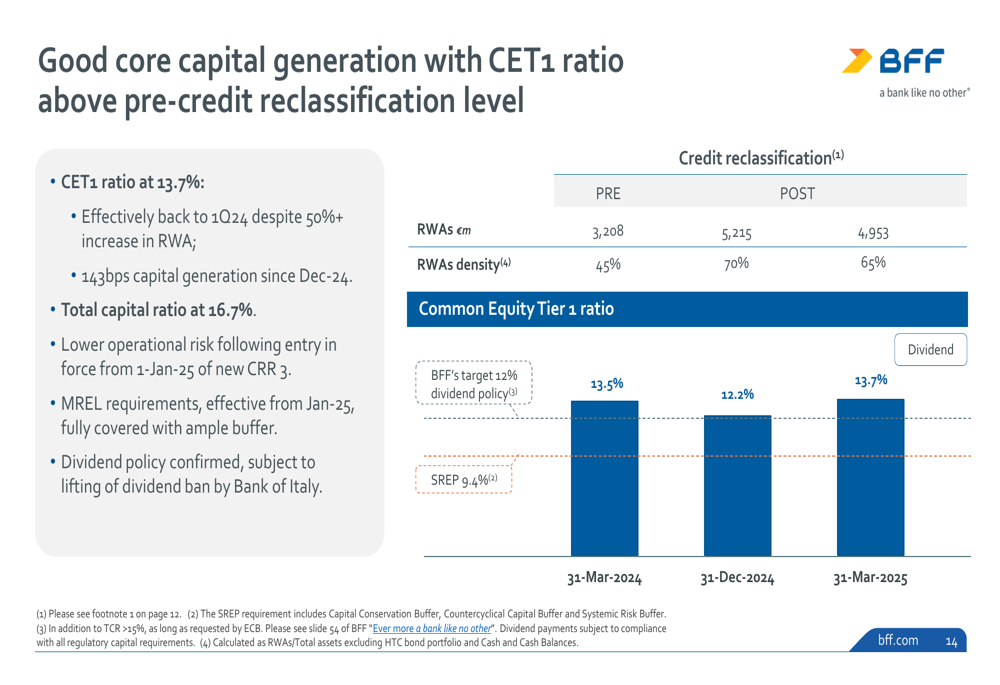

BFF maintained a stable balance sheet with total assets of €12.4 billion as of Q1 2025. The bank’s loan-to-deposit ratio stood at a healthy 68%, while the CET1 ratio reached 13.7%, comfortably above the bank’s 12% target. The following balance sheet breakdown illustrates the bank’s financial position:

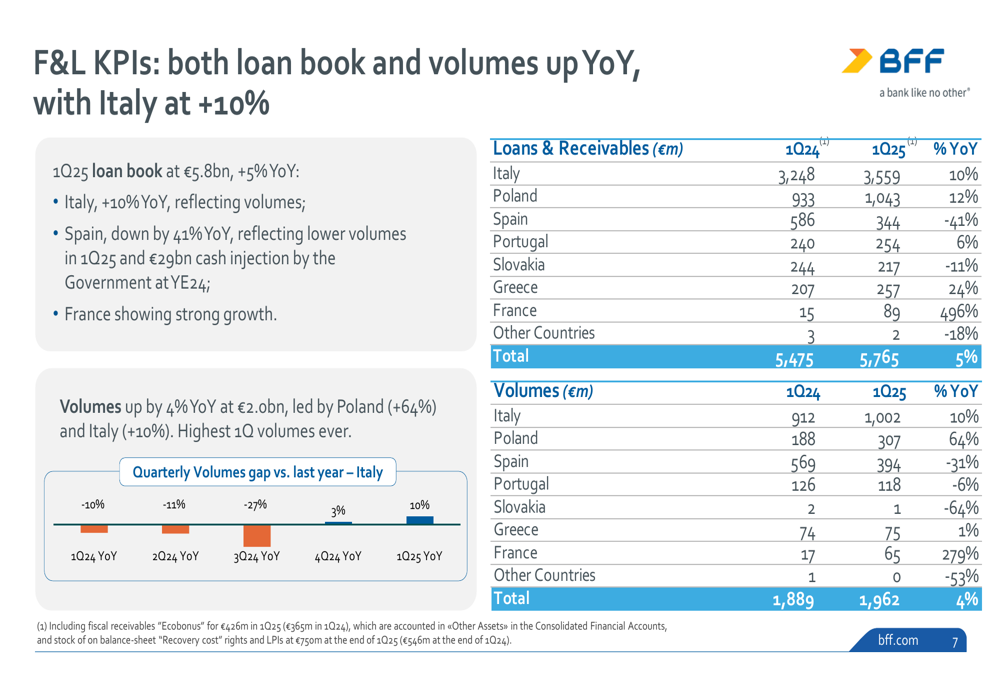

The Factoring & Lending segment, a core business for BFF, showed divergent performance across regions. While Italy demonstrated strong growth with a 10% year-over-year increase in loan volumes, Spain experienced a significant 41% decline. Poland emerged as a growth driver with volumes increasing by 64% year-over-year.

The following chart illustrates the loan book and volume trends across different regions:

Detailed Financial Analysis

BFF’s Securities Services division emerged as a standout performer, with Assets under Depositary (AuD) growing 21% year-over-year to €75.1 billion and Assets under Custody (AuC) increasing 9% to €128.1 billion. This growth translated into a 15% increase in revenues for the segment. Deposits from Securities Services showed impressive growth of 28% year-over-year, reaching €3.8 billion.

The Payments segment showed more modest results, with the number of transactions increasing 4% year-over-year, though revenues declined slightly by 3% to €15.9 million. End-of-period deposits in this segment decreased by 14% compared to the previous year.

BFF maintained disciplined cost management despite ongoing investments in the business. The cost-to-income ratio increased from 44% in Q1 2024 to 49% in Q1 2025, with operating expenses and depreciation & amortization growing by a modest 4% year-over-year.

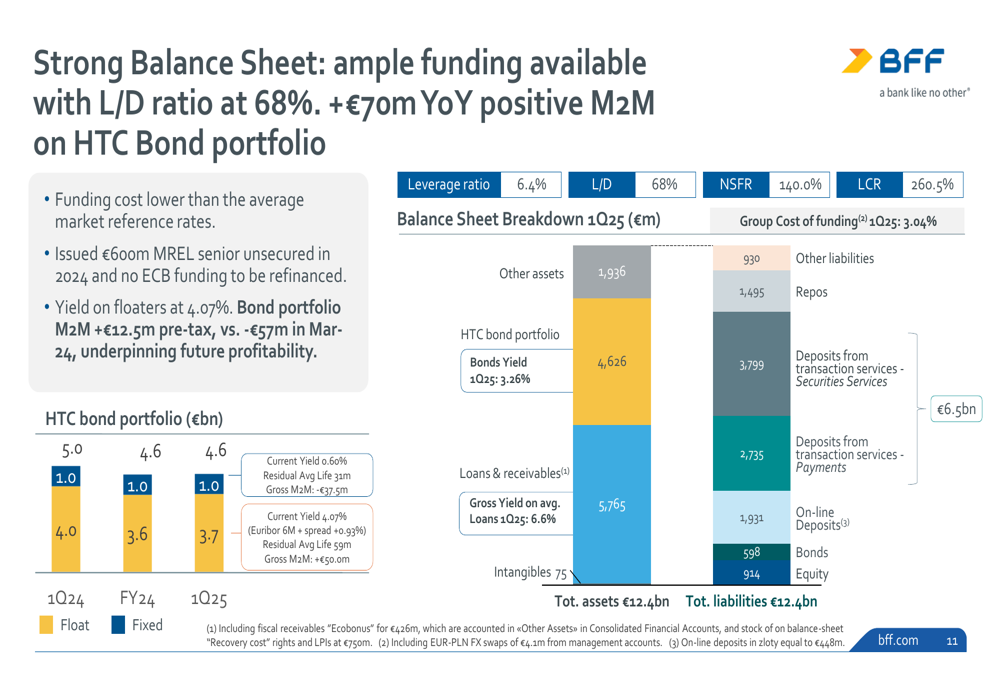

The bank’s balance sheet remained strong, with a positive mark-to-market of €70 million year-over-year on the HTC Bond portfolio. The following visualization provides a clear picture of BFF’s balance sheet strength:

Strategic Initiatives

BFF continues to maintain a low-risk profile, with 95% of its non-performing exposures related to public administration entities. The bank reported a cost of risk of just 4.2 basis points in Q1 2025, reflecting its conservative approach to lending.

The bank has made significant progress in reducing total past due exposures, as illustrated in the following chart:

Capital generation remained strong, with the CET1 ratio at 13.7%, effectively returning to Q1 2024 levels despite a more than 50% increase in risk-weighted assets. The bank confirmed that its MREL (Minimum Requirement for own funds and Eligible Liabilities) requirements are fully covered.

The following chart shows BFF’s capital position relative to regulatory requirements:

Forward-Looking Statements

BFF Bank confirmed its dividend policy, though implementation remains subject to the lifting of the dividend ban by the Bank of Italy. The bank also noted that deposit gathering operations in Greece are expected to be fully operational from June 2025, potentially providing an additional source of funding.

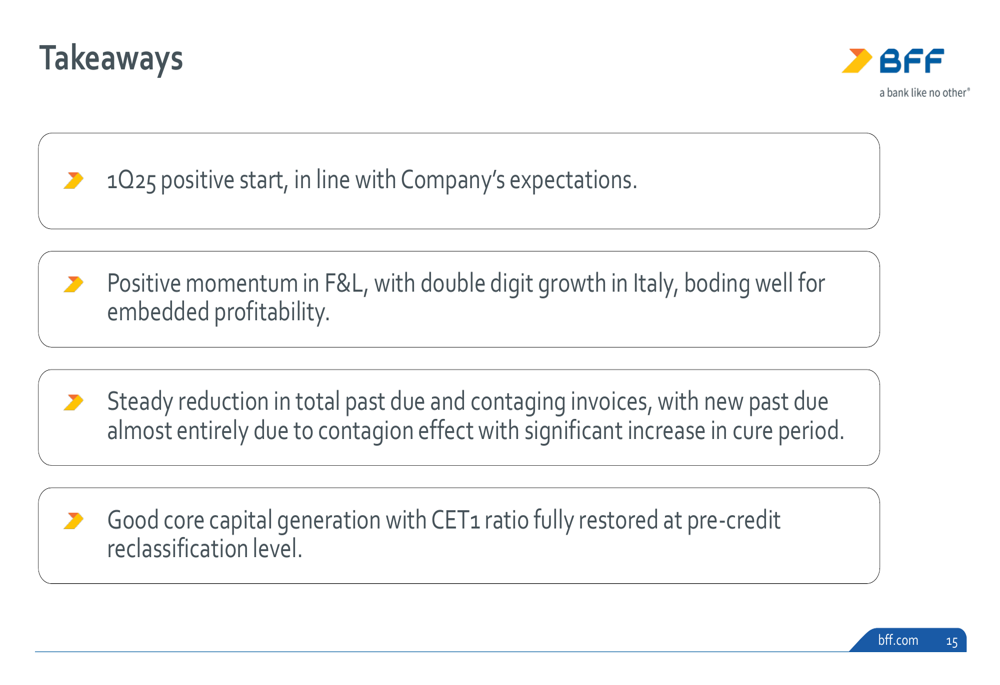

The key takeaways from BFF’s Q1 2025 results presentation highlight the positive start to the year, with momentum in the Factoring & Lending business, steady reduction in past due amounts, and strong capital generation:

BFF’s focus on maintaining a strong capital position while growing its core business segments suggests a cautious but optimistic outlook for the remainder of 2025, particularly if the strong performance in Italy and Poland can offset the weakness in Spain.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.