Bullish indicating open at $55-$60, IPO prices at $37

BioCryst Pharmaceuticals (NASDAQ:BCRX) reported strong second-quarter 2025 results on August 4, with ORLADEYO sales exceeding expectations and the company accelerating its path to profitability. The stock jumped 8.81% in premarket trading following the announcement.

Quarterly Performance Highlights

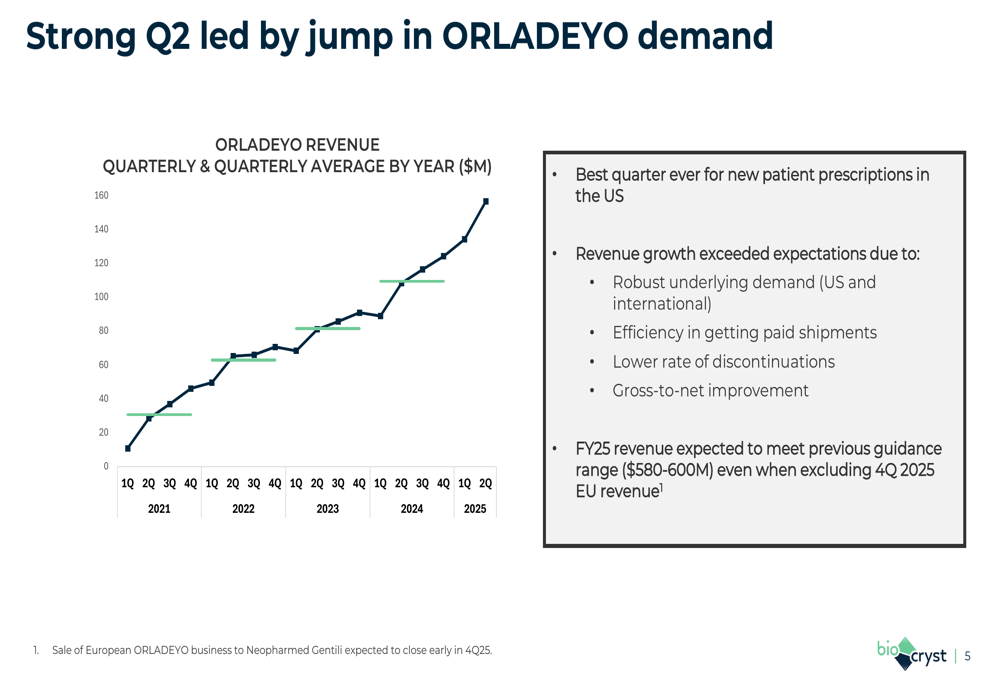

BioCryst delivered robust Q2 2025 performance driven primarily by increased demand for ORLADEYO, its oral treatment for hereditary angioedema (HAE). The company reported that revenue growth exceeded expectations due to robust underlying demand both in the US and internationally, improved efficiency in getting paid shipments, lower rate of discontinuations, and gross-to-net improvement.

The company also achieved its best quarter ever for new patient prescriptions in the US, indicating continued market penetration and adoption of ORLADEYO.

As shown in the following quarterly revenue chart, ORLADEYO has demonstrated consistent growth since its launch:

BioCryst maintained its full-year 2025 revenue guidance of $580-600 million, even when excluding 4Q 2025 EU revenue. This represents a 33-37% growth compared to the previous year, consistent with the guidance provided in their Q1 2025 earnings report.

ORLADEYO Growth and Market Position

Market research presented by BioCryst shows a significant shift in patient preferences toward oral administration for HAE long-term prophylaxis. The percentage of patients preferring oral prophylaxis has increased from 51% in 2023 to 70% in 2025, while preference for injection/infusion has dropped from 30% to just 13% during the same period.

BioCryst’s comprehensive market simulation, which involved 6,000 market interactions between healthcare providers, patients, and payers, projects that ORLADEYO will reach a steady state of over 2,000 patients in the U.S. by 2028, even as new products enter the market.

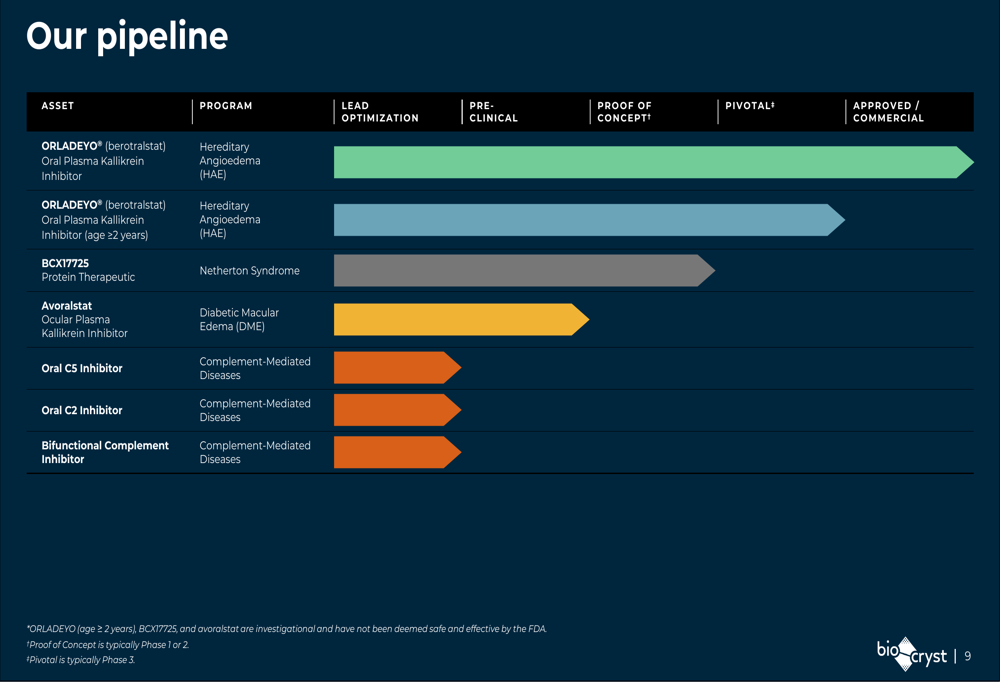

The company’s pipeline includes several promising assets at various stages of development, from lead optimization to commercial phase:

Pipeline Development Updates

A key near-term catalyst for BioCryst is the potential approval of ORLADEYO granules for children ages 2 to 11. Currently, injectable therapies are the only FDA-approved options for this age group. The PDUFA target date is December 12, 2025, with applications also submitted in the EU and Japan.

The company highlighted the development of BCX17725 for Netherton Syndrome, a rare genetic disorder with high unmet need. The diagnosed US population is approximately 1,600 patients, with potential to grow to 3,000-5,000 with greater diagnosis and treatment. The IND has been cleared by the FDA, and Phase 1 trials are underway.

BioCryst is also advancing Avoralstat as a potential treatment for Diabetic Macular Edema (DME), targeting a significant market opportunity of approximately 1.5 million DME patients in the US, with an estimated $4 billion VEGF market by 2028.

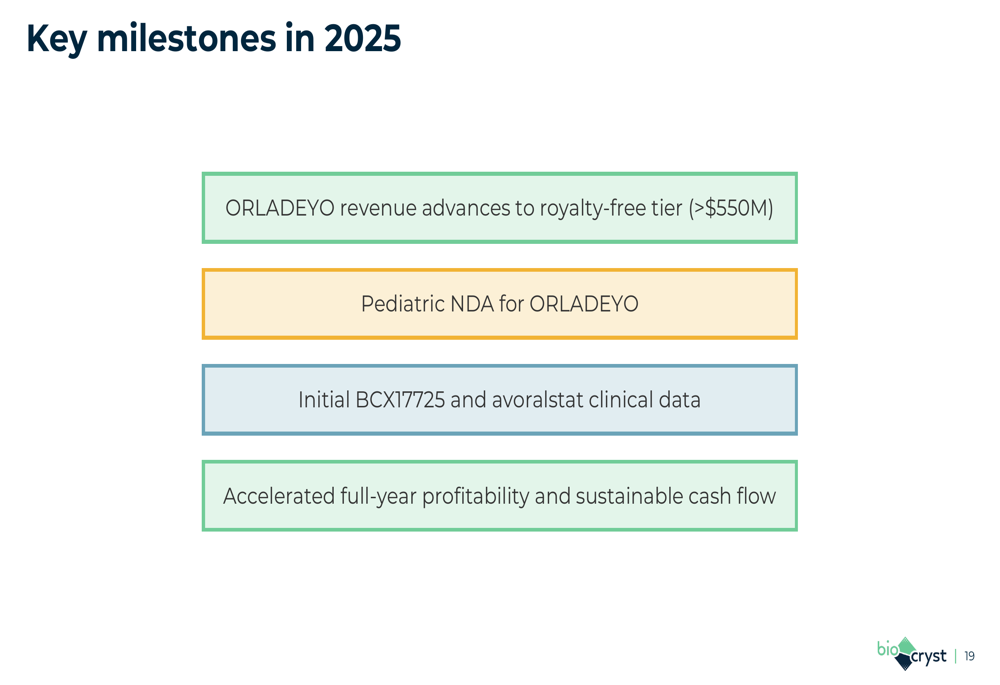

The company outlined several key milestones expected in 2025:

Financial Analysis and Outlook

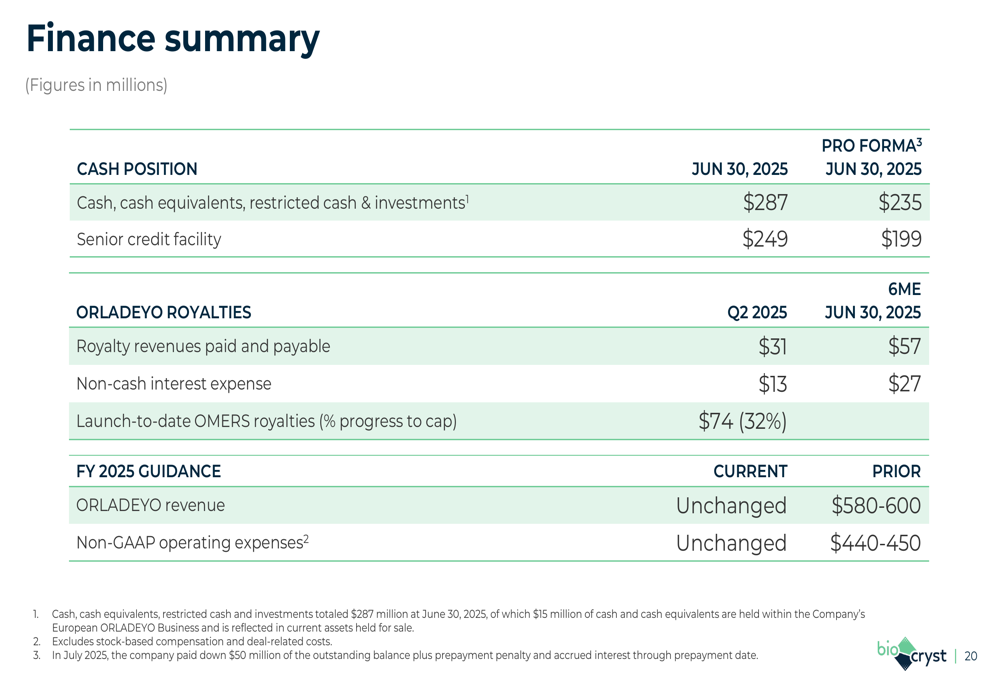

BioCryst’s financial position continues to strengthen, with $287 million in cash, cash equivalents, restricted cash and investments as of June 30, 2025 ($235 million on a pro forma basis). The company reported Q2 2025 ORLADEYO royalty revenues paid and payable of $31 million.

The financial summary presented during the call provides a comprehensive overview of the company’s current position:

Notably, BioCryst has significantly accelerated its path to profitability, expecting full-year operating profit in 2024 (excluding stock-based compensation), positive net income and cash flows in 2025, and meaningful and sustainable cash generation from 2026 onward.

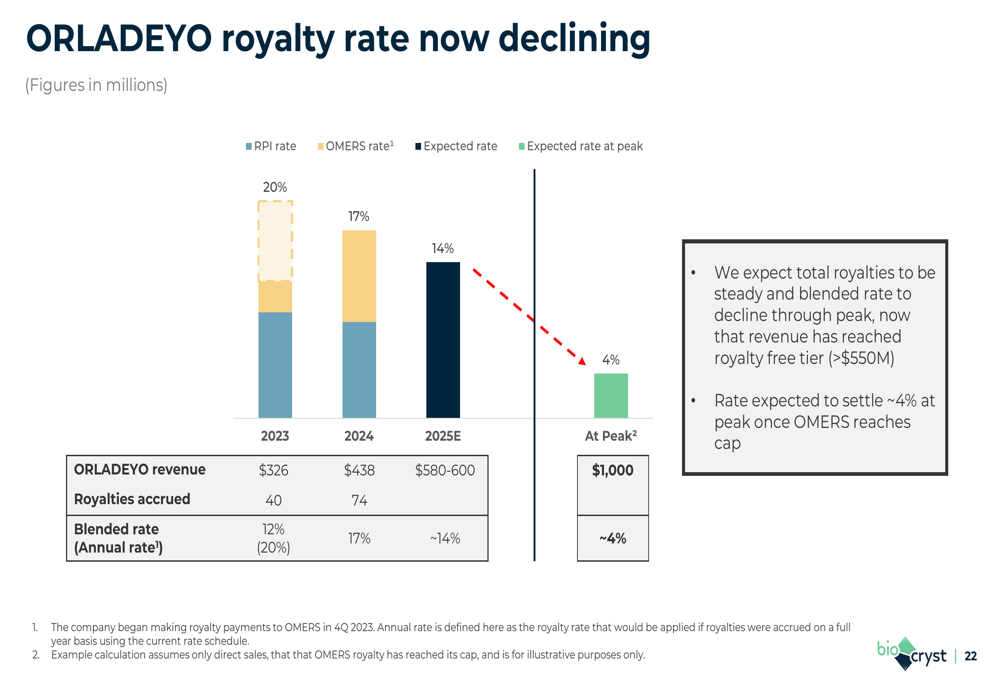

A key financial development is the declining royalty rate for ORLADEYO. As revenue has reached the royalty-free tier (>$550M), the blended royalty rate is expected to decline from 20% in 2023 to 14% in 2025, and eventually settle at approximately 4% at peak:

Forward-Looking Statements

BioCryst’s management expressed confidence in the company’s trajectory, highlighting the strong Q2 performance and accelerated path to profitability. The company maintained its full-year 2025 guidance for ORLADEYO revenue ($580-600 million) and non-GAAP operating expenses ($440-450 million).

The company’s strategy for achieving durable and profitable growth through the current decade emphasizes three key pillars: growing ORLADEYO to $1 billion in peak annual sales, advancing its clinical pipeline with near-term milestones, and achieving financial independence with a near-term path to profitability.

With ORLADEYO revenue now advancing to a royalty-free tier (>$550M), initial clinical data expected from BCX17725 and Avoralstat programs, and accelerated profitability, BioCryst appears well-positioned to deliver on its strategic objectives in 2025 and beyond.

The market’s positive reaction, with shares up 8.81% in premarket trading, suggests investors are optimistic about the company’s strong Q2 performance and improving financial outlook. This follows a 13.77% stock surge after Q1 2025 earnings, indicating continued momentum for BioCryst as it transitions to sustainable profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.