Street Calls of the Week

Introduction & Market Context

Swedish sportswear company Björn Borg AB (STO:BORG) presented its Q1 2025 financial results on May 16, showing record quarterly sales despite facing margin pressures. The company’s stock has experienced volatility recently, declining 3.34% to 57.8 SEK in the latest trading session, positioning it between its 52-week range of 43-67 SEK.

The Q1 results follow a strong performance in Q4 2024, when the company reported 19% growth. The current quarter’s 9% growth rate indicates a moderation in momentum, potentially contributing to recent stock weakness as investors weigh strong sales against margin concerns.

Quarterly Performance Highlights

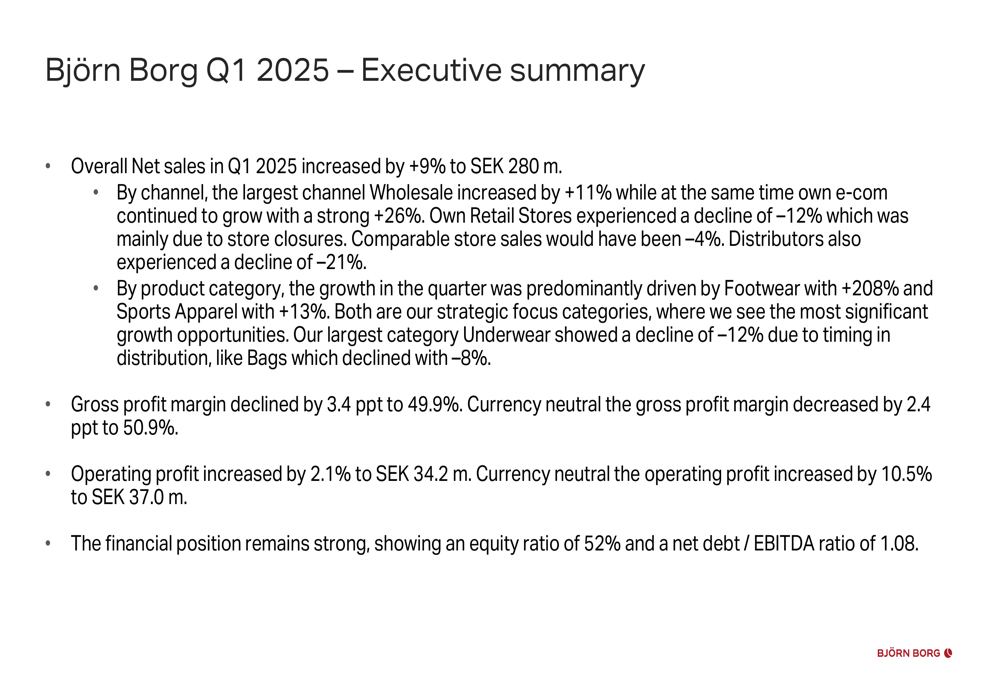

Björn Borg achieved record Q1 sales, with net revenue increasing 9% to SEK 280 million. This growth was primarily driven by extraordinary performance in footwear and continued strength in sportswear.

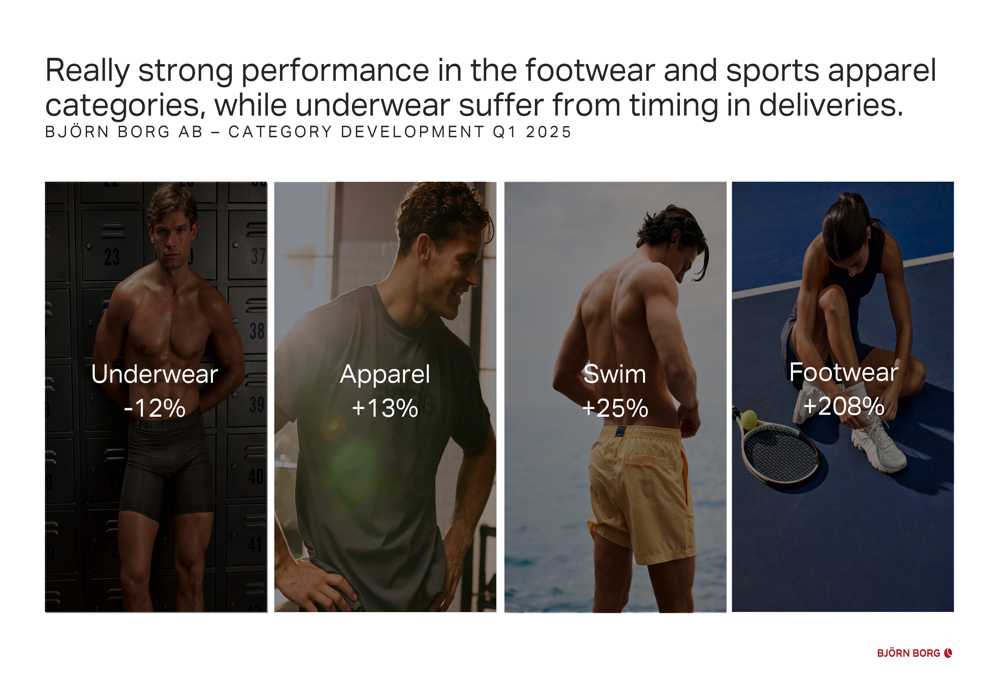

"Overall, it was a record sales quarter, driven primarily by our strategic focus areas: shoes (+208 percent) and sportswear (+13 percent)," said CEO Henrik Bunge (NYSE:BG) in the presentation.

The company’s executive summary highlights the varied performance across channels and product categories:

Channel performance showed strong divergence, with wholesale growing 11% and the company’s own e-commerce channel delivering impressive 26% growth. However, retail stores declined 12% (comparable stores -4%), and distributor sales fell 21%.

The footwear category was the standout performer with extraordinary 208% growth, reflecting successful integration efforts following the company’s strategic focus on this segment. Sports apparel grew 13% and swim products increased 25%, while the core underwear category declined 12%.

Detailed Financial Analysis

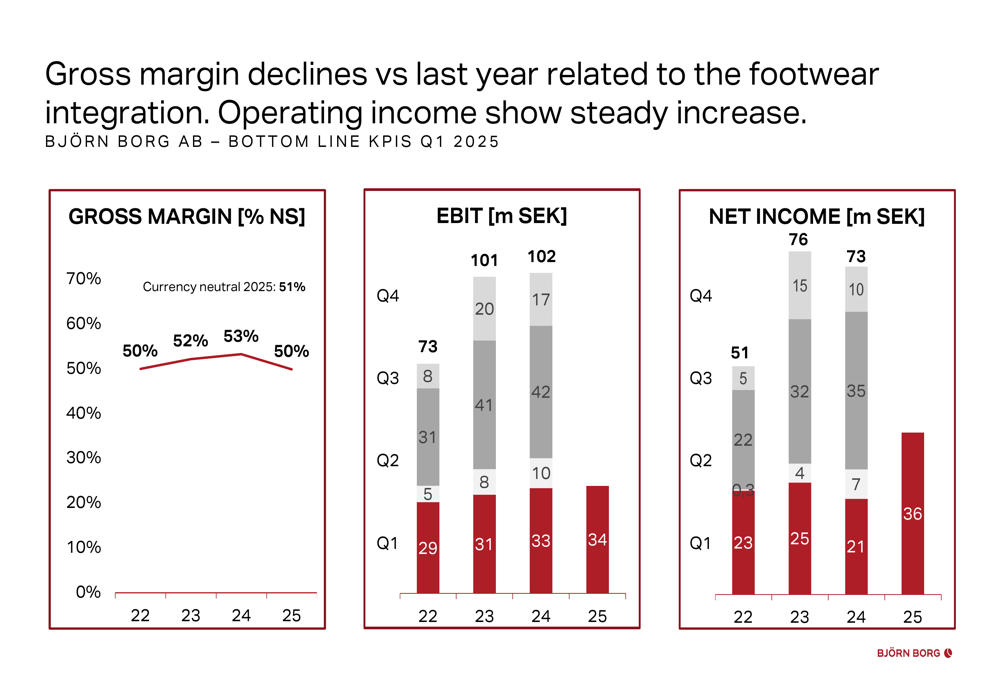

Despite the strong sales growth, Björn Borg faced margin pressures in Q1. Gross profit margin declined by 3.4 percentage points to 49.9% (or 50.9% currency neutral), continuing a downward trend from the 53.3% reported in Q4 2024.

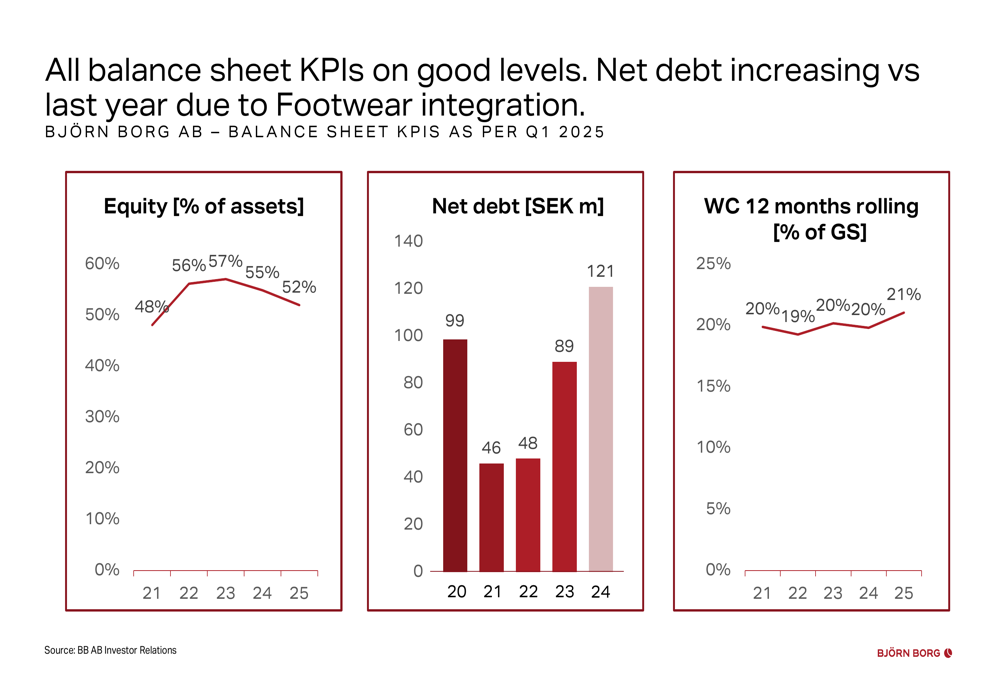

Operating profit increased modestly by 2.1% to SEK 34.2 million, though currency-neutral growth was more substantial at 10.5% (SEK 37.0 million). The company maintained a solid financial position with an equity ratio of 52% and a net debt/EBITDA ratio of 1.08.

The company’s bottom-line performance shows a positive trend in key financial metrics:

Notably, net income saw a significant jump to SEK 36 million in Q1 2025, compared to SEK 21 million in the same period of 2024, representing a 71% increase despite the gross margin pressure.

The balance sheet remains strong, though with some changes in key metrics:

Strategic Initiatives & Brand Development

Björn Borg continues to execute its business strategy focused on increasing online sales, growing sports apparel market share, and expanding geographically across Europe. The company maintains ambitious financial objectives including minimum 10% annual sales growth, 10% operating margin, and 50% dividend of net profit.

Brand awareness metrics show positive momentum, particularly in Germany, which the company identifies as a key growth market despite the 21% sales decline there in Q1. Purchase intention among male consumers increased 61% in Germany compared to Q1 2024.

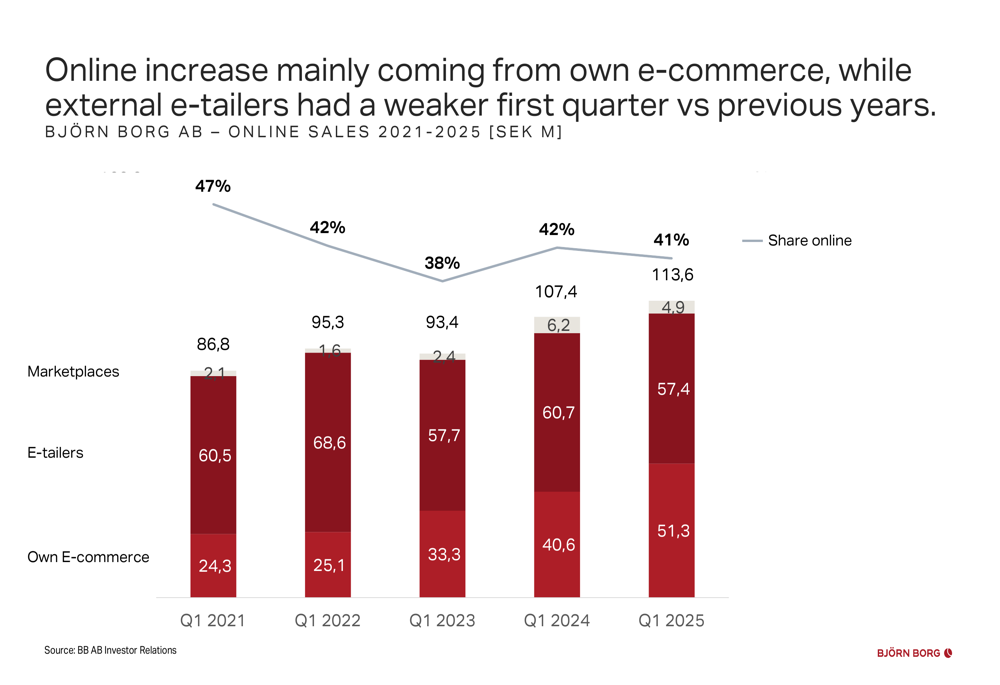

The company’s online strategy continues to evolve, with a clear shift toward direct e-commerce. While the company’s own e-commerce channel grew 26% to SEK 51.3 million, e-tailers declined 6% to SEK 57.4 million. Total (EPA:TTEF) online sales represented 41% of revenue in Q1 2025.

Forward-Looking Statements

Björn Borg highlighted three key takeaways from Q1 2025 that signal its strategic direction:

The company emphasized its commitment to the German market despite current sales challenges, noting significant improvements in brand metrics there. The successful footwear integration remains a central focus, with management indicating this will continue to be a growth driver.

For investors, the company outlined several rationales for investment, including its track record of profitable growth since 2014, stable dividend payments, and identified growth initiatives to support its target of at least 10% annual sales growth.

While the company faces challenges with declining margins and mixed geographical performance, management remains confident in its ability to execute its strategic plan, particularly in growing its online presence and expanding its footwear and sportswear categories.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.